New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

financial reporting financial statement analysis and valuation

International Financial Statement Analysis CFA Institute Investment Series 1st Edition Thomas R. Robinson, Hennie Van Greuning CFA, Elaine Henry, Michael A. Broihahn, Sir David Tweedie - Solutions

CROCO S.p.A. sells an intangible asset with a historical acquisition cost of €12 million and an accumulated depreciation of €2 million and reports a loss on the sale of €3.2 million.Which of the following amounts is most likely the sale price of the asset?A. €6.8 million B. €8.8 million

According to IFRS, all of the following pieces of information about property, plant, and equipment must be disclosed in a company’s financial statements and footnotes except for:A. useful lives.B. acquisition dates.C. amount of disposals.

According to IFRS, all of the following pieces of information about intangible assets must be disclosed in a company’s financial statements and footnotes except for:A. fair value.B. impairment loss.C. amortization rate.

Which of the following characteristics is most likely to differentiate investment property from property, plant, and equipment?A. It is tangible.B. It earns rent.C. It is long-lived.

If a company uses the fair value model to value investment property, changes in the fair value of the asset are least likely to affect:A. net income.B. net operating income.C. other comprehensive income.

Investment property is most likely to:A. earn rent.B. be held for resale.C. be used in the production of goods and services.

A company is most likely to:A. use a fair value model for some investment property and a cost model for other investment property.B. change from the fair value model when transactions on comparable properties become less frequent.C. change from the fair value model when the company transfers

With respect to Statement 1, which of the following is the most likely effect of management’s decision to expense rather than capitalize these expenditures?A. 2009 net profit margin is higher than if the expenditures had been capitalized.B. 2009 total asset turnover is lower than if the

With respect to Statement 2, what would be the most likely effect in 2010 if AMRC were to switch to an accelerated depreciation method for both financial and tax reporting?A. Net profit margin would decrease.B. Total asset turnover would increase.C. Cash flow from operating activities would

With respect to Statement 3, what is the most likely effect of the impairment loss?A. Net income in years prior to 2009 was likely understated.B. Net profit margins in years after 2009 will likely exceed the 2009 net profit margin.C. Cash flow from operating activities in 2009 was likely lower due

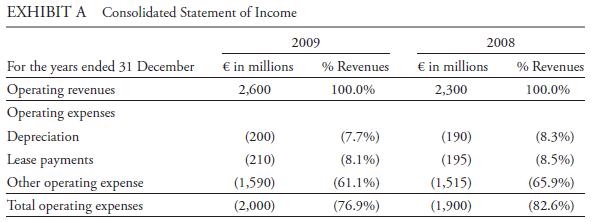

Based on Exhibits A and B, the best estimate of the average remaining useful life of the company’s plant and equipment at the end of 2009 is:A. 20.75 years.B. 24.25 years.C. 30.00 years.Melanie Hart, CFA, is a transportation analyst. Hart has been asked to write a research report on Altai

With respect to Statement 4, if AMRC had used its old classification method for its leases instead of its new classification method, its 2009 total asset turnover ratio would most likely be:A. lower.B. higher.C. the same.Melanie Hart, CFA, is a transportation analyst. Hart has been asked to write a

With respect to Statement 4 and Exhibit A, if AMRC had used its old classification method for its leases instead of its new classification method, the most likely effect on its 2009 ratios would be a:A. higher net profit margin.B. higher fixed asset turnover.C. higher total liabilities-to-total

Jordan’s response about the financial statement impact of Alpha’s decision to capitalize the cost of its new computer system is most likely correct with respect to:A. lower net income.B. lower total assets.C. higher cash flow from operating activities.Brian Jordan is interviewing for a junior

Jordan’s response about the ratio impact of Alpha’s decision to capitalize interest costs is most likely correct with respect to the:A. interest coverage ratio.B. fixed asset turnover ratio.C. interest coverage and fixed asset turnover ratios.Brian Jordan is interviewing for a junior equity

Jordan’s response about the impact of Alpha’s decision to classify its lease as an operating lease instead of finance lease is most likely incorrect with respect to:A. net income.B. solvency and activity ratios.C. cash flow from operating activities.Brian Jordan is interviewing for a junior

Jordan’s response about the impact of the different depreciation methods on net profit margin is most likely incorrect with respect to:A. accelerated depreciation.B. straight-line depreciation.C. units-of-production depreciation.Brian Jordan is interviewing for a junior equity analyst position at

Jordan’s response about his approach to estimating a company’s need to reinvest in its productive capacity is most likely correct regarding:A. estimating the average age of the asset base.B. estimating the total useful life of the asset base.C. estimating the average remaining useful life of

Jordan’s response about the effect of Beta’s impairment loss is most likely incorrect with respect to the impact on its:A. debt to total assets.B. fixed asset turnover.C. cash flow from operating activities.Brian Jordan is interviewing for a junior equity analyst position at Orion Investment

Jordan’s response about the effect of Alpha’s revaluation is most likely correct with respect to the impact on its:A. return on equity.B. return on assets.C. debt to capital ratio.Brian Jordan is interviewing for a junior equity analyst position at Orion Investment Advisors. As part of the

Debond Corp. (a hypothetical company) issues £1,000,000 worth of five-year bonds, dated 1 January 2010, when the market interest rate on bonds of comparable risk and terms is 5 percent per annum. The bonds pay 5 percent interest annually on 31 December. What are the sales proceeds of the bonds

