New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

intermediate accounting volume 2

Intermediate Accounting Volume 2 8th Edition Thomas H. Beechy, Joan E. Conrod, Elizabeth Farrell, Ingrid McLeod-Dick, Kayla Tomulka, Romi-Lee Sevel - Solutions

Darlington Industries Ltd. reported earnings of $1,000,000 in 20X6; no dividends were declared.Darlington has two classes of ordinary shares—Class A and Class B. The characteristics of the two classes of shares are as follows:• 60,000 Class A shares and 750,000 Class B shares were outstanding

Seeko Inc. is a public company that reports EPS figures. It has a 31 December year-end date. It issued its 20X4 year-end financial statements on 20 February 20X5. The following information relates to Seeko Inc.’s capital structure:Shares were issued as a result of a 10% stock dividend on 30

Murchie Ltd. earned $16,000,000 in 20X6 and paid dividends of $7,400,000. The company has two classes of voting shares. Class A shares have six votes per share, while Class B shares have one vote per share. Both participate in the distribution of net assets in the event of dissolution. There were

The following cases are independent:Case A Halifax Ltd. had 2,500,000 common shares outstanding on 1 January 20X8. On 1 March, 600,000 common shares were issued for cash. On 1 July, 300,000 common shares were repurchased and retired. On 1 November, 560,000 common shares were issued as a stock

Kouk Corp. has the following capital structure at the end of 20X7:• 100,000 Class A shares carrying five votes per share.• 100,000 Class B shares, carrying one vote per share.• Dividends are shared on a 5:1 ratio—$5 to Class A for every dollar paid to Class B.Additional information:• Kouk

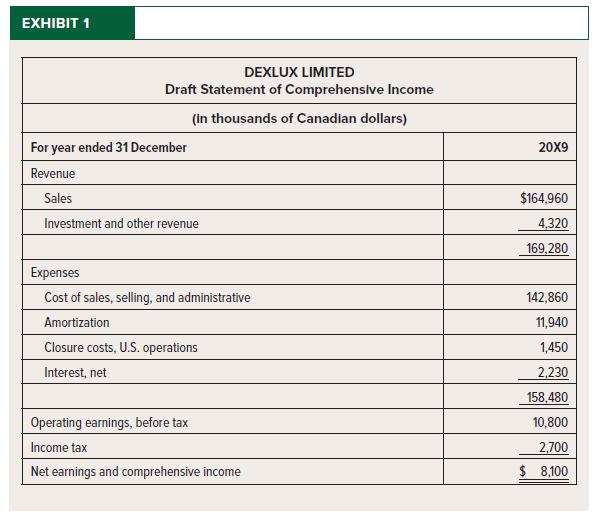

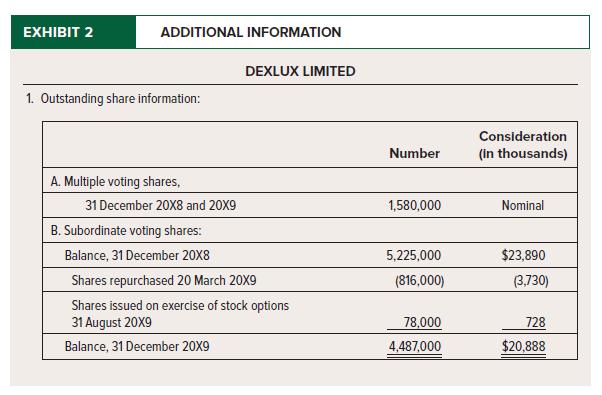

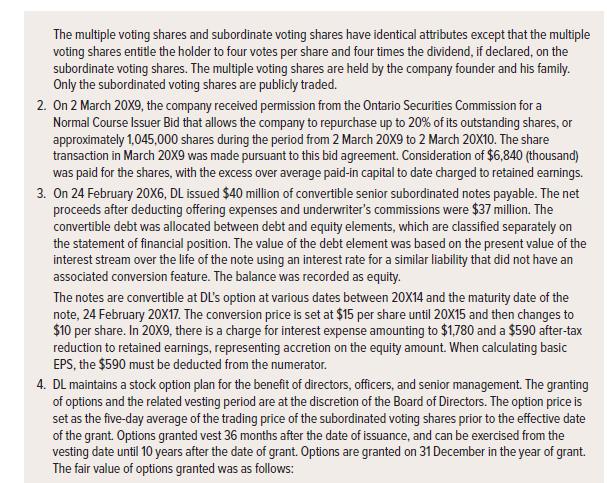

Dexlux Ltd. (DL) is a vertically integrated manufacturer and retailer of moderately priced high-fashion footwear, leather goods, and accessories. DL’s common shares are listed on the Toronto Stock Exchange. DL has stores in over 180 major Canadian shopping malls and operates over 50

The following cases are independent.Case A Jethrow Ltd. had 1,000,000 common shares outstanding on 1 January 20X2.• On 27 February 200,000 shares were issued for $50 each.• 300,000 shares were issued on 1 August.• A 2-for-1 stock split was distributed on 30 August.Case B On 1

Wilcorp Ltd. reported a loss of $610,000. There are 550,000 shares outstanding. The company has outstanding stock options for 100,000 common shares at $10 per share. The average common share price was $25 during the period.Required:1. Calculate the number of shares that would be added for the

