New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

cost accounting

Cost Accounting 4th Edition Jawahar Lal, Seema Srivastava - Solutions

Calculate the estimated cost of production of by-products X and Y at the point of separation from the main product.Selling expenses amount to 25% of total works cost, that is, including both pre-separation and post-separation work cost.Selling prices are arrived at by adding 20% of total cost, that

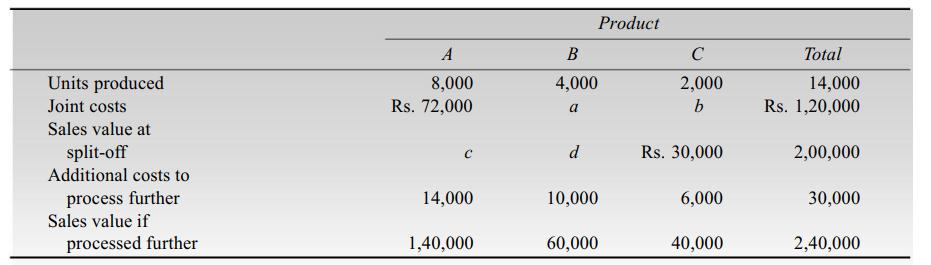

A company manufactures products A, B, and C from a joint process. Additional data are as follows:Derive the values for the lettered spaces. Units produced Joint costs Sales value at split-off Additional costs to process further Sales value if processed further A 8,000 Rs.

What do you understand by operating costing? In what industries is this costing applied?

A Truck starts with a load of 10 tonnes of goods from station P. It unloads 4 tonnes at station Q and rest of the goods at station R. It reaches back directly to station P after getting reloaded with 8 tonnes of goods at station R. The distances between P to Q, Q to R and then from R to P are 40

Write notes on.(i). Transport-costing (ii). Power house costing(iii). Canteen costing.

Distinguish between operating costing and operation costing.

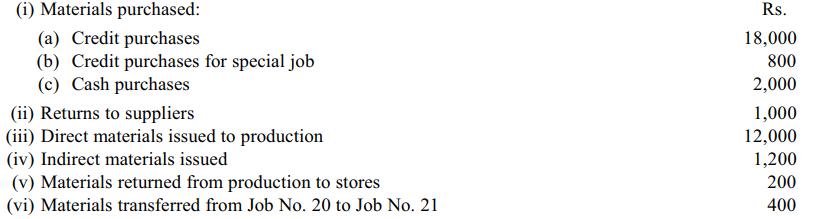

During June 2007, the following transactions took place in XYZ Co. Ltd. You are required to enter the transactions in the financial and cost books. (i) Materials purchased: (a) Credit purchases (b) Credit purchases for special job (c) Cash purchases (ii) Returns to suppliers (iii) Direct

What is non-integral accounting system?

The following figures have been extracted from the cost records of a manufacturing unit: Finished products: Entire output is sold at a profit of 10% on actual cost from work-in-progress. Other wages incurred Rs. 70,000; overhead incurred Rs. 2,50,000. Items not included in Cost Records: Income

What are cost control accounts? Describe their advantages?

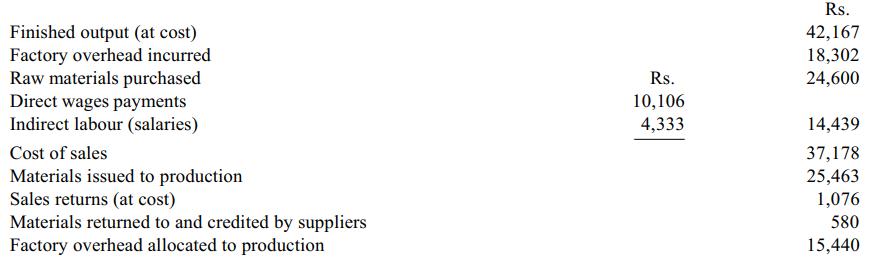

As at 31st March, the following balances existed in a companys cost ledger:During the next three months the following items arose: You are required to write up the accounts and schedule the closing balances, stating what each balance represents. Raw materials control A/c Work-in-progress

The cost ledger of a company shows the following balances as on January 1, 2007. Work-in-progress control A/c Finished stock ledger control A/c Works overhead suspense A/c Office and administration overhead suspense A/c Dr. Rs. 7,840 5,860 400 200 10,500 Cr Stores ledger control A/c General

Mention the principal ledgers maintained in financial accounts and cost accounts.

