New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

intermediate accounting volume 2

Intermediate Accounting Volume 2 8th Edition Thomas H. Beechy, Joan E. Conrod, Elizabeth Farrell, Ingrid McLeod-Dick, Kayla Tomulka, Romi-Lee Sevel - Solutions

Cloud Corp. began operations in 20X8. In its first year, the company had a net operating loss before tax for accounting purposes of $200,000. Depreciation was $230,000, and CCA was $250,000. The company claimed CCA in 20X8. Warranty costs expensed in the period were $150,000, and actual warranty

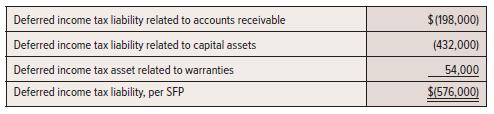

At the end of 20X8, Anderson Corp., a public company, had the following balances:In 20X8, the company had reported $1,350,000 of taxable income. It also reported a $550,000 long-term receivable, taxable when collected. At the end of 20X8, capital assets had a net book value of $4,800,000 and a UCC

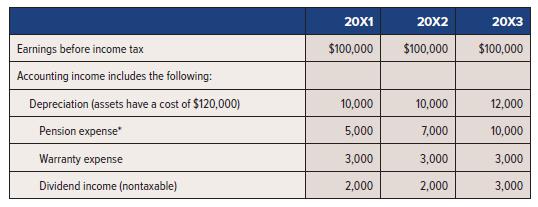

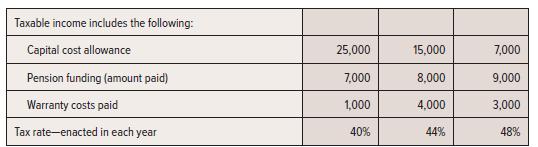

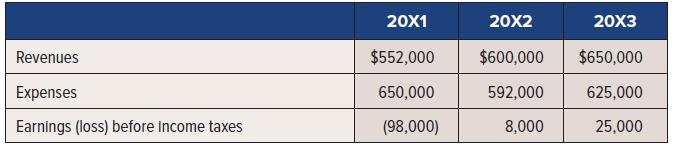

Crandall Corp. was formed in 20X1. The company uses the comprehensive tax allocation method. Relevant information pertaining to 20X1, 20X2, and 20X3 is as follows:*Pension amounts are tax deductible when paid, not when expensed. Over the long term, payments will equal total expense. The tax basis

Zhang Ltd. reported earnings before income tax of $560,000 in 20X9. The tax rate for 20X9 was 30% and was enacted during the year. The enacted tax rate at the end of the previous year was 28%.At the end of 20X8, the balance sheet of Zhang included the net book value of equipment of $795,000,

Behadrut Corporation uses IFRS for financial reporting. Information for 20X5 and 20X6 is provided below.Information relating to 20X5 is as follows:• The tax rate enacted in the year was 30%.• Machinery was purchased 1 January 20X5 for $2,000,000.• At the end of the year, the net book value of

Helon Corp. is a private company reporting under ASPE. Helon Corp. has selected to use the taxes payable method. Accounting income for 20X5 is $280,000. The following additional information is available for Helon Corp. for 20X5:a. Depreciation expense is $80,000 whereas CCA is $98,000.b. The income

Refer to the facts in A16-19.Data From A16-19In its first year of operations, Martha Enterprises Corp. reported the following information:a. Income before income taxes was $620,000.b. The company acquired capital assets costing $1,800,000; depreciation was $120,000, and CCA was $90,000.c. The

Telo Corp. is a private company that uses the taxes payable method.The following information is available for 20X2:1. Income before income taxes was $1,300,000.2. The company paid a fine for late sales tax remittance in the amount of $2,000 which was expensed for accounting purposes.3. Meals and

Melik Ltd. engages in activity that qualifies for investment tax credits (ITCs) in 20X6. The company has a tax rate of 32% and deducts the deferred investment credit from the asset on the balance sheet. It has a 31 December year-end and records annual adjusting entries. The following information is

Pegasus Printing began operations in 20X4 and has bought equipment for use in its printing operations in each of the last three years. This equipment qualifies for an investment tax credit of 14%. Information relating to the three years is shown below:a. Income before tax includes nondeductible

Refer to the case facts in A16-21.Data From A16-21Diversified Ltd. (DI) is a public company that started operations in 20X4. It opened a number of locations across Canada. In fiscal 20X4, the company had earnings before tax of $290,000. The tax rate for 20X4 was 30%. DI has a 31 December year-end.