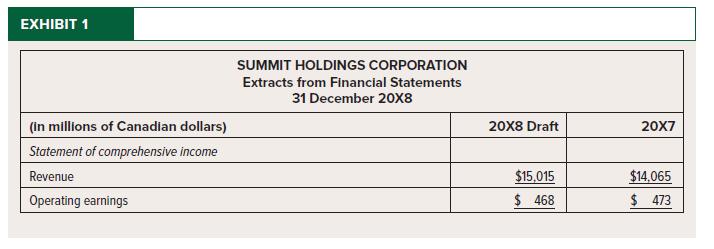

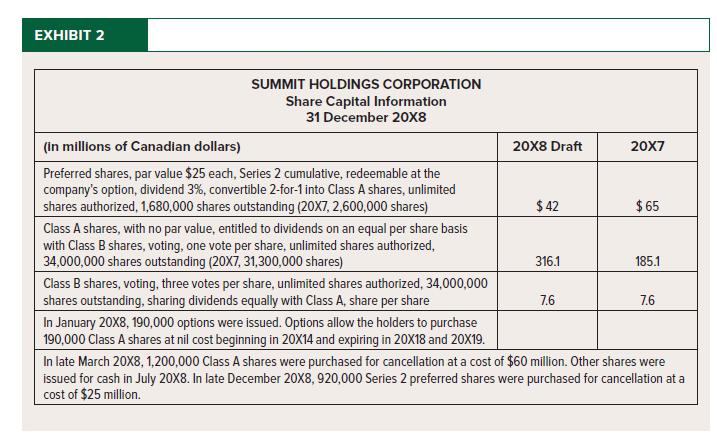

Summit Holdings Corporation (SHC) is a diversified Canadian company based in Winnipeg. SHC’s primary business is the distribution and retailing of pharmaceutical and health care products. Its shares are traded on the Toronto Stock Exchange. Common shares traded in the $8–$14 range in 20X8. The

CH Holdings Inc. has net earnings of $5,456,000 for the year ended 31 December 20X5. It has convertible bonds currently outstanding with a face value of $8,500,000 and a book value of $7,871,852 at 1 January, 20X5. The bonds have a coupon interest of 2.5% payable semi-annually on 30 June and 31

The following are independent scenarios.1. Rial Corp. designated convertible bonds as fair value through profit or loss (FVPL) on initial recognition. Management is unsure how to handle the liability for purposes of diluted EPS.2. Hekah Inc. issued bonds which are convertible at the company’s

CNZ Co. had 1,200,000 shares outstanding at the beginning of the year—1 June 20X8. During the year, the following transactions occurred:1 August 20X8—5,000 share options with an exercise price of $35 per share, were exercised.1 October 20X8—A 3:1 stock split was completed.1 February

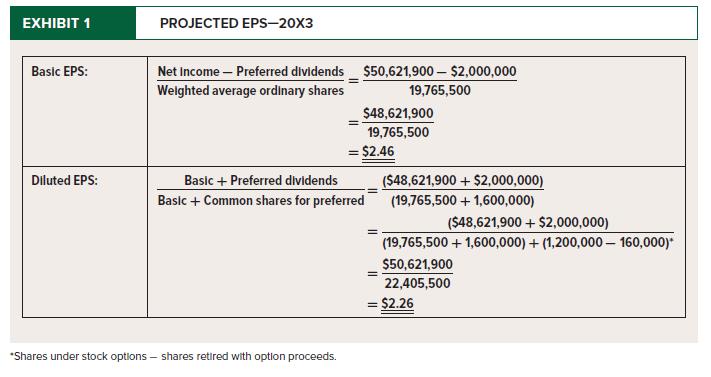

Bryant Corporation is a small public company trading on the TSX. Bryant Corporation has issued both common and preferred shares. During 20X3 the company paid cash dividends on its preferred shares. It also declared and paid a 10% stock dividend on common shares during the year. A third of the way

PhonUs Ltd. (PUL) is a Canadian public company involved in network technology for mobility telecommunications. This network technology allows super-fast data services to be offered through mobile platforms at a premium rate as a strategy to increase revenue per user for the carriers. PUL’s

Arca Ltd., a public company, has a defined benefit obligation. From their financial statements, you have determined that the pension obligation recognized in the financial statements has a discount rate of 6.0%; the net defined benefit obligation is $90 million; and the total pension expense was

Refer to the information in T20-2. Assume that Hominem Inc. had a loss on discontinued operations of $1,000,000 (after tax).Data From T20-2Hominem Inc. has 100,000 common shares outstanding. Earnings from continuing operations amounted to $1,500,000 (after tax) for the year ended 31 December 20X4.

The following are independent statements related to earnings per share.1. EPS calculations can be computed and then interpreted meaningfully as individual amounts without concern for comparisons.2. “Real dilution” occurs when new shares are issued without an instantly proportionate increase in

The following sentences are incomplete.1. When calculating WAOS, if there is a stock dividend during the reporting period, the additional shares are not weight-averaged; rather, they are.2. When included in EPS calculations, dilutive elements cause.3. Dilutive adjustments for issued options are

Angelo Ltd., a public company, had 600,000 common shares outstanding at the beginning of 20X4. On 1 March 20X4, Angelo purchased and retired 120,000 shares that had been owned by one of the company founders. On 30 June, the company issued 60,000 shares to a venture capital firm upon maturity of a

Jabba Inc. is looking to establish a post-employment benefit plan for its employees. The company has decided on the following structure for its plan.A contributory defined benefit plan. The plan would provide 2% per year worked × career average earnings. It would recognize past service up to a

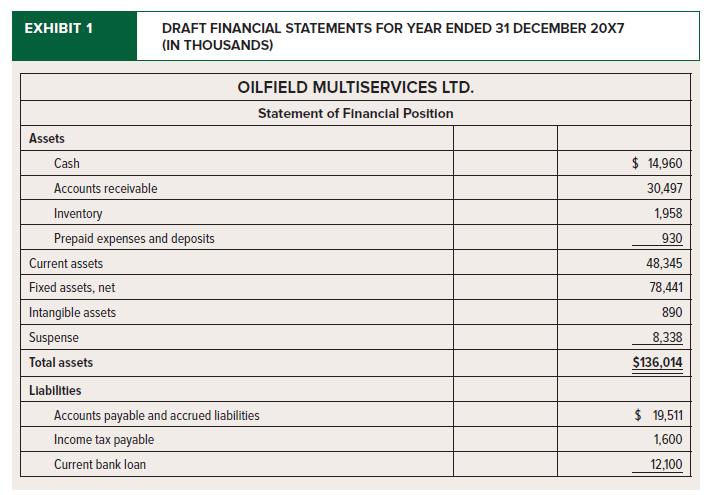

Oilfield Multiservices Ltd. (OML) offers oilfield operation services to the oil and gas industry in Alberta and Texas. OML owns no natural resource properties itself but assists in exploration activities through cementing and stimulation services. OML complies with ASPE. The company has prepared

Return to the facts of A19-22. Assume instead that this pension plan is sponsored by a private company and ASPE applies.Data From A19-22Solutions Ltd. sponsors a defined benefit pension plan for its employees. At the beginning of 20X3, there is an accrued SFP pension liability of $152,800, as

Return to the facts of A19-19. Assume instead that this pension plan is sponsored by a private company and ASPE applies.Data From A19-19Jones Manufacturing Inc. sponsored a defined benefit pension plan effective 1 January 20X7. The company uses the projected unit credit actuarial cost method

Genis Inc. is a large distributor located in Atlantic Canada. Genis’s draft financial statements show the following:The company has the following items that have not yet been recorded as of the end of the period:Share transactions:• Dividends totalling $450,000 were been declared in December.

