New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

intermediate accounting volume 2

Intermediate Accounting Volume 2 5th Edition Thomas H. Beechy - Solutions

Share Issuance: Lake Simcoe Limited (LSL) has unlimited no-par common shares authorized. The following transactions took place in the first year:a. To record authorization (memorandum).b. Issued 120,000 shares at \(\$ 32\); collected cash in full and issued the shares. Share issue costs amounted to

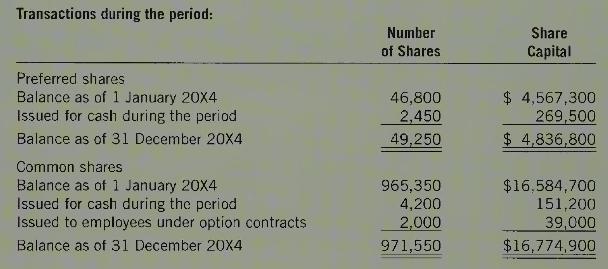

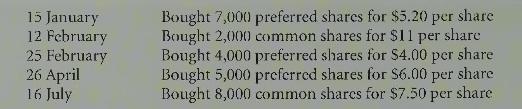

Share Retirement-Entries and Account Balances: The accounting records of Farhad Corporation showed that the company acquired and retired shares as following during the year:\begin{array}{ll}5 \text { January } & 2,000 \text { common shares at } \$ 10 \text { per share } \\6 \text { January } &

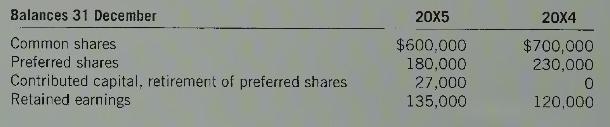

Share Retirement-Analysis: During 20X5, Veech Corporation had several changes in shareholders' equity. The comparative equity accounts for \(20 \mathrm{X} 4\) and 20X5:In 20X5, the only transactions affecting common and preferred share accounts were the retirement of 2,000 common shares and 1,000

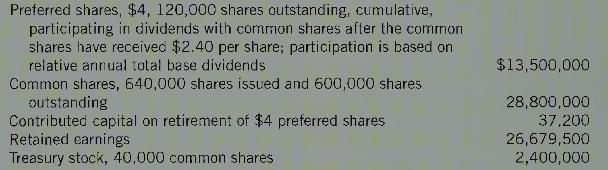

The following is the share capital note to the financial statements of Capital Corporation for the year ended 31 December 20X4:Note 17 Share capital Authorized share capital consists of an unlimited number of common shares and 100,000 non-voting, cumulative preference shares with a \(\$ 4\)

Retired Shares-Entries and Reporting: On 1 January 20X5, BC Ventures Corporation reported the following in shareholders' equity:\begin{array}{lr}\text { Preferred shares, 3,000 shares outstanding, no-par } & \$ 72,000 \\\text { Common shares, 20,000 shares outstanding, no-par } & 235,000

On 1 January 20X1, Winnipeg Corporation issued 10,000 no-par common shares at \(\$ 50\) per share. On 15 January 20X5, Winnipeg purchased 100 of its own common shares at \(\$ 55\) per share to be held as treasury stock. On 1 March 20X5, 20 of the treasury shares were resold at \(\$ 62\). On 31

Compute Dividends, Preferred Shares-Four Cases: Western Horizons Limited has the following shares outstanding:Common, no-par Preferred, no-par, \(\$ 0.75\)The matching dividend, if applicable, is \(\$ 1.00\) per share.Required:Compute the amount of dividends payable in total and per share on the

Mountain Construction Corporation is authorized to issue unlimited \(5(0.4)\) no-par preferred shares and unlimited no-par common shares. There are \(15,(060\) preferred and 45,000 common shares outstanding. In a five-year period, annual dividends paid were \(\$ 1,000, \$ 4,000, \$ 32,000, \$

