New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

intermediate accounting volume 2

Intermediate Accounting Volume 2 5th Edition Thomas H. Beechy - Solutions

Central Purchasing Limited owns the building it uses; it had an original cost of \(\$ 825,000\) and a net book value of \(\$ 450,000\) as of 1 January \(20 \mathrm{X} 2\). On this date, the building was sold to the Royal Leasing Company for \(\$ 480,000\), which also was the building's fair value,

Sportco Limited is suffering temporary cash flow difficulties due to poor economic conditions. To raise sufficient finance to allow operations to continue until economic conditions improve, Sportco entered into an agreement with a major lease corporation, Leaseco Limited. On 1 January 20X2, Sportco

Belangier Corporation has signed two leases in the past year. One lease is for handling equipment, the other for a truck.HANDLING EQUIPMENT:The handling equipment has a fair market value of \(\$ 274,000\). Lease payments are made each 2 January, the date the lease was signed. The lease is for four

On 31 December 20X1, Lessor Limited leased a reaming machine to a client for six years at \(\$ 48,000\) per year. Lease payments are to be made at the beginning of each lease year. Lessor purchased the machine for \(\$ 239,650\). Lessor negotiated the lease so as to receive a \(8 \%\) return

On 2 January 20X2, the National Leasing Company, a leasing subsidiary of a major Canadian chartered bank, entered into a lease with Alphon Limited (the lessee) for computer equipment. Terms of the lease are as follows:- The initial lease term is two years, with payments due each 31 December, at the

On 2 January 20X4, Yvan Limited entered into a five-year lease for office equipment from Jeffery Leasing Incorporation. The lease calls for annual lease payments of \(\$ 100,000\), payable at the beginning of each lease year. Yvan's incremental borrowing rate is \(6 \%\). The lessor's implicit rate

Sondheim Limited entered into a direct financing lease with New Age Leasing Corporation. The lease is for new specialized factory equipment that has a fair value of \(\$ 4,800,000\). The expected useful life of the equipment is 15 years, although its physical life is far greater. The initial lease

Parravano Incorporated has leased a serging machine from Xerox Leasing Corporation for annual beginning-of-year payments of \(\$ 15,000\) for 10 years. The lease term begins on 1 January 20X2. Parravano's fiscal year ends on 31 December. Parravano's incremental borrowing rate is \(9 \%\) per annum.

Lessor and lessee agreed to a non-cancellable lease for which the following information is available:a. Lessor's cost of the asset leased is \(\$ 40,308\). The asset is new at the inception of the lease term.b. Lease term is three years, starting 2 January 20X3.c. Estimated useful life of the

Each of the following items must be considered in preparing a statement of cash flows for Phillie Fashions for the year ended 31 December 20X6:1. Finance assets that had a cost of \(\$ 10,00061 / 2\) years before and were being depreciated straight-line on a 10 -year basis, with no estimated scrap