The following are independent statements regarding corporate income taxes:1. The choice to adopt the taxes payable method or future income taxes method is available only under ASPE.2. If a private company that adopts ASPE chooses the future income taxes method, the accounting for corporate taxes is

Tempo Inc. is a Canadian company that has operations in Canada and Australia. One source of temporary differences relates to the warranty it offers on its core products.Required:What type of information needs to be retained for appropriately calculating and maintaining the deferred tax balance

Diversified Ltd. (DI) is a public company that started operations in 20X4. It opened a number of locations across Canada. In fiscal 20X4, the company had earnings before tax of $290,000. The tax rate for 20X4 was 30%. DI has a 31 December year-end. The following occurred during 20X4.a. DI purchased

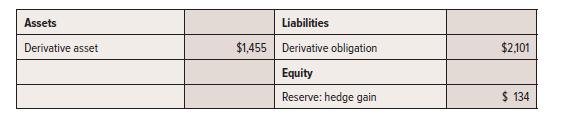

Moon Pacific Ltd. reported the following amounts on the 31 December 20X2 SFP (in thousands):Moon Pacific has material accounts receivable and purchase orders from customers that are denominated in euros. The company follows a policy of hedging all exchange exposure with futures

AZZY Ltd. issued preferred shares as part of a transfer of ownership under specified sections of the Income Tax Act. The company issued 400,000 shares, for a nominal dollar amount of $1 per share. The shares are retractable at $15 per share, anytime, at the holder’s option. Dividends of $20,000

Laffoley Corp. needs to raise $10,000,000 to finance a planned capital expansion. The company has investigated two alternatives:1. Issue $10 million of preferred shares at par. The shares can be redeemed at the company’s option at the end of 12 years for a price estimated to be in the region of

Closed Tech Ltd. issued convertible bonds on 1 July 20X8. The 15-year, 5% $10,000,000 bonds pay interest semi-annually each 30 June and 31 December. At the investor’s option, each $1,000 bond is convertible into 50 common shares on the bond’s maturity date.Bond market analysts indicated that if

Abbot Corporation is a real estate developer looking to build a new property in the Metro Vancouver area. In order to do so, they need to raise capital to finance the construction. The company has investigated two alternatives:1. Issue $95 million 10-year bonds, with an 8% coupon per annum. The

SCIFI Ltd. issued convertible bonds on 1 February 20X6. The 5-year, 3% $8,000,000 bonds pay interest semi-annually each 31 January and 31 July. At the investor’s option, each $1,000 bond is convertible into 50 common shares on the bond’s maturity date. The company has a 31 January year-end.Bond

Description of several financial instruments follows:Case 1 Convertible subordinated bonds payable, entitled to annual cash interest at 5%, paid semi-annually. At maturity, the bonds may be settled at the investor’s option through the issuance of common shares using an exchange price of $5 per

Mecca Energy Corp. issued a convertible bond on 1 August 20X9. The 10-year, 4% $12,000,000 bond pays interest semi-annually each 31 July and 31 January. At maturity, each $1,000 bond is convertible into 120 common shares. The bond was issued for $12,500,000. Market interest rates were approximately

Description of several financial instruments follows:Case 1 Class D Series 2 shares, carrying a dividend entitlement equal to $5 per share or an amount equal to common share dividends, whichever is higher, redeemable at the investor’s option at $62 per share. The company may, at its option,

Pont Chemical Remediation Ltd. issued options in 20X6 allowing the holder to acquire 50,000 common shares in five years’ time at an acquisition price of $20 per share. Using an option pricing model, the options are valued at $120,000. The options were issued for consulting and promotion work

