New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

intermediate accounting volume 2

Intermediate Accounting Volume 2 5th Edition Thomas H. Beechy - Solutions

Analyze each case and choose a letter code under each category (type and approach) to indicate the preferable accounting for each case.a. Changed the expected useful lives of depreciable assets from 15 years to 10 years to conform with industry practice.b. Discovered that a capital asset with a 10

The following 10 situations all involve a change in accounting. For each situation, assume the company is public unless specified otherwise.a. Straight-line depreciation for the past three years has been calculated with no deduction for residual value because none was expected; management now

Accounting Changes: Mohammed Motors Limited made the following changes to its accounting in 20X5:a. Increased the interest rate used to discount its pension obligations from \(6.0 \%\) to \(6.5 \%\).b. Renewed a lease on a roof that the company has been using for a microwave transmission tower. The

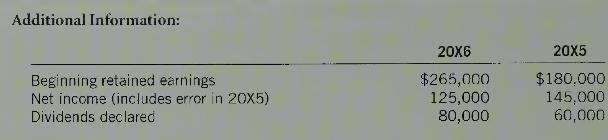

In 20X6, Cathode Company, a calendar fiscal-year company, discovered that depreciation expense was erroneously overstated \(\$ 40,000\) in both \(20 X 4\) and \(20 X 5\) for financial reporting purposes. Net income in \(20 X 6\) is correct. The tax rate is \(30 \%\). The error was made only for

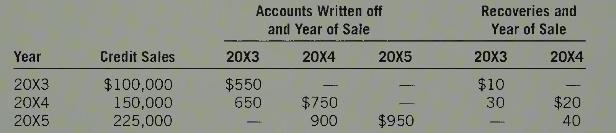

Betteroff Company was incorporated on 1 January 20X3. In the past, it has not provided an allowance for doubtful accounts. Instead, uncollectible accounts were expensed when written off and recoveries were credited to bad debt expense when collected. Accounts were written off if they were

Kate Limited has asked you to prepare appropriate journal entries for the following unrelated situations. There is no income tax.Case A An investment with an original cost of \(\$ 400,000\) was accounted for using the cost method in 20X0, 20X1, and 20X2. This year, 20X3, the company must conform to

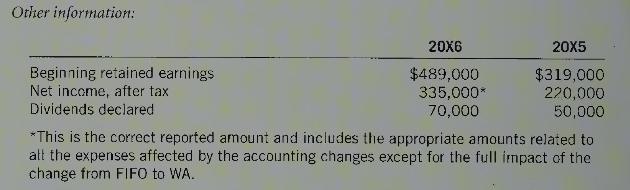

Armstrong Limited has used the average cost (AC) method to determine inventory values since first formed in \(20 X 3\). In \(20 X 7\), the company decided to switch to the FIFO method, to conform to industry practice. Armstrong will still use average cost for tax purposes. The tax rate is \(30

Zealand Company made several financial accounting changes in \(20 \mathrm{X} 6\) :First, the company changed the total useful life from 20 years to 14 years on a \(\$ 350,000\) asset purchased 1 January \(20 \mathrm{X} 2\). The asset was originally expected to be sold for \(\$ 50,000\) at the end

A company has always used the allowance method to value accounts receivable and establish a bad debt expense on the income statement. In the current year, it changed from using the aging method to the percentage of sales method to determine the extent of the required allowance. How would you

Why are changes in estimates so prevalent?

How is a change in accounting estimate accounted for?

A \(\$ 100,000\) asset is depreciated for six years on a straight-line basis using a 10 -year life and a \(\$ 10,000\) residual value. In year 7 , the remaining life is changed to five years, with a \(\$ 2,000\) residual value. How much depreciation expense should be recorded in year 7 ?

If there is doubt about whether a change is a change in policy or a change in estimate, how should it be treated? Why do you think accounting standards have this requirement?

Explain the difference between a voluntary and mandatory change in accounting policy.

What criteria must be met for a voluntary accounting policy change to be allowed? What difficulty is there in justifying a voluntary change?

What role do a company's reporting objectives play in changes in accounting policy?

Explain the difference between a change in estimate and an error correction.