Return to the facts of A19-13. Assume instead that this pension plan is sponsored by a private company and ASPE applies.Data From A19-13The following data relate to a defined benefit pension plan:Required:1. Prepare all entries for 20X9.2. Based on the entries based on requirement 1, calculate the

Return to the facts of A19-12. Assume instead that this pension plan is sponsored by a private company and ASPE applies.Data From A19-12The following data relate to a defined benefit pension plan:Required:1. Prepare an entry to record pension expense and an entry to record the contribution to the

Refer to the data of TR19-2. Assume now that the contribution to the plan assets was made 1 September 20X8 and pension payments to pensioners were paid evenly throughout the year.Data From TR19-2The following data are to be used for TR19-2 to TR19-6. Good day Ltd., a public company, has a defined

Return to the facts of A19-10. Assume instead that this pension plan is sponsored by a private company and ASPE applies.Data From A19-10Urban Life Ltd. sponsors a defined benefit pension plan for its employees. It is now the 20X9 fiscal year. An appropriate interest rate for long-term debt is

Lin Developments Ltd. provides post-employment benefits to its retirees for supplementary health care, including prescription medication. Lin had an accumulated OCI loss amount related to OPEBs of $45,000 at the beginning of the year, an experience loss related primarily to unexpected cost

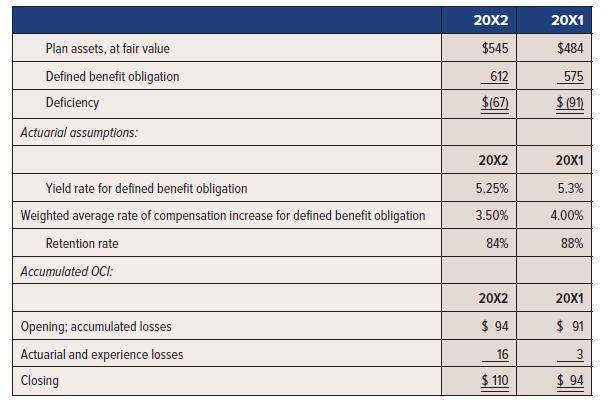

Extracts from the pension disclosures of Blue Pony Ltd. are shown below.Pension Benefits The estimated present value of accrued plan benefits and the estimated market value of the net assets available to provide for these benefits are as follows:Required:1. With respect to the actuarial assumptions

Return to the facts of A19-11. Assume instead that this pension plan is sponsored by a private company and ASPE applies.Data From A19-11Micro Computers Inc. sponsors a defined benefit pension plan for its employees. It is now the 20X2 fiscal year. Long-term corporate borrowing rates for companies

Car Wash Ltd. began a pension fund in the year 20X3, effective 1 January 20X4. Terms of the pension plan follow:• The yield rate on long-term high-grade corporate bonds is 5%.• Employees will receive partial credit for past service. The past service obligation, valued using the projected unit

Jetnow Ltd. has a defined benefit pension plan for its employees. The following information was provided by the actuary:Required:Prepare a spreadsheet for 20X3 that determines pension expense and also the closing net defined benefit asset or liability account and accumulated OCI. Benefit

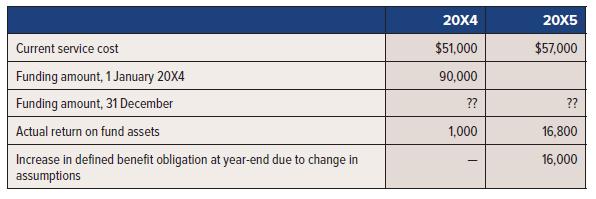

Morocco Corp. initiated a defined benefit pension plan on 1 January 20X5. The plan does not provide past service benefits for existing employees. The pension funding payment is made to the trustee on 31 December of each year. The following information is available for 20X5 and 20X6:Required:1.

Raka Ltd. provides supplementary post-employment benefits to its retirees. The benefits include dental, vision, and prescription medication. At the beginning of 20X3, Raka had an accumulated OCI loss amount related to OPEBs of $13,460.The following details have been provided to your regarding the

On 1 January 20X0, Rainbow Inc. established a defined benefit pension plan for its employees. At the inception of the plan, the present value of the defined benefit obligation relating to employees' past service was $240,000. The pension funding is made to a trustee each year on 31 December. The

Guetza has a defined benefit pension plan. At the end of the year 20X0, plan assets are $3,450,000, and the defined benefit obligation is $3,120,000. There is an asset ceiling that caps the net defined benefit asset at $140,000. The market yield rate for high-quality corporate bonds of similar term

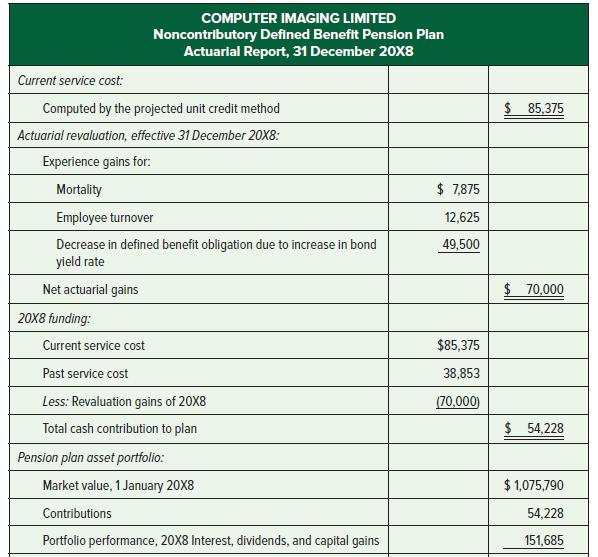

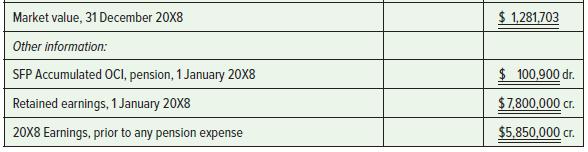

Computer Imaging Ltd. (CIL) established a formal pension plan 10 years ago to provide retirement benefits for all employees. The plan is noncontributory and is funded through a trustee that invests all funds and pays all benefits as they become due. Vesting occurs when the employee reaches age 45

