New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

cost accounting

Cost Accounting 4th Edition Jawahar Lal, Seema Srivastava - Solutions

The effect of a price reduction is always to reduce the P/V ratio, to raise the break-even point, and to shorten the margin of safety. Explain with a suitable illustration.

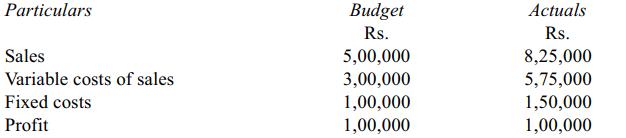

The Chief Cost Accountant of Vikas Limited found to his surprise that the actual profit for the period ending 30th June 2007 was the same as budgeted in spite of realising 10% more than the budgeted selling prices. The following were the results: You are required to assist the Chief Cost

Define break-even point. How can the break-even point be computed?

How is a break-even chart prepared? What information does the break-even chart give?

What are the basic assumptions in cost-volume-profit analysis under.(a). Absorption costing,(b). Variable costing?

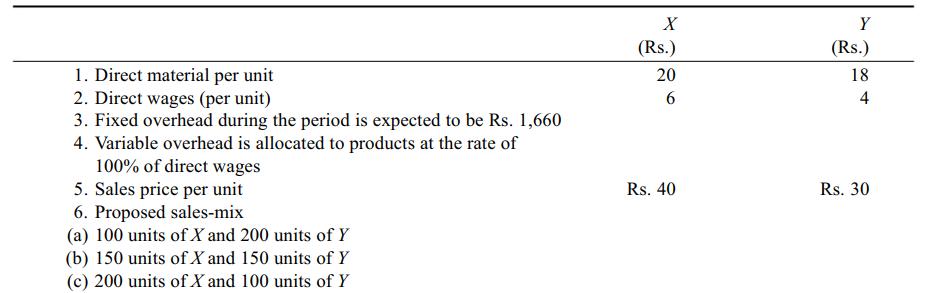

The following set of information is presented to you by your client AB Ltd., producing two products X and Y. As a cost accountant, you are requested to present to the management of AB Ltd. the following: (a). The unit marginal cost and unit contribution. (b). The total contribution and the

Mr. X has Rs. 2,00,000 investments in his business firm. He wants a 15% return on his money. From the analysis of recent cost figures, he finds that his variable operating cost is 60% of sales and his fixed costs are Rs. 80,000 per year. Show computations to answer the following questions: (a).

For product-mix decisions, what criteria can be used to select products that will maximise net income?

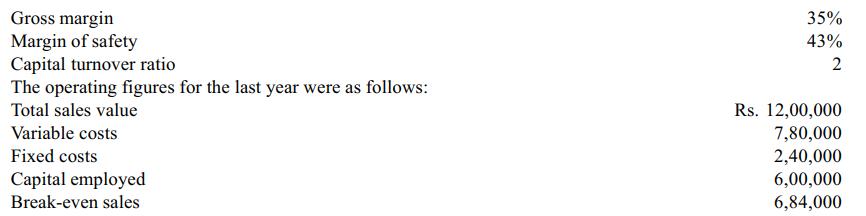

A company seeking to improve its competitive position, has launched a cost reduction programme in its existing plants, apart from trying to increase output. The present profit before tax comes to 15% of turnover and 30% of capital employed. Other relevant working ratios are: It has been proposed

Break-even analysis assumes that variable costs and revenues are linear and that fixed costs are fixed. Briefly explain why these assumptions may not be realistic.

Marginal costs reveal the lowest price at which a product can be sold during a trade depression, but they also reveal to management the most profitable lines during a period of intense trade activity. Explain, with examples, the second part of this statement.

Can there be two break-even points. Show with the help of a graph.

Distinguish between contribution and profit.

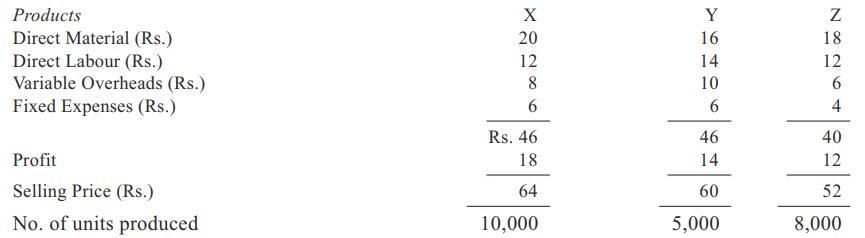

The costs per unit of three products X, Y and Z are given below: Production arrangements are such that if one product is given up the production of the others can be raised by 50%. The directors propose that product Z should be given up because the contribution from the product is the lowest.