Glamour Mining Ltd. currently has a debt to equity ratio of 2.5-to-1, based on $80 million of debt and $32 million of equity. The company is looking to raise $16 million in new financing and must choose one of the following:A. Convertible debt, unsecured, with a 7% interest rate, where conversion

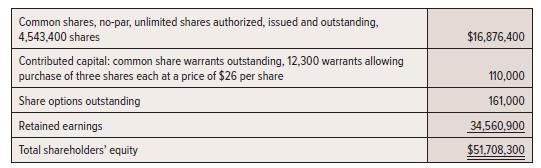

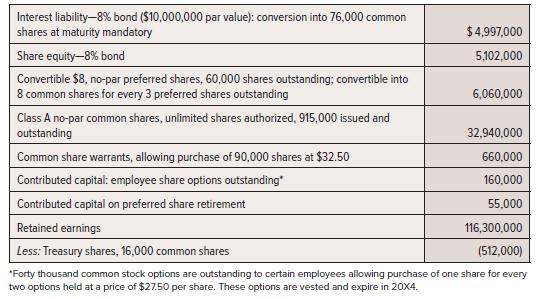

On 31 December 20X2, the shareholders’ equity section of Sersa Corp.’s statement of financial position was as follows:There were 46,000 share options outstanding, issued for legal services, valued at $161,000. These allow purchase of one share each for $19 cash; the options are exercisable over

Shurwood Ltd. issued 5,000,000 8%, 10-year, nonconvertible bonds with detachable warrants for $5,100,000. Shortly after issuance, the warrants trade for $300,000 in total, and the bonds were trading at 99, or $4,950,000, ex-warrants (i.e., without warrants attached).Required:1. Provide the journal

A description of several financial instruments follows:Case A Subordinated 8% debentures payable, interest payable semi-annually, due in the year 20X8. At maturity, the face value of the debentures may be converted, at the company’s option, into common shares at the market price at that time.

In 20X0 ten executive management were awarded units in a phantom stock plan. The plan entitles each executive to either 11,000 common shares or cash equal to the market value of 8,000 shares at the end of 20X3.The following additional information has been provided:At the time of the grant, the

Forgin Co. issued 500 common shares to We Can Advertize for advertising services. The shares currently are valued at $24 per share, and the advertising services rendered are valued at $11,000.Required:Provide the journal entry to be recorded with respect to issue of these shares.

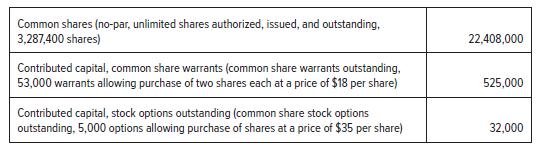

Cruz Inc., a publicly traded company, had the following balances in its shareholders’ equity accounts at the beginning of 20X3:The following transactions took place during the year:1. At the beginning of 20X3, all 53,000 warrants were exercised when the market value of the shares was $25 per

Marjorie Manufacturing Ltd. issued a convertible bond on 2 July 20X5. The $5 million bond pays annual interest of 8% each 30 June. Each $1,000 bond is convertible into 50 shares of common stock, at the investor’s option, on 1 July 20X10 until 1 July 20X15, after which time each $1,000 bond may be

Darling Petrol Corp. granted stock options to executives in early 20X1. The stock options vest over five years and expire after eight years. In total, the options allow the purchase of 400,000 shares at $2 per share. Option pricing models indicate that the options have a total fair value of

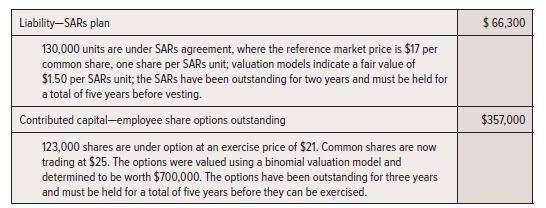

Smith Minerals Ltd. had compensation plans in effect for senior managers that included two longterm compensation elements. SFP accounts at the end of 20X6 are:Retention levels were estimated to be 85% at the end of 20X6.Required:1. Describe the two kinds of compensation plans above. Provide the