Accounting changes involve (a) policies and (b) estimates. Using these letters and the letter (c) for error corrections, identify each of the following types of change:a. A lessor discovers, while a long-term capital lease term is in progress, that an estimated material unguaranteed residual value

How is an accounting error accounted for?

What are the advantages of retrospective restatement for a change in accounting policy? Why is it not required for all changes in accounting policy?

Assume that a company had traditionally expensed development costs but now satisfies capitalization criteria and thus has changed its policy. Explain how the change in development cost accounting will affect the cash flow statement.

Mountain Mines Lubrication Ltd. (MML), a Canadian private company, supplies lubricant to mining operations in northern British Columbia and the Northwest Territories. MML commenced operations four years ago and is based in Prince George, B.C. MML has two lubricant products: "Slip Coat" and "Maximum

Regional Airlines (RA) is a wholly owned subsidiary of National Commercial Airlines (NCA). Both companies prepare financial statements in accordance with International Financial Reporting Standards (IFRS). RA is reviewing the basis upon which it records depreciation on the fuselage of certain

Lalani Couture Limited (LCL) is a privately held company headquartered in Montreal. The company operates a chain of retail clothing stores in major cities across Canada, although the bulk of the company stores are in Ontario and Quebec. LCL manufactures most of its apparel in its facility in

Philip Roth is just finishing his first week as chief financial officer of MTC. He was recruited from Atkins Consulting to replace the former CFO who had been relieved of his duties when major errors and shortfalls in certain inventory and trading accounts were discovered.MTC is the current

What is the formula for basic EPS? Describe the numerator and the denominator.

Explain why and when dividends on non-cumulative preferred shares must be subtracted from earnings to compute basic EPS.

What adjustments, in addition to preferred dividends, may be made to the numerator of basic EPS?

Why are weighted-average ordinary shares used in EPS calculations?

If common shares are issued during the year under a contract that involved meeting a contingent requirement, as of what date are the shares included in the weighted average ordinary share calculation?

A company split its common shares 2-for-1 on 30 June of its fiscal year, which ends on 31 December. Before the split, 4,000 common shares were outstanding. How many weighted-average ordinary shares should be used in computing EPS? How many shares should be used in computing a comparative EPS amount

What is the required EPS disclosure if discontinued operations are reported?

Assume that a company has two classes of shares that both have voting rights and are entitled to the proceeds of net assets on dissolution. One class is entitled to receive 10 times the dividends of the other class. How would the two classes be treated in calculating basic EPS?

What is the purpose of diluted EPS?

A company has basic EPS based on earnings from continuing operations of \(\$ 4.50\) and on net earnings, \(\$ 3.50\). A potentially dilutive element has an individual effect of \(\$ 4.00\). Is the element dilutive or anti-dilutive?

Specify the numerator and/or denominator item(s) that would be used when calculating diluted EPS for dilutive (a) convertible preferred shares, (b) convertible debt, (c) contingently issuable shares, and (d) options.

Options are outstanding for 100,000 shares at \(\$ 10\). The average market price during the period is \(\$ 25\). What adjustment would be made to the denominator of diluted EPS?

What is the difference between a dilutive security and an anti-dilutive security? Why is the distinction important in EPS considerations?

What does it mean if options are said to be in-the-money? Are options dilutive when they are in-the-money? Explain.

A company has an agreement outstanding at the end of the fiscal year that requires it to issue common shares in the future for no additional cash consideration if certain conditions are met. How does the company decide whether to include the shares in diluted EPS or exclude them?

CH Holdings has basic EPS of \(\$ 14\). The individual effect of convertible preferred shares is \(\$ 12\), and the individual effect of convertible bonds is \(\$ 6\). In which order should the convertible elements be included in diluted calculations? In what circumstances would the convertible

ABC Company has a \(\$ 14\) million convertible bond outstanding that requires payment of \(\$ 1.2\) million in interest annually. Interest expense is \(\$ 1.35\) million. Why is interest expense different than the interest paid? For the purposes of diluted EPS, which interest figure is relevant?

Wilcorp Limited reported basic EPS of (\$1.11), a loss of \$1.11 per common share, calculated as \((\$ 610,500) \div 550,000\). The company has stock options outstanding for 100,000 common shares at \(\$ 10\) per share. The average common share price was \(\$ 25\) during the period. Calculate

Under what circumstances are the EPS of prior years to be restated?