Compute Dividends, Retire Shares: Australia Ltd. reported the following items in shareholders' equity at 31 December 20X3:Required:1. No dividends were declared in \(20 \mathrm{X} 1\) or \(20 \mathrm{X} 2\). In \(20 \mathrm{X} 3, \$ 6,500,000\) in cash dividends was declared but has not been

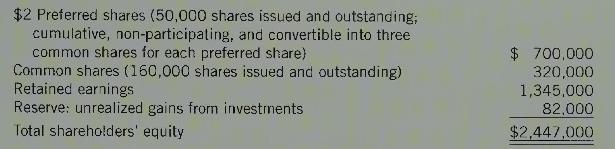

NovaCor Limited had the following shareholders' equity on 31 December 20X8:Earnings for \(20 \mathrm{X} 8\) had been \(\$ 307,000\) and comprehensive income, which also included a \(\$ 12,000\) unrealized gain on an investment, was \(\$ 319,000\). Basic earnings per share was calculated as \(\$

UMG Corporation reported balances in shareholder's equity:Each of the following cases is independent:Case A The Board of Directors declared and distributed a \(14 \%\) stock dividend, to be recorded at the fair value of the common shares, \(\$ 37\) per share.Case B The Board of Directors approved

Equity; Retirement and Stock Dividend: Davison Enterprises reported the following description of shareholders' equity on 31 December 20X6:There were no dividends in arrears. The following transactions took place in 20X7:20 Feb. Redeemed 1,000 preferred shares at the call price.28 Feb. Declared \(\$

Retained Earnings Calculation and Equity: Below are selected accounts from Serious Sound Corp. at 31 December 20X1. The accounts have not been closed for the year but transactions have been correctly recorded.\begin{array}{lr}\text { Stock dividend distributable, common shares } & 220,100 \\\text {

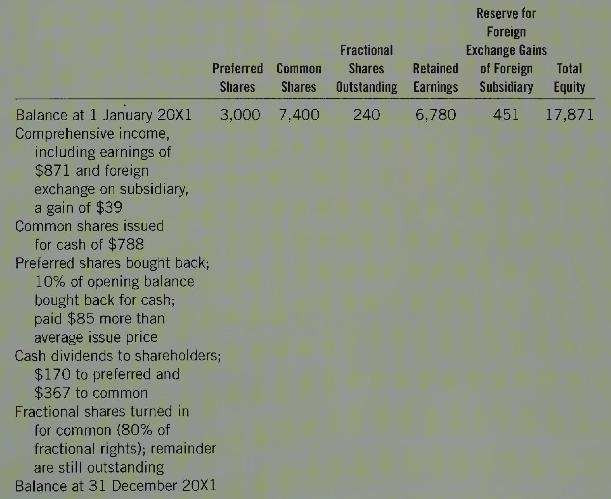

Statement of Changes in Equity: Below is a partially completed statement of changes in equity for Torino Capital Limited (in thousands of \(\$\) ).Required:Complete the statement of changes in equity to reflect the transactions and events described. Reserve for Foreign Fractional Exchange Gains

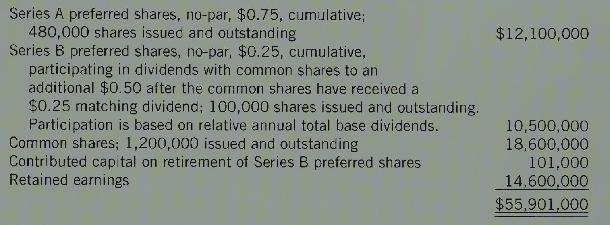

Statement of Changes in Equity: Green Energy Limited began 20X2 with shareholders' equity as follows:\begin{array}{lr}\text { Preferred shares; } \$ 1,240,000 \text { shares issued and outstanding } & \$ 6,000,000 \\\text { Common shares; } 1,200,000 \text { issued and } 1,000,000 \text { shares

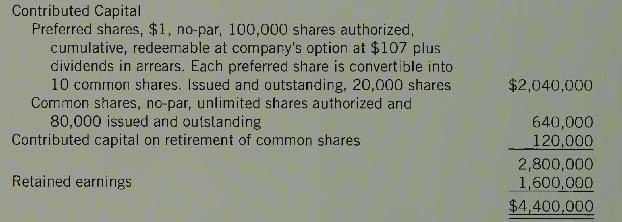

Entries and Shareholders' Equity: On 31 December 20X1, Kingdom Corporation had the following shareholders' equity:Dividends are two years in arrears on the Series B preferred shares.The following events and transactions took place during 20X2:15 Jamuary 25,000 Series A preferred shares were retired

Historically, what factors have dictated classification of a financial instrument as debt or equity? How is the classification made when based on the financial instruments rules?

