New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

business statistics communicating

Statistics For Business And Economics 10th Edition David R. Anderson, Dennis J. Sweeney, Thomas A. Williams - Solutions

1. Jerry Jeff Keen, the CFO of Boots Unlimited, a Texas corporation, has come to you regarding a potential restructuring of business operations. Boots has long manufactured its western boots in plants in Texas and Oklahoma. Recently, Boots has explored the possibility of setting up a manufacturing

56. LO.6 John McPherson is single, an attorney, and a U.S. citizen. He recently attended a seminar where he learned he could give up his U.S. citizenship, move to Bermuda (where he would pay no income tax), and operate his law practice long distance via the Internet with no U.S. tax consequences.

55. LO.6 Continue with the facts of Problem 54. What are the Federal income tax withholding requirements with respect to Martinho’s sale? Who pays the withheld amount to the U.S. Treasury?

54. LO.6 Martinho is a citizen of Brazil and lives there year-round. He has invested in a plot of Illinois farmland with a tax basis to him of $1 million. Martinho has no other business or investment activities in the United States. He is not subject to the alternative minimum tax. Upon sale of the

53. LO.6 Trace, Ltd., a foreign corporation, operates a trade or business in the United States. Trace’s U.S.-source income effectively connected with this trade or business is$800,000 for the current year. Trace’s current-year E & P is $600,000. Trace’s net U.S. equity was $8.2 million at the

52. LO.6 Clario, S.A., a Peruvian corporation, manufactures furniture in Peru. It sells the furniture to independent distributors in the United States. Because title to the furniture passes to the purchasers in the United States, Clario reports $1 million in U.S.-source income. Clario has no

51. LO.2, 6 IrishCo, a manufacturing corporation resident in Ireland, distributes products through a U.S. office. Current-year taxable income from such sales in the United States is $12 million. IrishCo’s U.S. office deposits working capital funds in short-term certificates of deposit with U.S.

50. LO.5 Money, Inc., a U.S. corporation, has $500,000 to invest overseas. For U.S. tax purposes, any additional gross income earned by Money will be taxed at 34%. Two possibilities for investment are:a. Invest the $500,000 in common stock of Exco (a foreign corporation). Exco common stock pays a

49. LO.5 Collins, Inc., a domestic corporation, operates a manufacturing branch in Singapore.During the current year, the manufacturing branch produces a loss of $300,000. Collins also earns interest income from investments in Europe, where it earns $800,000 in passive income. Collins paid no

48. LO.4, 5 Partin, Inc., a foreign subsidiary of Jones, Inc., a U.S. corporation, has pretax income of 200,000 euros for 2012. Partin accrues 60,000 euros in foreign taxes on this income. The average exchange rate for the tax year to which the taxes relate is 1.35€:$1.None of the income is

47. LO.5 Night, Inc., a domestic corporation, earned $300,000 from foreign manufacturing activities on which it paid $90,000 of foreign income taxes. Night’s foreign sales income is taxed at a 50% foreign tax rate. What amount of foreign sales income can Night earn without generating any excess

46. LO.5 For which of the following foreign income inclusions is a U.S. corporation potentially allowed an indirect FTC under § 902?a. Interest income from a 5% owned foreign corporation.b. Interest income from a 60% owned foreign corporation.c. Dividend income from a 5% owned foreign

45. LO.5 Canteen, Inc., a U.S. corporation, owns 100% of NewGrass, Ltd., a foreign corporation.NewGrass earns only general limitation income. During the current year, New-Grass paid Canteen a $10,000 dividend. The deemed-paid foreign tax credit associated with this dividend is $3,000. The foreign

44. LO.5 Elmwood, Inc., a domestic corporation, owns 15% of Correy, Ltd., a Hong Kong corporation. The remaining 85% of Correy is owned by Fortune Enterprises, a Canadian corporation. At the end of the current year, Correy has $400,000 in undistributed E & P and $200,000 in foreign taxes related to

43. LO.5 Mary, a U.S. citizen, is the sole shareholder of CanCo, a Canadian corporation.During its first year of operations, CanCo earns $14 million of foreign-source taxable income, pays $6 million of Canadian income taxes, and distributes a $2 million dividend to Mary. Can Mary claim a

42. LO.5 ABC, Inc., a domestic corporation, has $50 million of taxable income, including$15 million of general limitation foreign-source taxable income, on which ABC paid $5 million in foreign income taxes. The U.S. tax rate is 35%. What is ABC’s foreign tax credit?