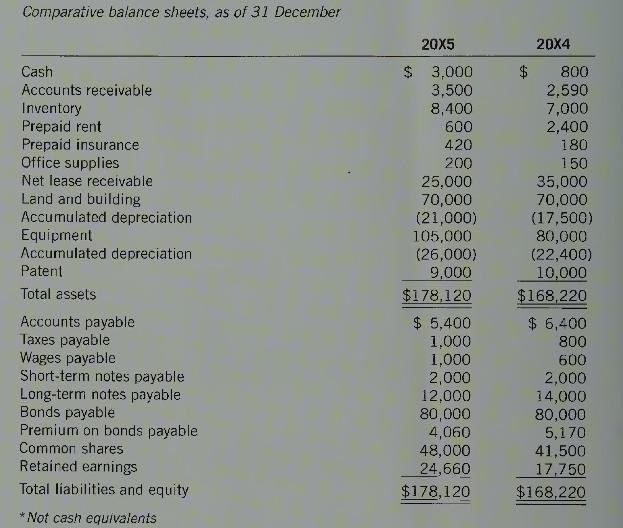

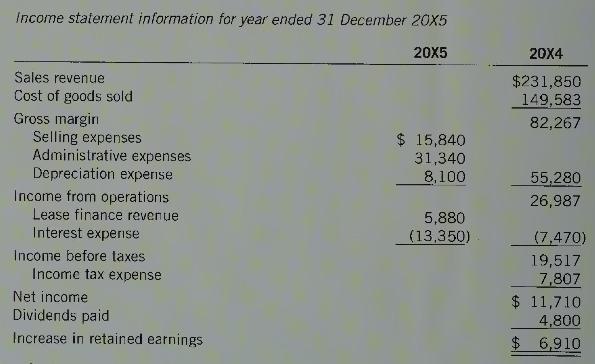

Laker Ltd., a public company, had the following information available at the end of \(20 \times 5\) :Required:Prepare a statement of cash flows, using the indirect method to disclose operating activities. Comparative balance sheets, as of 31 December 20X5 20X4 Cash $ 3,000 $ 800 Inventory Accounts

Distinguish between a defined contribution pension plan and a defined benefit pension plan. Why are defined contribution plans attractive to employers?

Why is it logical that contributions made by an employee to a pension plan vest immediately, while an employer's contributions may vest only after a certain period of time?

What is the incentive to the company for registering a pension plan?

Explain the impact each of the following variables would have on the yearly expense associated with a defined benefit pension plan:a. An increased rate of return on investments held by the pension planb. Lower than expected employee mortality ratesc. Higher than expected employee turnoverd. A

Assume that a pension plan must accumulate \(\$ 700,000\) by an employee's retirement age in order to fund a pension. Three different funding models have been used to project funding requirements for the first year. The estimates are \(\$ 2,600, \$ 6,300\), and \(\$ 1,100\). Identify three

In each of the following circumstances, identify the funding method that an employer would likely find most appealing:a. Conserve current cash balances.b. Have equal cash requirements each year.c. Use a funding pattern that could also be used to measure the pension expense.

List and define the five continuing components of pension expense.

How is interest on the defined benefit obligation measured?

What is a past service cost? How is it accounted for as part of pension expense?

Define the ARSP and explain when it is used as an amortization period.

What is the difference between an experience gain or loss and a gain or loss caused by a change in assumptions? How are the two accounted for in the calculation of net pension expense? What alternatives exist?

A company follows the practice of amortizing actuarial gains and losses to pension expense when the amount is outside the \(10 \%\) corridor. At the beginning of \(20 \mathrm{X} 4\), the balance of unamortized actuarial gains was \(\$ 27,000\). If the opening values of pension assets and

What limit is placed on pension fund assets?

When are gains and losses related to pension plan settlements and curtailments recognized?

When are the costs of enhanced pension entitlements associated with termination packages included in income?

If a pension has a benefit obligation of \(\$ 400,000\), pension fund assets of \(\$ 250,000\), and unrecognized losses of \(\$ 175,000\), what will be the resulting recognized accrued asset or liability pension account?

What justification is there for recording the net position of the pension plan, rather than the net position of the plan less unrecognized amounts?

Why are post-employment benefits other than pensions less likely to be fully funded? What difference will this make in financial statement treatment?

How would a private company account for a defined benefit pension plan if the simplified approach is used?

Deliveries-R-Us is a public company offering express freight transportation, small package ground delivery services, and other freight services. Capital assets include a broad range of assets, including a large fleet of aircraft and vehicles.The liability and equity portion of the SFP, and

For organizations with defined benefit pension plans, the actuary's estimate of the organization's obligation for pension benefits must be disclosed. The market value of pension plan assets available to satisfy that obligation is also disclosed in the notes to the financial statements. Within

Warmth Home Comfort Limited (WHCL) is a Canadian manufacturer of furnaces and air-conditioning units. The company was acquired by a group of 15 investors eight years ago. Three of the investors are senior managers with the company, including Jacob Kovacs, who is president and chief executive