IT Solutions Ltd. has a cash-settled SARs program for employees. These employees will receive a cash payment after five years of service, calculated as the excess of share price over $7.50. In early 20X1, employees in total are granted 60,000 units in the program.The fair value of one SARs unit is

On 1 January 20X4, Eledant Inc. issued a $9,000,000, 3-year bond that pays 7.5% for $9,400,000. The bond pays interest on 31 December each year. At the end of the term each bond can, at the holders’ option, be repaid in cash or converted to 30 common shares. Comparable bonds without the

Agmore Breakthrough Corp. is a small biotech company listed on the TSX. To conserve cash, the company frequently settles obligations through the issuance of options. Shares are now trading for $7 per share but have fluctuated between $5 and $21 in the last year. Selected transactions:a. Issued

Maritime Corp. is a junior mining company listed on the TSX. The common share price of Maritime fluctuates in value. Recent swings went from a high of $16 to a low of $0.30. Maritime issued stock options on 1 September 20X5 to a consultant, in exchange for a project completed over the last year.

The following data are related to Eli Products Ltd.:During the year, the following transactions took place and have been correctly recorded:a. Reported earnings and comprehensive income was $3,200,000. Cash dividends were paid at the end of the year.b. Retained earnings was reduced by $175,000 as

Acer Corp. reported the following balances at 1 January 20X1:The following events took place in 20X1:a. Common shares were issued to employees under the terms of existing outstanding share options. 16,000 options were exercised when the share market value was $45.b. Options were issued in exchange

Five vice-presidents of Spinner Entertainment Ltd. are awarded units in a phantom stock plan at the beginning of 20X5. At the end of 20X7, after three years of employment, each vice president is entitled to receive either:• 7,000 common shares; or• Cash equal to the market value of 5,000

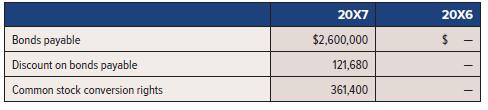

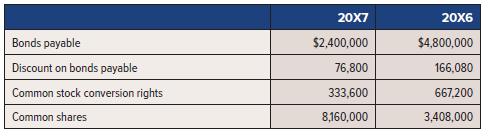

The following cases are independent:Case A Information from the 31 December 20X7 SFP of Holdco Ltd.:Convertible bonds were issued during the year. Discount amortization was $7,280 in 20X7.Case B Information from the 31 December 20X7 SFP of Sellco Ltd.:One-half of the bonds converted to common

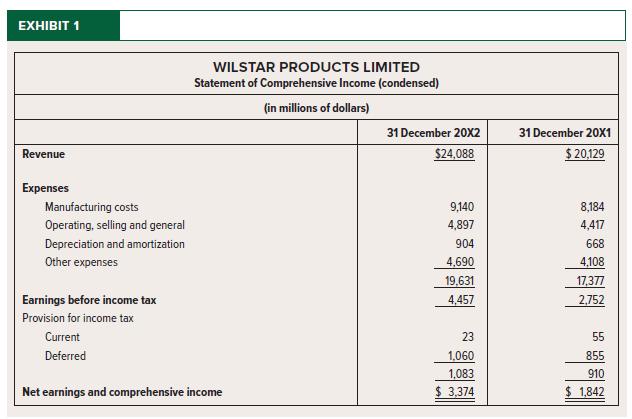

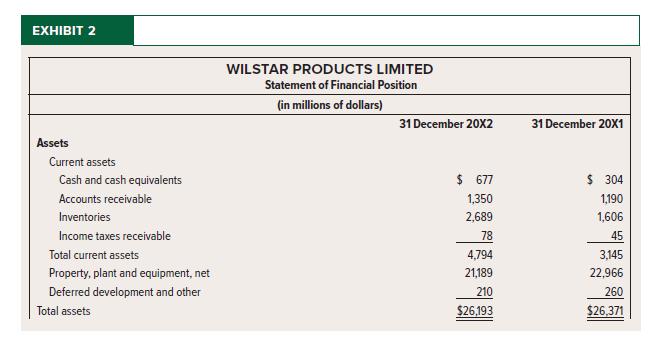

Wen Chu is a senior account manager for a large Canadian bank. The bank is considering the possibility of syndicating a large debenture issue for Wilstar Products Ltd. (WPL), a manufacturer of auto parts. Wen has been given the task of analyzing WPL’s financial performance. When the bank’s

