New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

cost accounting

Cost Accounting 4th Edition Jawahar Lal, Seema Srivastava - Solutions

A factory has three production departments A, B and C and also two service departments X and Y. The primary distribution of the estimated overheads in the factory has just been completed. These details and the quantum of service rendered by the service departments, to the other departments are

Explain how would you treat under/overabsorption of overheads in cost accounts.

Discuss the secondary distribution of overheads.

The canteen expenses should be apportioned to cost centres by: (a). Floor area or cubic capacity (b). The number of employees (c). The replacement value of machinery and equipment (d). The number of kilowatt hours

Describe the different bases on which factory expenses can be apportioned. Describe the merits and suitability of each of them.

Write a detailed critical note on the direct labour cost method of absorption of factory overheads.

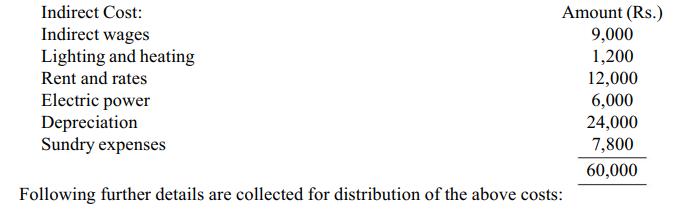

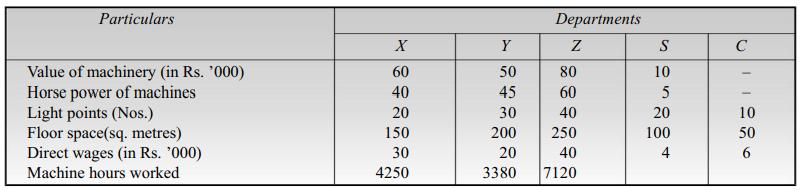

MM Ltd. has three production departments X, Y, Z and two service departments S and C. The following details are extracted from the books of accounts in respect of indirect expenses incurred during April 2005: The costs of the service departments are apportioned percentagewise as

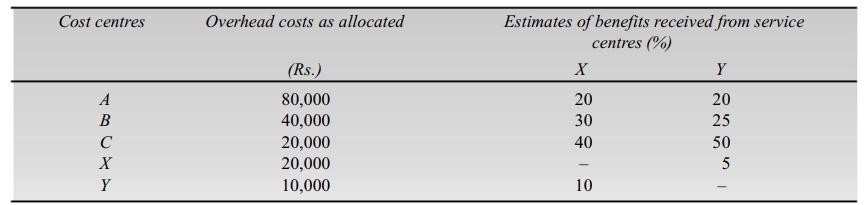

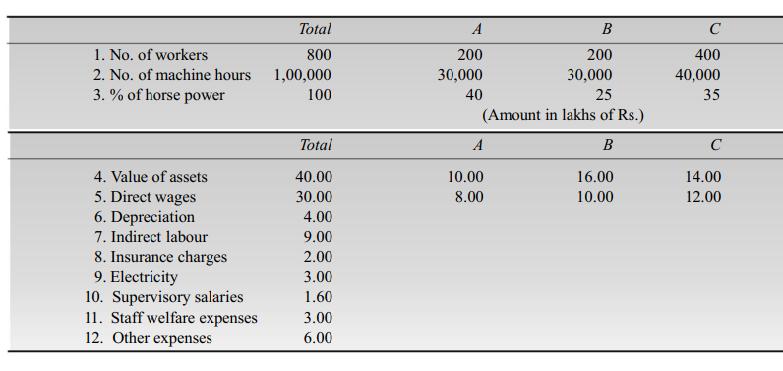

A company has three production centres, A, B and C and two service cost centres, X and Y. Costs allocated to service centres are required to be apportioned to the production centres to find our cost of production of different products. It is found that benefit of service cost centres is also

Which of the following bases of apportionment is most suited to sharing up the lighting costs between departments and cost centres? (a). Floor area or cubic capacity (b). The number of employees (c). The replacement value of machinery and equipment (d). The number of kilowatt

What information is necessary to calculate a machine hour rate for overhead absorption? State the conditions in which the method is most effective.

Indirect costs can also be described as: (a). Overhead costs (b). Prime costs (c). Variable costs (d). Total costs.