Sandsupport Corporation (SC) is a privately-owned company based in Alberta. The company provides support services for the oil and gas industry, especially for new exploration not only in Canada, but also in other countries such as Venezuela and Mexico.Due to the ever-increasing worldwide demand for

Michael Bliss is the President, CEO, and controlling shareholder of Bliss Air Line Limited (BALL). He started the company four years ago to provide low-cost charter service to holiday destinations. Although the airline is low cost, it is not no-frills; the airline's motto is "Travel with Bliss and

Sigma Auto Parts Ltd. is an Ontario-based manufacturer of automobile parts. The Canadian operations supply automotive components and parts to three U.S. states and two Japanese auto manufacturers. Approximately \(30 \%\) of Sigma's worldwide sales is generated by its Canadian operations.The company

Ellis Ingram Corporation (EIC) is a manufacturer of household appliances. The company is privately held with a broad shareholder group. The company has sizable loans outstanding, and audited financial statements are required to assess compliance with loan covenants, related to the current ratio and

At the beginning of the fiscal year, a tenant signs a three-year lease to rent office space at the rate of \(\$ 1,000\) per month. The first six months are free. How much rent expense should be recognized in the first year of the lease?

Under what circumstances is a lease normally considered a finance lease? What role does judgement play?

Give three reasons that a company might enter into a long-term lease instead of buying an asset outright.

A car dealer advertises a new car lease with the following terms:- \(\$ 3,500\) cash paid by the customer at the beginning of the lease;- Monthly payments of \(\$ 229\) for 48 months; and- The customer is required to pay \(\$ 2,650\) at the end of the lease, and then owns the vehicle.What is the

Under what circumstances would a deferred rent liability appear on the balance sheet of a company that is a lessee in an operating lease?

Define the following terms, as used in lease accounting standards:- Bargain purchase option (BPO).- Lease term.- Minimum net lease payments.- Contingent lease payments.- Bargain renewal term.- Guaranteed residual value.- Incremental borrowing rate.- Interest rate implicit in the lease.

Assume that a lessee signs a lease for a three-year term for \(\$ 1,000\) per year that has a renewal option at the lessee's option for a further three years for \(\$ 1,000\) per year. How long is the lease term, as defined by lease accounting standards?

How would your answer to Question 17-7 change if the renewal was at the lessor's option? If rental during the second term was \(\$ 1\) per year instead of \(\$ 1,000\) ?Data From Question 17-7:Assume that a lessee signs a lease for a three-year term for \(\$ 1,000\) per year that has a renewal

A lessee signs a lease for a two-year term that requires a yearly payment of \(\$ 14,000\), which includes \(\$ 2,500\) for insurance and maintenance cost. At the end of the twoyear term, there is a \(\$ 1,000\) BPO. How much are the minimum net lease payments?

Assume an asset has a fair market value of \(\$ 48,500\) and is leased for \(\$ 10,000\) per year for six years. Payments are made at the end of each year. Insurance costs included in this amount are \(\$ 1,000\), and there is a \(\$ 6,000\) guaranteed residual. What is the interest rate implicit

Assume a non-profit organization wishes to acquire a particular asset. Why might it be cheaper to lease rather than buy the asset?

Assume a lease involves payments of \(\$ 20,000\) per year, net of insurance costs, and is properly capitalized on the lessee's books at a \(10 \%\) interest rate for \(\$ 135,180\). How much interest would be recognized in the first year of the lease if the payments were made at the beginning of

A lessee enters into a five-year finance lease with a five-year bargain renewal option, and then the asset is returned to the lessor. How long would the depreciation period be for the asset? Assume that such an asset is expected to have a 12 -year useful life.

How is the current portion of the lease liability determined if the lease payments are due and payable at the end of the fiscal year? How would your answer change if the payments were due at the beginning of the period?

What is a sale and leaseback? How are such transactions accounted for?