A company with a 31 December year-end issues shares for cash and retires nonconvertible bonds with the proceeds on 10 January of the next fiscal year. What disclosure is required in the 31 December financial statements? Why?

Barbaro Ltd. plans to disclose a calculation of per share cash flow from operating activities in addition to EPS. What conditions must the company meet?

Drugstore Depot Limited (DDL) is a diversified Canadian company whose key businesses include retailing of drug store and food products, and real estate interests. Real estate is primarily held for DDL occupancy, although where DDL retail operations are an anchor tenant in a smaller mall, DDL

G Shoes Ltd. (GSL) is an integrated manufacturer and retailer of moderately priced highfashion footwear, leather goods, and accessories. GSL is a public company listed on the Toronto Stock Exchange. GSL has stores in over 180 major Canadian shopping malls, and operates over 50 "boutiques" in larger

ThurTech Limited (TTL) is a Canadian public company involved in network technology for mobility telecommunications. This network technology allows additional data services to be offered through a mobile platform, as a strategy to increase average revenue per user for the carriers. TTL's customers

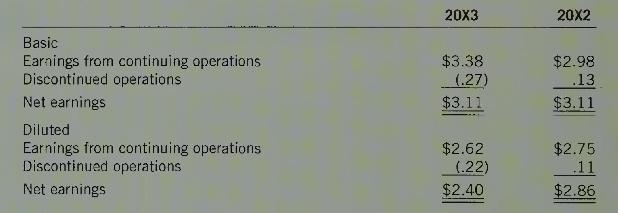

EPS information from the 20X3 Foran Resources Corp. financial statements is as follows:Required:1. Explain how basic EPS is calculated.2. Suggest a predicted target for basic EPS for 20X4, based on trends. Justify your choice.3. Explain the meaning of diluted EPS. What elements must Foran have in

The following cases are independent.Case A Reclamation Resources Limited had 2,860,000 common shares outstanding on 1 January 20X8. On 1 March, 286,000 common shares were issued as a \(10 \%\) stock dividend. On 1 June, 200,000 common shares were repurchased and retired. On 1 November, 400,000

The following cases are independent.Case A Knowledge Kingdom Corporation had 500,000 Series A shares and 250,000 Series B shares outstanding on January 1. Each non-voting Series A share has a \$2 per share cumulative dividend paid quarterly and is convertible into four Series B shares. Series B

In 20X2, McCullough Limited earned \(\$ 8,040,000\), and dividends of \(\$ 2,250,000\) were declared and paid. The company has two classes of voting shares. Class A shares have eight votes per share, while Class B shares have one vote per share. Both participate in the distribution of net assets in

Home Lake Mines Limited reported earnings of \(\$ 984,000\) in \(20 \mathrm{X} 8\) and declared no dividends. At the end of \(20 \mathrm{X} 8\), Home Lake Mines reported the following in the disclosure notes:Share CapitalMultiple Voting Shares: 400,000 shares are authorized but 60,000 shares were

On 1 January 20X1, Aker Aviation Services Ltd. entered into an agreement to purchase Moore Fuels Limited. The agreement included the following terms:1. Aker agreed to issue an additional \(2,000,000\) shares to the prior shareholders of Moore if Aker retained \(80 \%\) of the customers of Moore at

Wilcox Enterprises, a public company, is required to disclose earnings per share information in its financial statements for the year ended 31 December 20X6 . The facts about Wilcox's situation:a. At the beginning of the year, 450,000 common shares, issued for \(\$ 5.75\) million, were outstanding.

Waves Sound Solutions (WSS) reports the following calculations for basic EPS, for the year ended 31 December 20X4:Numerator: \(\quad\) Net earnings, \(\$ 18,600,000\), less preferred dividends of \(\$ 1,500,000\)Denominator: Weighted-average ordinary shares outstanding, \(6,240,000\)Basic EPS:

Information regarding Zhi Ltd:- Common shares outstanding on December 31, 20X1: 100,000. The company had issued 40,000 shares under a contingent share agreement on 1 December 20X2. It had also issued 50,000 common shares when preferred shares converted on 30 September \(20 \mathrm{X} 2\).- The