MNA is a Canadian-based pharmaceutical company that develops generic over-the-counter medicines.The company is publicly traded. The company sells its products to pharmacies across North America, and as a result has a significant number of U.S.-denominated accounts receivable. MNA sold US$220,000 in

Software Inc. (SI) is a private corporation formed in the 1990s. SI develops and sells software for many purposes; theft recovery, geomapping, data and device security, and IT asset management.To help motivate management, SI has a stock option plan.To help fund continued software development, SI

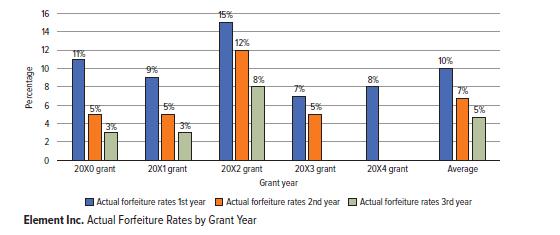

Element Inc. is a producer of leading-edge medical equipment. The company has always had competitive compensation packages for its employees. At the beginning of 20X5, 100 employees were awarded a total of 20,000 options at an exercise price of $10 per share. Each employee will receive 200 options.

Eldon Ltd. is a private company that complies with ASPE. Eldon issued the following financial instruments in 20X4:1. Convertible debentures issued at 103. The debentures require interest to be paid semi-annually at a nominal rate of 7% per annum. The debentures are convertible by the holder at any

Goldem Ltd. is a private company that complies with ASPE. The company issued the following financial instruments in 20X4:1. Retractable preferred shares. Issued 1,500 preferred shares to the owner of the company. The preferred shares may be redeemed at the option of the holder for $1.5 million. The

Argile Inc. is a Canadian private company. The company has a competitive stock-based compensation program for all of its 125 employees. Information from the 20X5 grant:• 500 shares options are granted to each employee for $5 per share.• The share options have a value of $209,700.• Share

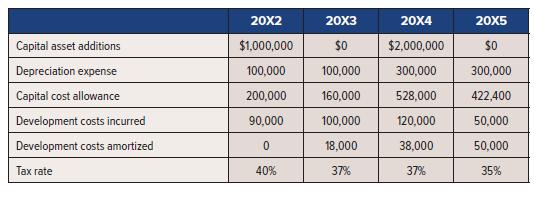

The following information has been provided for Relink Corporation for 20X2-20X5:Required:1. What is the tax basis of the capital assets in each year?2. What is the tax basis of the development costs in each year?3. What is the accounting basis of the capital assets in each year?4. What is the

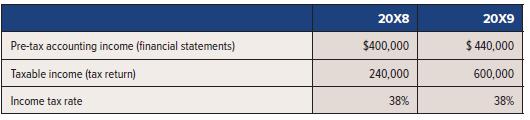

Nalad Corp. provided the following data related to accounting and taxable income:There are no existing temporary differences other than those reflected in these data. There are no permanent differences.Required:1. How much tax expense would be reported in each year if the taxes payable method was

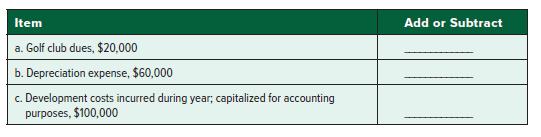

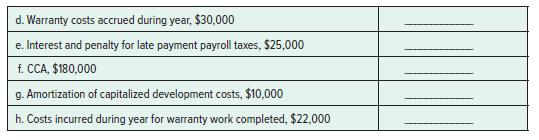

Listed below are a number of items that are required to adjust net income before income tax to taxable income.Required:1. For each item, indicate if it will be added or subtracted from net income before income taxes.2. For each item, indicate if it is a permanent difference or a temporary

