New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

cost accounting

Cost Accounting 4th Edition Jawahar Lal, Seema Srivastava - Solutions

Discuss the information which a well-designed cost report should give to management from the point of view of production and control. How should such information be given?

What is a two variance analysis of factory overheads. Give a brief description.

Explain the term variance and distinguish between controllable and uncontrollable variances.

Describe briefly the managerial use of variances.

Point out the difference between historical costing and standard costing.

In analysing variance it is found frequently that an adverse variance from one standard is related directly to a favourable variance from another. Give two examples of such a situation and comment briefly on each.

Distinguish between standard costs and budgeted costs.

What is sales value volume variance?

Define variance analysis. What are the ways of disposing cost variances?

What is fixed production overhead variance? Explain how this is calculated and further analysed.

Distinguish between budgetary control and standard costing.

Explain fixed overhead cost variance.

In analysing variance, it is found frequently that an adverse variance from one standard is related directly to a favourable variance from another.Give two examples of such a situation and comment briefly on each.

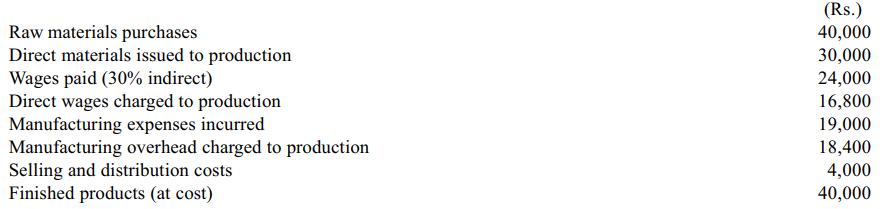

Journalise the following transactions assuming cost and financial accounts are integrated: Raw materials purchases Direct materials issued to production Wages paid (30% indirect) Direct wages charged to production Manufacturing expenses incurred Manufacturing overhead charged to production Selling

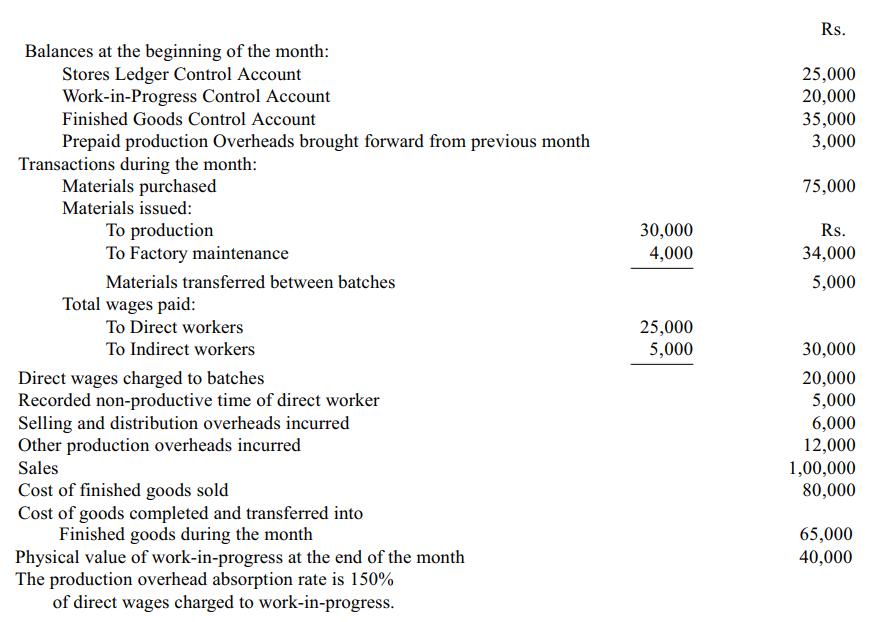

In the absence of the Chief Accountant, you have been asked to prepare a months cost accounts for a company which operate a batch costing system fully integrated with the financial accounts. The following relevant information is provided to you:Required: Prepare the following accounts for the

From the following particulars pass the journal entries in an integral accounting system:(a). Issued materials Rs. 3,00,000/- of which Rs. 2,80,000 (standard Rs 2,40,000) is direct material. (b). Net wages paid Rs. 70,000/-, Deductions being Rs. 12,000/- (standard Rs. 75,000/-) (c). Gross