Ivan Resources Corp. sponsors a defined benefit pension plan for its unionized labour force. The company disclosed the following in its annual financial statements:The company is considering the impact that changes in assumptions will have on its pension situation. Specifically, the following:a.

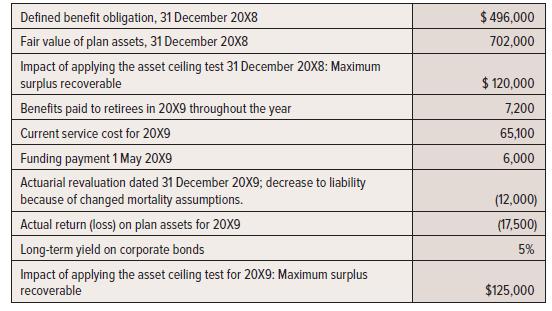

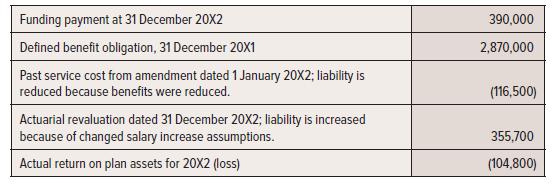

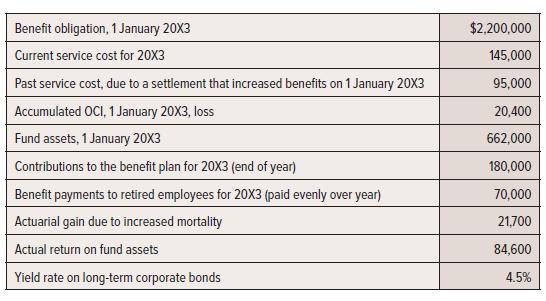

Faste Ltd. has a defined benefit pension plan. The following information relates to this plan:Required:1. Compute the defined benefit obligation at 31 December 20X1 and the fair value of plan assets on the same date.2. Analyze the three elements of pension accounting for 20X1: service cost, net

Gurung Co. has a noncontributory, defined benefit pension plan adopted on 1 January 20X5. On 31 December 20X5, the following information is available:For accounting purposes:• Interest rate used for pension amounts, 5%.• Past service cost, granted as of 1 January 20X5, $200,000. This is also

Maple Construction Corp. has a defined benefit pension plan. Information concerning the 20X7 and 20X8 fiscal years is presented below:From the plan actuary:• Current service cost in 20X7 is $430,000 and in 20X8 is $488,000.• Defined benefit obligation is $4,975,000 at the beginning of 20X7.•

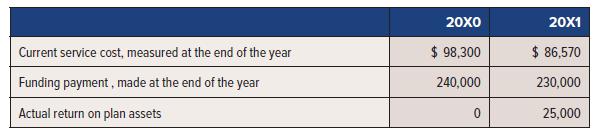

Micro Computers Inc. sponsors a defined benefit pension plan for its employees. It is now the 20X2 fiscal year. Long-term corporate borrowing rates for companies with this risk profile are 5%. Information with respect to the pension plan is as follows:Required:1. Calculate the SFP net defined

In late 20X0, Security Services Ltd. established a defined benefit pension plan for its employees. At the inception of the plan, the actuary determined the present value of the defined benefit obligation relating to employees’ past services to be $1 million, as of the beginning of 20X1. This

Refer to the data in TR19-2 and solutions to TR19-3 to TR19-5.Data From TR19-2The following data are to be used for TR19-2 to TR19-6. Good day Ltd., a public company, has a defined benefit pension plan and a 31 December year-end. The following information relates to the plan:Required:Prepare the

TCGY Ltd. reports the following data for 20X8:The company has a contributory defined benefit pension plan covering all employees over the age of 30.Required:1. How much did the pension plan assets change during the year? Name three items that would cause plan assets to change.2. How much did the

Refer to the data in TR19-9 and related solution for the opening balances. For 20X5, the following information is provided. The market yield rate for high-quality corporate bonds of similar term and identical currency is 5.5% at the end of the year. On 1 April 20X5, a contribution of $560,000 was

USLM Inc. has a defined benefit pension plan. At the end of the year 20X4, the pension fund assets were $7,670,000 and the defined benefit obligation was $7,250,000. Invoking the asset ceiling caps the net defined benefit asset at $315,000.Required:Prepare the journal entry to correctly recognize

Refer to the data in TR19-2 and your response to TR19-4.Data From TR19-2The following data are to be used for TR19-2 to TR19-6. Good day Ltd., a public company, has a defined benefit pension plan and a 31 December year-end. The following information relates to the plan:Required:Calculate and record

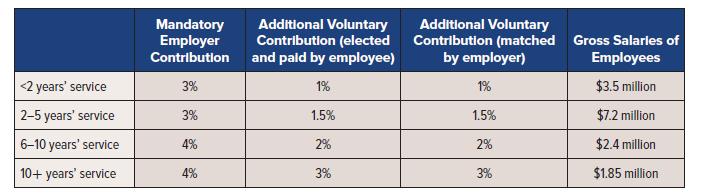

Gazra Inc. established a defined contribution pension plan at the beginning of 20X5. The company will contribute a specified percentage of each employee’s annual salary. These payments vest immediately, but the percentage contributed depends on the number of years that the employees have been