Debond Corp. issues £1,000,000 worth of five-year bonds, dated 1 January 2010, when the market interest rate on bonds of comparable risk and terms is 6 percent. The bonds pay 5 percent interest annually on 31 December. What are the sales proceeds of the bonds when issued, and how is the issuance

Debond Corp. issues £1,000,000 face value of five-year bonds, dated 1 January 2010, when the market interest rate is 6 percent. The sales proceeds are £957,876. The bonds pay 5 percent interest annually on 31 December.1. What is the interest payment on the bonds each year?2. What amount of

Prembond Corp. issues £1,000,000 face value of five-year bonds, dated 1 January 2010, when the market interest rate is 4 percent. The sales proceeds are £1,044,518. The bonds pay 5 percent interest annually on 31 December.1. What is the interest payment on the bonds each year?2. What amount of

The following are excerpts from Notes 2 and 13 of Sony Corporation’s (NYSE: SNE) 20-F filing for the fiscal year ended 31 March 2009. These discuss the option for reporting fair values in the balance sheet and illustrate financial statement disclosures of fair values.Excerpt from Note 2: Summary

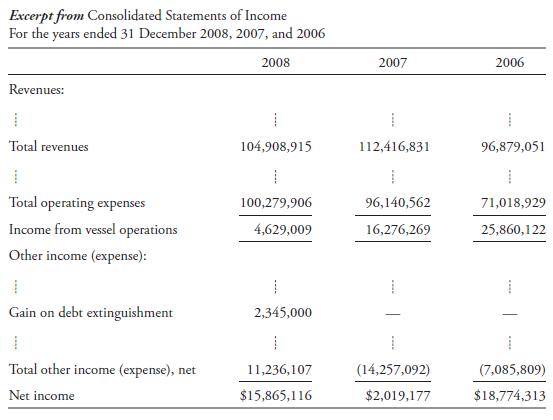

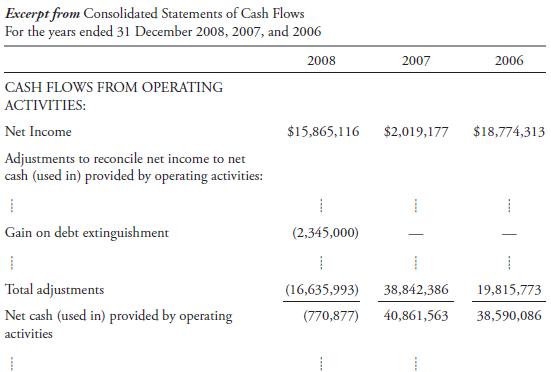

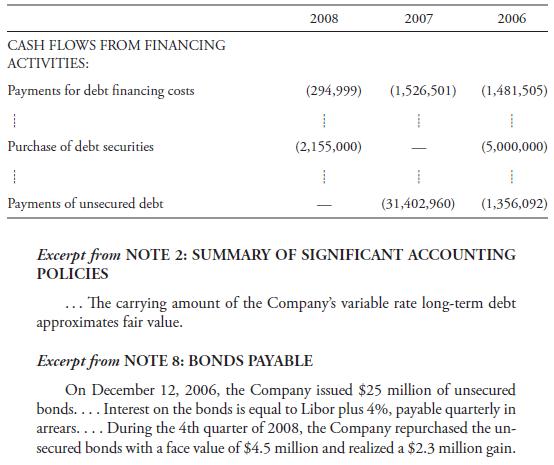

The following excerpts are from the 2008 20-F filing of B+H Ocean Carriers (NYSE Alternext: BHO ). In its statement of cash flows, the company uses the indirect method to reconcile net income with net cash (used in) provided by operations.1. The balance in bonds payable was reduced at redemption

The following excerpt is from TORM A/S (NASDAQ: TORM) from the Risk Factors section of Item 3, Key Information, in its fiscal year 2008 20-F filing. The excerpt illustrates debt covenants and their disclosure:Certain of our loan agreements contain restrictive covenants, which may limit our

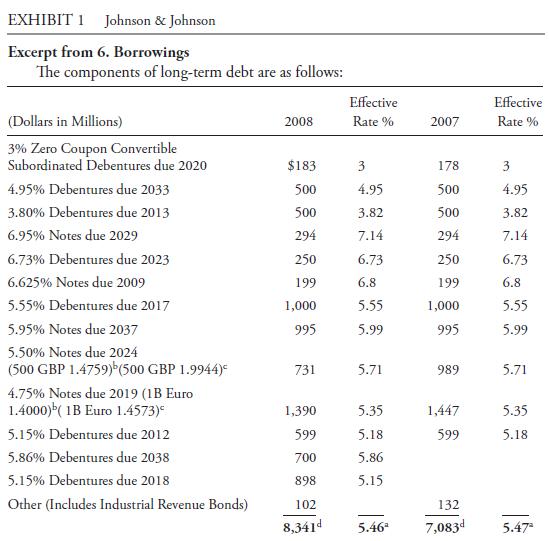

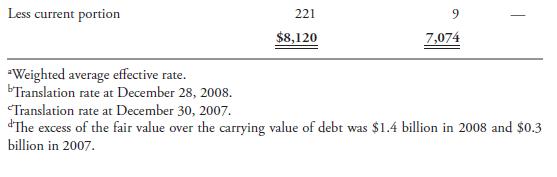

Exhibit 1 is an excerpt from Note 6 of Johnson & Johnson’s (NYSE: JNJ) 2008 financial statements that illustrates financial statement disclosure for long-term debt, including type and nature of long-term debt, effective interest rates, and required payments over the next five years. Johnson