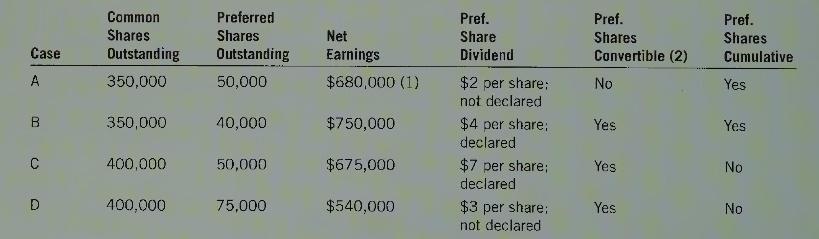

The following data relates to Gertron Ltd, a public company. Shares were outstanding for the entire year.(1) Includes \(\$ 135,000\) loss on discontinued operations in case A only.(2) If preferred shares are convertible, each preferred share is entitled to five common shares.Required:For each case,

MacDonald Company has reported basic earnings per Class A common share of \(\$ 2.61\). MacDonald has a tax rate of \(40 \%\). The average share price during the year was \(\$ 42\). Review each of the following items:A. Class B non-voting cumulative \(\$ 1\) shares, 75,000 shares outstanding all

Brandon Limited's statement of financial position at 31 December 20X2 reported the following:Additional data:a. During \(20 \mathrm{X} 2,30,000\) Class A shares were issued at \(\$ 50\) on 1 July. Dividends were declared and paid semi-annually, on 31 May and 30 November.b. Common share options are

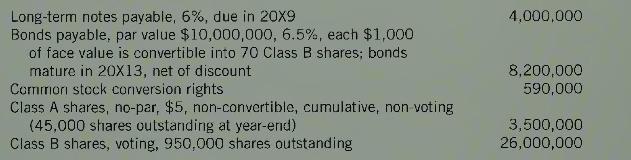

Interpretation: Marcella Corporation reported net earnings in 20X6 of \(\$ 1,345,000\), after an after-tax loss from discontinued operations of \(\$ 677,800\). Earnings from continuing operations was \(\$ 2,022,800\). The tax rate was \(30 \%\). Marcella reports the following information regarding

Carson Industries Limited (CIL) has a defined benefit pension plan covering all employees. The defined benefit obligation was \(\$ 7,004,000\) at the beginning of the current year, which is \(\$ 1,675,000\) higher than fund assets. Plan revaluation is done every three years, and plan improvements

TGY Limited has a defined contribution plan for its 160 employees. The plan is trusteed, and each year the company makes an annual contribution, matching employee contributions to the plan to a certain maximum. The funds are invested for the employees by the pension fund trustee using

A market analyst was quoted as saying:Defined benefit pension plans are really dead. Within 20 years, no companies in the private sector will be offering these plans - and the public sector is just daft if they don't follow suit. Why, in the first four months of this year, I know of dozens of

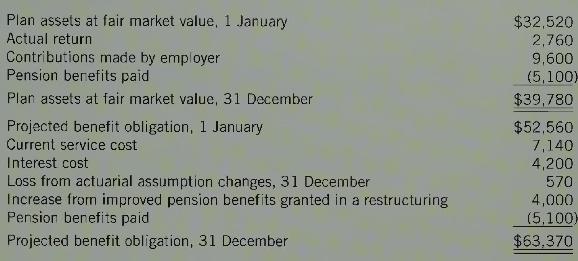

Belfiori Limited reports the following data for 20X8:The company has a contributory, defined benefit pension plan covering all employees over the age of 30 .Required:1. How much did the pension plan assets change during the year? Name three items that would cause plan assets to change.2. How much