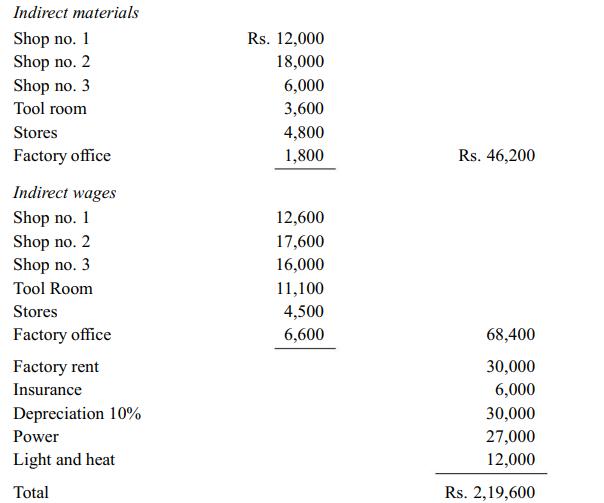

Following particulars have been extracted from the books of Reliable Co.: Further information regarding the operations is given below: You are required to prepare an overhead analysis sheet for the departments of Reliable Co. for the year showing the basis for apportionment. Indirect materials

Explain the concept of absorption of factory overheads.

Indirect costs which cannot be identified with a particular cost centre are shared out between cost centres using: (a). A recovery rate (b). An absorption rate (c). A method of apportionment (d). A method of allocation

What do you understand by classification, allocation and apportionment in relation to overhead expenses? Explain fully.

Which of the following is not an indirect cost? (a). Wages of production department machine operator. (b). Wages of a production department cleaner. (c). Materials used for machine maintenance in the production department.(d). Materials used to clean the production department floor.

Briefly describe two ways of dealing with apportioning service department costs among departments which, in addition to doing work for the main operation departments, also serve one another.

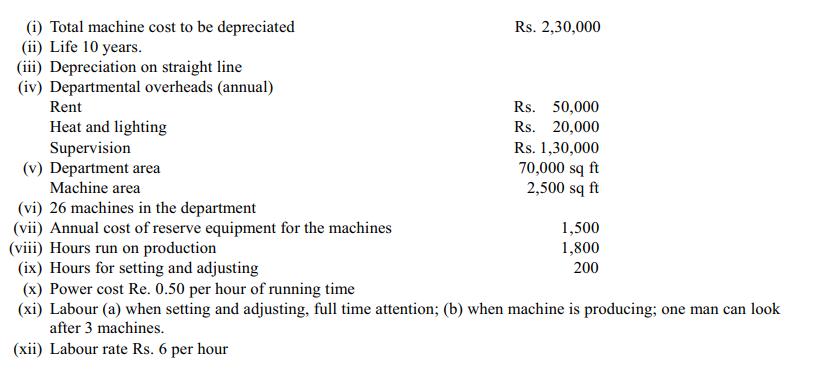

Compute the machine hour rate from the following data: (i) Total machine cost to be depreciated (ii) Life 10 years. (iii) Depreciation on straight line (iv) Departmental overheads (annual) Rent Heat and lighting Supervision (v) Department area Machine area (vi) 26 machines in the department (vii)

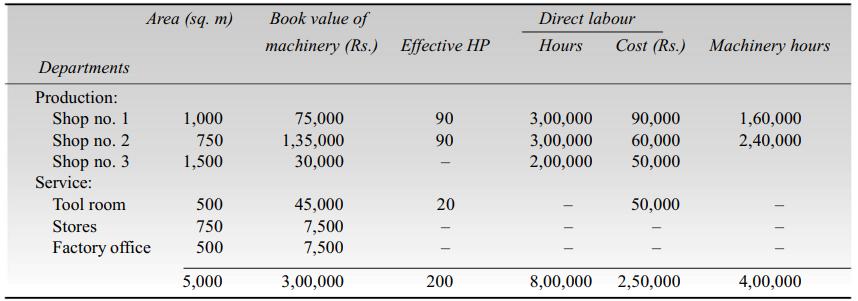

In a light engineering factory, the machine shop consists of three cost centres (A, B and C) each having three distinct sets of machines. The following are the details of estimates for the year 2001: Work out a composite machine hour rate for each of the three cost centres and indicate clearly the

Discuss the statement that the impact of overheads under varying conditions of production and sales is of greater interest to the management than its method of apportionment and allocation.

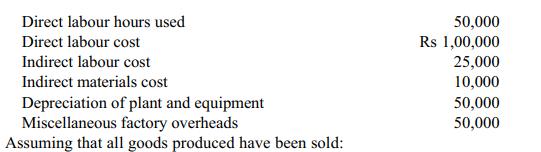

Sankalp Industries absorbs factory overhead costs at Rs. 2.50 per direct labour hour. Both opening and closing balance of work-in progress and finished goods inventories are zero.The following data are available for the year 2002: (i). Calculate factory overheads incurred and factory overheads

Overhead costs are usually classified according to variability. What are the necessities for such classification and what purpose do such classifications serve.

State in short the reasons for the use of predetermined rates for factory overhead absorption.