What is the distinguishing feature of debt?

Assume a company issues a financial instrument for \(\$ 50,000\) in \(20 \mathrm{X} 2\) and retires it through an open market purchase for \(\$ 56,000\) in \(20 X 5\). In each of the intervening years, an annual payment of \(\$ 2,500\) was paid to the investor. How will the financial instrument

Explain appropriate financial statement classification of retractable preferred shares, which have a required maturity date or are to be repaid at the option of the investor.

How is convertible debt classified if it is mandatorily convertible into a fixed number of shares? If it is convertible at the investor's option into a fixed number of shares?

Explain how to classify convertible debt if the conversion option specifies that the number of shares to be issued depends on the fair value of shares at the conversion date.

What happens to the common share conversion rights account, created when convertible debt is issued, when the bond is actually converted? What if the bond is repaid in cash instead?

If a \(\$ 400,000,8 \%\) mandatorily convertible bond is issued at par and \(\$ 76,400\) of the issuance price is attributable to the interest obligation, how much interest expense will be recorded in the first year? The effective yield is \(8 \%\). How much is paid to the investor each year?

What is the distinction between stock options and stock warrants?

How is a share-based payment to a supplier measured in the financial statements?

If share rights are recognized on issuance, what happens to the share rights account if the share rights are exercised? Allowed to lapse? Compare this to the treatment of the common share conversion option account associated with convertible bonds.

When would a share-based compensation contract, payable after three years, result in an equity account being recognized in the first year? A liability? Both equity and a liability?

Assume that a cash-settled share-based payment scheme is established for an employee group. It will vest over five years, and be paid at the end of the fifth year. The total fair value of the plan is estimated to be \(\$ 400,000\) at the end of year 1 , \(\$ 175,000\) at the end of year 2 , and

Repeat question 14 assuming that retention rates are estimated to be \(80 \%\) at the end of year \(1,75 \%\) at the end of year 2 , and \(60 \%\) at the end of year 3 . How much compensation expense recognized in the third year?

Share-based payments to employees are trued up by the end of the vesting period. If the plan is cash-settled, for what factors is it trued up? If it is equity-settled?

Explain the terms of a SARs program for employees.

Define a derivative, and a hedge.

Assume that a Canadian company sells a product to a U.S. customer, and that the sale is denominated in U.S. dollars. What kind of a derivative instrument will eliminate the exchange risk? How will the transaction balance and the derivative instrument be reflected in the financial statements?

What areas of disclosure are required for financial instruments?

Omni Services Ltd., a Canadian public company, is a conglomerate involved in publication of newspapers, media services, and information technology consulting. It recently entered into an agreement to purchase Techno Wizard Limited (T'WL), which operates a printing business in Manitoba. Omni assumed

On-the-Crest Ltd. (OCL) is a company operating in the used-vehicle industry. OCL derives its revenue from selling, licensing, and servicing software products for car dealers, from the sale of products to car dealers, and from the sale of used vehicles. Both through internal growth and acquisitions,

Creative Traders Ltd. (CTL) is a Canadian company that conducts business in several countries, using a variety of currencies. The notes to the financial statements pertaining to fair values of financial instruments for the past year, the year ended 31 December 20X1. CTL is quite thorough in

Classification: Elkridge Corporation issued the following financial instruments in \(20 X 4\) :1. Convertible debentures issued at 103 . The debentures require interest to be paid semiannually at a nominal rate of \(7 \%\) per annum. The debentures are convertible by the holder at any time up to