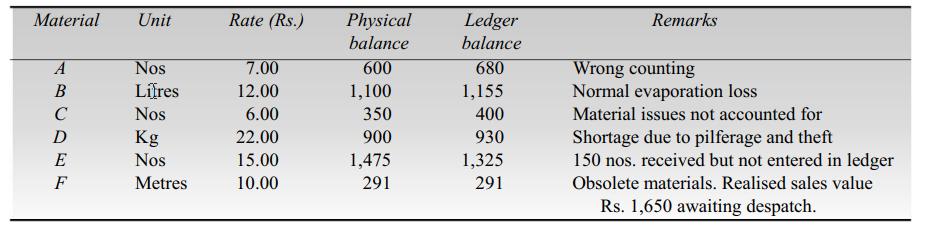

In the course of physical verification of stores as on 31st March 2007, following differences are revealed in case of AB Ltd.Prepare journal entries in the cost ledger to give effect to the above adjustments as called for. Material Unit A B C D E F Nos Lifres Nos Kg Nos Metres Rate

What do you understand by integrated accounts, and what are the principles involved? State the advantages of Integrated accounts.

What is an integrated accounting? State its advantages.

What do you understand by the integrated accounting system? State its advantages and prerequisites.

Distinguish between Interlocking and Integration System of cost and financial accounts?

Explain the accounts kept in Integrated Accounting System.

State the advantages of integrated cost and financial accounts.

Explain the basic requirements of an Integrated System of Accounting.

What is integrated accounting? Briefly describe the merits of integration.

Discuss the distinguishing features of a process cost system?

M/s Indu Industries Ltd. are the manufacturers of moonlight torches. The following data relate to manufacture of torches during the month of March 2007:Prepare Cost Sheet showing the cost and the profit per unit and the total profit earned. Raw material consumed Direct wages Machine-hour

Explain the nature of single costing.

The following details have been obtained from the cost records of Comet Paints Limited: Prepare a production account giving the maximum possible break-up of costs and profit. Stock of raw materials on Sept. 1, 2007 Stock of raw materials on Sept. 30, 2007 Direct wages Indirect

Describe briefly the procedure of presenting costs under single costing. Explain giving an example.

The Managing Director of a small manufacturing concern consults you as to the minimum price at which he can sell the output of one of the departments of the company which is intended for mass production in future. The companys records show the following particulars for this department for the past

The following is the summarised Trading and Profit and Loss A/c of K. Waterproof Manufactures, Ltd., for the year ending 31st march, 2007 in which year 800 waterproofs were sold by the said company.Following estimates were made by the costing department of the company for the year ending 31st

Explain the nature of operation costing.

Baluja Shoe Company manufactures two types of shoes A and B. Production costs for the year ended 31st December 2008 were as follows:There was no work-in-progress at the beginning or at the end of the year. It is ascertained that:(i). The cost of direct materials in type A shoes is twice as much as

Meera Industries Limited is a single product organisation having a manufacturing capacity of 6,000 units per week of 48 hours. The output data vis-à-vis different elements of cost for three consecutive weeks are as follows:As a cost accountant, you are asked by the company management to work out

The following information for the year ended 31st December, 2008 is obtained from the books and records of a factory:Factory overheads are 80% of wages. Office overheads are 25% of factory cost and selling distribution overheads are 10% of cost of production. The complete jobs realised Rs.

In a manufacturing company, a product passes through 5 operations. The output of the 5th operation becomes the finished product. The input, rejection, output and labour and overheads of each operation for a period are as under:You are required to: (i). Determine the input required in each

Xavier company manufactures many products. Each product passes through two production departments, which have the following cost structures: (a). Calculate the unit cost of each of these jobs on a full costing basis. (b). Recalculate unit costs on a variable costing basis. (c). Why

The following information for the year ending December 31, 2001 is obtained from the books and records of a factory:(i). Consolidated completed jobs acount,(ii). Consolidated work-in-progress account. Raw materials supplied from stores Wages Chargeable expenses Materials transferred to

(i). What is the nature of job costing? How are the costs recorded on job orders? (ii). Explain the meaning of contract costing and batch costing.