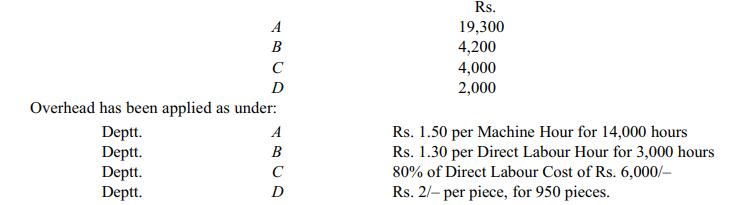

The factory overhead costs of four production departments of a company engaged in executing job orders, for an accounting year, are as follows:Find out the amount of department-wise under or over-absorbed factory overheads. A B C D Overhead has been applied as

Explain why predetermined overhead absorption rates are preferred to overhead absorption rates calculated from factual information after the end of a financial period.

The actual total expenditure of a light engineering factory was Rs. 6,75,912. Overheads were recorded at the rate of Rs. 2 per hour at normal capacity of the factory. Out of 10,000 units produced, only 8,000 units were sold. 500 units were in work in progress. Actual hours worked were 2,84,756.

What are the causes of under/over absorption of factory overheads? How will you deal with them in cost accounts?

A company absorbs production overheads on the basis of predetermined machine hour rate. For the month of March 2004 the budgeted machine hours were 8,500. During the month the actual machine hours worked were 7,928 actual overheads were Rs. 1,46,200 and there was under absorption of Rs.

Jones Ltd. has a budgeted activity level of 50,000 direct labour hours and budgeted production overheads of Rs. 100,000. You are required to calculate the underabsorbed and overabsorbed overheads, giving reasons, if, (a). 50,000 direct labour hours are worked and the actual overheads were Rs.

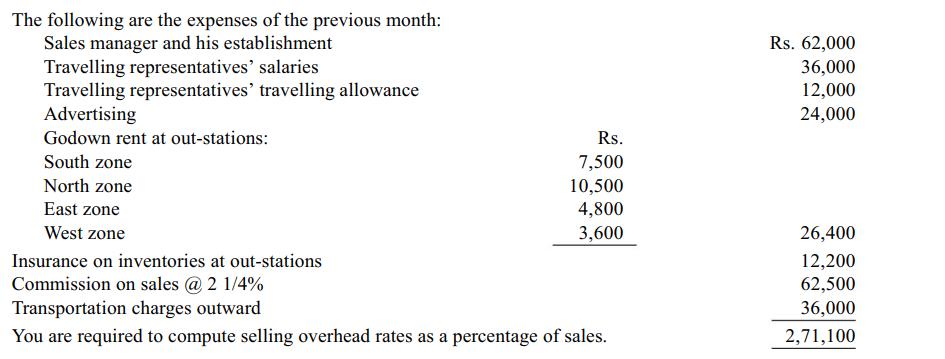

Following data is available relating to a company for a certain month: The company adopts sales basis and quantity basis for application of selling and distribution costs, respectively. Compute. (a). The territory-wise overhead recovery rates separately for selling and distribution

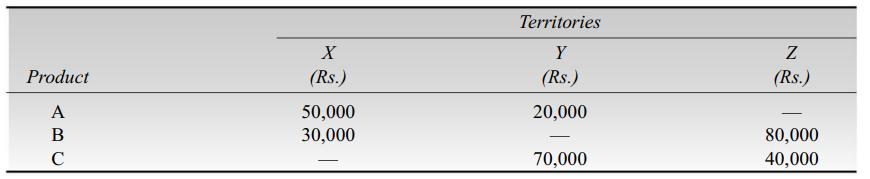

A company is producing three types of products, A, B, C. The sales territory of the company is divided into three areas, X, Y and Z. The estimated sales for the year are as under: Budgeted advertising cost is as under: You are required to find the advertising cost per cent on sales for

Explain the nature of administrative overheads. How are they apportioned to products?