What is meant by the term differential costing? Does differential cost mean the same thing as variable cost?

The type of costs presented to management for a non-routine decision should be limited to. (a). Relevant costs (b). Standard costs.(c). Controllable costs. (d). Conversion costs.

What is incremental cost? Does incremental cost mean the same thing as variable cost?

Merry-make Cassets Co., is expecting a profit of Rs. 2,50,000 for the current year. The following further information is available from records.The companys production capacity is not fully utilised and market research suggests following alternative strategies for the forthcoming year. (a).

Other things remaining the same, ideal product mix is determined in terms of.(a). Sales (b). Variable costs (c). Total costs (d). Contribution margin.

Give examples of how incremental costs are used in decision-making.

A departmental store is thinking of eliminating one of its departments because the accountant using the total cost basis to profitability analysis, says the department is operating at a loss. What should be investigated before the final decision is made?

Relevant costs are.(a). Future costs. (b). Standard costs. (c). Controllable costs. (d). Historical costs.

Explain the meaning and features of relevant costs. Give suitable examples to support your explanation.

The decision maker should consider in case of limiting factor(s) to maximise the profit. (a). Sales. (b). Contribution margin. (c). Variable costs. (d). Fixed costs.

Ventilators Ltd. wants to stabilise its production through the year. The approaches recommended are: (a). Maintan production at an even pace throughout the year, and get the off-season production stored on the premises.(b). Maintain production at an even pace but offer dealers a special discount

The measurable value of an alternative use of resources is referred to as a (an). (a). Opportunity cost. (b). Imputed cost. (c). Differential cost. (d). Sunk cost.

What do you mean by 'make or buy' decision. State the quantitative as well as qualitative considerations in inflnencing a make or buy decision.

A manager of a company reported the total additional cost required for the proposed increased production level. The increase in total cost is known as. (a). Controllable cost (b). Incremental cost (c). Opportunity cost.(d). Out-of-pocket cost.

Cost-benefit analysis is needed for resolving many managerial problems. List the various items of cost and benefits that you will quantify in respect of managerial decisions: (a). Add or drop a product. (b). Retain or replace (c). Shutdaun or continue.

A factory produces 24000 units. The cost sheet gives the following information: The product is sold at Rs. 20 per unit. The management proposed to increase the production by 3000 units for sales in the foreign market. It is estimated that semi-variable overheads will increase by Rs. 1,000. But the

Which of the following is usually an incremental cost. (a). Conversion cost (b). Period cost (c). Manufacturing overhead cost (d). Direct product cost.

Explain the basic characteristics of costs involved in decision-making.

A machine tool manufacturing company sells its lathes at Rs. 36,500 each made up as follows: (a). A firm in Arabia has offered to buy 10 companys lathes at Rs. 28,500 each. Should the company be interested in the business? (b). It has been decided to sell 5 such lathes to an engineering company

A cost incurred in the past and hence irrelevant for current decision making is a. (a). Fixed cost (b). Discretionary cost (c). Sunk cost (d). Direct cost.

State the costing data required for (i). Determining the priority of products,(ii). Make or buy decisions.

A cost that cannot be changed by any decision made now or in the future is a (an). (a). Indirect cost. (b). Uncontrollable cost. (c). Opportunity cost. (d). Sunk cost.

How would you go about determining the point at which a manufacturing company that is facing a period of operating losses should shut assuming that profitability of operations is the only point to be considered?

A company annually manufactures 10000 units of a product at a cost of 4 per unit and there is home market for consuming the entire volume of production at the sale price of 4.25 per unit. In the year 2002, there is a fall in the demand for home market which can consume 10000 units only at a sale

Due to industrial depression, a plant is running, at present, at 50% of its capacity. The following details are available. An exporter offers to buy 5000 units per month at the rate of Rs. 650 per unit and the company hesitates to accept the offer for fear of increasing its already large operating

Why is the contribution that a product makes towards the recovery of non-escapable costs a bettr measure of its profitability than the profit or loss reported on its sale after it has been charged with its fair share of all costs?