Consider the following independent scenarios:Scenario A Tomkin Inc. sells 6% convertible bonds for $1,080,000 that are due in 10 years. The market interest rate is 8%. Each $1,000 bond is convertible into 50 common shares, at the option of the investor. Shareholders must notify Tomkin of their

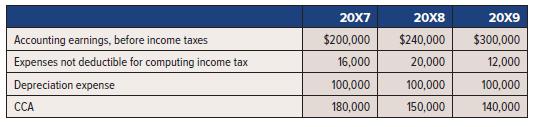

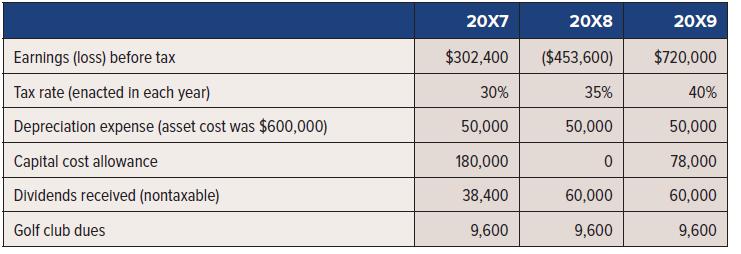

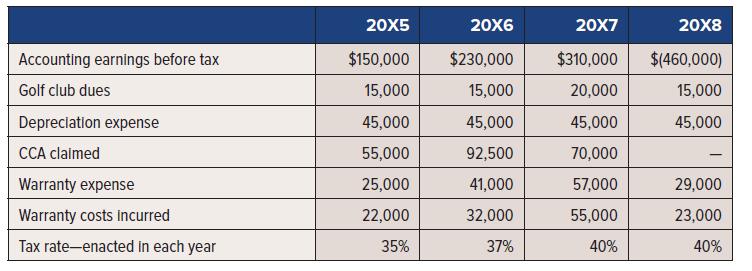

The financial statements of Dakar Corp. for a four-year period reflected the following pre-tax amounts:Dakar has a tax rate of 40% each year and claimed CCA for income tax purposes as follows: 20X4, $16,000; 20X5, $12,000; 20X6, $8,000; and 20X7, $4,000. There were no deferred income tax balances

The following is selected information from the accounting records of Slow Inc. for 20X9 its first year of operations:In determining pre-tax accounting earnings, the following deductions were made:For tax purposes, the following deductions were made:The capital assets, originally costing $625,000,

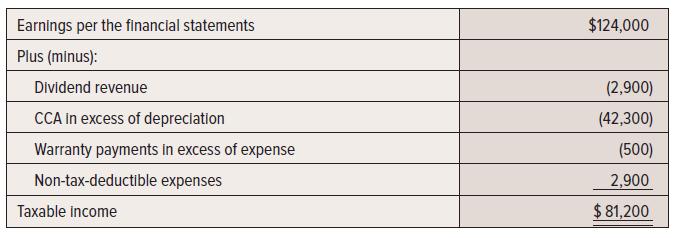

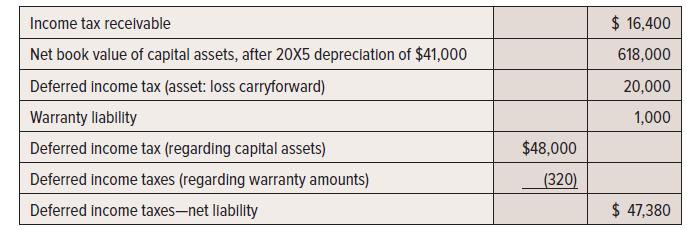

Hendrie Inc. reported earnings before income taxes of $2,200,000 in 20X9. The tax rate for this year is 40%.Required:1. Use the information from TR16-1. Calculate taxable income.2. What is the amount of income taxes payable?