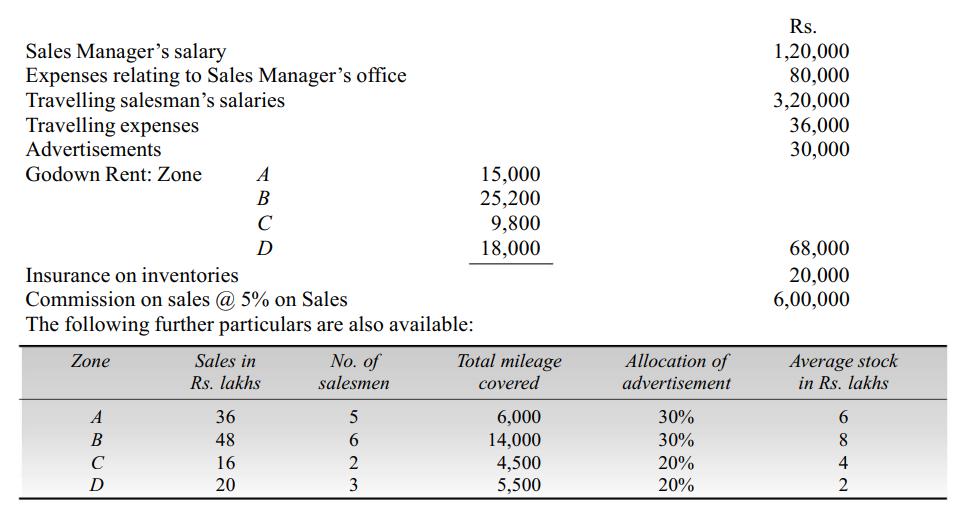

XYZ Ltd. a manufacturing company, having an extensive marketing network throughout the country, sells its products throughout four zonal sales offices, viz. A, B, C, and D. The budgeted expenditure for January 2008 are given below: Based on the above details, compute zonewise selling

Discuss the methods of absorption of selling and distribution overheads.

What problems are faced in applying administrative costs partly to the manufacturing and partly to the selling departments of a concern? How will you control administrative overhead of a concern?

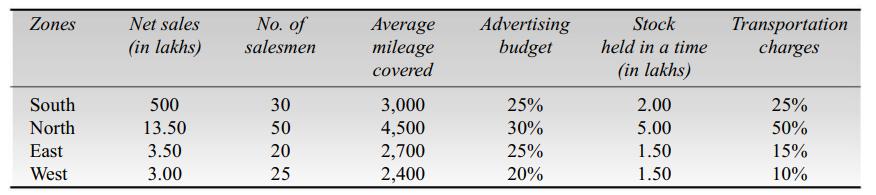

A match factory sells its goods in four district zones South, North, East and West. You have been given the particulars for January 2008 in respect of each zone mentioned as follows: Zones South North East West Net sales (in lakhs) 500 13.50 3.50 3.00 No.

Set out the main arguments for and against inclusion of interest on capital in cost accounts.

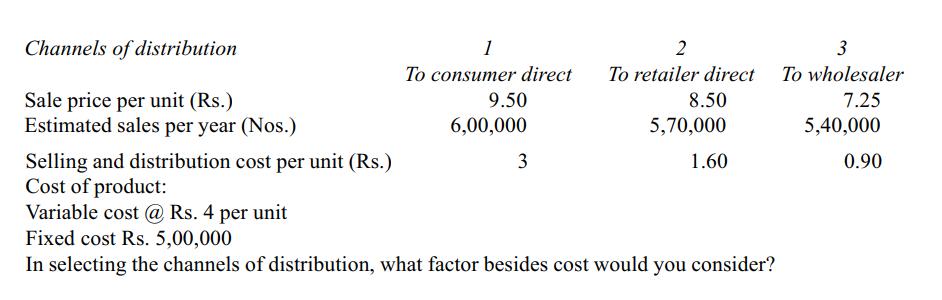

A company is supplying its products to the ultimate consumers through the wholesalers to retailers. The Managing Director thinks that if they sell through the retailers or to the consumers direct, they can increase their sales, earn better prices, and make more profit. As a cost accountant of the

Interest is a factor which cannot be disregarded by management. Comment on this statement.

Cost accounting has come to be an essential tool of the management.'' Comment.

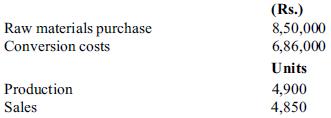

A firm has the following transactions for the month of January 2008.There are no opening inventory of raw materials, WIP and finished goods. The standard cost per unit is Rs. 310 (Rs. 170 for materials + Rs. 140 conversion cost). There was no closing WIP at the end of the period.Required:Make

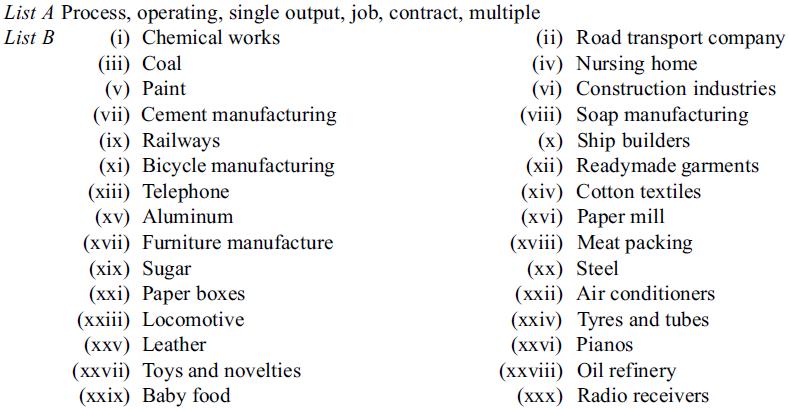

List A gives you different methods of costing which can be used in one or more industries or organisations given in List B. Mention the correct costing method of the industries in List B. List A Process, operating, single output, job, contract, multiple List B (i) Chemical works (iii) Coal (v)

''Financial accounting procedures are generally designed to ascertain the periodic profit or loss, but there are important limitations and deficiencies in the system.'' Discuss.