Which of the following production activities would be most likely to employ job order costing? (a). Ship building (b). Candy manufacturing (c). Toy manufacturing (d). Crude oil refining

Indicate how you would deal with the following items: (a). Plant and machinery pruchased and used on contract work. (b). Amounts received from contractee. (c). Materials lying unused at site.

A factory uses a job costing system. The following data are available form the books at the year ending 31st March 2002. Required:(a). Prepare a cost sheet indicating the prime cost, works cost, production cost, cost of sales and sales value. (b). In 200203, the factory has received an

In job-order costing, the basic document to accumulate and ascertain the cost of each order is the.(a). Purchase order (b). Requisition sheet (c). Invoice (d). Job cost sheet

Honesty Engineering Works has a machining shop in which it manufactures two auto parts, P1 and P2 out of forging F1 and F2. For the quarter ending December 2003, following cost data are available:You are given following further information: (a). Production and sale of P1 and P2 were as

(i). Discuss the implications of cost-plus contracts from the viewpoint of:(a). Manufacturer (b). Customer(ii). What is the relevance of the escalation clause provided in a contract?

Which of the following will not be used in job-order costing? (a). Standards. (b). Marginal costing. (c). Averaging of direct labour and material rates. (d). Factory overhead allocation based on direct labour. hours applied to the job.

Describe briefly the nature of accounting problems associated with job costing.

Engineers Ltd. undertook several contracts during the year 2001. The following information relate to contract No. 107: The contract took 13 weeks on its completion. The values of loose tools and stores returned at the end of the period were Rs. 200 and Rs. 3,000 respectively. The plant was

A manufacturing company has an installed capacity of 1,20,000 units per annum. The cost structure of the product manufactured is an under: The capacity utilisation for the next year is estimated at 60% for 2 months, 75% for 6 months and 80% for the balance part of the year. If the company is

How will you treat profit on incomplete contracts in cost accounts?

The following is the summarised information relating to contract accounts number 100: Included in the above information are wages Rs. 3,500, materials Rs. 4,000 and other expenses Rs. 2,500 which were incurred since certification. Depreciate plant at 10%. Prepare contract A/c. Contract

What do you understand by cost-plus contract and Escalation clause in contract costing?

ABC Ltd. began to trade on 1st January, 2006. During 2006 the company was engaged on only one contract of which the contract price was Rs. 5,00,000. Of the plant and materials charged to the contract, plant which cost Rs. 5,000 and materials which cost Rs. 4,000 were lost in an accident. On 31st

Explain the following: (i). Notional profit in contract costing. (ii). Retention money in contract costing.

Compute a conservative estimate of profit on a contract (which is 80% complete) from the following particulars. Illustrate at least four methods of computing the profit: (i) Total expenditure to date (ii) Estimated further expenditure to complete the contract (including contingencies) (iii)

Discuss the process of estimating profit/loss on incomplete contracts.

A contractor commenced work on a particular contract on 1st April, 2001. He closes the books of accounts for the year on 31st December of each year. The following information is revealed from his costing records on 31st December, 2001. A machine costing Rs. 30,000 remained in use on site for

SV construction Ltd. have obtained a contract for construction of a bridge. The value of the contract is Rs. 12 lakhs and the work commenced on 1st October, 2001. The following details are shown in their books for the year ending 30th September 2002.Life of plant purchased is 5 years and scrap

Kapoor Engineering Company undertakes a long-term contract which involves the fabrication of prestressed concrete blocks and the erection of the same on consumer's site. The following is supplied regarding the contract which is incomplete on 31st March, 2001. Cost incurred:You are required to

Pioneer Construction Company Ltd. obtained a contract for the erection of a multi-storey building. Building operations started in July 2001. The contract price was Rs. 9,00,000. On 30th June 2002, the end of the financial year, the cash received on account was Rs. 3,60,000, being 80% of the amount