DCM Metals Ltd. has a 31 December year-end. The tax rate is 30% in 20X4, 35% in 20X5, and 42% in 20X6. The company reports earnings as follows:Taxable income and accounting income are identical except for a $300,000 revenue reported for accounting purposes in 20X4, with one-half reported in 20X5

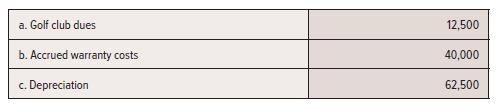

Lantz Ltd. reported earnings before income taxes of $540,000 in 20X5. The company had expensed $25,000 of golf club dues that were not tax deductible. There was tax-free dividend revenue of $10,000. Warranty expense was $40,000. Depreciation was $120,000, while CCA was $190,000.Warranty claims paid

At the end of 20X6, Tap Ltd. had accumulated temporary differences of $500,000 arising from CCA/depreciation on capital assets. UCC was $2,500,000 and net book value of these assets was $3,000,000. The balance of the deferred income tax liability account was $150,000. Over the next three years, Tap

McQuinn Corp. started operations in 20X5. The company acquired equipment on the first day of operations for a price of $180,000. The equipment will be depreciated for accounting purposes over three years on a straight-line basis. For determining income tax payable, the company can deduct one-half

Leonard Ltd. recorded revenue in 20X6 in the amount of $100,000. The amount will be collected from the customer in the amount of $40,000 in 20X7 and $60,000 in 20X8. The revenue will be taxable when the cash is received. Leonard’s income tax rate is 22%.Required:For each 31 December 20X6 through

At the end of 20X8, Bent Angel Ltd.’s statement of financial position showed equipment at total cost of $2,000,000. The equipment was being amortized at 10% per year, straight-line, and was 40% depreciated at the end of 20X8. The income tax files showed UCC for the equipment of $550,000. The

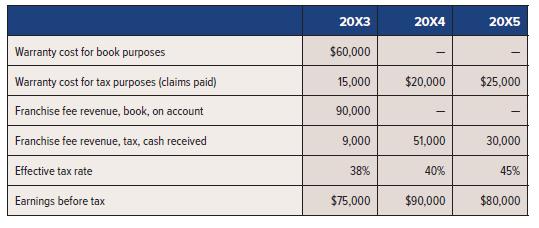

Golf Inc., which began operations in 20X3, uses the same policies for financial accounting and tax purposes with the exception of warranty costs and franchise fee revenue. Information about the $60,000 of warranty expenses and $90,000 franchise revenue accrued for book purposes is provided

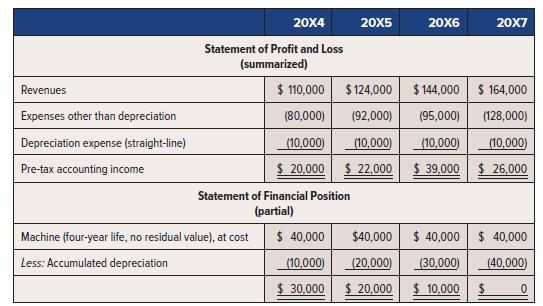

Stacy Corp. would have had identical income before tax on both its income tax returns and statements of profit and loss for the years 20X4 through 20X7, except for equipment that cost $120,000. The equipment has a four-year estimated life and no residual value. The equipment was depreciated for

Zygote Ltd. recorded warranty expense of $125,000 in 20X6, $35,000 in 20X7, and $75,000 in 20X8. Warranty claims paid were $70,000 in 20X6, $55,000 in 20X7, and $90,000 in 20X8. Warranty amounts are tax-deductible when the cash is paid. Zygote’s income tax rate is 28%.Required:For each 31

The following is a list of temporary differences:1. Depreciation versus CCA on equipment.2. Money received from a customer prior to services being performed; cash is taxable when received.3. An expense for warranty is recognized in the same period that revenue is recognized but is not

Marsh Corp. reported a deferred tax asset of $24,000 in 20X2, caused by a warranty liability of $80,000. The tax rate was 30%. In 20X3, accounting earnings were $200,000, warranty claims paid were $70,000, and warranty expense was $35,000. The tax rate is 22%.Required:1. Calculate tax payable.2.