Examine critically the drawbacks of conventional financial accounting. Do you think that these limitations have been overcome by the introduction of cost accounting in business?

Indicate whether the following statements are True or False:(i) The rental of a car which includes a fixed daily rate plus an extra fee for each kilometre driven is an example of a step cost.(ii) Assuming inflation, if a company wants to maximise net income, it would select FIFO as the method of

What is cost accounting? What are its objectives? How do cost accounting records help in the planning and control of operations of a business enterprise?

What is meant by cost accounting? In what essential respects does cost accounting differ from financial accounting?

Explain fully the concept of cost. How does cost accounting contribute to the effective and efficient management of an industrial establishment?

What is the function of a costing department in a manufacturing concern? How is the costing department useful to other departments in a manufacturing concern?

SV Ltd. is a manufacturing company which has a sound system of financial accounting. The management of the company, therefore, feels that there is no need for the installation of a cost accounting system. Prepare a report for management, bringing out the distinction between cost and financial

''A cost keeping system that simply records costs for the purpose of fixing sale prices has accomplished only a small part of its mission.'' What are the other functions of costing?

''Cost accounting is an unnecessary luxury for business establishments.'' Do you agree with the statement? Discuss.

Explain the important objectives of cost accounting.

''Cost accounting is a system of foresight and not a postmortem examination, it turns losses into profits, speedsup activities and eliminates waste.'' Discuss.

State the primary objectives of installation of a costing system. Apart from technical costing problems, what practical difficulties would you meet and how would you overcome them?

How far is cost information helpful for the following purposes:(a) Fixation of selling prices(b) Control of costs(c) Management decisions

''Limitations of financial accounting have made the management to realise the importance of cost accounting''. Comment.

What are the advantages of introduction of costing system in an industrial organisation?

Mention the factors which should be considered in installing a costing system in an organisation.

What is meant by cost accounting? Explain the difference between financial accounting and cost accounting.

What purposes do cost centres serve? Are cost centres and cost units related to each other?

''Cost accounting is becoming more and more relevant in the emerging economic scenario in India''. Comment.

Discuss the essentials of good cost accounting system.

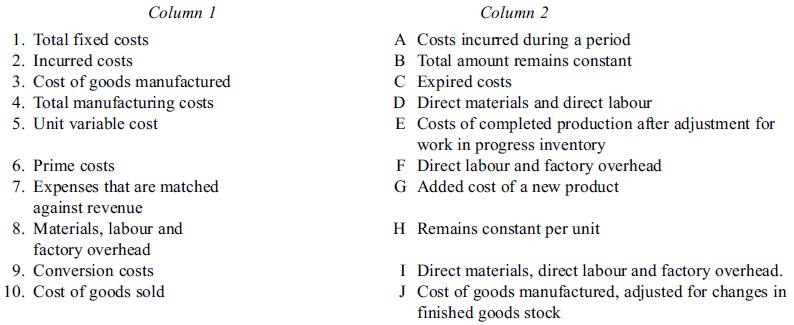

Match the items in Column 1 with the best choice in Column 2 Column 1 1. Total fixed costs 2. Incurred costs 3. Cost of goods manufactured 4. Total manufacturing costs 5. Unit variable cost 6. Prime costs 7. Expenses that are matched against revenue 8. Materials, labour and factory overhead 9.

You have been asked to install a costing system in a manufacturing company. What practical difficulties will you expect and how will you propose to overcome the same?

The following data are related to the manufacture of a standard product during the month of December 2001.You are required to prepare a cost sheet from the above showing:(a) The cost per unit.(b) The profit per unit sold and profit for the period Raw materials consumed Direct wages Machine hours

What is meant by management accounting? Discuss its objectives.

Lists two costs which are used in decision making but not entered in the accounting system under that designation.

In a company weekly minimum and maximum consumption of material A are 25 and 75 units respectively. The reorder quantity as fixed by the company is 300 units. The material is received within 4 to 6 weeks from issues of supply order. Calculate minimum level and maximum level of material A.

Compute the economic batch quantity for a company using batch costing with the following information:Annual demand for the component 400 unitsSetting up and order processing cost Rs. 50Cost of manufacturing one unit .................................... Rs. 100Rate of interest p.a.

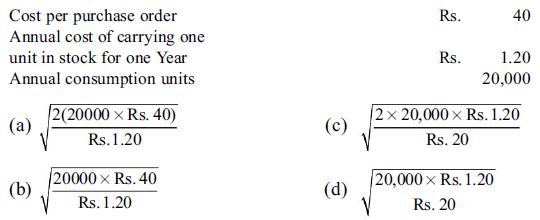

Given the following information, identify the correct calculation for the economic order quantity (EOQ) Cost per purchase order Annual cost of carrying one unit in stock for one Year Annual consumption units (a) (b) 2(20000 x Rs. 40) Rs.1.20 20000 x Rs.

