New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

model based testing for embedded systems

Wiley CPA Exam Review Problems And Solutions Vol 2 2011-2012 38th Edition O. Ray Whittington, Patrick R. Delaney - Solutions

22. Mien Co. is budgeting sales of 53,000 units of product Nous for October 2009. The manufacture of one unit of Nous requires four kilos of chemical Loire. During October 2009, Mien plans to reduce the inventory of Loire by 50,000 kilos and increase the finished goods inventory of Nous by 6,000

21. Which of the following is an output of a financial planning model?a. Strategic plan.b. Actual financial results.c. Projected financial statements.d. Variance analysis.

20. A single-product company prepares income statements using both absorption and variable costing methods. Manufacturing overhead cost applied per unit produced in 2009 was the same as in 2008. The 2009 variable costing statement reported a profit whereas the 2009 absorption costing statement

19. A manufacturing company prepares income statements using both absorption and variable costing methods. At the end of a period actual sales revenues, total gross profit, and total contribution margin approximated budgeted figures, whereas net income was substantially greater than the budgeted

18. At the end of Killo Co.’s first year of operations, 1,000 units of inventory remained on hand. Variable and fixed manufacturing costs per unit were $90 and $20, respectively.If Killo uses absorption costing rather than variable (direct)costing, the result would be a higher pretax income ofa.

17. Using the variable costing method, which of the following costs are assigned to inventory?Variable selling and Variable factory administrative costs overhead costsa. Yes Yesb. Yes Noc. No Nod. No Yes

16. In its first year of operations, Magna Manufacturers had the following costs when it produced 100,000 and sold 80,000 units of its only product:Manufacturing costs Fixed $180,000 Variable 160,000 Selling and admin. costs Fixed 90,000 Variable 40,000 How much lower would Magna’s net income be

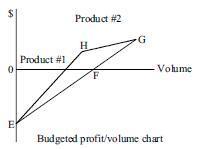

15. In the budgeted profit/volume chart below, EG represents a two-product company’s profit path. EH and HG represent the profit paths of products #1 and #2, respectively.Sales prices and cost behavior were as budgeted, actual total sales equaled budgeted sales, and there were no inventories.

14. In calculating the breakeven point for a multi-product company, which of the following assumptions are commonly made when variable costing is used?I. Sales volume equals production volume.II. Variable costs are constant per unit.III. A given sales mix is maintained for all volume changes.a. I

13. Thomas Company sells products X, Y, and Z. Thomas sells three units of X for each unit of Z, and two units of Y for each unit of X. The contribution margins are $1.00 per unit of X, $1.50 per unit of Y, and $3.00 per unit of Z.Fixed costs are $600,000. How many units of X would Thomas sell at

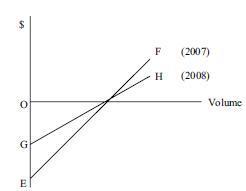

12. In the profit-volume chart below, EF and GH represent the profit-volume graphs of a single-product company for 2007 and 2008, respectively.If 2007 and 2008 unit sales prices are identical, how did total fixed costs and unit variable costs of 2008 change compared to 2007? 2008 total 2008 unit

11. Which one of the following is and advantage of using variable costing?a. Variable costing complies with the US Internal Revenue Code.b. Variable costing complies with generally accepted accounting principles.c. Variable costing makes cost-volume relationships more easily apparent.d. Variable

10. If sales dollars are used to measure activity levels, total costs and total revenues may be read from the X and Y axis as follows:Total costs Total revenuesa. X or Y X or Yb. X or Y X onlyc. Y only X or Yd. Y only X only

9. At point A compared to point B, as a percentage of sales revenues Variable costs are Fixed costs area. Greater Greaterb. Greater The samec. The same The samed. The same Greater

8. On January 1, 2009, Lake Co. increased its direct manufacturing labor wage rates. All other budgeted costs and revenues were unchanged. How did this increase affect Lake’s budgeted breakeven point and budgeted margin of safety?Budgeted Budgeted Breakeven point margin of safetya. Increase