There are three major approaches to measure and allocate pension amounts to given fiscal years. These approaches are used by actuaries to determine funding amounts and by accountants to determine amounts to be recorded in financial statements. Holo Co. has a defined benefit pension plan that has

Refer to the data in TR19-2.Data From TR19-2The following data are to be used for TR19-2 to TR19-6. Good day Ltd., a public company, has a defined benefit pension plan and a 31 December year-end. The following information relates to the plan:Required:Calculate and record the second element of

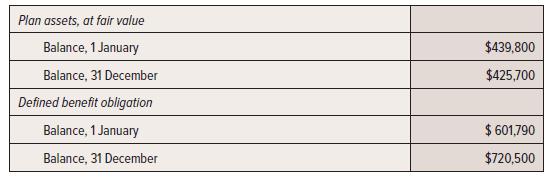

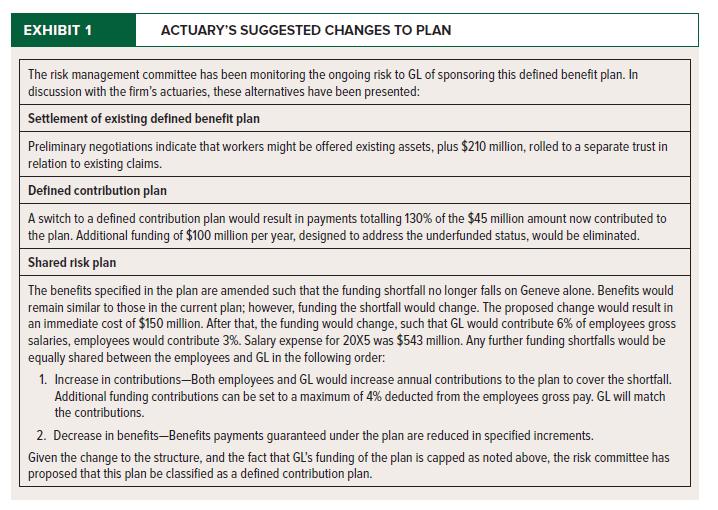

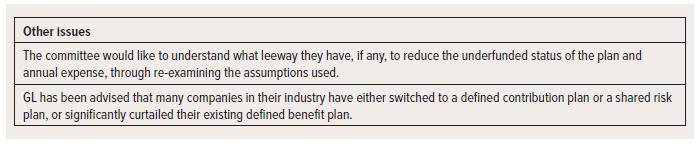

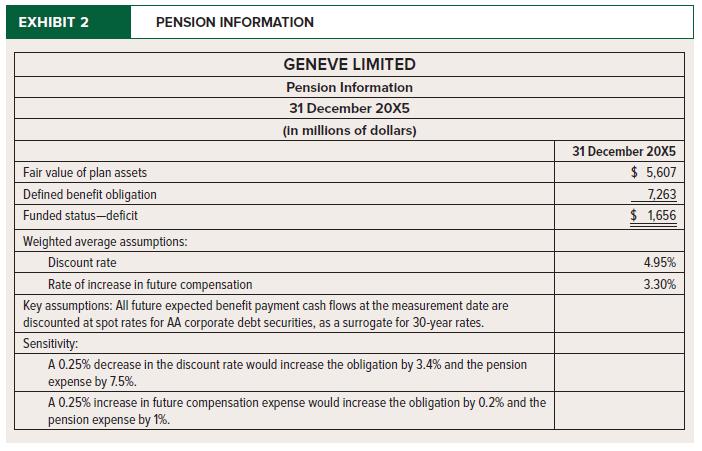

Geneve Ltd. (GL) is a manufacturer of personal and commercial transportation solutions, including train engines and train cars. The company is one of the largest private companies in Canada and complies with ASPE. GL must comply with total-debt-to-equity covenants for long-term debt arrangements,

Refer to the data in TR19-2.Data From TR19-2The following data are to be used for TR19-2 to TR19-6. Good day Ltd., a public company, has a defined benefit pension plan and a 31 December year-end. The following information relates to the plan:Required:Calculate and record the first element of

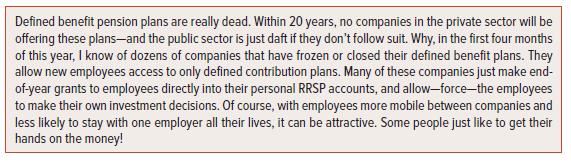

A company has a contributory defined benefit pension plan covering all employees over the age of 30. An analyst was quoted as saying:Required:1. What factors associated with defined benefit plans have led to the trend toward defined contribution plans?2. Evaluate the attractiveness of defined

Consider the following independent scenarios:Scenario A Wertz Ltd. has a pension plan for its employees. The plan requires that Wertz contribute 4% of employee salaries to a pension fund, managed by a trustee. The fund assets are pooled together and managed collectively, but the fund trustee