An Electronics Company has the following cost structure for an electronic product.Fixed selling and administrative costs Rs. 6,00,000.Additional information: (i). Budgeted production and sale for the next year is 20000 units. (ii). The management feels that a minimum return of 20% is required on

In the long run, selling price will tend to equal costs plus reasonable profits. Discuss.

List the factors taken into consideration in fixing the selling price by a business firm.

Discuss full cost-plus and marginal cost-plus methods of pricing. Which pricing method can be useful to a firm and under what situations.

Product pricing is an important area for management decision making. State briefly the broad objectives of pricing policy. Mention specifically situations where prices are fixed below the variable cost.

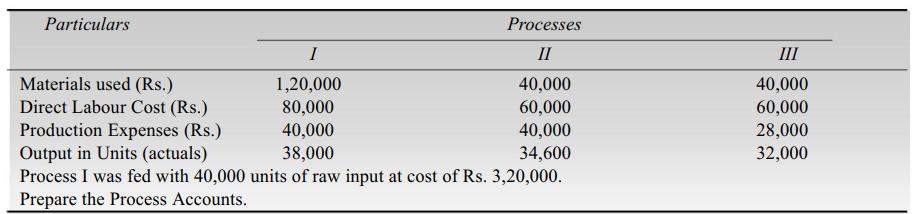

Prepare a statement of equivalent production, statement of cost, process account from the following information using the average method: During the period 60,000 units were completed and transferred to Process II. Closing stock 40,000 units, degree of completion. Opening

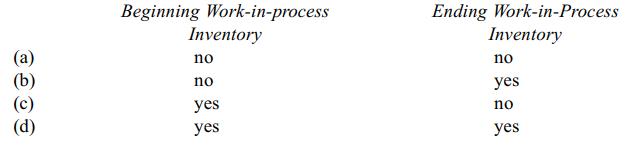

The first-in, first-out method of process costing differs from the weighted-average method in that the first-in, first-out method. (a). Considers the stage of completion of beginning work-in-process inventory in computing equivalent units of production, whereas the weighted-average method does

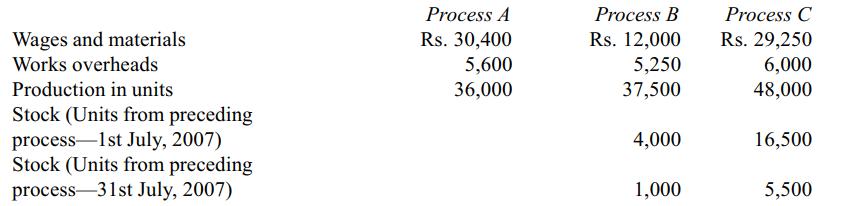

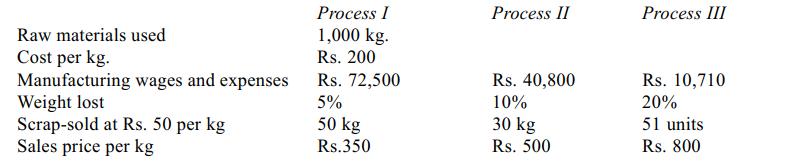

From the following figures show the cost of three processes of manufacture. The production of each process is passed on to the next process immediately on completion. Wages and materials Works overheads Production in units Stock (Units from preceding process 1st July, 2007) Stock (Units from

Prepare process cost accounts from the following data:Production overhead incurred is Rs. 1,60,000 and is recovered on 200% of direct wages. Production during the period was 20,000 units. There was no opening or closing work-in-progress. Items Direct material Direct wages Direct

Define integrated accounting system. Distinguish it with non-integrated accounting system.

When should process costing method be used in assigning costs of products. (a). If the product is manufactured on the basis of each order received. (b). When production is only partially completed during the accounting period. (c). If the product is composed of mass-produced

From the following Figures, prepare process accounts indicating the cost of process and the total cost. The production was 480 articles per week. Office overheads amounting to Rs. 1,700 should be apportioned on the basis of wages. Ignore stock in hand and work-in-progress at the beginning and

The following data are available pertaining to a product after passing through two processes A and B: Output transferred to process C from process B, 9120 units for Rs. 49,263.The wastage of process C is sold at Re 1.00 per unit. The overhead charges were 168% of direct labour. The final product

Compare the cost accumulation and summarising procedures of a job order cost system and a process cost system.