Describe the meaning objectives, and basic principles of materials control system.

In a factory component A is used as follows:Calculate the following for component A:(a) Re-order level(b) Maximum level(c) Minimum level(d) Average stock level Normal usage 50 kg per week Maximum usage 75 kg per week Re-order period 4 to 6 weeks Minimum usage 25 kg per week Re-order quantity 300 kg

Economic order quantity (EOQ) model is used by a business to(a) Minimise the cost of placing orders(b) Minimise the unit purchase price of inventory(c) Minimise the number of orders placed during a year(d) Minimise the required amount of safety stock(e) Minimise the combined costs of placing orders

P. Ltd., is engaged in the manufacture of industrial pumps of a standard description. The company uses about 75,000 valves per year for its production and the usage is fairly constant at 6,250 valves per month. The valves cost Rs. 1.50 per unit when brought in quantities and the carrying cost is

What are the important requirements of a materials control system.

The calculation of inventory re-order point in units requires the(a) Purchase price per month(b) Annual demand for units(c) Daily demand for units(d) Storage cost per unit(e) Warehouse capacity

A company manufactures a product having a monthly demand of 2000 units. For one unit of finished product 2 kg of a particular raw material item is needed. The purchase price of the materials is Rs. 20 per kg. The ordering cost is Rs. 120 per order and the holding cost is 10% per annum.

A company manufactures a product from a raw material, which is purchased at Rs. 60 per kg. The company incurs a handling cost of Rs. 360 plus freight of Rs. 390 per order. The incremental carrying cost of inventory of raw material is Re 0.50 per kg per month. In addition, the cost of working

Materials control system would be most useful to a(a) Manufacturer(b) Wholesaler(c) Hospital(d) Retailer

A producer has estimated annual purchase requirement of 30,000 units of a material. Unit price of material is Rs. 50. Annual cost of carrying inventory is 20%. Ordering cost for an order is Rs. 60. Find out Economic Order Quantity (EOQ).

Which of the following items would most likely be included in the calculation of economic order quality?(a) Price(b) Cost(c) Demand(d) Supply

Annual requirement of a particular item of inventory is 10,000 units. Inventory carrying cost per unit per year is 20% and ordering cost is Rs. 40 per order. The price quoted by the supplier is Rs. 4/unit. However, the supplier is ready to give a discount of 5% for orders of 1,500 units or more. Is

About 50 items are required every day for a machine. A fixed cost of Rs. 50 per order is incurred for placing an order. The inventory carrying cost per item amount to Re. 0.02 per day. The lead period is 32 days. Compute:(i) Economic Order Quantity(ii) Re-order level

Explain Just-In-Time purchases.

From the following information calculate Economic Order Quantity, and the number of orders to be placed in one quarter of the year: (i) Quarterly consumption of materials (ii) Cost of placing one order (iii) Cost Per unit (iv) Storage and carrying Cost 2,000 kg. Rs. 50 Rs. 40 8% on average inventory

Vijay Industries manufactures a product X. On 1st January 2007, there were 5000 units of finished product in stock. Other stocks on 1st January 2007 were as follows:The information available from cost records for the year ended 31st December 2007 was as follows:There are 15000 units of finished

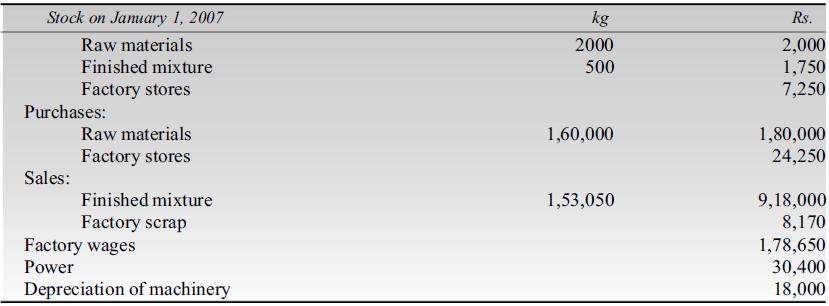

The following particulars relating to the year 2007 have been taken from the books of a chemical works manufacturing and selling a chemical mixture:The stock of finished mixture at the end of 2007 is to be valued at the factory cost of the mixture for that year. The purchase of raw materials

Calculate the maximum stock level from the following:EOQ-300 unitsUsage rate-25 to 75 units per weekReorder period-4 to 6 weeks.

Define the term 'cost'. How is it different from expense?