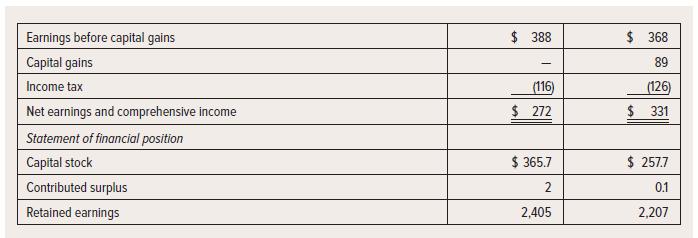

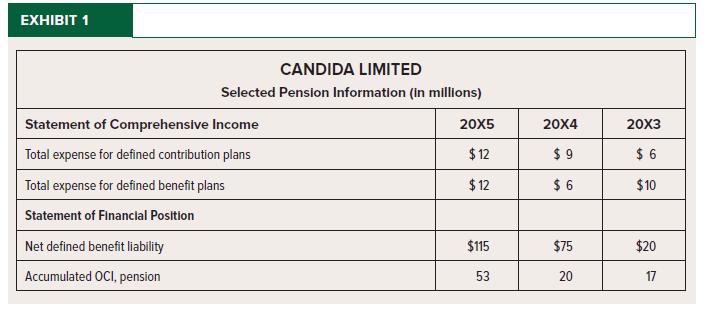

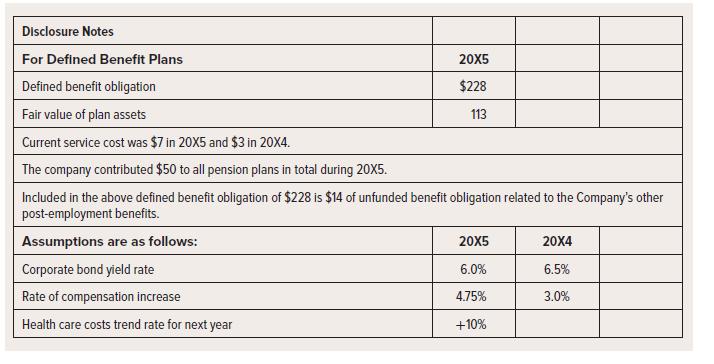

Candida Ltd. is a Canadian public company in the business of exploration, production, and marketing of natural gas. It also has power generation operations. Earnings in 20X5 were $2.4 billion, and total assets were $24.1 billion.You have recently begun work in the finance and accounting department.

Zio Ltd. established a defined contribution pension plan at the beginning of 20X9. The company will contribute 3% of each employee’s salary annually. Total salaries in 20X9 were expected to be $7.3 million. Accordingly, Zio paid $219,000 into the fund. After the year-end, it was determined that

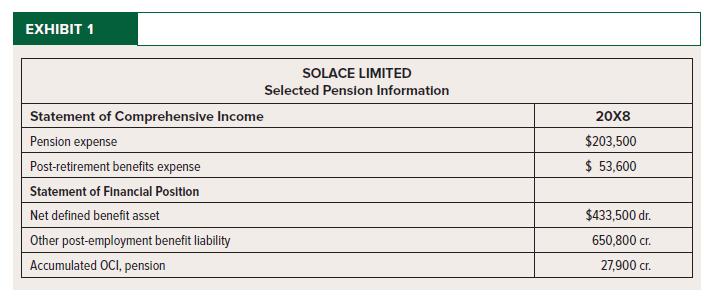

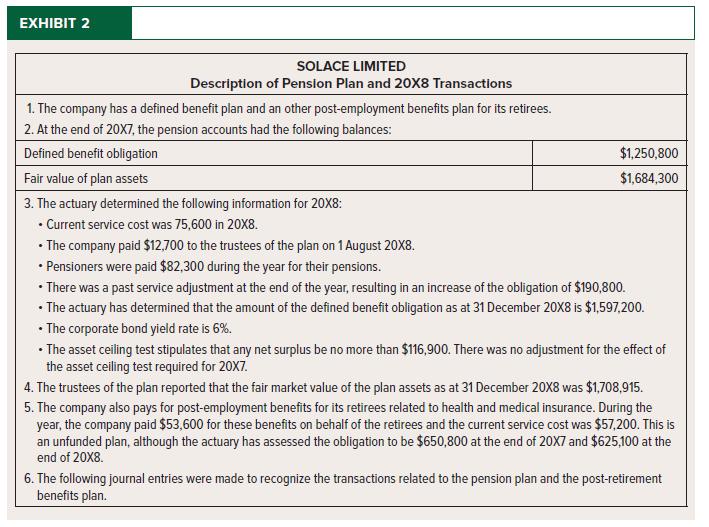

Solace Ltd. (SL) is a grocery food distributor operating nationally throughout Canada. The CFO for the company died suddenly during the year and the payroll accountant was put in charge of recording all of the transactions related to the pension plan. The company has a December fiscal year-end. You

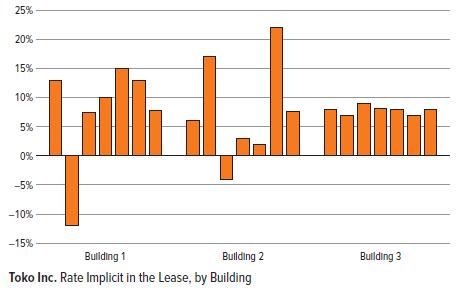

Toko Inc. is a real estate investor. The company purchases commercial properties and then resells them once the property has grown in value. This is normally done by renewing leases at higher rates or finding new tenants. You work for Toko and have been assigned to help out with their most recent

Argyle Ltd. signed a 24-month lease to rent a new computer for $170 per month. The fair value of the computer is $3,600. The lease will commence on 1 November 20X1 with payments beginning immediately. Assume that Argyle Ltd.’s IBR is 0.7% per month. Argyle is unaware of the implicit rate in the

Sotherlin Inc. has a defined contribution plan. It has agreed to pay $275,000 now at the end of 20X4 and another payment of $200,000 at the end of 20X6 for employees’ services for 20X4. The current interest rate is 5%.Required:Prepare the journal entry for the pension expense for 20X4.

Complete the sentences below:1. The actuarial cost method that must be used to determine current service cost is the ____________________.2. A pension plan where the risk of the level of eventual pension payments rests with the employee is called ____________________.3. A contributory pension plan

Brookdom Properties is a real estate developer and property manager. The company owns and operates a portfolio of retail, office, and hotel properties throughout Canada. Their mandate is to purchase high-value properties, and lease them to tenants.Required:List the data that would need to be

Jordin is an equipment dealer that occasionally uses leasing as a means of selling its products. On 1 January 20X1, Jordin leased equipment to Easten Corp. The lease term was four years with annual lease payments of $5,769 to be paid on each 31 December. The equipment has an estimated zero residual

Refer to the information in A18-9. Jeffrey Leasing Inc. is a public company. Jeffrey’s implicit interest rate in the Yvan lease is 6%.Data From A18-9On 2 January 20X4, Yvan Ltd., a public company, entered into a five-year equipment lease with Jeffery Leasing Inc. The lease calls for annual lease

Keener Construction Ltd. leased equipment for five years from Dominion Leasing Inc. for use in a building project. At the end of the five-year term, Keener returns the asset to Dominion Leasing Inc. and has a residual value guarantee of $80,000. No renewal option is available to Keener. The lease