Martin Ltd., in the first year of its operations, reported the following information regarding its operations:a. Earnings before tax for the year was $2,500,000 and the tax rate was 38%.b. Depreciation was $240,000, and CCA was $134,000. Net book value at year-end was $1,680,000, while UCC was

In its first year of operations, Martha Enterprises Corp. reported the following information:a. Income before income taxes was $620,000.b. The company acquired capital assets costing $1,800,000; depreciation was $120,000, and CCA was $90,000.c. The company recorded an expense of $125,000 for the

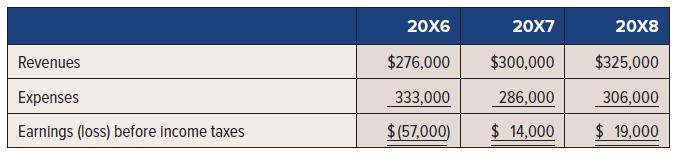

The pre-tax income of Barrows Ltd. for the first three years was as follows:The company had no temporary differences in any of the three years. The income tax rate was constant at 36%.In 20X6 and 20X7, the prospect for future earnings was highly uncertain. In 20X8, management decided that the

The following information pertains to Towers Corp.:• From 20X1 through 20X3, Towers had pre-tax income totalling $150,000.• In 20X4, Towers had a pre-tax loss of $550,000.• Earnings of each year is equal to taxable income.• The income tax rate was 40% from 20X1 through 20X4.• In 20X4, a

The 20X6 records of Laredo Inc. show the following reconciliation of accounting and taxable income:In 20X5, Laredo had reported an operating loss, the tax benefit of which was fully recognized in 20X5 through loss carryback and recognition of a deferred income tax asset. Selected SFP accounts at

Refer to case facts in A17-19.Data From A17-19On 1 January 20X7, Chang Inc. commenced business operations. At 31 December 20X9, the following information relates to Chang:Required:Prepare the journal entries for income taxes for 20X7, 20X8, and 20X9. Assume the company uses the taxes payable

Refer to case facts in A17-8.Data From A17-8Benata Ltd. started operations in 20X5 and purchased buildings and equipment with an original cost of $400,000. Benata reported the following information:Required:Prepare the journal entries for income taxes for each of the four years. Assume the company

The pre-tax income for Xing Inc. for the first three years of operations is provided below.Xing Inc. had no sources of temporary differences in 20X1, 20X2, and 20X3. The income tax rate was 34% in all three years.In 20X1 and 20X2 management was unable to predict with certainty that there would be

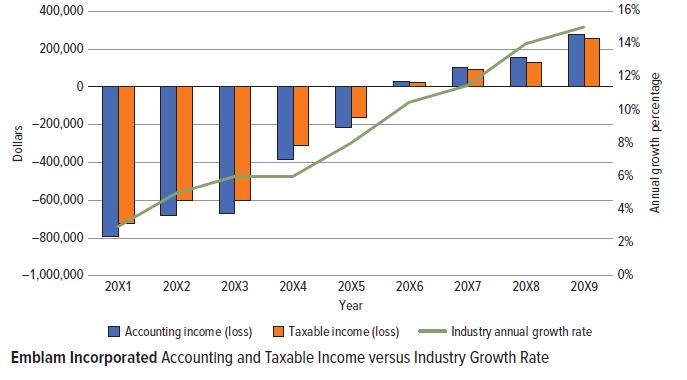

Emblam Incorporated is a biotechnology firm, engaging in research and development (R&D). During 20X1–20X5, its first five years, it engaged in heavy R&D activities without having yet secured any customers. The product was first sold in 20X6 to several small customers, after the product

Kriyati Corp. is a private company that is strongly considering going public in the near future. In 20X9 it has a taxable loss of $10,000,000. For the prior three years Kriyati Corp. had taxable profits of $2,000,000 (20X6), $5,000,000 (20X7), and $1,000,000 (20X8). The 20X9 loss is the result of

Toldo Corporation is a medium-sized manufacturing company based in Canada. It has a South African subsidiary, Dinto Corporation, that is consolidated in its annual financial statements. Toldo has a deferred tax liability related to capital assets; Dintro has a deferred tax asset related to a

Showing 2300 - 2400

of 2378

First

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

Step by Step Answers