A contractor has entered into a long-term contract at an agreed price of Rs. 1,75,000 subject to an escalation clause for materials and wages as spelt out in the contract and corresponding actual are as follows:Reckoning the full actual consumption of materials and wages, the company has claimed a

The following information relates to a building contract for Rs. 10,00,000. The value of plant at the end of 2001 and 2002 was Rs. 7,000 and Rs. 5,000 respectively. Prepare: (i). The contract account,(ii). Contractee account for two years 2001 and 2002 taking into consideration such

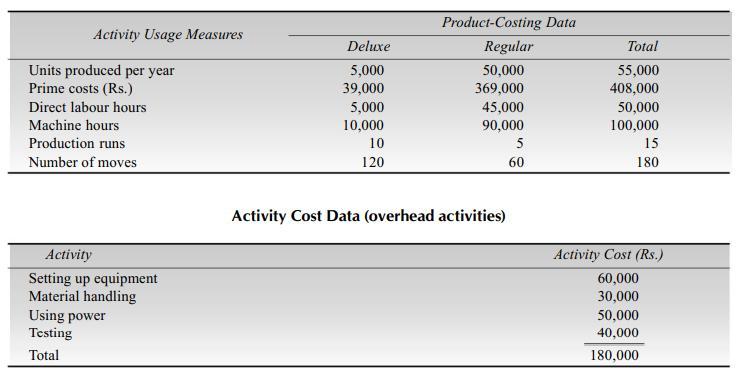

ABC Company produces two types of stereo units. Activity data follows: Required: (i). Calculate the consumption ratios for each activity. (ii). Group activities based on the consumption ratios and activity level. (iii). Calculate a rate for each pooled group of

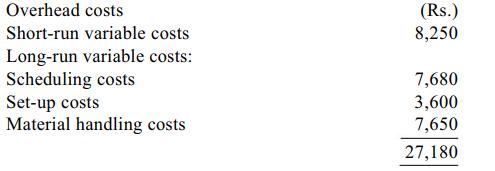

ABC company has been incurring two types of overhead costs-material handling and quality inspection. The costs expected for these categories for the coming year are as follows: The company currently charges overhead using direct labour hours and expected actual capacity. This figure is 50,000

What is Activity-Based Costing? Why is it needed?

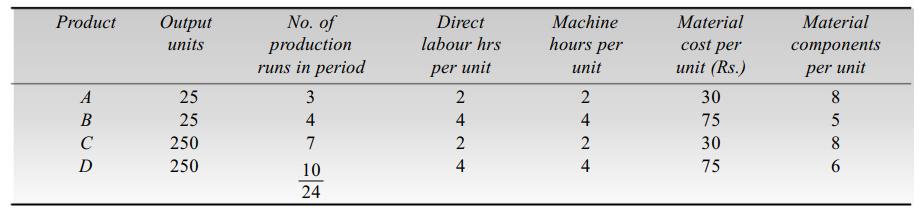

Assume that firm makes four products A, B, C and D. Data for the past period are as follows: Direct labour costs Rs. 7 per hour: Find the unit production cost.(a). Using conventional product costing using a labour hour or machine hour overhead absorption rate. (b). Using ABC with the

What is a cost driver? What is the role of cost driver in tracing costs to products?

Explain the steps in applying Activity-Based Costing (ABC) in a manufacturing Company.

How are activities grouped in a manufacturing company?

Distinguish between activity-based costing and traditional costing system.

Define unit level activities, batch level activities, product level activities and facility level activities.

Overhead costs are source of product cost distortion. Do you agree, Explain.

Explain the concept of Activity-Based Costing and Cost Drivers.

Explain briefly each of the following categories in Activity-Based Costing (ABC) by giving at least two examples:(i). Unit level activities (ii). Batch level activities (iii). Product level activities (iv) Facility level activities

Define Activity-Based management (ABM). What is its importance?

Describe the prime cost method of absorption of factory overheads. Explain fully and illustrate the basic conditions necessary for its application.