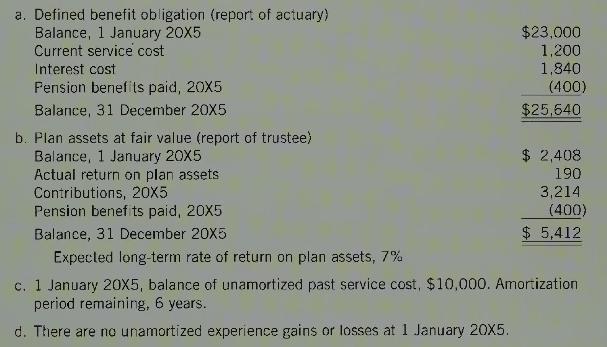

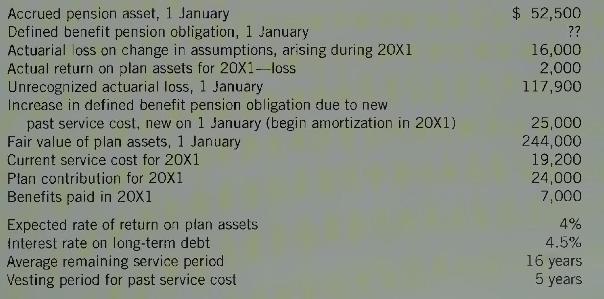

The following information relates to a defined benefit pension plan:Required:1. Provide the entries to record pension expense and cash paid to the trustee for 20X5. The company follows the practice of amortizing actuarial gains and losses to pension expense when the 1 January amount is outside the

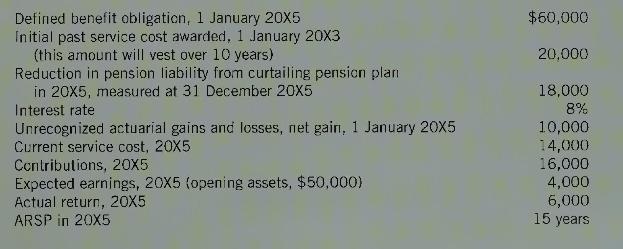

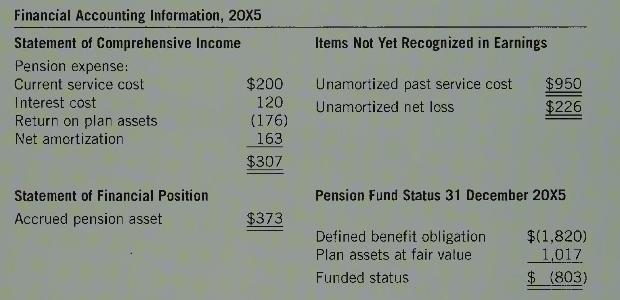

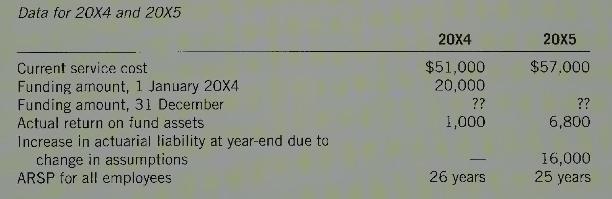

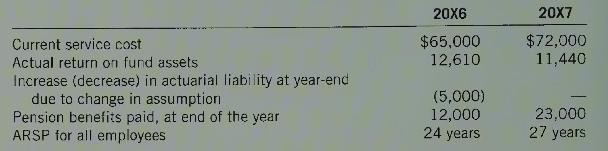

From Limited has a non-contributory, defined benefit pension plan. Pension plan data to be used for accounting purposes for the 20X9 year are as follows (in \(\$\) thousands):Required:1. Calculate pension expense for 20X9. The company follows the practice of amortizing actuarial gains and losses to

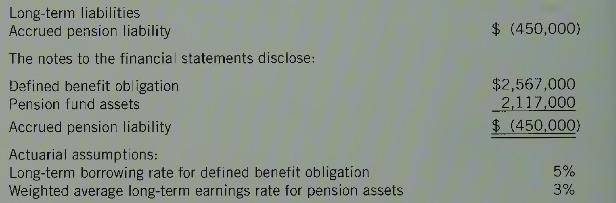

HTR Resources Ltd. has a non-contributory defined bencfit pension plan for its employees. At the beginning of \(20 \times 8\), there is unrecognized past service cost of \(\$ 4,380\) and unrecognized actuarial losses of \(\$ 5,460\) (all amounts in thousands). The data for \(20 \mathrm{X} 8\) is as

The 20X5 records of Jax Company provided the following data related to its non-contributory, defined benefit pension plan (in \(\$\) thousands):Required:1. Compute \(20 \times 5\) pension expense.2. Give the \(20 X 5\) entry(ies) for Jax Company to record pension expense and funding.3. Past service

Actuarial Gains and Losses: The following information relates to the pension plan of CCL Corporation, which has a contributory defined benefit pension plan:The following cases are independent.Case \(A\)CCL includes expected earnings at a rate of \(4 \%\) in the calculation of pension expense.

The following information relates to the pension plan of Butler Machinery Corporation, which has a contributory defined benefit pension plan:The following cases are independent.Case \(A\)Butler includes expected earnings at a rate of \(5 \%\) in the calculation of pension expense. Opening

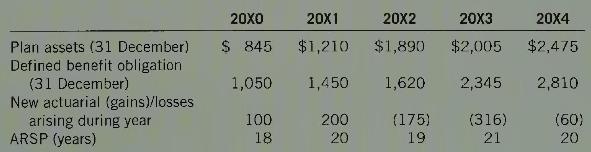

Lowen Limited has a defined benefit pension plan. Data with respect to the plan, which was initiated in \(20 \mathrm{X} 0\) (in thousands) is as follows:Required:1. Using the \(10 \%\) corridor rule, determine the actuarial gain or loss to be included in pension expense in each year from \(20

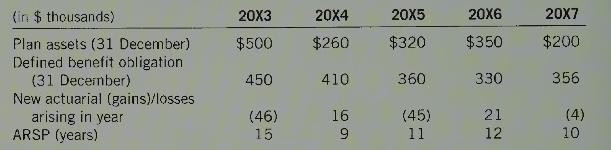

Fenerty Fabrics has a defined benefit pension plan that arose in \(20 X 3\). The following information relates to the plan:Required:1. What alternatives does Fenerty have to account for its actuarial gains and losses? Explain.2. For each year, what amount would be included in pension expense if

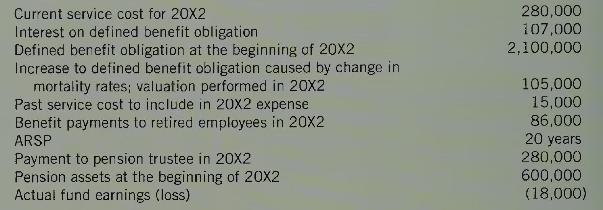

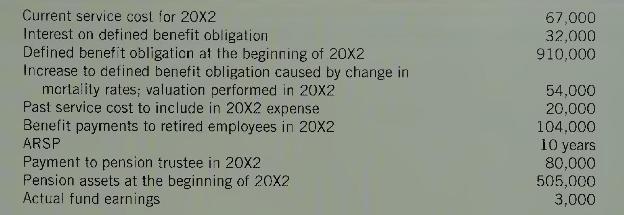

Okamura Construction Corp. has a defined benefitFrom the Plan Actuary:- Current service cost in \(20 \mathrm{X} 7\) is \(\$ 430,000\) and in \(20 X 8\) is \(\$ 488,000\).- Defined benefit obligation is \(\$ 4,975,000\) at the beginning of \(20 X 7\).- Unamortized past service cost at the beginning

Fox Company has a non-contributory, defined benefit pension plan adopted on 1 January \(20 X 5\). On 31 December 20X5, the following information is available:For accounting purposes- Interest rate used for discounting and asset return, \(5 \%\).- Past service cost, granted as of 1 January, \(\$

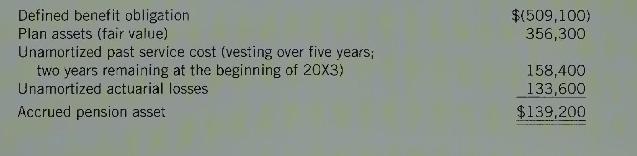

Super Sport Limited sponsors a defined benefit pension plan for its employees. At the beginning of \(20 \mathrm{X} 3\), there is a pension asset of \(\$ 139,200\), as follows:Required:1. Calculate the corridor test to establish required amortization of actuarial gains and losses in \(20 \times 3\)

The following information relates to the contributory defined benefit pension plan of Daniels Corporation:The information was prepared for the 20X5 annual financial statements and is accurate; the pension plan terms granted PSC entitlements in 20X2 when the plan was amended. The president of

In late 20X0, Winnipeg Valves Limited established a defined benefit pension plan for its employees. At the inception of the plan, the actuary determined the present value of the defined benefit obligation relating to employees' past services to be \(\$ 1\) million, as of the end of \(20 \mathrm{X}

Markon Consultants Limited began a pension fund in the year 20X3, effective 1 January 20X4. Terms of the pension plan follow:- The expected earnings rate on plan assets is \(6 \%\).- Employees will receive partial credit for past service. The past service obligation, valued using the projected

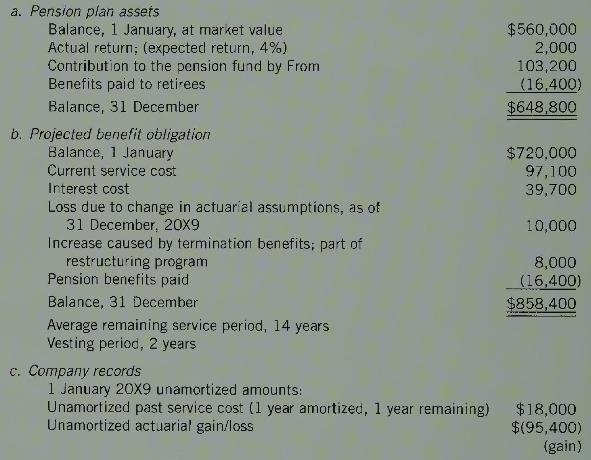

Comprehensive: Power Ltd. has a defined benefit pension plan. At the end of 20X0, the financial statements showed the following:Assumptions and policies have not changed in 20X1. Actual fund earnings in \(20 \mathrm{X} 1\) were a loss of \(\$ 156,000\). Current service cost was \(\$ 246,000\) in

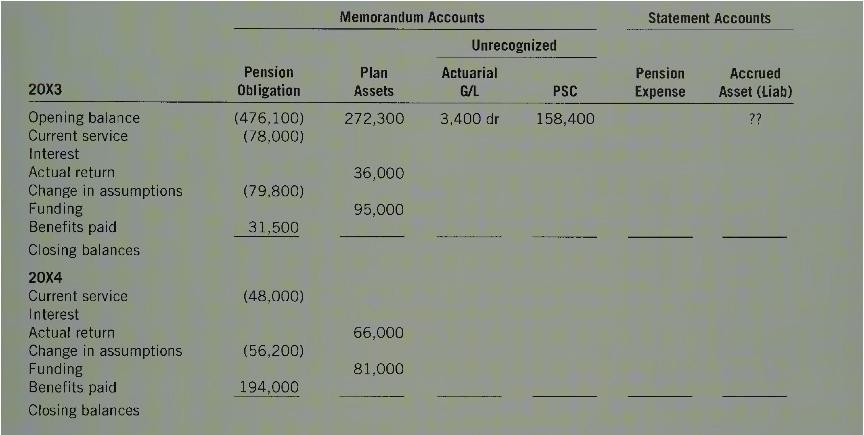

The following partial spreadsheet has been prepared:Required:Complete the spreadsheet. Label any lines added. The interest rate and earnings rate, as needed, is \(6 \%\) Assume that the amortization period for all amounts is 15 years. The company uses the \(10 \%\) corridor rule for actuarial gains

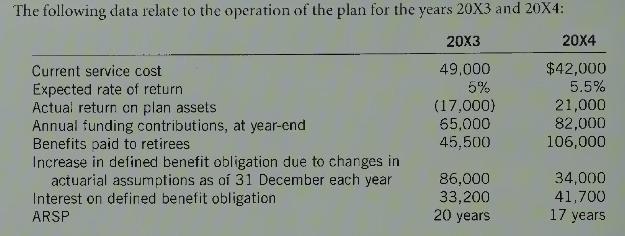

Scharf Limited has a defined benefit pension plan. The following information relates to this plan:Required:1. Calculate pension expense for \(20 \times 1\), and the closing balance of the recorded accrued pension asset. Reconcile the recorded pension asset balance to the assets and defined benefit

Neotech Industries (NI) was created in \(20 \mathrm{X} 0\). The company is in the optical equipment industry. Its made-to-order scientific and medical equipment requires large investments in research and development. To fund these needs, Neotech completed a public stock offering, in 20X4. Although

On 15 August 20X1, Argyle Ltd. signed a three-year lease to rent a computer system from Basil Ltd. for \(\$ 10,000\) per month. The lease will commence on 1 October 20X1. Three months' rent is payable at the lease inception; remaining rent is due at the beginning of each month. Basil will install

The Association of Western Agricultural Producers leases space in an office complex and has recently signed a new, five-year lease, at the rate of \(\$ 4,000\) per month. However, the lessor offered six months "free" rent at the beginning of the lease as an inducement for the Association to sign

Burrill Limited has an 7\% incremental borrowing rate at the local bank. On 1 January 20X1, Burrill signed the following lease agreement for a piece of equipment. The equipment has a fair value of \(\$ 170,000\) and a 12-year economic life. Other information is as follows:- The non-cancellable

Niko Limited signed a lease for a five-year term that requires yearly, beginning-of-year payments of \(\$ 104,000\), including \(\$ 9,600\) of annual maintenance and property taxes. Niko guarantees a residual value of \(\$ 26,500\) at the end of the lease term, although both parties expect the

Canadian Leasing Company leased a piece of machinery to Ornamental Concrete Limited, with the following terms:- The lease is for five years; Ornamental cannot cancel the lease during this period.- The lease payment is \(\$ 79,600\). Included in this is \(\$ 7,900\) in estimated insurance costs.- At

Entries: Lu Limited is expanding and needs more manufacturing equipment. The company has been offered a lease contract for equipment with a fair value of \(\$ 116,000\). The lease has a five-year term, end of year payment renewable for a further two years at the option of the lessee. Annual rental

Hui Corporation has negotiated a lease for new machinery. The machinery has a fair value of \(\$ 550,000\) and an expected economic life of seven years. The lease has a five-year term. Annual rental is paid at the beginning of the lease year, in the amount of \(\$ 104,300\). Insurance and operating

Consider each of the following lease arrangements:1. Abbaz Corporation signs a two-year lease for office space in a large, downtown office complex. Abbaz plans to have a permanent presence in the downtown area but has moved office premises several times in the past 10 years, motivated by factors

On 17 August 20X1, Renfrew Corporation negotiated a lease agreement with National Leasing Company (NLC) for computer equipment. The equipment has an expected economic life of 7 years and a fair market value of \(\$ 36,000\). The lease term is for 5 years, beginning on 1 October 20X1. Lease payments

Packard Limited is planning on leasing 150 desktop computers from Hewlett Corporation. The list price for the computers is \(\$ 2,000\) each, or \(\$ 300,000\) in total. The lease will be for three years, starting on 1 October \(20 \mathrm{X} 4\). The lease payments are \(\$ 26,000\) at the

Videos-to-Go signed a lease for a vehicle that had an expected economic life of eight years and a fair value of \(\$ 18,000\). The lessor is the leasing subsidiary of a national car manufacturer. The terms of the lease are as follows:- The lease term begins on 1 January 20X2, and runs for five

Access Limited has decided to lease office equipment with a fair market value of \(\$ 580,000\). The lease is with the Imperial Leasing Corporation, a U.S.-based subsidiary of a Japanese financial firm. The terms of the lease are as follows:- The initial lease term is five years. The lease

Implicit Interest Rate; Future Balance: Guido Limited is a retailer of home appliances. Guido leased a building for 25 years. The lease commenced on 1 January 20X1. The annual lease payment is \(\$ 820,000\), payable by the beginning of each lease year, and includes executory costs estimated at

Fair Value Cap: Christal Corporation leased equipment from Henan Leasing Limited for three years at \(\$ 30,000\) per quarter. The lease begins on 1 May 20X5. Payments are due at the end of each lease quarter (that is, the first payment will be due on 31 July 20X5). The fair value of the equipment

On 31 December 20X1, Lessee Limited entered into a lease agreement by which Lessee leased a jutling machine for six years. Annual lease payments are \(\$ 20,000\), payable at the beginning of each lease year (31 December). At the end of the lease, possession of the machine will revert to the

On 31 March 20X2, Supergrocery Inc., a private company, sold its major distribution facility, with a 30 -year remaining life, to National Leasing Company for \(\$ 9,000,000\) cash. The facility had an original cost of \(\$ 10,400,000\) and accumulated depreciation of \(\$ 3,600,000\) on the date of

Showing 1200 - 1300

of 2378

First

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

Last

Step by Step Answers