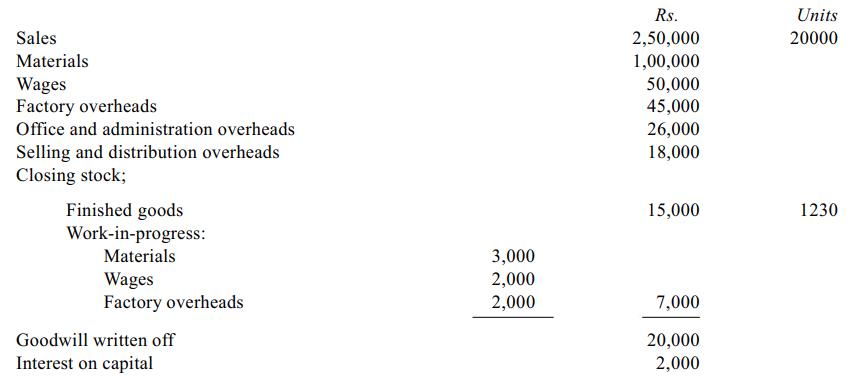

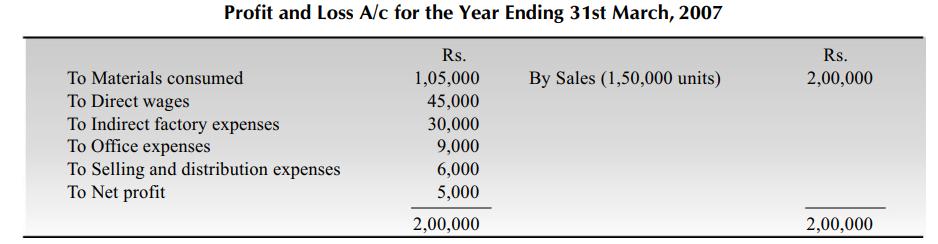

The following transactions have been extracted from the financial books of a company: In costing books factory overhead is charged at 100% on wages, administration overhead at 10% of factory cost and selling and distribution at the rate of Re 1 per unit sold. Prepare a statement reconciling the

Explain the need for reconciliation of cost and financial accounts.

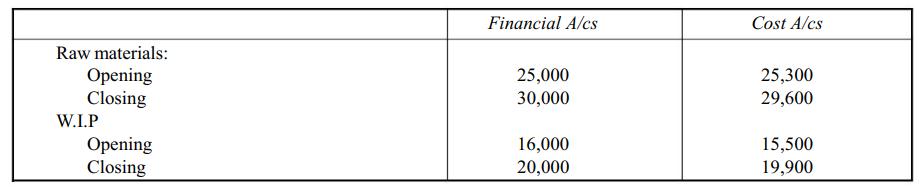

Prepare a Reconciliation Account from the following details: Profit as per cost accounts were of Rs. 59,700 while the profits as per financial accounts were of Rs. 60,000. The values of opening and closing stock as shown in cost accounts and financial accounts were as under: Raw

From the following figures prepare reconciliation statement: Profit as per costing records Factory overheads under-recovered in costing Selling and Administration overheads over-recovered in costing Bank interest credited in financial books Preliminary expenses written off in financial

The following figure are available from financial accounts for the year ending 31st March, 2002: Factory overhead recovered at 20% on prime cost. Administration overhead at Rs. 3 per unit of production. Selling and distribution overhead at Rs 4 per unit sold.Prepare:1. Costing profit and loss

It has been stated that the results worked out from the costing records and those worked out from the financial accounts may not necessarily agree. Why?

During the year a companys profits have been estimated from the costing system to be Rs. 46,126, whereas the financial accounts audited by the auditors disclose a profit of Rs. 33,248. Given the following information, you are required to prepare a reconciliation statement showing clearly the

Give reasons as to why it is necessary to reconcile cost accounts and financial accounts. What is the accounting procedure to be adopted for their reconciliation?

From the following information, reconcile the profit as per cost accounts with financial accounts:Dividend and interest received Rs. 600. Loss on sale of investments Rs. 1,000. Interest charged by the bank not considered in Financial Accounts and Cost Accounts Rs. 1,500. Goodwill written off

From the information given below, prepare (i). A statement showing costing profit and loss.(ii). Another statement reconciling the costing profits with those shown by financial accounts:The normal output of the factory is 1,00,000 units. Factory expenses of a fixed nature are Rs. 18,000. Office