41. LO.5 Dunne, Inc., a U.S. corporation, earned $400,000 in total taxable income, including$50,000 in foreign-source taxable income from its branch manufacturing operations in Brazil and $20,000 in foreign-source income from interest earned on bonds issued by Dutch corporations. Dunne paid $25,000

40. LO.5 Blunt, Inc., a U.S. corporation, earned $600,000 in total taxable income, including$80,000 in foreign-source taxable income from its German branch’s manufacturing operations and $30,000 in foreign-source taxable income from its Swiss branch’s engineering services operations. Blunt paid

39. LO.5 Weather, Inc., a domestic corporation, operates in both Fredonia and the United States. This year, the business generated taxable income of $600,000 from foreign sources and $900,000 from U.S. sources. All of Weather’s foreign-source income is in the general limitation basket.

38. LO.5 Brandy, a U.S. corporation, operates a manufacturing branch in Chad, which does not have an income tax treaty with the United States. Brandy’s worldwide Federal taxable income is $30 million, so it is subject to a 35% marginal tax rate. Profits and taxes in Chad for the current year are

37. LO.5 Round, Inc., a U.S. corporation, owns 80% of the only class of stock of Square, Inc., a CFC. Square is a CFC until May 1 of the current tax year (not a leap year). Round has held the stock since Square was organized and continues to hold it for the entire year.Round and Square are both

36. LO.5 Hart Enterprises, a U.S. corporation, owns 100% of OK, Ltd., an Irish corporation.OK’s gross income for the year is $10 million. Determine OK’s Subpart F income(before any expenses) from the transactions that it reported this year.a. OK received $600,000 from sales of products

35. LO.5 USCo owns 65% of the voting stock of LandCo, a Country X corporation. Terra, an unrelated Country Y corporation, owns the other 35% of LandCo. LandCo owns 100% of the voting stock of OceanCo, a Country Z corporation. Assuming that USCo is a U.S. shareholder, do LandCo and OceanCo meet the

34. LO.5 Beach, Inc., a domestic corporation, operates a branch in Mexico. Over the last 10 years, this branch has generated $50 million in losses. For the last 3 years, however, the branch has been profitable and has earned enough income to entirely offset the prior losses. Most of the assets are

33. LO.4, 5 Teal, Inc., a foreign corporation, pays a dividend to its shareholders on November 30. Red, Inc., a U.S. corporation and 7% shareholder in Teal, receives a dividend of 10,000K (a foreign currency). Pertinent exchange rates are as follows:November 30 .9K:$1 Average for year .7K:$1

32. LO.4 Juarez is a citizen and resident of the United States. He pays all of his living expenses in U.S. dollars. He operates an unincorporated trade or business buying and selling rare books over the Internet to customers in Mexico. All income and expenses of the rare book business are in pesos.

31. LO.4 Table, Inc., a U.S. corporation, operates a manufacturing branch in Mexico and a sales branch in Canada. The Mexican branch uses the peso for all of its activities, and the Canadian branch uses the Canadian dollar for all of its activities. Write a letter to Karen Burns, Table’s tax

30. LO.4 Peck, Inc., a U.S. corporation, purchases weight-lifting equipment for resale from HiDisu, a Japanese corporation, for 75 million yen. On the date of purchase, 75 yen is equal to $1 U.S. (¥75:$1). The purchase is made on December 15, 2012, with payment due in 90 days. Peck is a calendar

29. LO.3 Create, Inc., produces inventory in its foreign manufacturing plants for sale in the United States. Its foreign manufacturing assets have a tax book value of $5 million and a fair market value of $15 million. Its assets related to the sales activity have a tax book value of $2 million and

28. LO.3 USCo incurred $100,000 in interest expense for the current year. The tax book value of USCo’s assets generating foreign-source income is $5 million. The tax book value of USCo’s assets generating U.S.-source income is $45 million. How much of the interest expense is allocated and