The following excerpt is from the fiscal year 2008 Annual Report of the China Petroleum & Chemical Corporation (NYSE Euronext: SNP).Excerpt from NOTE 29: DEBENTURES PAYABLE On 26 February 2008, the Company issued convertible bonds with stock warrants due 2014 with an aggregate principal amount of

CAPBS Inc. enters into a lease agreement to acquire the use of a piece of machinery for four years beginning on 1 January 2010. The lease requires four annual payments of€28,679 starting on 1 January 2010. The useful life of the machine is four years, and its salvage value is zero. CAPBS accounts

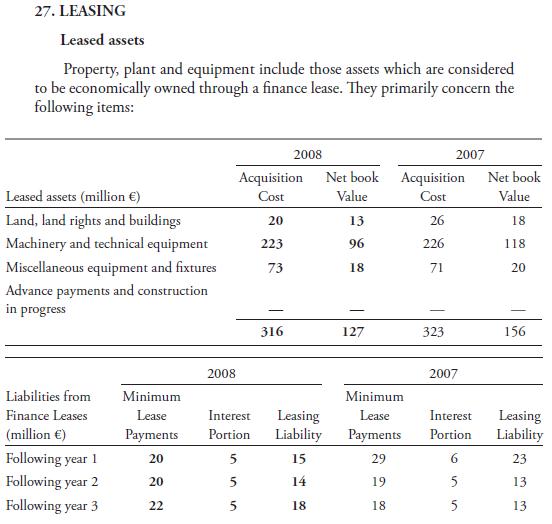

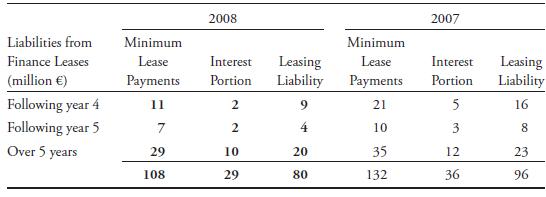

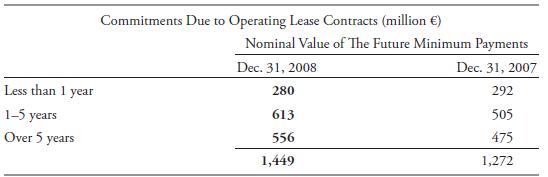

BASF Group (OTC: BASFY) has significant commitments under finance and operating leases. Presented below is selected note disclosure from its fiscal year 2008 financial statements.In the current business year and in 2007, no additional lease payments arising from contractual obligations were

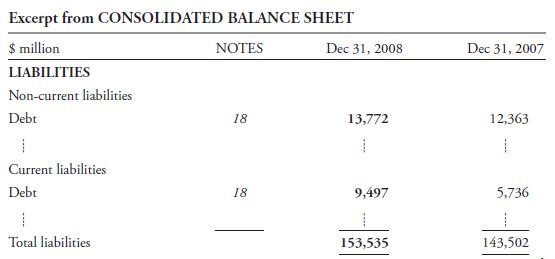

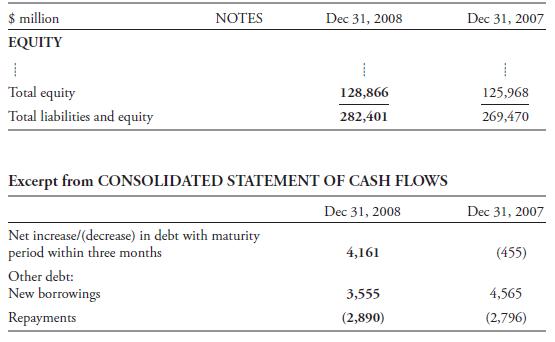

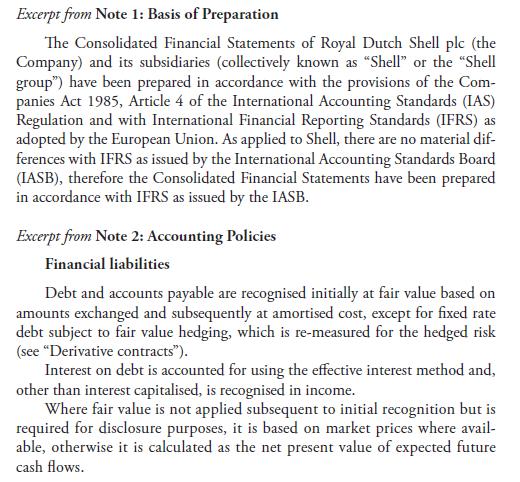

Use the following excerpts taken from Royal Dutch Shell (LSE: RDSA) 2008 consolidated financial statements and notes to the consolidated financial statements to answer the questions below.Use the above information to answer the following questions:1. How does Royal Dutch Shell initially value its