Convertible Debt, Investor's Option: Nero Solutions Company issued an \(\$ 800,000,6 \%\), three-year bond for \(\$ 806,000\). The bond pays interest annually, at each yearend. At maturity, the bond can be repaid in cash or converted to 60,000 common shares at the investor's option. The market

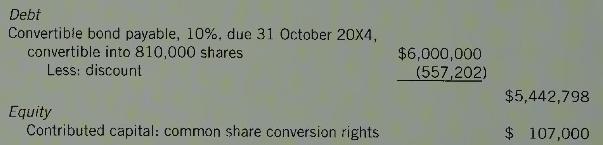

Convertible Bond, Investor's Option: Bixon Corp. Ltd. issued convertible bonds payable on 1 January \(20 \mathrm{Xl}\), when the market interest rate was \(10 \%\). The bond indenture stated: \(\$ 7,500,000\) of \(8 \%\) subordinated convertible debentures payable, interest payable semi-annually,

NewTech Ltd. has a 31 December fiscal year-end. The company issued convertible bonds on 1 July 20X4. The \(\$ 5,000,000\) bonds pay annual interest of \(8 \%\) each 30 June and mature on 30 June 20X19. At the investor's option, each \(\$ 1,000\) bond is convertible into 50 common shares on the

Convertible Debt, Three Cases: The following cases are independent:Case AOn 1 November 20X1, Bertha Builders Limited issued a convertible bond that was convertible in 15 years' time into 78,000 common shares at the investor's option. The bond had a \(\$ 5,000,000\) par value, and \(7 \%\) interest

Ferguson Memorials Limited issued a \(\$ 1,000,000,5 \%\) annual interest non-convertible bond with detachable stock warrants. One warrant is attached to each \(\$ 1,000\) bond and allows the holder to buy two common shares for \(\$ 28\) each at any time over the next 10 years. The existing market

Acorn Growth Limited is a small technology company listed on the TSX. To conserve cash, the company frequently settles obligations through the issuance of rights and options. Shares are now trading for \(\$ 8\) per share, but have fluctuated between \(\$ 5\) and \(\$ 22\) in the last year. Selected

Just In Co. issues 500,000 SARs to its eight-member top management group. These SARs allow the managers to receive a cash payment, after holding the SARs for five years. The SARs vest on the payment date. The value of the SARs is calculated as the difference between the \(\$ 34\) per share fair

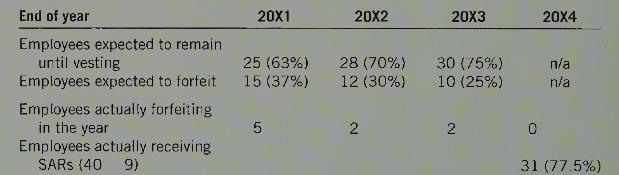

Cash-settled: Sousa Minerals has a SARs program for managers. These individuals receive a cash payment after four years of service, calculated as the excess of share price over \(\$ 2\). In early \(20 \mathrm{X}\), individuals in the 40 -member management team are granted a total of 100,000 SARs

Ming Limited has an executive stock option plan as follows: Each qualified manager will receive, on 1 January, an option for the computed number of common shares at a computed price. The number of option shares and the option price are determined by the Board of Directors, with advice from the

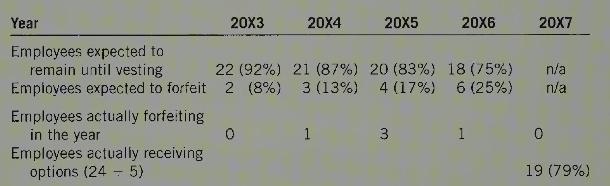

Ding Solutions Limited is authorized to issue unlimited numbers of common shares, of which \(1,675,000\) have been issued at an average price of \(\$ 75\) per share. On 1 January 20X3, the company granted stock options to each of its 24 senior executives. The stock options provide that each