27. LO.3 Willa, a U.S. corporation, owns the rights to a patent related to a medical device.Willa licenses the rights to use the patent to IrishCo, which uses the patent in its manufacturing facility located in Ireland. What is the sourcing of the $1 million of royalty income received by Willa from

26. LO.3 Chock, a U.S. corporation, purchases inventory for resale from distributors within the United States and resells this inventory at a $1 million profit to customers outside the United States. Title to the goods passes outside the United States. What is the sourcing of Chock’s inventory

25. LO.3 Determine whether the source of income for the following sales is U.S. or foreign.a. Suarez, an NRA, sells stock in Home Depot, a U.S. corporation, through a broker in San Antonio.b. Chris sells stock in IBM, a U.S. corporation, to her brother, Rich. Both Chris and Rich are NRAs, and the

24. LO.3 Gloria Wang, an NRA, is a professional golfer. She played in seven tournaments in the United States in the current year and earned $200,000 in prizes from these tournaments.She deposited the winnings in a bank account she opened in Mexico City after her first tournament win.Gloria played a

23. LO.3 Madison, a U.S. resident, received the following income items for the current tax year. Identify the source of each income item as either U.S. or foreign.a. $3,000 dividend from U.S. Flower Company, a U.S. corporation, that operates solely in the eastern United States.b. $6,000 dividend

22. LO.4, 5 RedCo, a domestic corporation, incorporates GreenCo, a new wholly owned entity in Germany. Under both German and U.S. legal principles, this entity is a corporation.RedCo faces a 35% U.S. tax rate.GreenCo earns $800,000 in net profits from its German activities and makes no dividend

21. LO.1, 3, 5 If a U.S. taxpayer is subject to U.S. income tax on profits earned outside the United States and such profits are also subject to income tax in the foreign jurisdiction, how does the U.S. taxpayer escape double taxation? Draft a short speech that you will give to your university’s

20. LO.6 Write a memo on the difference between “inbound” and “outbound” activities in the context of U.S. taxation of international income.

19. LO.3, 6 Sloop, Inc., a foreign corporation, sells wireless devices in several countries, including the United States. In fact, currently 25% of Sloop’s sales income is sourced in the United States (through branches in New York and Chicago). Sloop is considering opening additional branches in

18. LO.6 In general terms, how is a non-U.S. person taxed on his or her U.S. business income? Investment income? Ignore the effects of tax treaties in your answer.

17. LO.5 Working with the FTC may involve “baskets” of foreign-source income and deductions. Explain this term.

16. LO.5 Molly, Inc., a domestic corporation, owns 15% of PJ, Inc., and 12% of Emma, Inc., both foreign corporations. Molly is paid gross dividends of $35,000 and $18,000 from PJ and Emma, respectively. PJ withheld and paid more than $10,500 in foreign taxes on the $35,000 dividend.PJ’s country

15. LO.5 Klein, a domestic corporation, receives a $10,000 dividend from ForCo, a wholly owned foreign corporation. The deemed-paid FTC associated with this dividend is $3,000.What is the total gross income included in Klein’s tax return as a result of this dividend?

14. LO.5 QuinnCo could not claim all of the income taxes it paid to Japan as a foreign tax credit (FTC) this year. What computational limit probably kept QuinnCo from taking its full FTC?

13. LO.5 Linker is a corporate entity organized in France. It is owned equally by 100 U.S.shareholders. The shareholders are not related to each other; they purchased the shares from a broker. Is Linker a CFC? Explain.

12. LO.5 Joanna owns 5% of Axel, a foreign corporation. Joanna’s son, Fred, is considering acquiring 15% of Axel from an NRA. The remainder of Axel is owned 27% by unrelated U.S. persons and 53% by unrelated NRAs. Currently, Fred operates (as a sole proprietorship)a manufacturing business that

11. LO.5 Summarize the ownership rules that apply in determining whether a non-U.S. entity is a controlled foreign corporation (CFC) under the U.S. Federal income tax rules.

10. LO.5 Write a memo to a U.S. client explaining why some of the profit it generated from a non-U.S. subsidiary still is included in its U.S. taxable income.