In a factory, overheads of a particular department are recovered on the basis of Rs. 5 per machine hour. The total expenses incurred and the actual machine hours for the department for the month of August were Rs. 80,000 and 10,000 hours, respectively. Of the amount of Rs. 80,000, Rs. 15,000 became

The level of production activity fluctuates widely in your company from month to month. Because of this the incidence of depreciation on unit cost varies considerably. The management decides that you find out a suitable method to correct this.

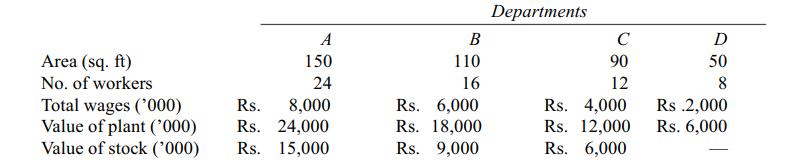

The Moden Company has four departments. A, B and C are the production departments and D is a servicing department. The actual cost for a period are as follows:The following data are also available in respect of four departments: Apportion the above costs to the various departments on the

In a manufacturing company where costing is done with a view to fix prices, state whether and, if so, to what extent the following items are included in cost.(i). Interest on borrowings. (ii). Bonus and gratuity (iii). Depreciation on plant and machinery.

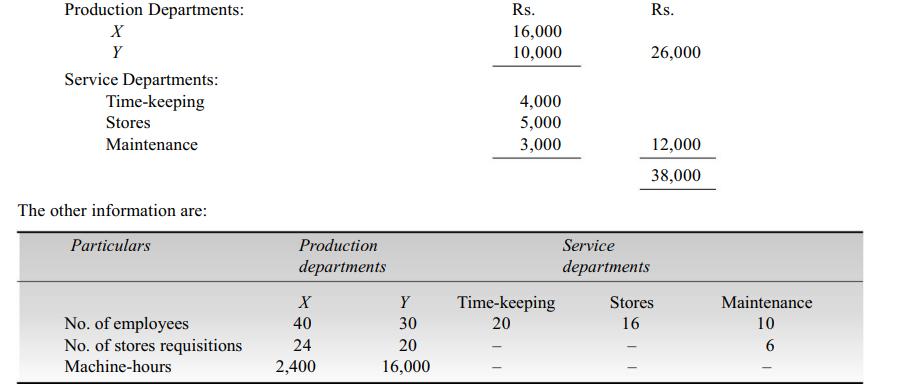

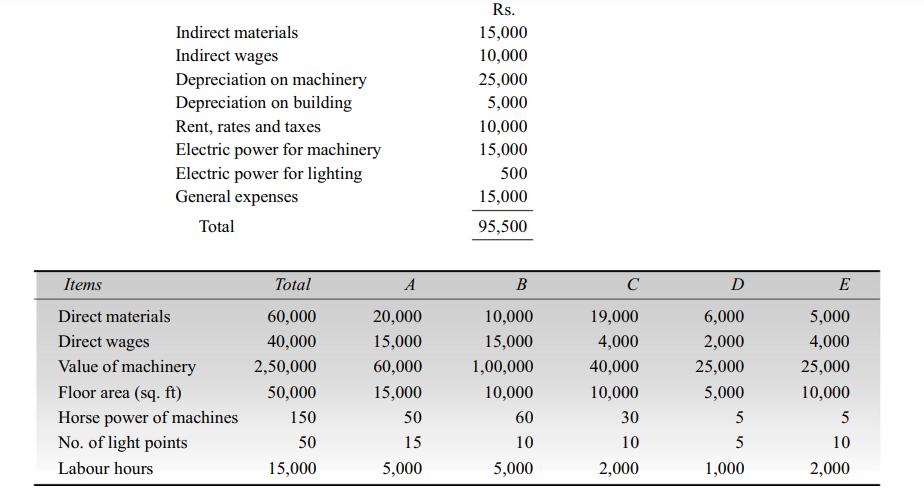

A manufacturing company has 2 production departments X and Y and 3 service departments Time keeping, Stores and Maintenance. The departmental summary showed the following expenses for October 2001.You are required to make departmental allocation of expenses. Production

Deccan Manufacturing Ltd. have three departments which are regarded as production departments. Service departments, costs are distributed to these production departments using the Step Ladder Method of distribution. Estimates of factory overhead costs to be incurred by each department in the

Factory overhead includes (a). All manufacturing costs (b). All manufacturing costs except direct materials and direct labour (c). Indirect materials but not indirect labour (d). Indirect labour but not indirect materials.