Refer to the information in A18-8.Data From A18-8On 31 December 20X0, Columbia Inc. entered into an agreement with Scotia Ltd. to lease equipment with a useful life of 6 years. Columbia Inc. will make four equal payments of $100,000 at the beginning of each lease year. Columbia Inc. anticipates

Matteo Laboratories Ltd. (MLL) leased lab equipment from LabEquip Corp (LEC). The lease term is three years with an annual rent of $40,000, due at the beginning of the year. Initial costs for installation were $20,000, paid by MLL. The equipment has an expected useful life of four years and a fair

On 10 December 20X0, Noel Inc. entered into a six-year equipment lease with Williams Ltd. The terms of the lease are as follows:• The lease term will begin on 1 January 20X1.• The fair value of the equipment at the inception of the lease is $120,000. The equipment’s expected useful life is

On 2 January 20X5, Jayden Inc (lessee) entered into an agreement with Holstead Inc (lessor) to lease some equipment for five years. The terms of the agreement are as follows:• The fair value of the equipment at the inception of the lease is $101,000. Additional direct costs relating to the lease

On 24 February 20X1, Ready Distributing Ltd., a private company, signed a lease for conveyor equipment. This is specialized equipment that can be used only in Ready’s manufacturing plant. The fair value of the leased equipment is $500,000.The lease will commence on 1 October 20X1. The lease is

Pierce Inc. owns a building in downtown Halifax. Pierce enters into an agreement with Mattenay Corporation whereby Mattenay sells the building—but not the land on which it sits—to Mattenay and simultaneously leases it back. The details are as follows:• The original cost of the building was

JMK owns a distribution factory that it uses to store its inventory. On 1 January 20X7, the factory was sold to a large REIT for $8,700,000. The factory had an original cost of $16,000,000 and accumulated depreciation of $6,400,000 on the date of sale. As part of the agreement, the building was

On 1 January 20X2, Supergrocery Inc. sold its major distribution facility, with a 22-year remaining life, to a real estate investment trust (REIT) for $9,000,000 cash, its estimated fair value. The facility had an original cost of $10,400,000 and accumulated depreciation of $3,600,000 on the date

In May 20X0, LFT entered into the following arrangement to lease some manufacturing equipment starting on 1 June 20X0. Additional details are as follows:• The lease term commences on 1 June and is 5 years. The company has a 2 year option to renew at the same rate, which they expect to

Lessee Ltd. agreed to a noncancellable lease for which the following information is available:a. The asset is new at the inception of the lease term and is worth $160,000.b. Lease term is four years, starting 1 January 20X1.c. Estimated useful life of the leased asset is six years.d. The lessee has

Bombay Ltd. is expanding and needs more manufacturing equipment. The company has been offered a lease contract for equipment with a fair value of $260,000. The lease has a five-year term, with beginning-of-year payments. The lease is renewable for a further two years at the option of the lessee.

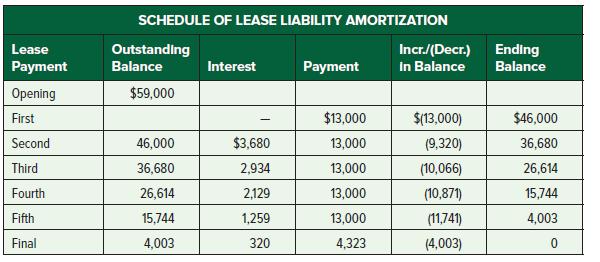

Griffiths Ltd. has a five-year lease, and the following lease liability amortization table was prepared when the lease was originally signed, using an 8% interest rate. Griffiths expects to pay $4,323 at the end of the lease related to the residual value guarantee.Required:1. The lease was entered

Jain Corp. has negotiated a lease for new machinery. Jain Corp. is excited about the new products it will be able to produce with this machinery at gross margins much higher than historical levels. The machinery has a fair value of $412,500 and an expected economic life of seven years. The lease

Watson Co. entered into a lease arrangement for a truck on 1 April 20X2 that had the following terms:• The lease payments are $12,500 per year, payable each 1 April for four years. The lease may be renewed at the option of the lessor for a further five years for $3,600 per year.• Based on an

On 1 January 20X1, Canada Leasing Inc. acquired an asset on behalf of Magnum Ltd. for $100,000. Canada Leasing and Magnum enter into a six-year lease for the asset, effective 1 January 20X1, with equal payments made by Magnum at the beginning of each lease year. Canada Leasing will earn 8% (before

On 2 January 20X4, Yvan Ltd., a public company, entered into a five-year equipment lease with Jeffery Leasing Inc. The lease calls for annual lease payments of $150,000, payable at the beginning of each lease year. Yvan’s IBR is 7%. Yvan does not know the lessor’s interest rate. The fair value

On 31 December 20X0, Columbia Inc. entered into an agreement with Scotia Ltd. to lease equipment with a useful life of 6 years. Columbia Inc. will make four equal payments of $100,000 at the beginning of each lease year. Columbia Inc. anticipates that the equipment will have a residual value of

Tartufo Corp. entered into a 5-year lease agreement with Gelato Inc. to lease equipment beginning on January 1, 20X5. The IBR is 9% while the rate implicit in the lease is 8%. Tartufo Corp. is aware of the rate implicit in the lease.Annual payments of $61,500 at the beginning of the year are

Niko Ltd. signed a lease for a five-year term that requires yearly, beginning-of-year payments of $104,000 including maintenance.Based on allocating the lease payment on relative stand-alone prices, the lease component is $94,400 and the non-lease component for maintenance is $9,600. Niko has a

On 1 January 20X2 Grocers R Us entered into a lease to rent a mid-sized tractor trailer from TT Inc. with the following terms:• The company will rent a tractor-trailer beginning 1 April 20X2 for a 4-year period. The fair value of the trailer is $280,000 and has a useful life of 7 years. The

On 31 December 20X6 Joseph’s Renovations Ltd. (JRL) entered into a lease to rent construction equipment that had the following terms:• JRL’s incremental borrowing rate is 8%; prime rate is 6%; and the implicit rate known by JRL is 9%;• The equipment’s fair value on 31 December 20X6 is