Suppose that a company owns a building. The company enters into a sale and leaseback arrangement to sell the building and then lease it back. The company makes a substantial profit on the sale. How should the gain from the sale be accounted for?

Suppose that a lessor is a private Canadian corporation. How does its status as a private corporation affect classification of a lease, as compared to a public corporation?

What interest rate does the lessor use for discounting calculations associated with a lease?

Describe the nature of a sales-type lease. What kinds of entities offer such leases?

In a sales-type lease, how does separation of the sale component from the lease component affect revenue recognition in the current and future years?

What is the benefit that arises as a result of a tax loss?

Over what period can a tax loss be used as an offset against taxable income?

Why do companies usually use tax losses as carrybacks before using them as carryforwards?

When do recognition and realization coincide for tax losses?

Why is it desirable to recognize the benefit of a tax loss carryforward in the period of the accounting loss? Under what circumstances would such a benefit be realized?

What criteria must be met to recognize the benefit of a tax loss carryforward in the period of the accounting loss?

ABC Company has a taxable loss of \(\$ 100,000\). The tax rate is \(40 \%\). What is the potential benefit of the tax loss?

A company reports an accounting loss of \(\$ 75,000\). Depreciation for the year was \(\$ 216,000\), and CCA was \(\$ 321,000\). The company wishes to maximize its tax loss. How much is the tax loss?

Refer again to the data in Question 16-8. Assume instead that the company wishes to minimize its taxable loss/maximize taxable income. How much is the taxable income (loss)? Explain.

Explain why a company might choose not to claim CCA when it reports (a) accounting income and (b) an accounting loss.

Define the term "more likely than not."

What strategies can be used to increase the likelihood that a tax loss carryforward will be used?

Provide three examples of favourable evidence in assessing the likelihood that a tax loss carryforward will be used in the carryforward period.

A company has a tax loss of \(\$ 497,000\) in \(20 X 4\), when the tax rate was \(40 \%\). The tax loss is expected to be used in 20X6. At present, there is an enacted tax rate of \(42 \%\) for 20X5. The government intends to increase the tax rate to \(45 \%\) in 20X6, but no legislation concerning

A company recorded the benefit of a tax loss carryforward in the year of the loss. Two years later, the balance of probability shifts, and it appears that the loss will likely not be used in the carryforward period. What accounting entry is required if a direct adjustment is made (i.e., not to a

A company did not recognize the benefit of a tax loss carryforward in the year of the loss. Two years later, the balance of probability shifts, and it appears that the loss will likely be used in the carryforward period. What accounting entries are required in each year if a valuation account is

How will income change if a tax loss carryforward, previously recognized, is now considered to be unlikely?

A company has recorded a \(\$ 40,000\) benefit in relation to a \(\$ 100,000\) tax loss carryforward. The tax rate changes to \(35 \%\). What entry is appropriate?

Give three objections to the practice of recording a tax loss carryforward prior to realization.

What disclosure is required in relation to tax loss carryforwards?

Graham Corporation provided the following data related to accounting and taxable income:There are no existing temporary differences other than those reflected in this data. There are no permanent differences.Required:1. How much tax expense would be reported in each year if the taxes payable method

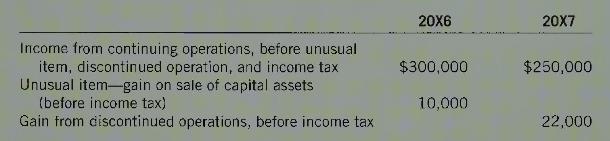

Maynes Limited reported the following information (in thousands) for 20X6 and 20X7:Mayne's income tax rate is \(35 \%\). The 20X6 unusual gain is not taxable until 20X7. The 20X7 gain on discontinued operations is fully taxable in \(20 \mathrm{X} 7\).Required:1. Prepare a partial statement of