DIRFIN Inc. owns a piece of machinery and plans to lease the machine on 1 January 2010. In the lease contract, DIRFIN requires four annual payments of €28,679 starting on 1 January 2010. DIRFIN is confident that the payments will be received.The useful life of the machine is four years, and its

Assume a (hypothetical) company, Selnow, manufactures machinery and enters into an agreement to lease a machine on 1 January 2010. Under the lease, the company is to receive four annual payments of €28,679 starting on 1 January 2010. Selnow is confident that the payments will be received. The

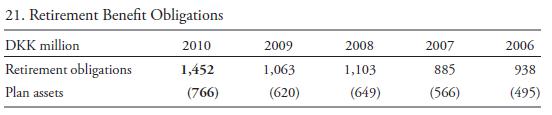

The following are excerpts of pension-related disclosures from Novo Nordisk’s (NYSE: NVO) 2010 Annual Report. NOVO Nordisk reports under IFRS. These financial statements were issued prior to the updated IFRS for pension accounting, which (effective January 2013) requires companies to show the

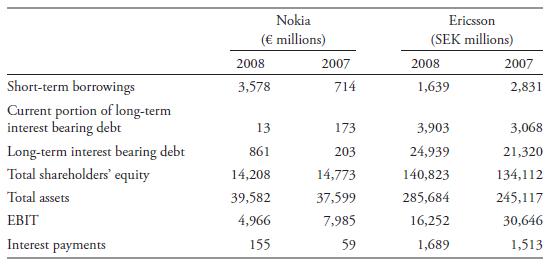

A credit analyst is evaluating and comparing the solvency of two companies—Nokia Corporation (NYSE: NOK) and LM Ericsson Telephone Company (NYSE: ERIC)—at the beginning of 2009. The following data are gathered from the companies’ 2008 annual reports and 20-F filings:Use the above information

A company issues €1 million of bonds at face value. When the bonds are issued, the company will record a:A. cash inflow from investing activities.B. cash inflow from financing activities.C. cash inflow from operating activities.

At the time of issue of 4.50% coupon bonds, the effective interest rate was 5.00%. The bonds were most likely issued at:A. par.B. a discount.C. a premium.

Oil Exploration LLC paid $45,000 in printing, legal fees, commissions, and other costs associated with its recent bond issue. It is most likely to record these costs on its financial statements as:A. an asset under US GAAP and reduction of the carrying value of the debt under IFRS.B. a liability

On 1 January 2010, Elegant Fragrances Company issues £1,000,000 face value, five-year bonds with annual interest payments of £55,000 to be paid each 31 December. The market interest rate is 6.0 percent. Using the effective interest rate method of amortisation, Elegant Fragrances is most likely to

Consolidated Enterprises issues €10 million face value, five-year bonds with a coupon rate of 6.5 percent. At the time of issuance, the market interest rate is 6.0 percent. Using the effective interest rate method of amortisation, the carrying value after one year will be closest to:A. €10.17

The management of Bank EZ repurchases its own bonds in the open market. They pay €6.5 million for bonds with a face value of €10.0 million and a carrying value of €9.8 million. The bank will most likely report:A. other comprehensive income of €3.3 million.B. other comprehensive income of

Innovative Inventions, Inc. needs to raise €10 million. If the company chooses to issue zero-coupon bonds, its debt-to-equity ratio will most likely :A. rise as the maturity date approaches.B. decline as the maturity date approaches.C. remain constant throughout the life of the bond.

Fairmont Golf issued fixed rate debt when interest rates were 6 percent. Rates have since risen to 7 percent. Using only the carrying amount (based on historical cost) reported on the balance sheet to analyze the company’s financial position would most likely cause an analyst to:A. overestimate

Debt covenants are least likely to place restrictions on the issuer’s ability to:A. pay dividends.B. issue additional debt.C. issue additional equity.

Compared to using a finance lease, a lessee that makes use of an operating lease will most likely report higher:A. debt.B. rent expense.C. cash flow from operating activity.

Which of the following is most likely a lessee’s disclosure about operating leases?A. Lease liabilities.B. Future obligations by maturity.C. Net carrying amounts of leased assets.

For a lessor, the leased asset appears on the balance sheet and continues to be depreciated when the lease is classified as:A. a sales-type lease.B. an operating lease.C. a financing lease.

Under US GAAP, a lessor’s reported revenues at lease inception will be highest if the lease is classified as:A. a sales-type lease.B. an operating lease.C. a direct financing lease.

A lessor will record interest income if a lease is classified as:A. a capital lease.B. an operating lease.C. either a capital or an operating lease.