7. Product Cott has sales of $200,000, a contribution margin of 20%, and a margin of safety of $80,000. What is Cott’s fixed cost?a. $16,000b. $24,000c. $80,000d. $96,000

6. Breakeven analysis assumes that over the relevant rangea. Unit revenues are nonlinear.b. Unit variable costs are unchanged.c. Total costs are unchanged.d. Total fixed costs are nonlinear.** CMA adapted

5. During 2008, Thor Lab supplied hospitals with a comprehensive diagnostic kit for $120. At a volume of 80,000 kits, Thor had fixed costs of $1,000,000 and a profit before income taxes of $200,000. Due to an adverse legal decision, Thor’s 2009 liability insurance increased by $1,200,000 over

4. Associated Supply, Inc. is considering introducing a new product that will require a $250,000 investment of capital. The necessary funds would be raised through a bank loan at an interest rate of 8%. The fixed operating costs associated with the product would be $122,500 while the contribution

3. Del Co. has fixed costs of $100,000 and breakeven sales of $800,000. What is its projected profit at $1,200,000 sales?a. $ 50,000b. $150,000c. $200,000d. $400,000

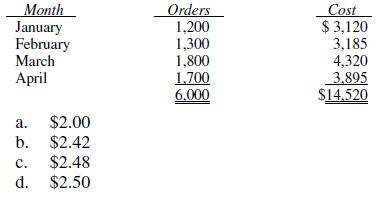

Day Mail Order Co. applied the high-low method of cost estimation to customer order data for the first four months of 2009. What is the estimated variable order filling cost component per order? Month Orders Cost January 1,200 $ 3,120 February 1,300 3,185 March 1,800 4,320 April 1,700 3.895 6.000

The following information pertains to a by-product called Moy:Sales in 2009 5,000 units Selling price per unit $6 Selling costs per unit 2 Processing costs 0 Inventory of Moy was recorded at net realizable value when produced in 2008. No units of Moy were produced in 2009.What amount should be

Mig Co., which began operations in 2009, produces gasoline and a gasoline by-product. The following information is available pertaining to 2009 sales and production:Total production costs to split-off point $120,000 Gasoline sales 270,000 By-product sales 30,000 Gasoline inventory, 12/31/09 15,000

For purposes of allocating joint costs to joint products, the sales price at point of sale, reduced by cost to complete after split-off, is assumed to be equal to thea. Joint costs.b. Total costs.c. Net sales value at split-off.d. Sales price less a normal profit margin at point of sale.

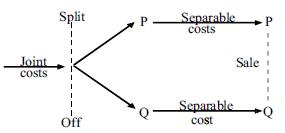

The diagram below represents the production and sales relationships of joint products P and Q. Joint costs are incurred until split-off, then separable costs are incurred in refining each product. Market values of P and Q at split-off are used to allocate joint costs.If the market value of P at

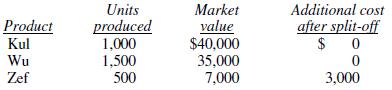

Lane Co. produces main products Kul and Wu. The process also yields by-product Zef. Net realizable value of by-product Zef is subtracted from joint production cost of Kul and Wu. The following information pertains to production in July 2009 at a joint cost of $54,000:If Lane uses the net realizable

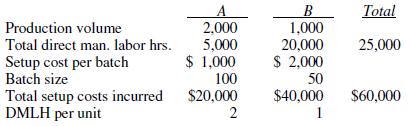

Hoger Corporation accumulated the following cost information for its two products, A and B:A traditional costing system would allocate setup costs on the basis of DMLH. An ABC system would trace costs by spreading the costs per batch over the units in a batch. What is the setup cost per unit of

Nile Co.’s cost allocation and product costing procedures follow activity-based costing principles. Activities have been identified and classified as being either valueadding or non-value-adding as to each product. Which of the following activities, used in Nile’s production process, is

In an activity-based costing system, cost reduction is accomplished by identifying and eliminating All cost drivers Non-value-adding activitiesa. No Nob. Yes Yesc. No Yesd. Yes No

In an activity-based costing system, what should be used to assign a department’s manufacturing overhead costs to products produced in varying lot sizes?a. A single cause-and-effect relationship.b. Multiple cause-and-effect relationships.c. Relative net sales values of the products.d. A

Which of the following is true about activity-based costing?a. It should not be used with process or job costing.b. It can be used only with process costing.c. It can be used only with job costing.d. It can be used with either process or job costing.