Able Co. had compensation plans in effect for senior managers that included two long-term compensation elements. Retention levels were estimated to be \(80 \%\) at the end of \(20 \mathrm{X} 4\). SFP accounts at the end of \(20 \mathrm{X} 4\) :Required:1. Describe the likely features of the two

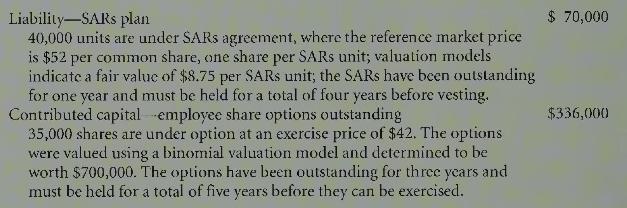

Mercury Limited issued long-term compensation contracts for its 10 -member executive team as follows:1. Mercury issued a total of 40,000 SARs units at the beginning of \(20 \mathrm{X} 3\). These SARs units vest and are exercisable after three years. The value of a SARs unit, to be paid in cash, is

Treetoo Limited wishes to buy 10,000 shares of \(\mathrm{YCo}\), a publiclytraded company. Treetoo enters into a contract, through a broker, to buy the shares in 40 days' time, at a price of \(\$ 3\) per share, the current fair value. The broker requires a \(10 \%\) margin to be maintained at all

Starco Corp. wishes to purchase 5,000 shares of Gertrom Ltd., a publicly-traded company. Starco contracts to buy the shares from a related party, Unit Ltd., for \(\$ 62\) per share in 90 days' time. The fair value was \(\$ 62\) per share on this day. One month later, at year-end, the fair value of

Notting Hill Limited reported the following amounts on the 31 December 20X2 SFP:Notting Hill has material accounts receivable and purchase orders that are denominated in U.S. dollars. The company follows a policy of hedging all exchange exposure with futures contracts.Required:1. Explain how

Why is it common for companies to label income tax expense as a provision for income taxes?

How can differences between accounting and taxable income be classified? Define each classification.

XTE Corporation (a) uses straight-line depreciation for its financial accounting and accelerated depreciation on its income tax return and (b) expenses golf club dues for its top management. What kind of tax difference is caused by each of these items? Explain.

Temporary differences are said to "originate" and "reverse." What do these terms mean?

Give three examples of a permanent difference, and three examples of a temporary difference.

Explain the two acceptable alternative options for the extent of allocation possible in dealing with interperiod tax allocation.

Sometimes the taxes payable method is called the flow-through method. Why might this name seem appropriate? When is this method generally accepted in Canada?

Why is the balance in a deferred income tax liability account not discounted?

Thertot Limited reported \(\$ 100,000\) of income in \(20 \mathrm{X} 4, \$ 300,000\) of income in \(20 X 5\), and \(\$ 500,000\) of income in \(20 \times 6\). Included in \(20 \times 4\) income is an expense, \(\$ 50,000\), that cannot be deducted for tax purposes until \(20 \mathrm{X} 6\). Assume

ATW Corporation has completed an analysis of its accounting income, taxable income, and the temporary differences. Taxable income is \(\$ 200,000\), and there are two temporary differences, which result in (a) a deferred income tax asset of \(\$ 15,000\) and (b) a deferred income tax liability of

A company has \(\$ 200,000\) in originating temporary differences in \(20 \mathrm{X} 6\), its first year of operation. The temporary differences give rise to a deferred income tax liability. The tax rate is \(34 \%\) in \(20 X 6\). In \(20 X 7\), there were no new temporary differences, but the tax

A company reports a \(\$ 1,000,000\) revenue (long-term receivable and associated revenue) in accounting income in year 1. It is taxable income when collected in year 4. What is the accounting carrying value of the receivable at the end of year 1? The tax basis? Assuming that the tax rate is \(40

A company bought \(\$ 1,000,000\) of capital assets at the beginning of year 1. Year 1 amortization was \(\$ 200,000\) and CCA was \(\$ 100,000\). What is the tax basis of the assets at the end of year 1? The accounting carrying value? If the tax rate is \(20 \%\), what is the balance in the

When do items on the statement of financial position have a different accounting carrying value and tax basis?