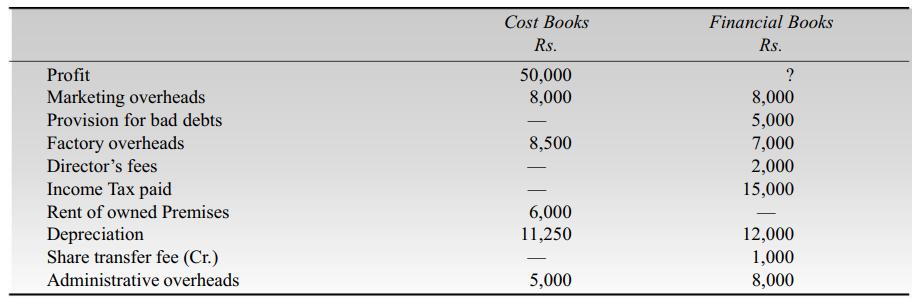

From the following figure, prepare a reconciliation statement: Profit Marketing overheads Provision for bad debts Factory overheads Director's fees Income Tax paid Rent of owned Premises Depreciation Share transfer fee (Cr.) Administrative overheads Cost

Indicate the reasons why it is necessary for the cost and financial accounts of an organisation to be reconciled and explain the main sources of difference which would enter into such a reconciliation.

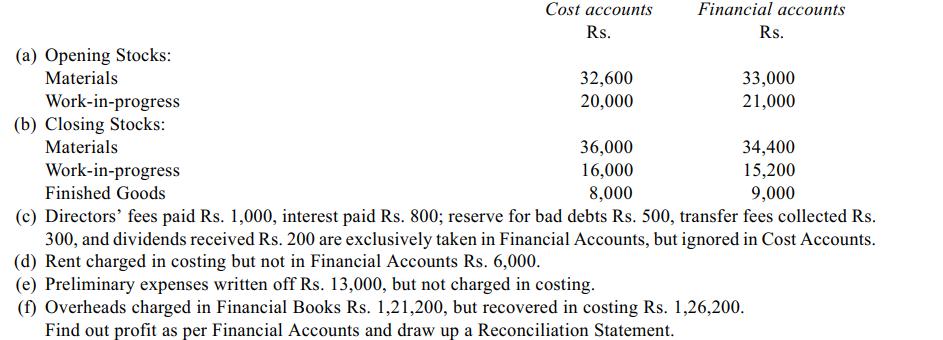

The profit as per cost accounts is Rs. 1,65,300. The following details are ascertained on comparison of the Cost and Financial Accounts. (a) Opening Stocks: Materials Work-in-progress (b) Closing Stocks: Materials Cost accounts Rs. 32,600 20,000 36,000 16,000 8,000 Financial

Discuss the main sources of difference between profit shown by financial accounts and profit shown by cost accounts.

Describe in brief the conditions which necessitate reconciliation of financial and cost records.

Gain More Ltd. showed a net loss of Rs. 6,30,000 as per the financial accounts for the year ended 31st March, 2004. The cost accounts however disclosed a loss of Rs. 5,00,000 for the same period. On scrutiny of the two accounts the following are available: Factory overheads

What is a reconciliation statement?. Give reasones for the difference in profit as per cost accounts and financial accounts.

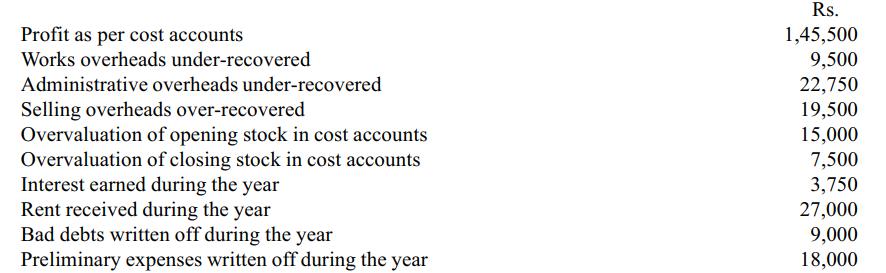

From the following data prepare a Reconciliation Statement: Profit as per cost accounts Works overheads under-recovered Administrative overheads under-recovered Selling overheads over-recovered Overvaluation of opening stock in cost accounts Overvaluation of closing stock in cost accounts Interest

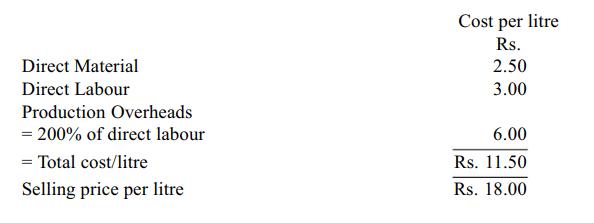

The profit and loss account of Oil India (Pvt) Ltd. for the year ended 31st March, 2003, is as follows:As per the cost records the direct expenses have been estimated at a cost of Rs. 30 per kg and administration expenses at Rs. 15 per kg. The profit as per the costing records are Rs. 1,10,400.