Rundle Corporation acquired new equipment for \(\$ 400,000\) in \(20 \mathrm{X} 4\). For accounting purposes, the equipment will be depreciated over four years, straight-line, with a full-year's depreciation in the first year. For income tax purposes, Olivetti can take CCA over the next three years

Agnew Corporation started operations in \(20 X 1\). The company acquired equipment in the first year for a price of \(\$ 90,000\). The equipment will be depreciated for accounting purposes over three years on a straight-line basis (with a full year's depreciation in the year of acquisition). For

The records of Retter Corporation, at the end of 20X4, provided the following data related to income taxes:a. Golf club dues expense in \(20 \mathrm{X} 4, \$ 16,000\), properly recorded for accounting purposes but not tax deductible at any time.b. Investment income in \(20 \mathrm{X} 4, \$

Scarlett Corporation reported accounting income before taxes as follows: \(20 \mathrm{X} 4, \$ 150,000 ; 20 \mathrm{X} 5, \$ 92,000\). Taxable income for each year would have been the same as pre-tax accounting income except for the tax effects, arising for the first time in \(20 \mathrm{X} 4\), of

The pre-tax income statements for VCR Corporation for two years (summarized) were as follows:For tax purposes, the following income tax differences existed:a. Revenues on the 20X6 statement of profit and loss include \(\$ 45,000\) rent, which is taxable in \(20 \times 5\) but was unearned at the

Hogarth Incorporated recorded instalment sales revenue of \(\$ 60,000\) in \(20 \mathrm{X} 1\) and \(\$ 200,000\) in \(20 \mathrm{X} 2\). The revenue is not taxable until collected. Of the year \(20 \times 1\) revenue, \(\$ 50,000\) was collected in \(20 \times 2\) and the remaining \(\$ 10,000\)

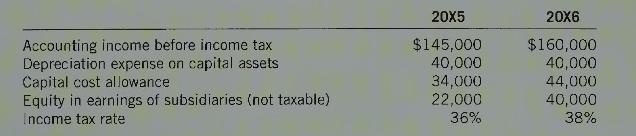

Thomas Incorporated started operations on 1 January 20X5 and purchased \(\$ 400,000\) of capital assets. Information on the first two years of operations is as follows:Required:Prepare all income tax journal entries for \(20 X 5\) and 20X6. 20X5 20X6 Accounting income before income tax $145,000

Solway Company has a deferred income tax liability in the amount of \(\$ 200,000\) at 31 December \(20 X 4\), relating to a \(\$ 500,000\) receivable. This sale was recorded for accounting purposes in 20X4 but is not taxable until the cash is collected. In \(20 X 5, \$ 300,000\) is collected.

Change in Tax Rates: On 1 January 20X3, Highmark Corporation reported the following amounts on the statement of financial position:On this date, the net book value of capital assets was \(\$ 1,750,000\) and undepreciated capital cost was \(\$ 1,450,000\). There was a warranty liability of \(\$

Change in Tax Rates: On December 31, 20X6, Silk Corporation reported the following amounts on the statement of financial position:On this date, the net book value of capital assets was \(\$ 1,380,000\) and undepreciated capital cost was \(\$ 980,000\). There was an estimated warranty liability of

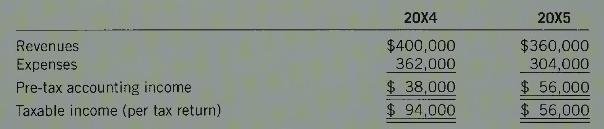

The statements of profit and loss for Gardner Corporation for two years (summarized) were as follows:The income tax rate is \(38 \%\) in \(20 \mathrm{X} 4\) and \(40 \%\) in \(20 \mathrm{X} 5\). The \(20 \mathrm{X} 5\) tax rate was enacted in 20X5. For tax purposes, the following differences

The records of Morgan Corporation provided the following data at the end of years 1 through 4 relating to income tax allocation:The above amounts include only one temporary difference; no other changes occurred. At the end of year 1 , the company prepaid an expense of \(\$ 30,000\), which was then