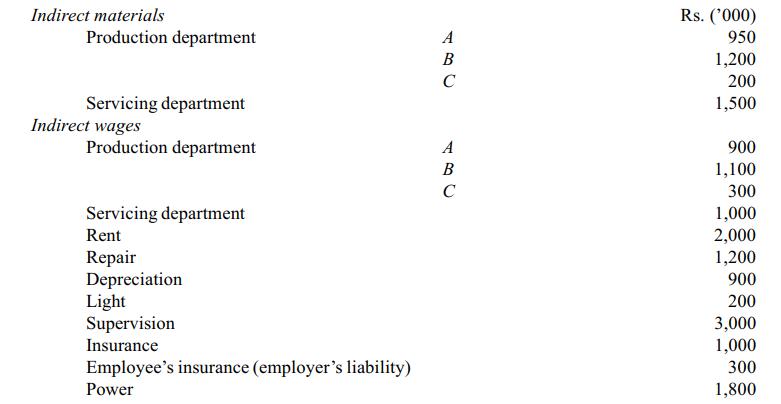

The overhead of a manufacturing company has been analysed to the point of primary distribution as given below.The canteen is to be apportioned on the basis of employees: The powerhouse is to be apportioned on the basis of electricity used: Production departments: Service

In order to identify costs that relate to a specific product, an allocation base should be chosen that (a). Does not have a cause and effect relationship (b). Has a cause and effect relationship (c). Considers variable costs but not fixed costs (d). Considers direct materials

Explain the general principles to be kept in mind while considering whether item of expenditure is to be treated as overhead.

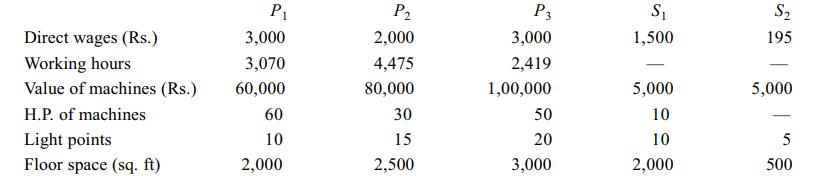

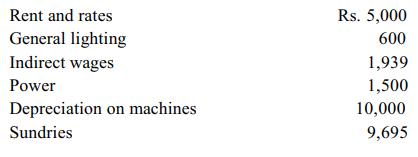

Modern Manufacturers Ltd. has three Production Departments P1, P2, P3 and two Service Departments S1 and S2 the details pertaining to which are as under:The following figures extracted from accounting records are relevant: The expenses of the Services Departments are allocated as under:Find

Differentiate between apportionment and absorption of overhead.

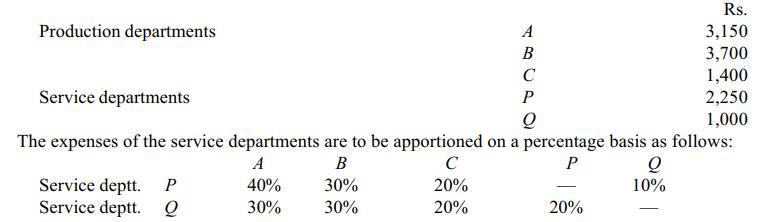

A company has three production departments, A, B and C and two service departments, P and Q. The following figures are available as per departmental distribution summary: Production departments A B C P Service departments Q The expenses of the service departments are to be apportioned on a

What is the importance of machine hour as a basis for the absorption of factory overheads?