9. LO.5 What are the important concepts to be considered when U.S. assets are transferred outside the country to be used in starting a new business?

8. LO.4 When dealing with the rules concerning gain and loss from foreign currency transactions, the taxpayer must identify its qualified business units (QBUs). What is a QBU? How many QBUs can a business operate?

7. LO.4 Weinke is a business organized in Austria, where the local currency is the euro.Nevertheless, Weinke’s U.S. branch uses the U.S. dollar as its functional currency. How can this be?

6. LO.3 “The IRS can use § 482 to overturn all of the international tax planning that our company is doing.” Explain.

5. LO.3 Write a memo outlining the issues that arise when attempting to source income that is earned from Internet-based activities.

4. LO.3 When is dividend income paid by a non-U.S. entity to a U.S. investor not foreignsource income? Be specific.

3. LO.2 Kelly, a U.S. citizen, earns interest income that is sourced in Germany. How could a U.S. tax treaty with Germany reduce Kelly’s taxes on the interest?

2. LO.1, 5 Liang, a U.S. citizen, owns 100% of ForCo, a foreign corporation not engaged in a U.S. trade or business. Is Liang subject to any U.S. income tax on her dealings with ForCo? Explain.

1. LO.1 “U.S. persons are taxed on their worldwide income.” Explain.

3. Find a state/local tax policy organization (e.g., the Committee on State Taxation). Read its current newsletter. In an e-mail to your instructor, summarize a major article in the newsletter. Look especially for articles on one of these topics:• Judicial and legislative developments concerning

2. Many states offer a tax credit for expenditures made in state for new computing and energy-saving equipment. For your state and one of its neighbors, summarize in a table three of the tax incentives offered through the income, sales, or property tax structure. In your table, list at least the

1. Send an e-mail to the secretary of revenue for your home state proposing adoption of at least two of the following provisions that do not currently exist in your state.a. Increase the apportionment weight for the sales factor.b. Exempt computer and communications technology from the

46. LO.9 Prepare a PowerPoint presentation (maximum of six slides) entitled “Planning Principles for Our Multistate Clients.” The slides will be used to lead a 20-minute discussion with colleagues in the corporate tax department. Keep the outline general, but assume that your colleagues have

45. LO.5, 9 Dread Corporation operates in a high-tax state. The firm asks you for advice on a plan to outsource administrative work done in its home state to independent contractors.This work now costs the company $750,000 in wages and benefits. Dread’s total payroll for the year is $8 million,

44. LO.8 Indicate for each transaction whether a sales (S ) or use (U ) tax applies or whether the transaction is nontaxable (N ). Where the laws vary among states, assume that the most common rules apply. All taxpayers are individuals.a. A resident of State A purchases an automobile in A.b. A

43. LO.8 Using the following information from the books and records of Grande Corporation, determine Grande’s total sales that are subject to State C’s sales tax. Grande operates a retail hardware store.Sales to C consumers, general merchandise $1,100,000 Sales to C consumers, crutches and

42. LO.7 Hernandez, which has been an S corporation since inception, is subject to tax in States Y and Z. On Schedule K of its Federal Form 1120S, Hernandez reported ordinary income of $500,000 from its business, taxable interest income of $10,000, capital loss of $30,000, and $40,000 of dividend

41. LO.6 Chang Corporation is part of a three-corporation unitary business. The group has a water’s edge election in effect with respect to unitary State Q. State B does not apply the unitary concept with respect to its corporate income tax laws. Nor does Despina, a European country to which

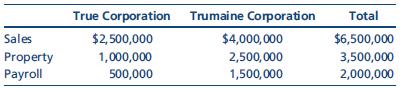

40. LO.6, 9 True Corporation, a wholly owned subsidiary of Trumaine Corporation, generated a $400,000 taxable loss in its first year of operations. True’s activities and sales are restricted to State A, which imposes an 8% income tax. In the same year, Trumaine’s taxable income is $1 million.