At the end of 20X4, Varna Ltd. had accumulated temporary differences of \(\$ 500,000\) arising from CCA/depreciation on capital assets. The balance of the deferred income tax liability account was \(\$ 200,000\). Over the next three years, Varna experienced the following:*Excess of tax-deductible

In its first year of operations, Lee Corporation reported the following information:a. Income before income taxes was \(\$ 2,000,000\).b. The company acquired capital assets costing \(\$ 1,800,000\); depreciation was \(\$ 300,000\) and CCA was \(\$ 180,000\).c. The company recorded an expense of

A. Grossery Limited is a wholesale grocery distributor formed in 20X4, with warehouses in several locations in southern Ontario. The company uses the liability method of tax allocation. In fiscal 20X4, the company had net income before tax of \(\$ 90,000\). The following items were included in the

At the end of 20X8, Lambert Corporation reported the following items in the financial statements:In \(20 \mathrm{X} 8\), the company reported \(\$ 214,500\) of taxable income. It also reported a \(\$ 450,000\) long-term receivable, taxable when collected. Capital assets, with a net book value of

Liquid Limited reported income before income tax of \(\$ 175,900\) in \(20 \mathrm{X} 9\). The tax rate for \(20 \mathrm{X} 9\) was \(38 \%\) and was enacted during the year. The enacted tax rate at the end of the previous year was \(35 \%\).At the end of 20X8, the balance sheet of Liquid included

At the beginning of 20X1, Farcus Corporation had the following future tax accounts:Deferred tax asset \(\$ 19,600\)Warranty expense to date has been \(\$ 126,000\); claims paid have been \(\$ 70,000\). There is a \(\$ 56,000\) warranty liability included in short-term liabilities on the statement

Components of Shareholders' Equity: The following accounts are taken from the general ledger of GRL Trading Limited on 31 December 20X1:\begin{array}{lr}\text { Preferred shares, no-par value, } \$ 2 \text {, unlimited number authorized, } \\\quad \text { cumulative and fully participating; }

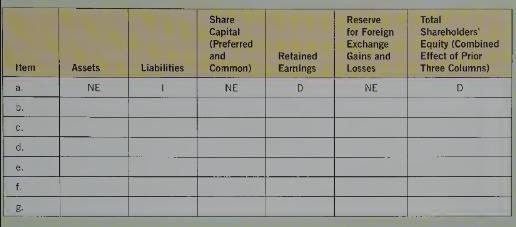

Effect of Transactions: The following transactions will change the SFP in some way:a. Declare a cash dividend, to be paid in three weeks' time.b. Declare and issue a stock dividend, recorded at fair value.c. Pay a cash dividend already declared and recorded.d. Issue common shares for land.e.

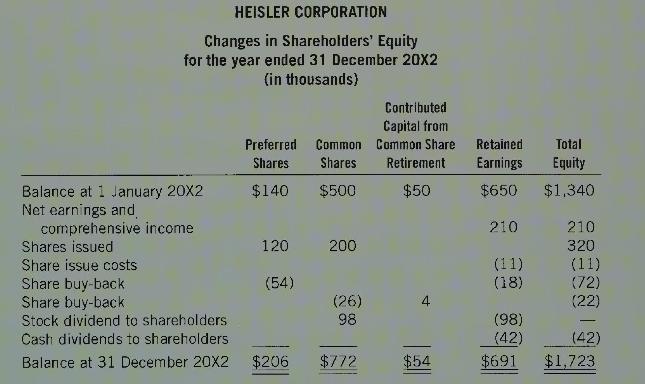

Effect of Transactions: The following statement of changes in shareholders' equity summarizes various equity transactions that occurred during \(20 \mathrm{X} 2\) :Required:Journalize the transactions in the statement of shareholders' equity. For earnings, close the income summary to retained

Showing 1300 - 1400

of 2378

First

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

Last

Step by Step Answers