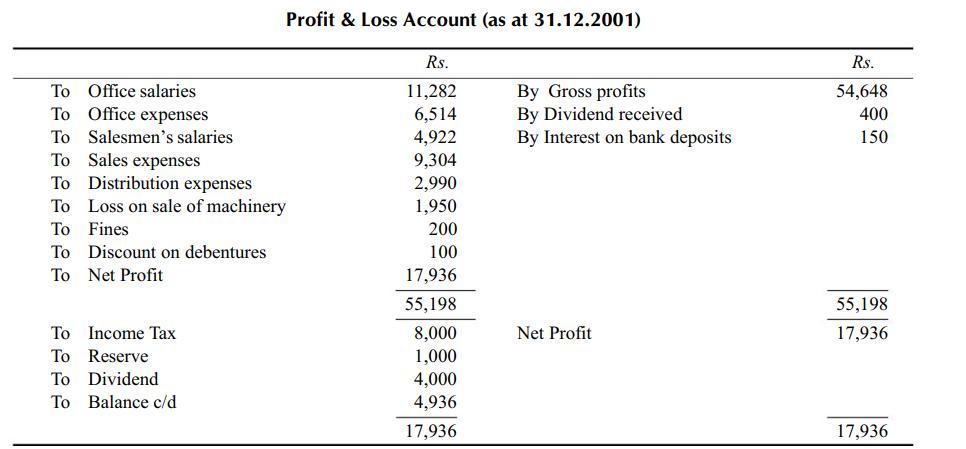

From the following Profit and Loss Account, draw up a Memorandum Reconciliation Account, showing the Profit as per cost accounts: The cost accountant of the company has ascertained a profit of Rs. 19,936 as per his books. To Office salaries To Office expenses Profit & Loss Account (as at

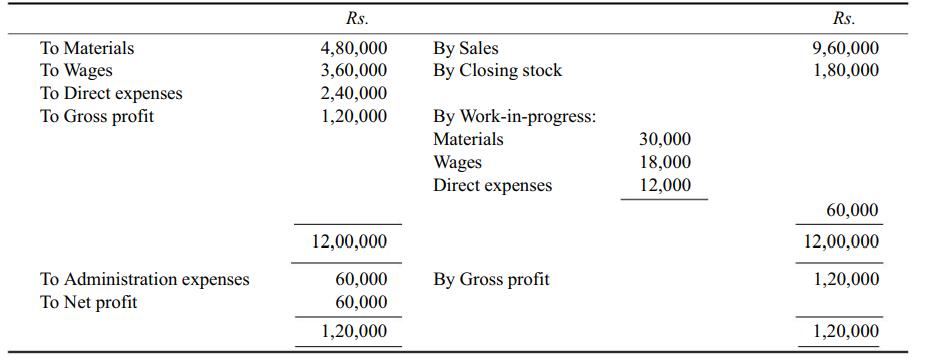

Hind General Corporation produces only one product which had the following costs. The normal capacity is set at 200,000 units. There are no work-in-progress inventories. In 2001, the company produced 200000 units and sold 90 per cent of them at a price of Rs. 7 per unit. In 2002, the company

What do you mean by marginal costing? Discuss its usefulness and limitations.

The following cost information relates to factory for two years. Work out the profit under absorption costing and marginal costing for the two years. Also state any abnormality in the results disclosed by absorption costing. Assume FIFO basis. Installed capacity (units) Opening stock

To obtain the break-even point in rupee sales value, total fixed costs are divided by: (a). Variable cost per unit; (b). Contribution margin per unit; (c). Fixed cost per unit; (d). Profit/volume ratio.

Write a lucid note on marginal costing indicating its effect on profit computations.

The break-even point is the point at which: (a). There is no profit, no loss; (b). Contribution margin is equal to total fixed cost; (c). Total revenue is equal to total cost; (d). All of the above.

What are the most important areas of management decisions opened up by the application of the marginal (direct) costing method?

Stock, production and sales data for Industrial Detergents Ltd. are given below: The company has a single product, for which the financial data, based on an activity level of 60,000 litres per period, are as follows: Administrative overheads are fixed at Rs. 1,00,000 per period and half of the

The primary difference between a fixed budget and a variable (flexible) budget is that a fixed budget: (a). Includes only fixed costs, while a variable budget includes only variable costs. (b). Is concerned with only further acquisitions of fixed costs, while a variable budget is concerned with

Marginal costs reveal the lowest price at which a product can be sold during a trade depression, but they also reveal to management the most profitable lines during the period of intense trade activity. Explain with examples, the second part of this statement.