Cavalier Copper Mines has $840 million in total liabilities and $520 million in shareholders’ equity. It discloses operating lease commitments over the next five years with a present value of $100 million. If the lease commitments are treated as debt, the debt-to-total-capital ratio is closest

Penben Corporation has a defined benefit pension plan. At 31 December, its pension obligation is €10 million and pension assets are €9 million. Under either IFRS or US GAAP, the reporting on the balance sheet would be closest to which of the following?A. €10 million is shown as a liability,

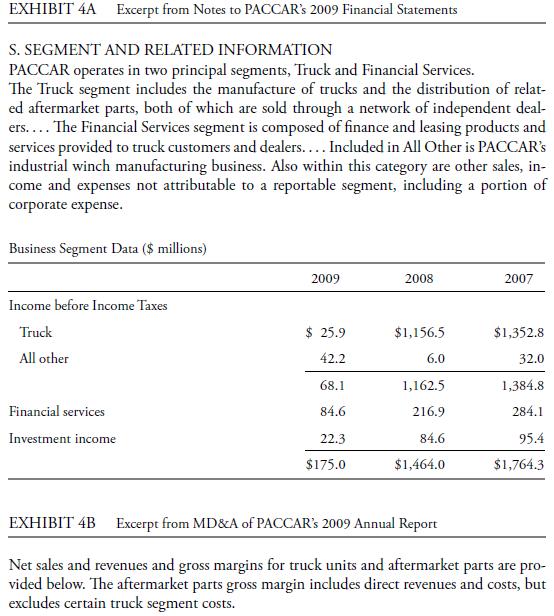

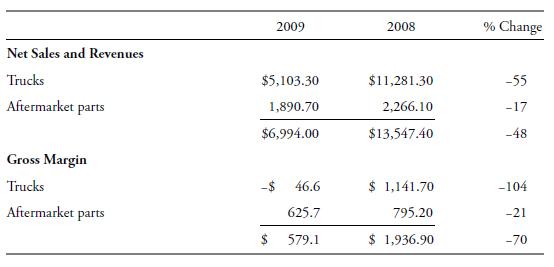

PACCAR Inc. (PCAR: NasdaqGS) designs, manufactures, and distributes trucks and related aftermarket parts that are sold worldwide under the Kenworth, Peterbilt, and DAF nameplates. In 2013, the US SEC charged PACCAR for various accounting deficiencies that “clouded their financial reporting to

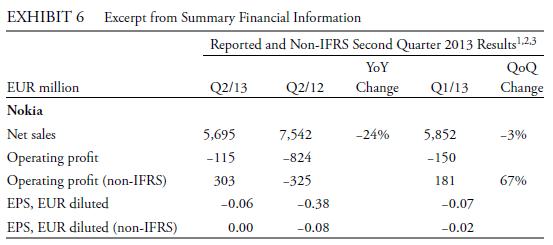

Nokia Corporation (NASDAQ OMX Helsinki and NYSE:NOK), a global telecommunications company headquartered in Finland, operates three businesses: Devices & Services, HERE (the new brand for location and mapping services, formerly called Location & Commerce), and Nokia Siemens Networks. Exhibit

Jake Lake, a financial analyst, has identified several items in the financial reports of several (hypothetical) companies. Describe each of these items in the context of the financial reporting quality spectrum.1. ABC Co.’s 2012 earnings totaled $233 million, including a $100 million gain from

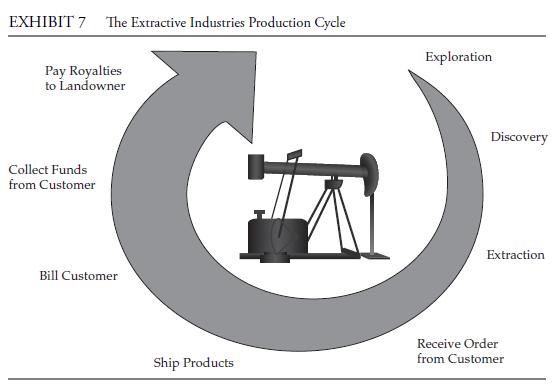

Exhibit 7 depicts the typical exploration and production operating cycle, beginning with exploration activities, through realization of cash from customers, and beyond, to the payment of royalties from cash collections that are often due to landowners and/or host governments.Under both IFRS and US

For each of the following two scenarios, identify(1) factors that might motivate the company’s managers to manipulate reported financial amounts(2) applicable mechanisms that could discipline financial reporting quality.1. ABC Co. is a private company. Bank NTBig has made a loan to ABC Co. ABC is