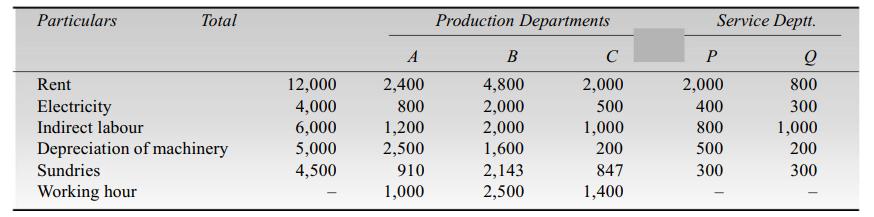

You are supplied with the following information and required to work out the production hour rate of recovery of overheads in Departments A, B and C. Expenses of Service Department P and Q are apportioned as under: Particulars Rent Electricity Indirect labour Total Depreciation of

Explain briefly various methods of absorption of factory overheads.

Added cost of a new product will be (a). Materials and labour (b). Materials, labour and factory overhead (c). Materials, labour, factory and administrative overhead (d). Materials, labour and administrative overhead.

Modern Machines Ltd. have three Production Departments (A, B and C) and two Service Departments (D and E). From the following figures extracted from the records of the company, calculate the overhead rate per labour hour: The expenses of Service Department D and E are to be apportioned as

What do you mean by over-absorption and under-absorption of overheads? How would you treat such over and under absorbed factory-overheads in cost accounts?

The rent of business premises should be shared out between cost centres according to: (a). Floor area or cubic capacity. (b). The number of employees. (c). The replacement value of machinery and equipment.(d). The number of kilowatt hours.

The budgeted fixed overheads amounted to Rs. 84,000. The budgeted and actual production amounted to 20,000 units and 24,000 units respectively. This means that there will be: (a). An under-absorption of Rs. 16,800.(b). An under-absorption of Rs. 14,000. (c). An over-absorption of Rs.

Distinguish between allocation, apportionment and absorption of overheads.

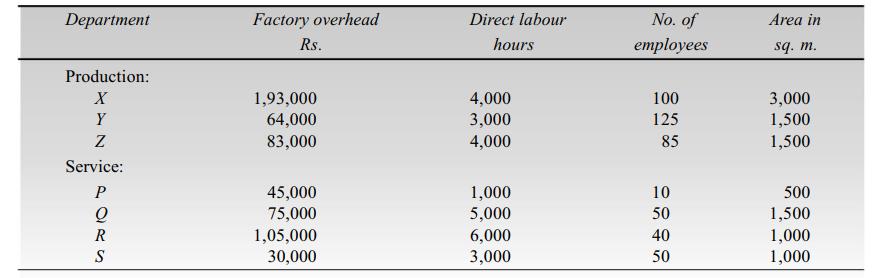

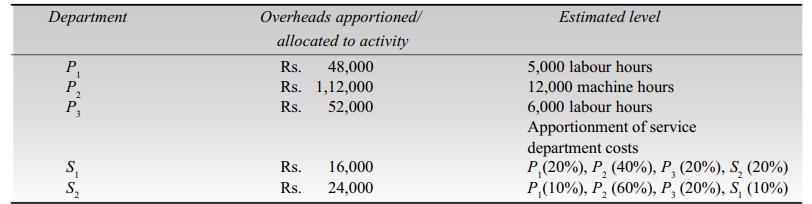

A factory has three production departments (P1, P2 and P3) and two service departments (S1 and S2). Budgeted overheads for the next year have been allocated/apportioned by the cost department among the five departments. The secondary distribution of service department overheads is pending and the

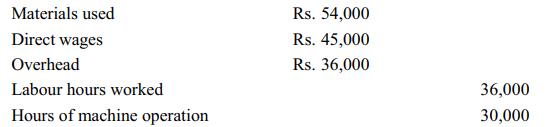

The production department of a factory furnishes the following information for the month of October: For an order executed by the department during the period, the relevant information was as under:Calculate the overhead charges chargeable to the job by the following methods; (i). Direct

What are the requisites of a good method of absorption of factory overhead?

The insurance of buildings is best apportioned to cost centres using: (a). Floor area or cubic capacity (b). The number of employees (c). The replacement value of machinery and equipment (d). The number of kilowatt hours.

Showing 6200 - 6300

of 6579

First

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

Step by Step Answers