A factory produces a standard product. The following information is given to you from which you are required to prepare a cost sheet for January 2000.Factory overheads 80% of direct wagesOffice overheads 10% of works costSelling and distribution expenses Rs 2 per unit soldUnits produced and sold

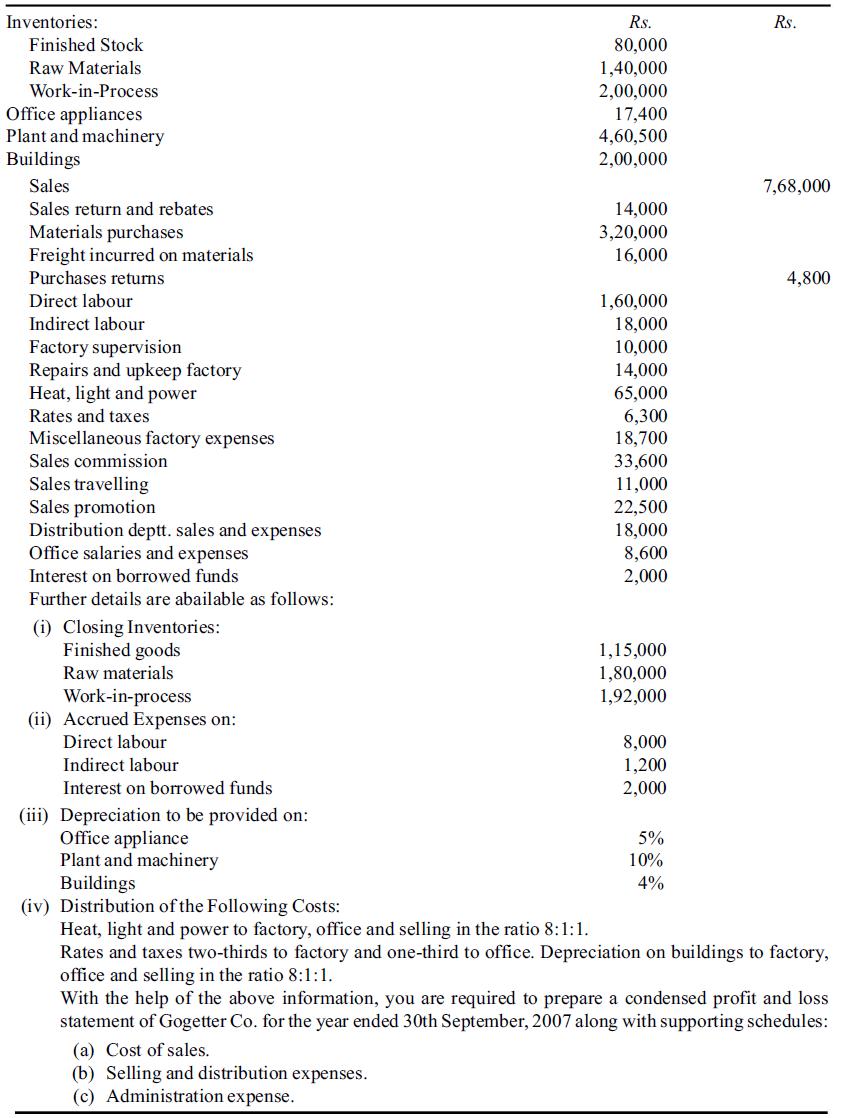

The following figures are extracted from the trial balance of Gogetter Co. on 30th September, 2007: Inventories: Finished Stock Raw Materials Work-in-Process Office appliances Plant and machinery Buildings Sales Sales return and rebates Materials purchases Freight incurred on materials Purchases

What is meant by 'differential cost'?

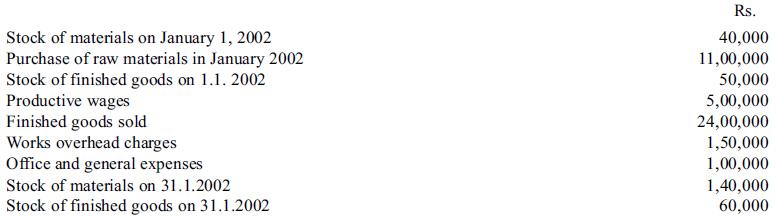

From the following particulars of a manufacturing firm, prepare a statement showing:(a) Cost of materials consumed(b) Works cost(c) Cost of production(d) Percentage of works overhead to productive wages(e) Percentage of general overhead to works cost Stock of materials on January 1, 2002 Purchase