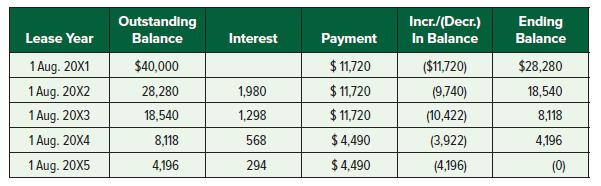

The following lease liability amortization table was developed for Smith Company and Lease 34T:Required:1. Provide an independent proof of the $18,540 liability balance after the second payment.2. Smith has a 31 December fiscal year-end. How much interest expense is recorded in 20X3?3. What is the

On 1 January 20X6 Canadian Leasing Inc. leased a piece of machinery to Ornamental Concrete Ltd., with the following terms:• The lease is for five years; Ornamental cannot cancel the lease during this period.• The lease payment is $79,600 per year including insurance payments. Based on

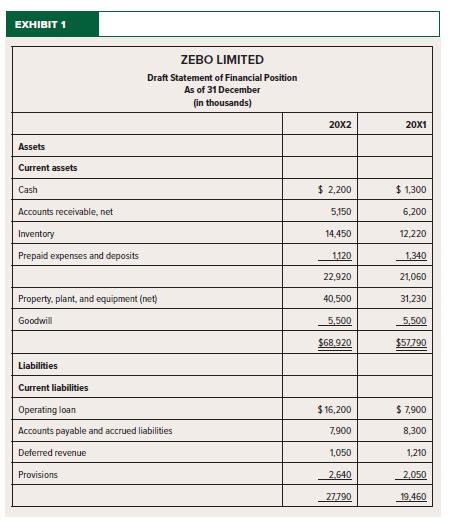

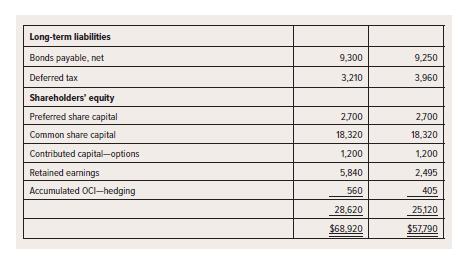

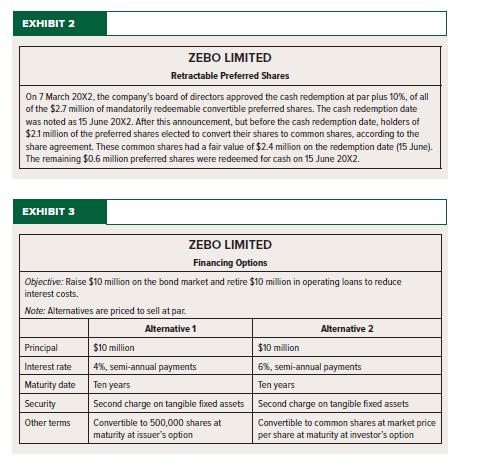

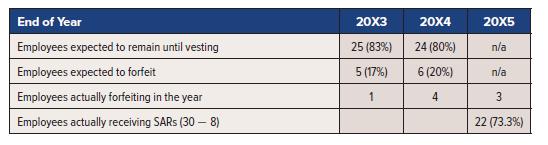

“Amelia, I need you to put your other projects on hold and do a little work on these financials for me.”You follow Jeng Wong, your boss and special projects manager for Holdings Ltd., into his office. It is mid-January 20X3 and Jeng needs your assistance in reviewing some issues at Zebo Ltd., a

Peridis Inc. has entered into a contract with an asset-based finance company to lease some equipment commencing January 1, 20X1. The lease payments are $20,000 per year for 8 years, with payments commencing at the start of each lease year. At the end of the lease, Peridis guarantees to either (1)

On 18 December 20X1, Kushner Construction Ltd. leased a crane from Schultz Equipment Inc. for use in a building project. The lease is for three years. The lease commences on 1 January 20X2.Annual lease payments are $150,000, payable at the beginning of each year. In addition, Kushner must pay

Information has been gathered for two leases:Lease A • The fair value of the equipment is $800,000 at the inception of the lease.• The lease term is 5 years, and there is a 3-year renewal term at the option of the lessor.• Annual lease payments are $145,000 per year for the first 5 years

A large, public telecommunications company has the following leases: Lease A Lease of office space for 5 years, with a 5-year renewal period. Rental payments are $5,000/month, due at the beginning of each month. Lease B Leases of IT equipment for individual employees. Equipment

Argyle Ltd. signed a 24-month lease to rent a new computer for $170 per month. The fair value of the computer is $3,600. The lease will commence on 1 November 20X1 with payments beginning immediately. Assume that Argyle Ltd.’s IBR is 0.7% per month. Argyle is unaware of the implicit rate in the

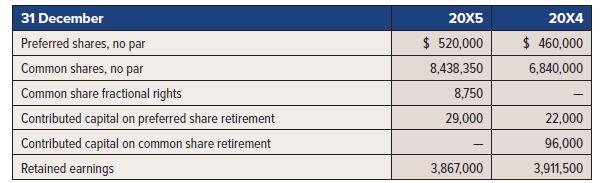

Pacific Trading Co. has a SARs program for managers. These individuals receive a cash payment after three years of service, calculated as the excess of share price over $10. In early 20X3, the 30 members of the management team in total are granted 25,000 units in the program. The payment is made at

On 1 June 20X6 Marino Developments Inc. entered into a 12-month contract to lease a backhoe from Constructors Ltd. for $3,700 monthly with payments made at the beginning of each month. Marino’s annual incremental borrowing rate is 6% and Marino is not aware of the rate implicit in the lease. The

The following data relates to Ottawa Ltd.:Transactions during the year:1. Preferred shares were issued for $100,000 during the year. Share issue costs of $2,000 were charged directly to retained earnings. Other preferred shares were retired.2. On 31 December 20X4, there were 570,000 common shares

Scenario A Crayoli Inc. is a publicly traded company. During the year, one of the bigger investors contributed land that was purchased by the investor for $800,000 in exchange for 40,000 common shares. The land was recently appraised at $1.5million. Crayoli’s common shares are currently

Showing 2000 - 2100

of 2378

First

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

Step by Step Answers