Which is the best cost accumulation procedure to use when there is a continuous mass production of like units. (a). Actual (b). Standard (c). Job order (d). Process

What is equivalent production? What is its effect on computed unit cost?

Which of the following is a characteristic of a process costing method? (a). Work-in-progress inventory restated in terms of completed units.(b). Costs are accumulated by order. (c). It is used by a company manufacturing on customers orders.(d). Standard costs are not applicable.

Normal wastage and abnormal wastage should be classified as: Normal (a) Period cost (b) Product cost (c) Period cost (d) Product cost Abnormal Period cost Period cost Product cost Product cost

In a certain process, material is mixed and cooked in batches of 1,000 lbs each. Cooking results in 10 percent loss of weight of the mixture. Since the cooking requires considerable skill and constant watching, there is generally a further loss for spoilage which is not discovered until processing

The finished product of a manufacturing company passes through three Processes, viz., I, II and III. The normal wastage in each process is 5%, 7% and 10% for the Processes I, II and III respectively (calculated with reference to the number of units fed into each process). The scrap generated out of

How is opening work-in-progress handled in average costing?

Normal wastage is properly classified as: (a). An extraordinary item (b). Period cost (c). Product cost (d). Deferred charge

What are some of the disadvantages of the FIFO costing method?

If the amount of wastage in a manufacturing process is abnormal, it should be classified as: (a). Deferred charge (b). Joint cost (c). Period cost (d). Product cost

A product passes through three Processes A, B and C. 10,000 units a cost of Rs. 1.10 were issued to Process-A. The other direct expenses were as follows:The wastage of Process-A was 5% and in Process-B 4%. The wastage of Process-A was sold at Re. 0.25 per unit and that of B at Re. 0.50 per unit and

What is the meaning of the term split-off? What is its significance in product costing?

The type of wastage that should not affect the recorded costs of closing inventories is: (a). Abnormal wastage (b). Normal wastage (c). Seasonal wastage (d). Standard wastage

An article passes through three successive operations from the raw material to the finished product stage. The following data are available from the production records of a particular month:(a). Determine the input required to be introduced in the first operation in number of pieces in order to

What are joint costs? What problems are created by joint costs?

Each of the following is a method by which to allocate joint costs except. (a). Relative sales value (b). Relative profitability (c). Relative weight, volume (d). Average unit cost

Explain the difference between a main product and a by-product.

How can the income from the sale of by-products be shown on the income statement?

Department I of Coromandel Chemicals conducts a process which requires mixing of materials and cooking of the mixture in batches of 1,000 lbs each. Cooking results in 10 per cent loss of weight of the mixture. Also, past experience shows that two batches out of every ten started in the process are

Product Z is obtained after it passes through three distinct processes. The following information is obtained from the accounts for the month ending December 31, 2008. 1,000 units at Rs. 3 each were introduced to Process I. There was no stock, material or work-in-progress at the beginning or

Does the showing of income from by-products on the income statement influence the unit cost of the main product?

Joint costs are most frequently allocated based upon relative.(a). Profitability (b). Conversion costs (c). Sales value (d). Prime costs.

The finished product of a factory has to pass through three Processes A, B and C. The normal wastage of each process is 2% in A, 5% in B and 10% in C. The percentage of waste is computed on the number of units entering each process. The scrap value of wastage of Process A, B and C are Rs. 10, Rs.

What is the difference between physical quantity method and sales value method?

In order to compute equivalent units of production using FIFO method of process costing, work for the period must be broken down to units.(a). Completed during the period and units in ending inventory. (b). Completed from the beginning inventory, started and completed during the month and

Define and explain the term joint products and by-products. Enumerate the method which may be employed in costing joint product.