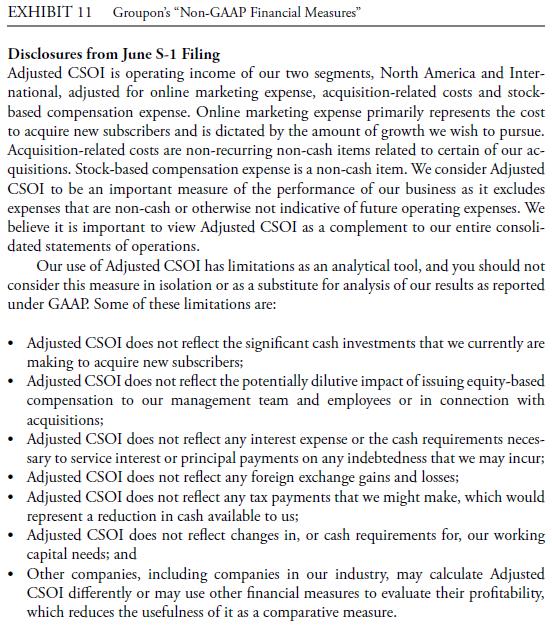

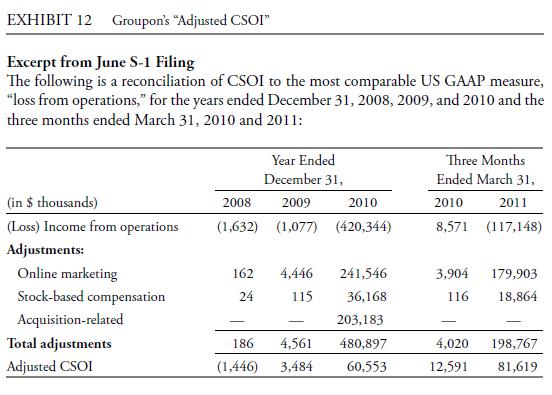

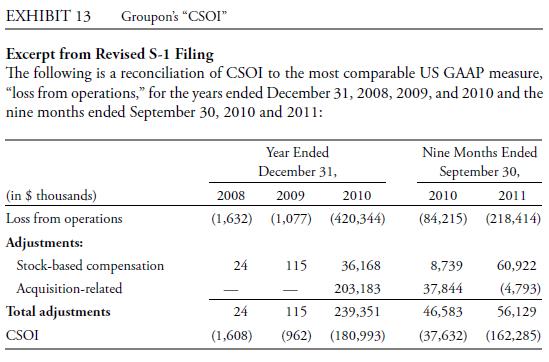

Groupon is an online discount merchant. In the company’s initial S-1 registration statement in 2011, then-CEO Andrew Mason gave prospective investors an up-front warning in a section entitled “We don’t measure ourselves in conventional ways.” He described Groupon’s adjusted consolidated

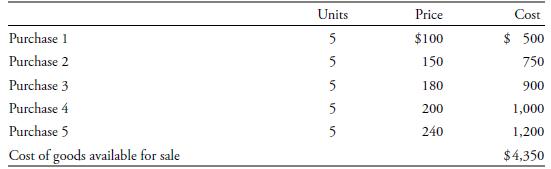

A company starts operations with no inventory at the beginning of a fiscal year and makes purchases of a good for resale five times during the period at increasing prices.Each purchase is for the same number of units of the good. The purchases, and the cost of goods available for sale, appear in

The information provided by a low-quality financial report will most likely :A. decrease company value.B. indicate earnings are not sustainable.C. impede the assessment of earnings quality.

To properly assess a company’s past performance, an analyst requires:A. high earnings quality.B. high financial reporting quality.C. both high earnings quality and high financial reporting quality.

Low quality earnings most likely reflect:A. low-quality financial reporting.B. company activities which are unsustainable.C. information that does not faithfully represent company activities.

Financial reports of the lowest level of quality reflect:A. fictitious events.B. biased accounting choices.C. accounting that is non-compliant with GAAP.

If a particular accounting choice is considered aggressive in nature, then the financial performance for the current period would most likely :A. be neutral.B. exhibit an upward bias.C. exhibit a downward bias.

Which of the following is most likely to reflect conservative accounting choices?A. Decreased reported earnings in later periods B. Increased reported earnings in the current period C. Increased debt reported on the balance sheet at the end of the current period

Which of the following statements most likely describes a situation that would motivate a manager to issue low-quality financial reports?A. The manager’s compensation is tied to stock price performance.B. The manager has increased the market share of products significantly.C. The manager has

A company is experiencing a period of strong financial performance. In order to increase the likelihood of exceeding analysts’ earnings forecasts in the next reporting period, the company would most likely undertake accounting choices that:A. inflate reported revenue in the current period.B.

Which of the following situations will most likely motivate managers to inflate earnings in the current period?A. Possibility of bond covenant violation B. Earnings in excess of analysts’ forecasts C. Earnings that are greater than the previous year

Which of the following best describes an opportunity for management to issue low-quality financial reports?A. Ineffective board of directors B. Pressure to achieve some performance level C. Corporate concerns about financing in the future

An audit opinion of a company’s financial reports is most likely intended to:A. detect fraud.B. reveal misstatements.C. assure that financial information is presented fairly.

If a company uses a non-GAAP financial measure in an SEC filing, then the company must:A. give more prominence to the non-GAAP measure if it is used in earnings releases.B. provide a reconciliation of the non-GAAP measure and equivalent GAAP measure.C. exclude charges requiring cash settlement from

A company wishing to increase earnings in the current period may choose to:A. decrease the useful life of depreciable assets.B. lower estimates of uncollectible accounts receivables.C. classify a purchase as an expense rather than a capital expenditure.

Bias in revenue recognition would least likely be suspected if:A. the firm engages in barter transactions.B. reported revenue is higher than the previous quarter.C. revenue is recognized before goods are shipped to customers.

Which of the following is an indication that a company may be recognizing revenue prematurely?Relative to its competitors, the company’s:A. asset turnover is decreasing.B. receivables turnover is increasing.C. days sales outstanding is increasing.