Margin of safety is referred to as: (a). Excess of actual sales over fixed expenses;(b). Excess of actual sales over variable expenses; (c). Excess of actual sales over break-even sales; (d). Excess of budgeted sales over fixed costs.

Discuss the following terms in relation to marginal costing.(a). Key factor, (b). P/V ratio,(c). Margin of safety.

Profit/Volume Ratio of a company is 50%, while its margin of safety is 40%. If sales volume of the company is Rs. 50 lakhs, find out its break-even point and net profit.

(a). What do you understand by the term margin of safety with reference to volume of production?(b). How do the following reflect on a break-even volume and on a P/V ratio; (i). Increase in total fixed cost;(ii). Increase in total physical sales; (iii). Decrease in variable costs per unit.

Total fixed cost Rs. 12,000, Actual sales Rs. 48,000, Margin of safety Rs. 8,000. Determine the P/V ratio.

X Ltd. has earned contribution of Rs. 2,00,000 and net profit of Rs. 1,50,000 on sales Rs. 8,00,000. What is its margin of safety?

What do you understand by the term break-even analysis? Enumerate its uses.

When output is 3,000 units, the average cost per unit is Rs. 4. When output is increased to 4000 units, the average cost is Rs. 3.50 per unit. The break-even point is 5,000 units. Find the P/V ratio.

How do income statements prepared under the absorption costing and marginal costing concepts differ?

Contribution margin is known as (a). Marginal income (b). Gross profit (c). Net income (d). Net profit

Compared with absorption costing when will variable costing report lower profits, higher profits, the same profits?

The break-even analysis may be described as (a). Comparison between production and sales.(b). Comparison to make out capacity utilisation. (c). Comparison between target set and actual achievement.(d). Comparison between sales and costs.

The profit volume ratio of X Ltd. is 50% and the margin of safety is 40%. You are required to calculate the net profit if the sales volume is Rs. 1,00,000.

In what ways is variable costing better adapted to managerial use in profit planning, decision-making and control?

B & Co. has recorded the following data in the two most recent periods:What is the best estimate of the firms fixed costs per period? Total Cost of Production (Rs.) 14,600 19,400 Volume of Production (units) 800 1,200

An increase in sales price.(a). Does not affect the break-even point.(b). Lowers the net profit. (c). Increases, the break-even point.(d). Lowers the break-even point.

Why do the supporters of marginal costing state that fixed costs are not to be included in inventories?

Profit under traditional costing and marginal costing system will be the same if.(a). There are no opening and closing stocks. (b). There is opening stock and no closing stock. (c). There is closing stock and no opening stock.(d). There are opening and closing stocks.

Discuss the uses of CVP analysis and its significance to management.

In classifying a particular cost as fixed or variable, the volume or activity level is extremely important." Discuss and illustrate this statement.

Fixed cost per unit decrease when (a). Production volume increases.(b). Production volume decreases. (c). Variable costs per unit decreases. (d). Prime costs per unit decreases.

The contribution approach is the foundation of CVP logic and related techniques. Discuss.

Indian Plastics make plastic buckets. An analysis of their accounting reveals: Required: (i). Find the break-even point. (ii). Find the number of buckets to be sold to get a profit of Rs. 30,000. (iii). If the company can manufacture 600 buckets more per year with an additional fixed cost of

Within a relevant range, the amount of variable costs per unit.(a). Differs at each production level.(b). Remains constant at each production level (c). Increases as production increases.(d). Decreases as production increases.

Discuss the role of contribution in marginal costing in decisions relating to fixation of selling price.

Margin of safety is referred to as.(a). Excess of budgeted or actual sales over the variable expenses and fixed expense, at break-even. (b). Excess of budgeted or actual sales revenue over the fixed expenses. (c). Excess of actual sales over budgeted sales. (d). Excess of sales revenue over the

The most useful information derived from a break-even chart is the (a). Amount of sales revenue needed to cover variable costs. (b). Amount of sales revenue needed to cover fixed costs. (c). Relationship among revenues, variable costs and fixed costs at various levels of activity. (d). Volume

State with reasons whether the following propositions are correct.(a). In an undertaking with a high fixed cost, break-even point can be attained at a lower level of activity. (b). Profit is represented by the product of the margin of safety and the P/V ratio.(c). In relation to normal sales, a

An enthusiastic marketing manager suggests to his managing director that only if he is permitted to reduce the selling price of a product by 20%, he would be able to achieve a 30% increase in sales volume. The managing director, finding that the sales volume increase exceeds in percentage the

Each of the following would affect the break-even point except a change in the.(a). Number of units sold (b). Variable cost per unit (c). Total fixed costs (d). Sales price per unit.