Do permanent differences cause the accounting carrying value and tax basis of the related item on the statement of financial position to differ?

On the statement of financial position, are deferred income taxes debits or credits? Explain. Is a debit to a deferred income tax account always a decrease, and a credit always an increase? Explain.

Assume that a company reports a deferred income tax liability of \(\$ 500,000\). The enacted tax rate goes down. How will the account on the statement of financial position change if the liability method is used?

What kinds of differences cause a company to report taxes at a rate different than the statutory rate?

What is an investment tax credit?

Explain two different approaches to account for an investment tax credit for a capital asset.

How might an ITC received because of qualifying expenditures for capital assets be reported on the statement of financial position?

Deep Harbour Limited (DHL) is a private company owned by Daniel Lalande. Lalande started the company in 20X1, and DHL has reported reasonably consistent growth in profits from fiscal 20X1 to 20X7. The company is in the plastic moulding business, making everything from toys to dashboards.The year

Canadian Products Limited (CPL) is a very large private Canadian company. CPL has been contemplating going public, which, according to business analysts, is just a matter of time. Recently, the president wrote a letter to you, the accounting advisor, complaining about Canadian tax standards and

You are a professional accountant in public practice. You have just left a meeting with Michel Lessard, a local entrepreneur, who is considering a potential acquisition. Mr. Lessard, with four others, is considering buying Darcy Ltd (DL), a company that is now the subsidiary of Micah Holdings

Describe the main categories of shareholders' equity.

If common shares are issued for capital assets, how is a value determined for the transaction?

What is the difference, from an accounting perspective, between par and no-par shares?

Briefly explain the alternatives for accounting for share issue costs.

When a company has 100,000 shares issued, and 10,000 shares held as treasury shares, how many shares are outstanding? If a cash dividend of \(\$ 2\) per share were declared, how much total dividend would be paid?

How can shares that are not callable be reacquired by a company? Why must corporations exercise caution in these transactions?

Why will EPS increase when shares are retired?

Identify and explain a transaction that causes other contributed capital to increase but does not result in any increase in assets or decrease in the liabilities of a corporation.

Explain how the purchase price is allocated when shares are reacquired and retired at a cost lower than average issuance price to date. What changes if average issuance price is lower?

When shares are retired, is the original issue price of those individual shares relevant? Why or why not?

What is the effect on assets, liabilities, and shareholders' equity of the (a) purchase of treasury stock and (b) sale of treasury stock?

Explain the difference between cumulative and non-cumulative preferred shares, and the difference between non-participating, partially participating, and fully participating preferred shares.

What are fractional share rights and why are they sometimes issued in connection with a stock dividend?

How is the entry to record a (cash) liquidating dividend different from the entry to record a normal cash dividend?

What do shareholders receive when a scrip dividend is declared?

Compare a stock split, both its substance and accounting recognition, to a large stock dividend. In what ways are the two the same or different?

If a shareholder donates a valuable piece of art to a company, to be displayed in the company boardroom, does the company record a gain on the transaction?

What are the common sources of reserves in equity?

Topsail Ltd. was founded ten years ago by Dave Jetson, a carpenter and entrepreneur. Topsail Ltd. is a growing construction company, building houses and doing major renovations for residential customers throughout the greater Moncton area. Dave is the president and sole common shareholder of the

Birch Corporation is a small, owner-managed company that manufactures and distributes wood mouldings. At 30 June 20X6, Reg Muise owned \(70 \%\) of the shares of Birch while Fran Cote owned the remaining \(30 \%\). There had been a third shareholder, Harry Ma, but his shares were repurchased and

In September 20X4, Giovanni Lorenzoni purchased a 40 hectare grape vineyard in southern Ontario. Giovanni is a successful restaurateur who owns and operates a familyoriented restaurant that offers fine cuisine at reasonable prices. As a restaurateur, Giovanni had always been interested in wines and

What three time elements are embedded in the definition of a liability?

Showing 1400 - 1500

of 2378

First

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

Last

Step by Step Answers