Which of the following would most likely signal that a company may be using aggressive accrual accounting policies to shift current expenses to later periods? Over the last five year period, the ratio of cash flow to net income has:A. increased each year.B. decreased each year.C. fluctuated from

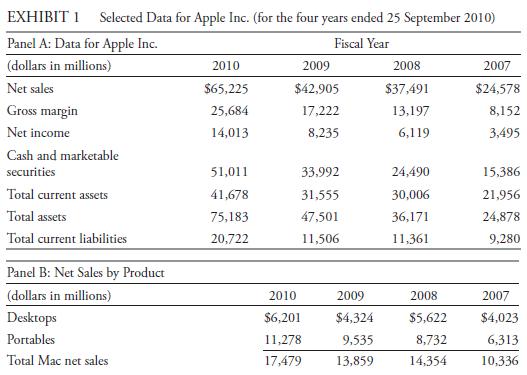

Apple Inc. (NASDAQ: AAPL) is a company that has evolved and adapted over time.In its 1994 Prospectus (Form 424B5) fi led with the US SEC, Apple identified itself as “one of the world’s leading personal computer technology companies.” At that time, most of its revenue was generated by computer

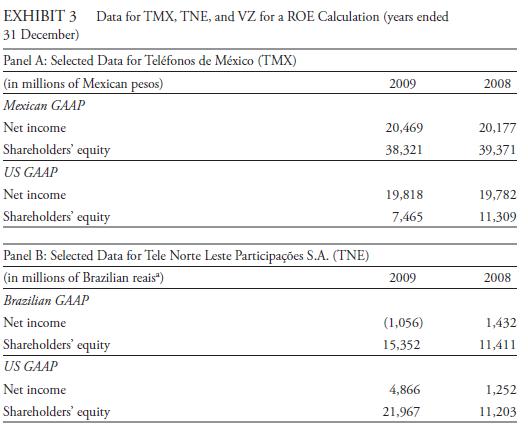

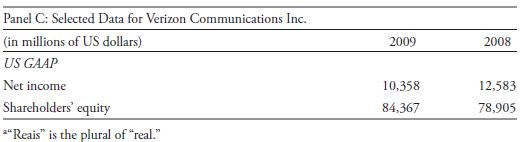

In the process of comparing the 2009 performance of three telecommunication companies—Teléfonos de México, S.A.B. DE C.V. (NYSE: TMX), Tele Norte Leste Participações S.A. (NYSE: TNE), and Verizon Communications Inc. (NYSE: VZ)—an analyst prepared Exhibit 3 to evaluate whether the

One approach to projecting operating profit is to determine a company’s average operating profit margin over the previous several years and apply that margin to a forecast of the company’s sales. Use the following information on three companies to answer Questions 1 and 2 below:• Johnson &

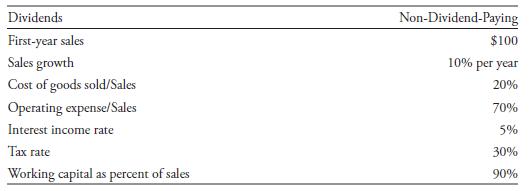

Assume a company is formed with $100 of equity capital, all of which is immediately invested in working capital. Assumptions are as follows:Based on this information, forecast the company’s net income and cash flow for five years. Dividends First-year sales Sales growth Cost of goods sold/Sales

Brown Corporation had an average days-of-sales-outstanding (DSO) period of 19 days in 2009. An analyst thinks that Brown’s DSO will decline in 2010 (because of expected improvements in the company’s collections department) to match the industry average of 15 days. Total sales (all on credit) in

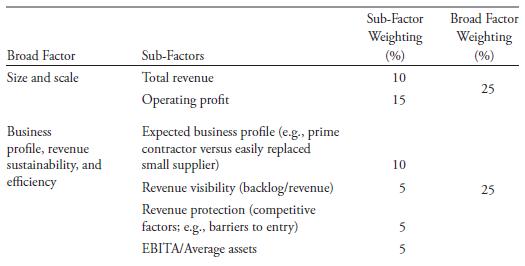

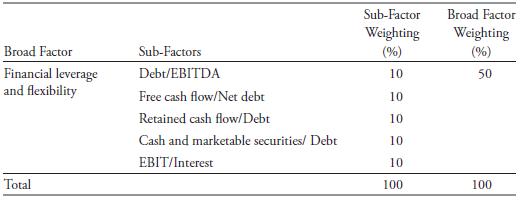

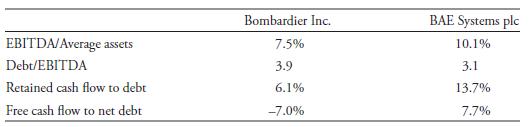

Moody’s considers a number of items when assigning credit ratings for the global aerospace and defense industry, including quantitative measures of three broad factors: size and scale; business profile, revenue sustainability, and efficiency; and financial leverage and flexibility. A company’s

A credit analyst is assessing the efficiency and leverage of two aerospace companies on the basis of certain sub-factors identified by Moody’s. The analyst collects the information from the companies’ annual reports and calculates the following ratios:Based solely on the data given, which

Below are two alternative strategies under consideration by an investment firm:Strategy A : Invest in stocks that are components of a global equity index, have a ROE above the median ROE of all stocks in the index, and have a P/E less than the median P/E.Strategy B : Invest in stocks that are

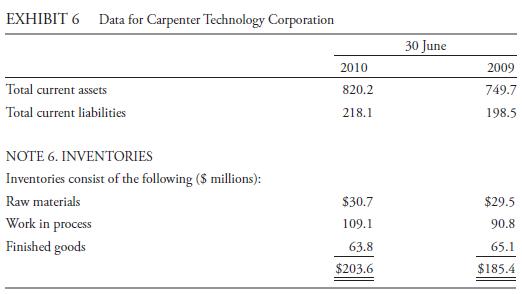

An analyst is comparing the financial performance of Carpenter Technology Corporation (NYSE: CRS), a US company operating in the specialty metals industry, with the financial performance of a similar company that uses IFRS for reporting. Under IFRS, this company uses the FIFO method of inventory