Cadbury Schweppes Limited, a British chocolate and soft drink company, is planning to establish a subsidiary company in India to produce, Schweppes Mineral Water. Based on the estimated annual sales of 40,000 bottles of the mineral water, cost studies produced the following estimates for the

Under marginal costing system, the contribution margin discloses the excess of.(a). Revenue over fixed costs (b). Projected revenues over the break-even point (c). Revenues over variable costs (d). Variable costs over fixed costs.

Enumerate the factors which can change the break-even point.

The method of cost accounting that lends itself to break-even analysis is.(a). Variable (Marginal) (b). Standard (c). Absolute (d). Absorption

Triple X company produces these products with the following characteristics: Total fixed costs for the company are Rs. 12,40,000. Assuming that the product mix would be the same at the break-even point, compute the break-even point in:(a). Unit (total and by product line). (b). Sales Rupees

Marginal costing rewards sales whereas absorption costing rewards production. Comment.

Cost volume profit analysis allows management to determine relative profitability of a product by.(a). Highlighting potential bottlenecks in the production process. (b). Keeping fixed costs to an absolute minimum. (c). Determining contribution margin per unit and projected profits at various

Absorption costing obscures the total amount of fixed costs whereas variable costing highlights it Comment.

The following figures are available from the records of Venus Enterprises as at 31st March: Calculate: (a). The P/V ratio and total fixed expenses; (b). The break-even level of sales: (c). Sales required to earn a profit of Rs. 90 lakhs; (d). Profit or loss that would arise if the sales were

Two manufacturing companies which have the following operating details decide to merge. Assuming that the proposal is implemented, calculate: (i). Break-even sales of the merged plant and the capacity utilisation at that stage. (ii). Profitability of the merged plant at 80% capacity

Mention some possible courses of action to improve profit-volume ratio.

Given the following notations, what is the break-even sales in rupees? (a) (c) SP FC + VC FC VC + SP (b) (d) VC SP - FC FC (SP - VC) + SP

What is meant by cost-volume-profit analysis? How CVP analysis is useful for the management?

Company A and Company B, both under the same management, make and sell the same type of product. Their budgeted profit and loss accounts for January June 2002 are as under:You are required to.(i). Calculate the break-even point for each company. (ii). Calculate the sales volume at which each of

What is the term that means all manufacturing costs (direct and indirect, variable and fixed) which contribute to the production of the product and are traced to output and inventories.(a). Job-order costing. (b). Process costing (c). Full or absorption costing (d). Variable or marginal or

Tractors Ltd. have an installed capacity of 5000 tractors per annum. They are presently operating at about 35% of installed capacity. For the coming year, they have budgeted as follows: Factory expenses as well as selling expenses are variable to the extent of 20%. Calculate the break-even

Mention the basic assumption made for 'Break-even Analysis' and examine how far they are valid.

What costs are treated as product costs under variable (marginal) costing? (a). Only direct costs.(b). Only variable production costs. (c). All variable costs.(d). All variable and fixed manufacturing costs.

From, the following data, which product would you recommend for manufacture in the factory? Total machine hours available in the factory are 60000. Per unit of Standard manufacturing time Direct materials Direct labour @ Rs. 10 per hour Variable over head @ Rs. 6 per hour Selling price Product A 2

What is profit-volume graph? Explain how it is drawn? What are its important limitations?

Discuss the importance of fixed and variable costs for decision making at project stage and at operations stage.

Calculate the effect on profit of a proposed change in Sales Mix from the following data: Existing sales mix Sales (in Rs.) Variable cost (in Rs.) Fixed cost (in Rs.) Proposed sales mix M 80,000 48,000 Rs.

Distinguish between marginal costing and absorption costing.

SV Ltd., a multi-product company furnishes you the following data relating to the year 2005: Assuming that there is no change in prices and variable cost and that the fixed expenses are incurred equally in the two half year periods, calculate for the year 2005: (i). The P/V ratio (ii). Fixed

Showing 6000 - 6100

of 6579

First

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

Step by Step Answers