39. LO.5, 9 Crate Corporation, a calendar year taxpayer, has established nexus with numerous states. On December 3, Crate sold one of its two facilities in State X. The cost of this facility was $800,000.On January 1, Crate owned property with a cost of $3 million, $1.5 million of which was located

38. LO.5 Assume the same facts as in Problem 37, except that nonbusiness income is apportionable in B.

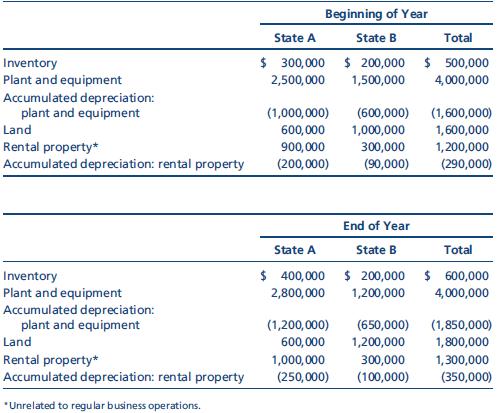

37. LO.5 Kim Corporation, a calendar year taxpayer, has manufacturing facilities in States A and B. A summary of Kim’s property holdings follows.Determine Kim’s property factors for the two states assuming that the statutes of both A and B provide that average historical cost of business

36. LO.5, 9 Quinn Corporation is subject to tax in States G, H, and I. Quinn’s compensation expense includes the following:Officers’ salaries are included in the payroll factor for G and I, but not for H. Compute Quinn’s payroll factors for G, H, and I. Comment on your results. State G State

35. LO.5, 9 State E applies a throwback rule to sales, while State F does not. State G has not adopted an income tax to date. Orange Corporation, headquartered in E, reported the following sales for the year. All of the goods were shipped from Orange’s E manufacturing facilities. Determine its

34. LO.5 McKay Corporation operates in two states, as indicated below. This year’s operations generated $300,000 of apportionable income.Compute McKay’s State A taxable income assuming that State A apportions income based on a:a. Three-factor formula, equally weighted.b. Double-weighted sales

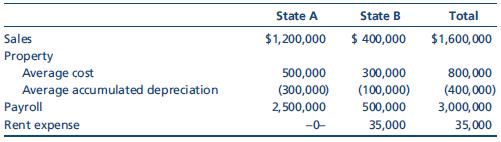

33. LO.5 Assume the same facts as in Problem 31, except that both states employ a threefactor formula, under which sales are double-weighted. The basis of the property factor in A is historical cost, while the basis of this factor in B is the net depreciated basis. Neither A nor B includes rent

32. LO.5 Assume the same facts as in Problem 31, except that A uses a single-factor apportionment formula that consists solely of sales and B uses a three-factor apportionment formula that equally weights sales, property (at historical cost), and payroll. State B does not include rent payments in

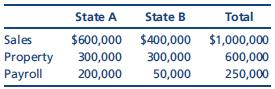

31. LO.5 Dillman Corporation has nexus in States A and B. Dillman’s activities for the year are summarized below.Determine the apportionment factors for A and B assuming that A uses a three-factor apportionment formula under which sales, property (net depreciated basis), and payroll are equally

30. LO.1 Flip Corporation is subject to tax only in State X. Flip generated the following income and deductions. State income taxes are not deductible for X income tax purposes.Sales $4,000,000 Cost of sales 2,800,000 State X income tax expense 200,000 Depreciation allowed for Federal tax purposes

29. LO.1 Perk Corporation is subject to tax only in State A. Perk generated the following income and deductions.Federal taxable income $300,000 State A income tax expense 15,000 Refund of State A income tax 3,000 Depreciation allowed for Federal tax purposes 200,000 Depreciation allowed for state

28. LO.1 For each of the following independent cases, indicate whether the circumstances call for an addition modification (A), a subtraction modification (S), or no modification(N) in computing state taxable income. Then indicate the amount of any modification.The starting point in computing State

27. LO.1 Use Figure 24.1 to provide the required information for Warbler Corporation, whose Federal taxable income totals $10 million.Warbler apportions 60% of its business income to State C. Warbler generates$3 million of nonbusiness income each year, and 20% of that income is allocated to C.