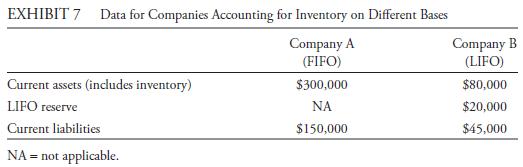

Company A reports under IFRS and uses the FIFO method of inventory accounting.Company B reports under US GAAP and uses the LIFO method. Exhibit 7 gives data pertaining to current assets, LIFO reserves, and current liabilities of these companies.Based on the data given in Exhibit 7 , compare the

An analyst is evaluating the financial statements of two companies in the same industry.The companies have similar strategies with respect to the use of equipment in manufacturing their products. The following information is provided (amounts in millions):1. Based on the information given, estimate

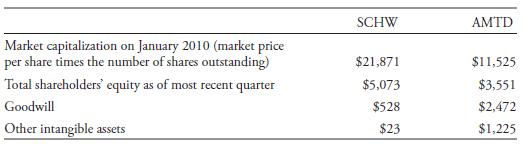

Miano Marseglia is an analyst who is evaluating the relative valuation of two securities brokerage companies: TD Ameritrade Holding Corporation (NasdaqGS: AMTD) and the Charles Schwab Corporation (NYSE: SCHW). As one part of an overall analysis, Marseglia would like to see how the two companies

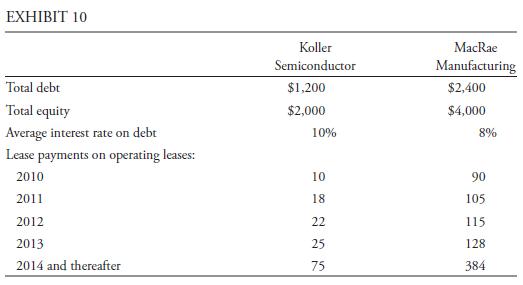

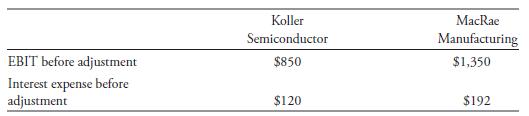

An analyst is evaluating the capital structure of two (hypothetical) companies, Koller Semiconductor and MacRae Manufacturing, as of the beginning of 2010. Koller Semiconductor makes somewhat less use of operating leases than MacRae Manufacturing.The analyst has the additional information in

The analyst is also evaluating the interest coverage ratio of the companies in the previous example, Koller Semiconductor and MacRae Manufacturing.The prior-year (2009) rent expense was $11 for Koller Semiconductor and $90 for MacRae Manufacturing.Using the information in Example 14 and the

Projecting profit margins into the future on the basis of past results would be most reliable when the company:A. is in the commodities business.B. operates in a single business segment.C. is a large, diversified company operating in mature industries.

Galambos Corporation had an average receivables collection period of 19 days in 2003.Galambos has stated that it wants to decrease its collection period in 2004 to match the industry average of 15 days. Credit sales in 2003 were $300 million, and analysts expect credit sales to increase to $400

Credit analysts are likely to consider which of the following in making a rating recommendation?A. Business risk but not financial risk B. Financial risk but not business risk C. Both business risk and financial risk

When screening for potential equity investments based on return on equity, to control risk, an analyst would be most likely to include a criterion that requires:A. positive net income.B. negative net income.C. negative shareholders’ equity

One concern when screening for stocks with low price-to-earnings ratios is that companies with low P/Es may be financially weak. What criterion might an analyst include to avoid inadvertently selecting weak companies?A. Net income less than zero B. Debt-to-total assets ratio below a certain cutoff

When a database eliminates companies that cease to exist because of a merger or bankruptcy, this can result in:A. look-ahead bias.B. back-testing bias.C. survivorship bias.

In a comprehensive financial analysis, financial statements should be:A. used as reported without adjustment.B. adjusted after completing ratio analysis.C. adjusted for differences in accounting standards, such as international financial reporting standards and US generally accepted accounting

When comparing financial statements prepared under IFRS with those prepared under US GAAP, analysts may need to make adjustments related to:A. realized losses.B. unrealized gains and losses for trading securities.C. unrealized gains and losses for available-for-sale securities.

When comparing a US company that uses the last in, first out (LIFO) method of inventory with companies that prepare their financial statements under international financial reporting standards (IFRS), analysts should be aware that according to IFRS, the LIFO method of inventory:A. is never

An analyst is evaluating the balance sheet of a US company that uses last in, first out(LIFO) accounting for inventory. Th e analyst collects the following data:After adjusting the amounts to convert to the first in, first out (FIFO) method, inventory at 31 December 2006 would be closest to:A.

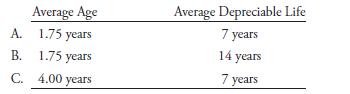

An analyst gathered the following data for a company ($ millions):The average age and average depreciable life of the company’s fixed assets at the end of 2001 are closest to: Gross investment in fixed assets Accumulated depreciation 31 Dec 2000 $2.8 $1.2 31 Dec 2001 $2.8 $1.6

Showing 1500 - 1600

of 1960

First

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

Step by Step Answers