From the industries listed below, choose the one most likely to use process costing in accounting for production costs: (a). Road builders (b). Electrical contractor (c). Newspaper publisher (d). Automobile repair shop

What are transferred-in costs as used in a process cost accounting system?(a). Labour that is transferred from another department within the same plant instead of hiring temporary workers from the outside.(b). Cost of the production of a previous internal process that is subsequently used in a

A product, which uses 100 tons as input per month passes through two Processes. The details of cost in Process 1 for April 2003 are:The total loss in Process 1 is 2% of input, and the scrap is 8% of input with a value of Rs. 12,000 per ton. The material to Process 2 is transferred at cost. The

The units transferred in from the first department to the second department should be included in the computation of the equivalent-units divisor for the second department for which of the following methods of process costing? (a) (b) (d) First-In, First-Out yes yes no no Weighted

The product of a manufacturing concern passes through two Processes A and B and then to finished stock. It is ascertained that in each process 5% of the total weight is lost and 10% is scrap, which from processes A and B realises Rs. 80 per kg and Rs. 200 per kg respectively.The following are the

Explain with an example the concept of equivalent production for valuation of work-in-progress.

Define joint products and by-products. Explain the various bases available for apportionment of joint costs to joint products.

Purchased materials added in the second department of a three department process that do not increase the number of units produced in the second department would.(a). Not change the amount transferred to the next department.(b). Decrease total work-in-process inventory. (c). Increase the

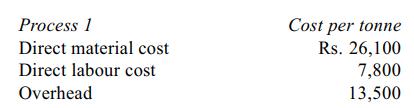

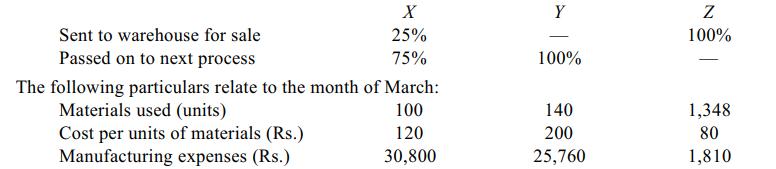

XYZ Ltd. manufactures and sells three chemicals produced by consecutive processes known as X,Y and Z. In each process, 2% of the total weight put in is lost and 10% is scrap, which from processes X and Y realised Rs. 100 a units and from Z Rs. 200 a units. The products of the three processes are

A Product passes through three processes. Figure relating to production for the 6 months of 2005 are as follows: Management expenses were Rs. 17,500, selling expenses Rs. 10,000 and interest on borrowed capital Rs. 4,000. Two thirds of Process I and one-half of Process II are passed on to

Distinguish between normal and abnormal wastage of materials with specific reference to their accounting treatment and control.

Purchased materials added in the second department of a three-department process that increase the number of units produced in the second department would always. (a). Change the direct labour cost percentage in the ending work-in-process inventory. (b). Cause no adjustment to the unit

What are equivalent units of production? Mention two principal methods of calculating equivalent units.

The percentage of completion of the beginning work-in-process inventory should be included in the computation of the equivalent units of production for which of the following methods of process costing? First-in, First-out yes yes no no Weighted Average no yes yes no

Explain briefly the procedure for the valuation of work-in-progress.

In the computation of manufacturing cost per equivalent unit, the weighted-average method of process costing considers.(a). Current costs only. (b). Current costs plus cost of ending work-in-process inventory. (c). Current costs less cost of beginning work-in-process inventory. (d).

Mention the different methods of by-product cost accounting.

In a given process-costing system, the equivalent-units divisor is computed for the weighted-average method. With respect to conversion costs, the percentage of completion for the current period only is included in the calculation of the. (a) (d) Beginning

Process 2 receives units from Process 1 and after carrying out work on the units transfers them to Process 3. For the accounting period the relevant data were as follows:The costs of the period were Rs. 33,160 and no units were scrapped.Required: Prepare the Process Account for Process 2 using

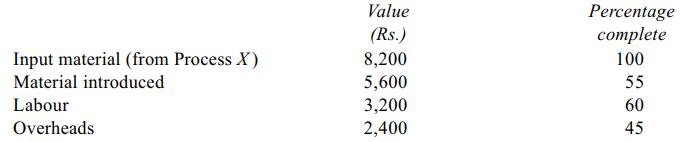

The following data relate to Process Y for accounting period 2. At the beginning of period 2, there were 800 units partly completed which had the following values:During the period 4,300 units were transferred from Process X at a value of Rs. 46,500 and other costs were: At the end of the

Showing 6100 - 6200

of 6579

First

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

Step by Step Answers