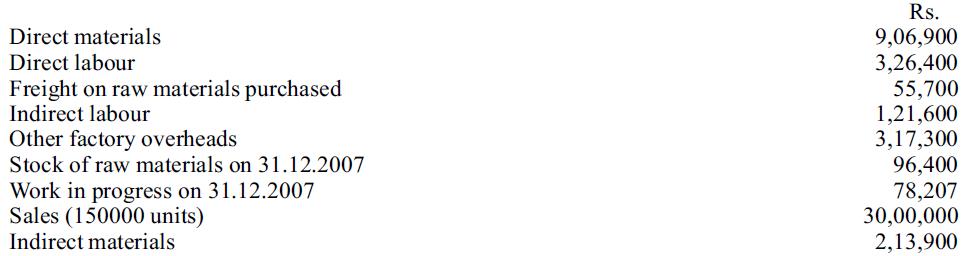

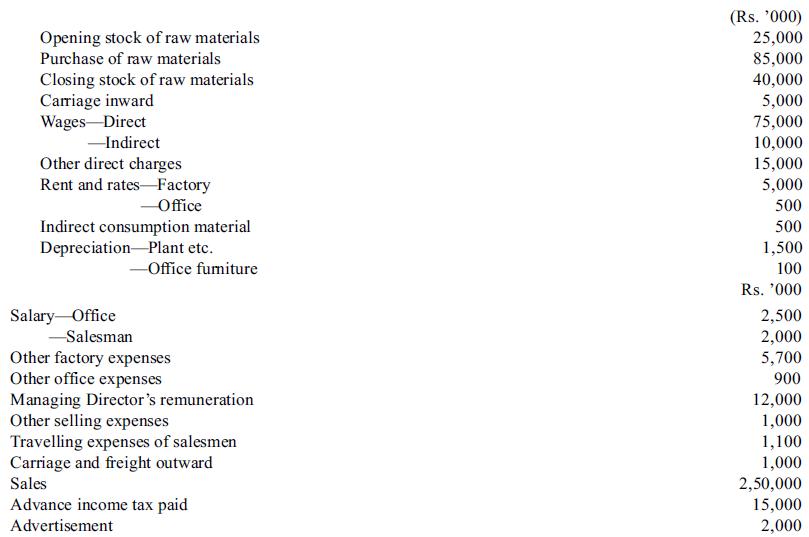

The following data have been extracted from the books of M/s Moonshine Industries for the calendar year 2002.The Managing Directors remuneration is to be allocated as Rs. 40,00,000 to the factory, Rs. 20,00,000 to the office and Rs. 60,00,000 to the selling departments. From the above information

What is the meaning of the term incremental cost? Does incremental cost mean the same thing as variable cost?

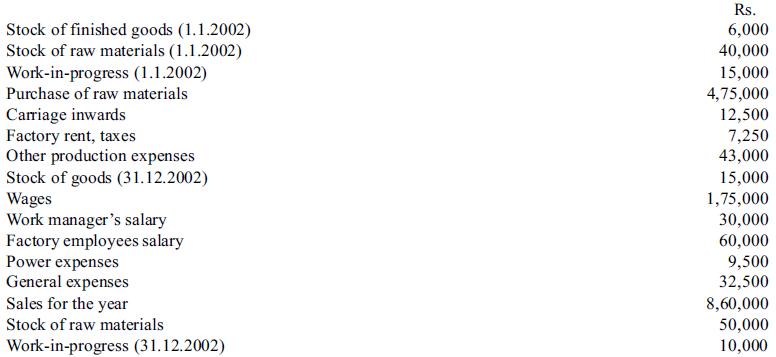

From the following particulars, prepare a cost sheet for the year ended 31.12.2002 Stock of finished goods (1.1.2002) Stock of raw materials (1.1.2002) Work-in-progress (1.1.2002) Purchase of raw materials Carriage inwards Factory rent, taxes Other production expenses Stock of goods

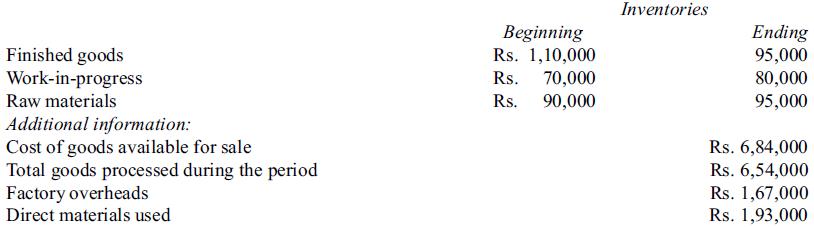

The following inventory data relates to XYZ Ltd:Requirements:(i) Determine raw materials purchases.(ii) Determine the direct labour cost incurred.(iii) Determine the cost of goods sold Finished goods Work-in-progress Raw materials Additional information: Cost of goods available for sale Total goods

Explain the nature of product and period cost. How do they affect net income of a business enterprise?

X Ltd. manufactures four brands of toys-A, B, C and D. If the company limits the manufacture to just one brand, the monthly production will be:A - 50000 unitsB - 100000 unitsC - 150000 unitsD - 300000 unitsYou are given the following set of information from which you are requested to find out the

Showing 6300 - 6400

of 6579

First

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

Step by Step Answers