26. LO.1 Use Figure 24.1 to compute Balboa Corporation’s State F taxable income for the year.Addition modifications $29,000 Allocated income (total) 25,000 Allocated income (State F) 3,000 Allocated income (State G) 22,000 Tax credits 800 Federal taxable income 90,000 Subtraction modifications

25. LO.9 As the director of the multistate tax planning department of a consulting firm, you are developing a brochure to highlight the services it can provide. Part of the brochure is a list of five or so key techniques that clients can use to reduce state income tax liabilities. Develop this list

24. LO.2, 9 Your client, Ecru Limited, is considering an expansion of its sales operations, but it fears adverse resulting tax consequences. Write a memo for the tax research file identifying the planning opportunities presented by the ability of a corporation to terminate or create income tax

23. LO.9 Your client, HillTop, is a retailer of women’s clothing. It has increased sales during the holiday season by advertising gift cards for in-store and online use. HillTop has found that gift card holders who come into the store tend to purchase goods that total more than the amount of the

22. LO.8 List three or more taxes, other than the income and sales/use tax, that a state or local jurisdiction might levy.

21. LO.8 Create a PowerPoint outline describing the major exemptions and exclusions from the sales/use tax base of most states. Use your slides to discuss this topic with your accounting students’ club.

20. LO.8 HernandezCo wants to avoid the creation of sales/use tax nexus with State G.The HernandezCo sales representatives believe that they will lose customers because of an increase in their products’ prices due to the new tax obligations. Are the sales representatives correct to be concerned

19. LO.7 The Quail LLC operates solely in State W. As a pass-through entity, Quail does not pay any W taxes. Evaluate this statement.

18. LO.7 Chip and Dale are the only shareholders of VisitTime, a medical transportation firm that is organized as an S corporation. VisitTime makes quarterly estimated income tax payments, related to Chip’s stock ownership, to State Q, its headquarters state.Explain.

17. LO.6 Carmina operates a multinational business from Colorado, a state that applies the unitary theory and requires combined state income tax reporting. Most of her off-shore customers are located in the United Kingdom and Germany, where sales prices and property valuations are relatively high.

16. LO.6 Your client makes the comment, “Unitary corporate income taxation is a bad idea for the business community.” Is her characterization correct? Elaborate.

15. LO.6 State A enjoys a prosperous economy, with high real estate values and compensation levels. State B’s economy has seen better days—property values are depressed, and unemployment is higher than in other states. Most consumer goods are priced at about 10% less in B than in A. Both A and

14. LO.6 The trend in state income taxation is for states to adopt a version of the unitary theory of multijurisdictional taxation in their statutes and regulations.a. Explain why some states are attracted to the unitary theory and a combined reporting scheme of multistate income taxation.b. Is the

13. LO.5 Keystone, your tax consulting client, is considering an expansion program that would entail the construction of a new logistics center in State Q. List at least five questions you should ask in determining whether an asset that is owned by Keystone is to be included in State Q’s property

12. LO.5 Megan is a telecommuter and works most days from her home in Tennessee.Twice a month, she travels to Georgia for a staff meeting at the Atlanta headquarters. In which state’s payroll factor should Megan’s compensation be included if:a. Megan is an employee and is covered by the

11. LO.5 Continue with the facts of Question 10. Another large shipment was made in May to a customer in South Dakota, a state that does not impose any corporate income tax.Is this sale to be included in SpillCo’s Iowa sales factor? Explain.

10. LO.5 In computing the corporate income taxes for Iowa-based SpillCo, should a single large sale in August, in which merchandise was shipped to a customer in Kentucky, be included in the Iowa sales factor?

9. LO.3 The trend in state income taxation is to move from an equal three-factor apportionment formula to a formula that places extra weight on the sales factor. Several states now use sales-factor-only apportionment. Explain why this development is attractive to the taxing states.

8. LO.3 Regarding the apportionment formula used to compute state taxable income, does each of the following independent characterizations describe a taxpayer that is based in state or out of state? Explain.a. The sales factor is positively correlated with the payroll, but not the property,

7. LO.3 Indicate whether each of the following items should be allocated or apportioned by the taxpayer in computing state corporate taxable income. Assume that the state follows the general rules of UDITPA.a. Profits from sales activities.b. Gain on the sale of a plot of land held by a real estate

Showing 700 - 800

of 7675

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers