New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

intermediate accounting volume 2

Intermediate Accounting Volume 2 2nd Edition Hanlon, Hodder, Nelson, Roulstone, Dragoo - Solutions

Baltimore Inc. reported pretax GAAP income of \(\$ 45,000\) in 2020 . In analyzing differences between GAAP income and taxable income, the company determined that it had deducted \(\$ 5,000\) in nondeductible fines and added \(\$ 2,800\) in tax-exempt municipal interest revenue to GAAP income.

Refer to information in Brief Exercise 18-33. Prepare a reconciliation between Baltimore Inc.'s effective and statutory tax rates.Exercise 18-33Baltimore Inc. reported pretax GAAP income of \(\$ 45,000\) in 2020 . In analyzing differences between GAAP income and taxable income, the company

Lake Company has pretax GAAP income of \(\$ 100,000\) in 2020, its first year of operations. Lake Company has depreciation expense in 2020 for GAAP purposes that is \(\$ 60,000\) less than the amount of depreciation expense for tax purposes. In addition, \(\$ 5,000\) of regulatory fines included in

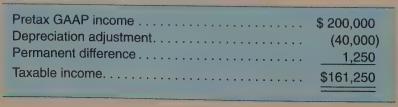

Evergreen Company's 2020 reconciliation between pretax GAAP income and taxable income is as follows. Pretax GAAP income.. Depreciation adjustment. Permanent difference. Taxable income.. $ 200,000 (40,000) 1,250 $161,250

The company had one temporary difference due to the GAAP basis of equipment exceeding the tax basis of the equipment. Record the income tax journal entry for 2020, assuming an enacted tax rate of \(25 \%\). Assume that the December 31,2019 , deferred tax liability balance was \(\$ 5,000\).

In 2020, Explorers Inc. completed installment sales of \(\$ 80,000\), recorded in full as accounts receivable and as revenue. For tax purposes, it recognizes income when cash is received. Cash related to the installment sales is expected to be received in the following years: 2021 of \(\$ 10,000 ;

The Jets Company recorded a deferred tax liability in the amount of \(\$ 18,750\) in December 2020, due to the book value of equipment exceeding the tax basis of equipment by \(\$ 75,000\). The difference will reverse equally over the next three years. In late 2020, the enacted tax rate increased

In 2020, Lambeau Inc. suffered a loss of \(\$ 100,000\). The enacted tax rate is \(25 \%\). Prepare Lambeau's entry for the loss carryforward on December 31, 2020, assuming that management determined that it was more likely than not that the deferred tax asset would be realized.

In 2020, Cardinals Company operated at a tax loss, totaling \(\$ 88,000\) during its first year of business. Assuming a tax rate of \(25 \%\), and that income is expected in 2021 , record the entry to reflect the tax benefit of the net operating loss on December 31, 2020. Cardinals Company

Springs Inc. has taken a tax position in 2020 that it believes is based on fairly clear tax law for the payment of \(\$ 80,000\) in salaries and benefits to employees. There are no limits on deductibility and all amounts were fully paid within the statutory time limit, although there is some

Kate Club Inc. has determined that there are four temporary differences between the tax basis and the GAAP book value of assets and liabilities that resulted in the following deferred taxes: (a) deferred tax liability related to accelerated tax depreciation over straight-line depreciation: \(\$

The following information was obtained from recent annual reports on \(10-\mathrm{K}\) for American Eagle Outfitters, Inc. Compute the debt-to-equity ratio (a) including deferred tax liabilities as part of total liabilities, and (b) excluding deferred tax liabilities as part of total liabilities. $

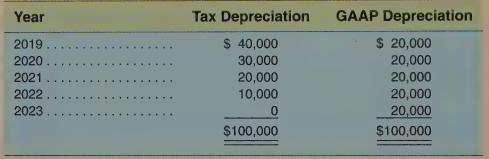

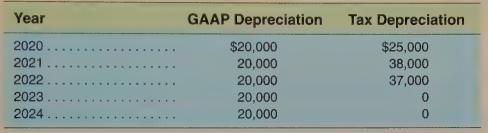

Staples Corporation would have had identical income before taxes on both its income tax returns and its income statements for the years 2020 through 2023 except for a depreciable asset that cost \(\$ 120,000\). The asset was depreciated for income tax purposes using the following amounts: \(2020,

Repeat the requirements of Exercise 18-44, but now assume that the asset was \(100 \%\) expensed for tax purposes in 2020.Exercise 18-44Staples Corporation would have had identical income before taxes on both its income tax returns and its income statements for the years 2020 through 2023 except

For 2020, Trendy Inc. calculated taxable income of \(\$ 30,000\) after taking into account one temporary difference: prepaid insurance expense on a GAAP basis exceeds prepaid insurance on a tax basis by \(\$ 5,000\). The tax rate is \(25 \%\) and there were no balances in deferred tax accounts at

On December 31, 2020, for GAAP purposes, Clubs Inc. reported a balance of \(\$ 70,000\) in Prepaid Maintenance Expense for services to be received over the following year. For tax purposes, however, prepaid costs are deducted immediately when paid. Pretax GAAP income is \(\$ 300,000\) and the tax

On December 31, 2020, for GAAP purposes, Clubs Inc. reported a balance of \(\$ 40,000\) in a warranty liability for anticipated costs to satisfy future warranty claims. No claims were paid in 2020. Pretax GAAP income is \(\$ 300,000\) and the tax rate is \(25 \%\). Assume no other differences

The records of Anderson Inc. provide the following information for the tax year 2020.- There was no beginning balance in deferred tax account(s).- Taxable income for 2020 was \(\$ 60,000\).- Tax rate is \(25 \%\).- Three temporary differences were identified:1. Estimated litigation accrual of \(\$

Lake Company has the following results of operations on December 31, 2020.1. Pretax GAAP income in 2020 , its first year of operations, totals \(\$ 100,000\). Taxable income is \(\$ 90,000\).2. Lake Company recorded an installment sale receivable totaling \(\$ 60,000\), with a tax basis of \(\$

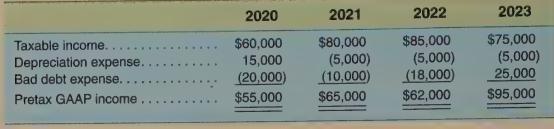

The records of Cross Corporation provided the following reconciliation between taxable income and pretax GAAP income.- The depreciation adjustment results from a difference between the GAAP basis and tax basis of depreciable equipment.- The bad debt expense adjustment results from a difference

The records of TNA Corporation at the end of 2020 provided the following data related to income taxes.- Unrealized gain on the company's investment portfolio, \(\$ 50,000\); recognized in net income for accounting purposes at the end of 2020 . Amount will be considered for tax purposes when sold,

The following information is available for Rapper Inc.- Taxable income in 2020: \(\$ 115,000\)- Accounts receivable on installment sales • GAAP basis: \(\$ 150,000\)• Tax basis: \(\$ 0\)- Tax rate: \(25 \%\)- Deferred revenue on services • GAAP basis: \(\$ 35,000\)• Tax basis: \(\$ 0\)-

For 2020, Raleigh Corporation had taxable income of \(\$ 100,000\) and an income tax rate of \(25 \%\). Raleigh had a \(\$ 75,000\) credit balance in its Deferred Tax Liability account. This credit balance was due to the following two temporary differences.- Carrying value of equipment for

Cruse Corporation started operations on January 1,2020 . Taxable income from the tax return is \(\$ 2,850,000\). Income tax rate is \(25 \%\). There were no beginning balances in deferred tax accounts.Additional information- On December 31, 2020, GAAP basis of installment sale receivables, \(\$

A-1 Company had pretax GAAP income of \(\$ 50,000\) for the tax year ended December \(31,2020\).Requireda. Determine taxable income given the following separate situations.1. Excess accelerated depreciation for tax purposes, \(\$ 5,000\)2. Unrealized holding gain on securities accounted for under

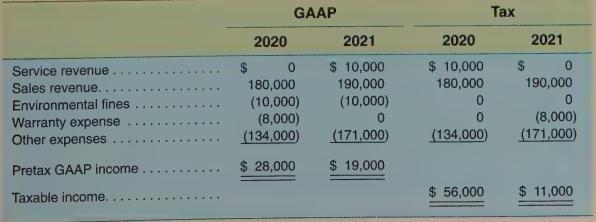

The income statements for Prince Inc. for two years (summarized) follow.Additional information - Environmental fines are not deductible for income tax purposes.- The amount collected in 2020 related to deferred service revenue \((\$ 10,000)\) was taxable in 2020.- Accrued warranty costs of \(\$

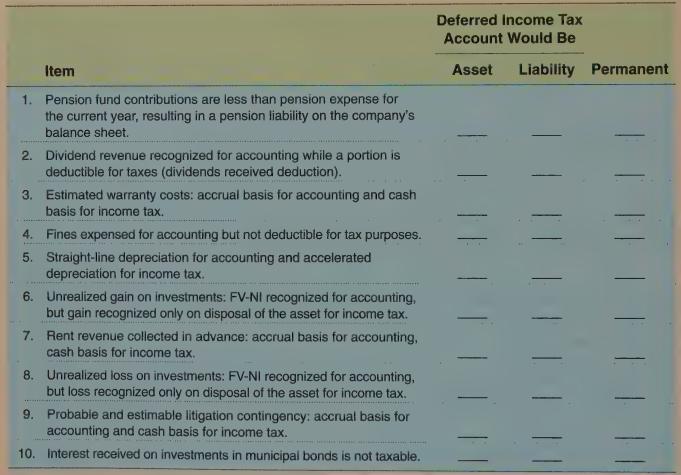

Listed below are ten separate situations. For each item indicates whether the difference is (1) temporary creating a deferred tax asset or a deferred tax liability or (2) permanent. Item 1. Pension fund contributions are less than pension expense for the current year, resulting in a pension

Fox Corporation purchased a machine on January 1,2020 , that cost \(\$ 40,000\). The machine had an estimated service life of five years and no residual value. Fox uses straight-line depreciation for accounting purposes and accelerated depreciation for the income tax return as follows: \(2020,30 \%

Allied Corp. has a deferred tax asset balance of \(\$ 50,000\) on December 31,2020 , due to a temporary difference related to a warranty expense accrual that is not deductible for tax purposes. The deferred tax asset balance has increased \(\$ 10,000\) over the prior year ending balance of \(\$

Assume the same information in Exercise 18-61, except that there is a \(\$ 12,000\) beginning balance in the valuation allowance.Requireda. Record the income tax journal entries on December 31, 2020, assuming that it is more likely than not that the deferred tax asset will be realized.b. Record the

Wittco Company reports pretax GAAP income in 2020, its first year of operations, of \(\$ 100,000\). Temporary differences in the GAAP basis and tax basis of assets arose in 2020 from the following two sources.- Prepayment of 2021 rent in the amount of \(\$ 24,000\) in 2020.- An installment sale

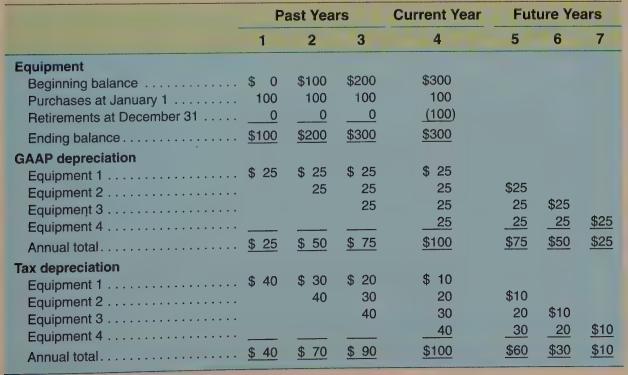

On January 1 of each of the first four years of its existence, Allway Company purchases a new unit of equipment. Each unit has a four-year life and zero salvage value, costs \(\$ 100,000\), and is depreciated for GAAP and tax purposes as shown below. The income tax rate is \(25 \%\). Allway has a

The Billboard Company has a deferred tax liability in the amount of \(\$ 14,000\) at December 31, 2020, relating to a \(\$ 40,000\) installment sale receivable, \(\$ 20,000\) of which is collected in 2021 . The tax rate in 2021 is \(35 \%\). However, the rate for 2022 and thereafter is changed

In 2020, Adele Company accrued a legal liability of \(\$ 500,000\) for payments expected to be paid (and will be deducted when paid) as follows: 2021 : \(\$ 250,000 ; 2022\) : \(\$ 150,000\); and \(2023: \$ 100,000\). The company's pretax GAAP income is \(\$ 5\) million. Enacted tax rates are as

A plant asset purchased by Krest Inc. for \(\$ 100,000\) late in 2018 is to be depreciated as follows.In 2020 , taxable income was \(\$ 450,000\) and the tax rate is \(25 \%\). Future enacted tax rates are as follows: 2021 ; \(25 \% ; 2022: 30 \%\); and 2023: \(30 \%\). The deferred tax liability

On December 31, 2020, Colgait Inc. had an installment sale receivable balance of \(\$ 90,000\) recognized on its financial statements, while the amount was not recognized for tax purposes. Colgait Inc. also had a warranty accrual of \(\$ 20,000\) on December 31,2020 , that is not deductible for tax

Aim Inc. had the following activity for the years 2020-2022.- Prepaid maintenance contract: \(\$ 30,000\) on January 1,2020 , for a three-year period beginning January 1 , 2020.- Deferred revenue: \(\$ 45,000\) on January 1,2020 , for a three-year period beginning January \(1,2020\).- Pretax GAAP

Tyson Corporation reported pretax income from operations in 2020 of \(\$ 80,000\) (the first year of operations). In 2021, the corporation experienced a \(\$ 40,000\) NOL (pretax loss from operations). Management is confident the company will have taxable income in excess of \(\$ 50,000\) in 2022.

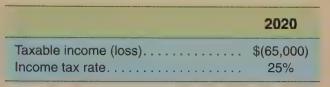

Decker Corporation experienced a loss in 2020. Additional information for Decker Corporation follows.There were no temporary differences from 2018 to 2020 other than any related to a net operating loss carryforward.Requireda. Record income taxes for 2020 and 2021 assuming the following.- For 2021,

Toner Corporation computed the following taxable income and loss: 2020 taxable income, \(\$ 10,000\) and 2021 taxable loss, \(\$ 40,000\). At the end of 2021 , Toner made the following estimates: 2022 taxable income, \(\$ 4,000,2023\) taxable income, \(\$ 11,000\), and 2024 taxable income, \(\$

DNSE Inc. began operations in 2019. In its first year the company had a net operating loss of \(\$ 10,000\), which was carried forward and used to reduce income tax payable in 2020. In 2020, DNSE had taxable income of \(\$ 40,000\) before the use of the NOL carryforward. At December 31, 2020, DNSE

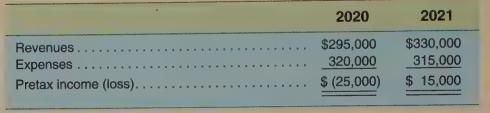

The financial statements of Gibson Corporation for the first two years of operations reflected the following amounts.Assume a tax rate of \(25 \%\) for 2020 and 2021.Estimates of future earnings at the end of each year, 2020 and 2021 are zero. There are no temporary differences.Requireda. Provide

ABC Inc. reported taxable income for the years 2019-2023 as follows.The enacted tax rate is \(25 \%\). There are no differences between taxable income/loss and GAAP income/loss. Management believes that the full amount of tax loss carryforward benefit is more likely than not to be

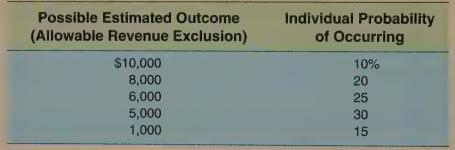

Randolph Inc. considered the probability of a recent tax position taken related to the exclusion of certain revenues of \(\$ 10,000\) from taxable revenue. Randolph determined that this position is more likely than not to be sustained in future discussions with taxing authorities. Using available

In 2020, Rafting Inc, had pretax GAAP income of \(\$ 100,000\) and the federal statutory tax rate is \(25 \%\). Rafting Inc. has no temporary differences, and so there is no deferred tax component to income tax expense. However, Rafting Inc. has the following permanent difference items.- Fines paid

The following items create deferred tax assets and deferred tax liabilities at December 31, 2020.1. Prepaid operating expenses of \(\$ 25,000\) are tax deductible when paid.2. Excess tax depreciation (MACRS) over GAAP depreciation (straight-line) is \(\$ 22,000\).3. Warranty liability of \(\$

On January 1, 2020. Keefe Corporation purchased equipment at a cost of \(\$ 100,000\). The equipment has a fiveyear life and no salvage value. The depreciation schedule for tax and accounting purposes follows.Pretax GAAP income for each year 2020 through 2023 is \(\$ 120,000\) and the tax rate is

Refer to the data and information given in Problem 18-79 for Keefe Corporation. Assume that the tax rate for 2020 through 2022 is known to be \(25 \%\), but that a new law is passed in 2020 that will raise the tax rate in 2023 and thereafter to \(30 \%\). Assume pretax GAAP income equals \(\$

Whirlpools Corporation provided the following information: taxable income based on its 2020 tax return, \(\$ 47,600\); income tax rate, \(25 \%\). There were two temporary differences.- December 31, 2020, collected rent in advance for 2021, resulting in deferred rent revenue of \(\$ 5,000\). The

Terms frequently used in accounting for income tax along with descriptions of the terms are included in the following two lists.Terms- 1. Deferred tax asset _ 2. Taxable temporary difference- 3. Permanent difference _ 4. Valuation allowance- 5. Temporary difference _ 6. Taxable income- 7.

What are the advantages of leasing from the lessee's perspective?

What is meant by capitalization of a lease from the viewpoint of the lessee?

What types of leases are capitalized by a lessee? Under what condition would a lessee not capitalize a lease?

From a lessee's standpoint, leases are classified as finance or operating leases. What criteria are used to identify a finance lease?

What lease payments are used in determining whether the present value of lease payments is greater than or equal to substantially all of the fair value of the underlying asset?

How is a lease liability calculated?

How is a right-of-use asset calculated?

How does a lessee determine what interest rate is appropriate to discount the lease liability?

How does an unguaranteed residual value in a sales-type lease affect the lessor's accounting in recording the entries at the date of inception of the lease?

How is a guaranteed residual value treated differently by the lessee when determining the classification of leases as compared to the recording of a lease liability?

Define initial direct costs.

How does a lessee derecognize a right-of-use asset and lease liability over the term of an operating lease?

How does a lessee derecognize a right-of-use asset and lease liability over the term of a finance lease?

If a lessee records a right-of-use asset related to a finance lease, over what period would the lessee recognize amortization expense? What conditions impact your answer?

How does a lessor account for an operating lease?

How does a lessor account for a sales-type lease?

If a lessor determines that payments from a lessee pertaining to a sales-type lease are not probable, how would the lessor account for the lease?

What qualifies as a short-term lease and how would a lessee account for a short-term lease?

What determines whether a lease modification results in a separate lease or in a modification of an existing lease?

What types of qualitative information should be disclosed about a company's leases?

On January 1, 2020, Lessee Company leases equipment with a fair value of \(\$ 2,000\) from Lessor Company for 3 years, with no renewal options. The estimated life of the equipment is 5 years and there is no purchase option at the end of the lease term. The annual lease payment is \(\$ 700\), which

On January 1, 2020, Lessee Company leases a vehicle with a fair value of \(\$ 30,000\) from Lessor Company for 3 years, with no renewal options. The estimated life of the vehicle is 6 years and Lessee Company has an option to purchase the vehicle at lease end at the vehicle's fair value which the

A lessee is evaluating whether a lease term is a major part of the remaining life of an asset in order to determine the proper lease classification. The lessee leases office space through a lease with a 10 -year term. The lease has a renewal option for an additional 5 years at a rental price that

For each of the following four separate finance lease scenarios, determine the lease payment that the lessee should use to determine the appropriate lease classification.a. Lease payments are \(\$ 3,000\) per month plus \(5 \%\) of lessee net sales. Lessee sales for year one are estimated to be

For each of the following four separate finance lease scenarios, determine the lease payment that the lessee should use to determine the appropriate lease classification.a. An annual lease payment for equipment was \(\$ 50,000\) and included a fee of \(\$ 5,000\) for maintenance of the equipment.b.

Pier10 Inc. entered into a 5-year lease and recorded a right-of-use asset and lease liability of \(\$ 88,000\) on January 1, 2020. Pier10 Inc. was aware of the lessor's implicit rate of interest of 5\%. The equipment under lease had an estimated 5-year useful life with no residual value. The first

Referring to the information in Brief Exercise 17-26, show the balance sheet presentation on December 31, 2020, and the income statement presentation for the year ended December 31, 2020.Exercise 17-26Pier10 Inc. entered into a 5-year lease and recorded a right-of-use asset and lease liability of

Lessee Company enters into a 6-year finance lease of non-specialized equipment with Lessor Company on January 1,2020 . Lessee has agreed to pay \(\$ 28,000\) annually beginning immediately on January 1,2020 . The lessor estimates the residual value of the equipment to be \(\$ 5,000\) at lease end,

Referring to the information in Brief Exercise 17-28, assume the same information except that the lessee guaranteed the residual value for \(\$ 5,000\) at the end of the lease term. Compute the value of the lease liability for the lessee on January 1,2020 , under the following separate scenarios.a.

Lessee Company enters into a 6-year finance lease of non-specialized equipment with Lessor Company on January 1,2020 . Lessee has agreed to pay \(\$ 28,000\) annually beginning immediately on January 1,2020 . The lease includes an option for the lessee to purchase the equipment at \(\$ 3,000\),

Smith, the lessee, signs an 8-year lease agreement of a floor of a building on December 31, 2020 that requires annual payments of \(\$ 70,000\), beginning immediately. The residual value is guaranteed to the lessor of \(\$ 50,000\) at the end of the lease term. Smith estimates that the residual

Frontier Inc. enters into an 8 -year lease contract to lease equipment with a useful life of 8 years. Annual lease payments are due with the first payment made immediately on January 1, 2020, the commencement of the lease. No residual value is expected or guaranteed of the underlying equipment.

Franklin Co. leased its manufactured equipment to Parker Inc. for a 4-year term. Franklin Co. reported a book value of \(\$ 55,000\) for the equipment in its inventory account. The lease commenced on January 1,2020 , with the first annual payment of \(\$ 18,500\) due immediately. The equipment has

Referring to the information in Brief Exercise 17-33, record Franklin's required journal entry to record interest revenue on December 31, 2020.Exercise 17-33Franklin Co. leased its manufactured equipment to Parker Inc. for a 4-year term. Franklin Co. reported a book value of \(\$ 55,000\) for the

Referring to the information in Brief Exercise 17-33, record Franklin's required journal entry at the commencement of the lease, assuming that the collectibility of payments is not probable.Exercise 17-33Franklin Co. leased its manufactured equipment to Parker Inc. for a 4-year term. Franklin Co.

Kelly Inc. leased equipment, originally reported in inventory, to General Engines Inc. for a 4-year lease term and recorded the lease as a sales-type lease. At the expiration of the lease, the equipment had a fair value equal to the guaranteed residual value of \(\$ 13,000\), and was returned to

Referring to the information in Brief Exercise 17-31, record the lessor's journal entries on December 31, 2020, assuming that the lease is properly classified as a sales-type lease. The carrying value of the equipment is \(\$ 450,000\) at the commencement of the lease.Exercise 17-31Smith, the

A lessor, Ace Corp. enters into an equipment lease with a lessee, Spades Inc. The terms of the lease require annual lease payments of \(\$ 48,000\) over a 10 -year period, with the first payment due immediately upon the commencement of the lease on January 1,2020 . There is no estimated residual

Hearts Inc. (Lessor) enters into a 10-year lease of equipment with Spades Inc. (Lessee) on January 1, 2020. Hearts Inc. sells and leases the equipment, which is not specialized in nature and is expected to have alternative use to Hearts Inc. at the end of the 10 -year lease term. Under the lease,

Konverse Inc. is negotiating an agreement to lease equipment to a lessee for 6 years. The fair value of the equipment is \(\$ 50,000\) and the lessor expects a rate of return of \(7 \%\) on the lease contract and no residual value. If the first annual payment is required at the commencement of the

Armstrong Inc. is negotiating an agreement to lease equipment to a lessee for 5 years. The fair value of the equipment is \(\$ 150,000\) and the lessor expects a rate of return of \(6 \%\) on the lease contract. The lessee has an option to purchase the equipment at the end of the 5 -year term at

Marshall Inc. is negotiating an agreement to lease equipment to a lessee for 5 years. The equipment has a useful life of 8 years. The fair value of the equipment is \(\$ 80,000\) and the lessor expects a rate of return of \(5 \%\) on the lease contract. Marshall Inc. expects the equipment to have a

Quest Inc. is negotiating an agreement to lease equipment to a lessee for 8 years. The equipment has a useful life of 10 years. The fair value of the equipment is \(\$ 40,000\) and the lessor expects a rate of return of \(8 \%\) on the lease contract. The lessee guarantees a residual value of \(\$

Solutions Inc. signs a 10-year lease for a building owned by Property Inc. that is appropriately classified as an operating lease by both the lessee and lessor. Lease payments are \(\$ 150,000\) per year. The building has an estimated useful life of 30 years with no salvage value. What amount would

Gomez Inc. leases a vehicle from CareMax Inc. on January 1, 2020, for a three-year period, appropriately classified by Gomez Inc. as an operating lease. Gomez agrees to make \(\$ 6,000\) annual payments beginning on January 1, 2020. Prepare the journal entries for Gomez in 2020 assuming that Gomez

Lessor Co. enters into an operating lease of property with Lessee Co. on January 1, 2020, for a five-year term at an annual fixed lease payment of \(\$ 10,000\) (beginning of period payments). Prepare the journal entries in 2020 for the lessee assuming that the lessee is aware of the rate implicit

Kulver's Inc. leases equipment from Equip Inc. on January 1, 2020, under a 3-year operating lease. Kulver's agrees to pay Equip Inc. \(\$ 15,000\) annually with the first payment due on January 1, 2020. As an incentive for Kulver's to sign the lease by January 1, Equip Inc. paid Kulver's Inc. \(\$

Referring to the information in Brief Exercise 17-44, and assuming that the building has a fair value of \(\$ 2,000,000\) at the commencement of the lease, what amount would Property Inc. recognize in its income statement (ignoring taxes) for the year ended December 31, 2020? Assume that Property

Referring to the information in Brief Exercise 17-45, prepare the journal entries in 2020 for CareMax Inc. assuming that the fair value of the vehicle is \(\$ 28,000\) and it has a useful life of 6 years with no salvage value (depreciated using the straight-line method).Exercise 17-45Gomez Inc.

Universal Inc. signed a contract to lease equipment for a 4-year term on January 1,2020 , for \(\$ 20,000\) annually beginning immediately. The lease included a purchase option at the end of the lease for \(\$ 8,000\), that at the commencement of the lease, Universal did not believe would exercise.

Showing 800 - 900

of 2378

First

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

Last

Step by Step Answers