What is the normal effect on the numbers of cost pools and allocation bases when an activity-based cost (ABC)system replaces a traditional cost system?Cost pools Allocation basesa. No effect No effectb. Increase No effectc. No effect Increased. Increase Increase

In Belk Co.’s just-in-time production system, costs per setup were reduced from $28 to $2. In the process of reducing inventory levels, Belk found that there were fixed facility and administrative costs that previously had not been included in the carrying cost calculation. The result was an

An assembly plant accumulates its variable and fixed manufacturing overhead costs in a single cost pool which are then applied to work in process using a single application base. The assembly plant management wants to estimate the magnitude of the total manufacturing overhead costs for different

Which of the following would be a reasonable basis for allocating the material handling costs to the units produced in an activity-based costing system?a. Number of production runs per year.b. Number of components per completed unit.c. Amount of time required to produce one unit.d. Amount of

Using the weighted-average method, the total cost of the units in the ending work in process inventory at May 31 isa. $ 86,400b. $154,800c. $155,328d. $156,960

Using the weighted-average method, the equivalent unit conversion cost for May isa. $5.65b. $5.83c. $6.00d. $6.41

Using the weighted-average method, the equivalent unit cost of materials for May isa. $4.12b. $4.50c. $4.60d. $5.03

Using the FIFO method, the total cost of units in the ending work in process inventory at May 31 isa. $153,168b. $145,800c. $155,328d. $156,960

Using the FIFO method, the equivalent unit conversion cost for May isa. $5.65b. $5.83c. $6.00d. $6.20

Using the FIFO method, the equivalent unit cost of materials for May isa. $4.12b. $4.50c. $4.60d. $4.80

Using the FIFO method, the equivalent units of production for conversion costs area. 85,600 units.b. 88,800 units.c. 95,200 units.d. 98,400 units.

Using the first-in, first-out (FIFO) method, the equivalent units of production for materials area. 97,600 units.b. 104,000 units.c. 107,200 units.d. 108,000 units.

In its April 2009 production, Hern Corp., which does not use a standard cost system, incurred total production costs of $900,000, of which Hern attributed $60,000 to normal spoilage and $30,000 to abnormal spoilage. Hern should account for this spoilage asa. Period cost of $90,000.b. Inventoriable

A department adds material at the beginning of a process and identifies defective units when the process is 40%complete. At the beginning of the period, there was no work in process. At the end of the period, the number of work in process units equaled the number of units transferred to finished

A process costing system was used for a department that began operations in January 2009. Approximately the same number of physical units, at the same degree of completion, were in work in process at the end of both January and February. Monthly conversion costs are allocated between ending work in

In process 2, material G is added when a batch is 60%complete. Ending work in process units, which are 50%complete, would be included in the computation of equivalent units for Conversion costs Material Ga. Yes Nob. No Yesc. No Nod. Yes Yes

In computing the current period’s manufacturing cost per equivalent unit, the FIFO method of process costing considers current period costsa. Only.b. Plus cost of beginning work in process inventory.c. Less cost of beginning work in process inventory.d. Plus cost of ending work in process

The Forming Department is the first of a two-stage production process. Spoilage is identified when the units have completed the Forming process. Costs of spoiled units are assigned to units completed and transferred to the second department in the period spoilage is identified. The following

The following information pertains to Lap Co.’s Palo Division for the month of April:Number of units Cost of materials Beginning work in process 15,000 $ 5,500 Started in April 40,000 18,000 Units completed 42,500 Ending work in process 12,500 All materials are added at the beginning of the

In a process cost system, the application of factory overhead usually would be recorded as an increase ina. Finished goods inventory control.b. Factory overhead control.c. Cost of goods sold.d. Work in process inventory control.

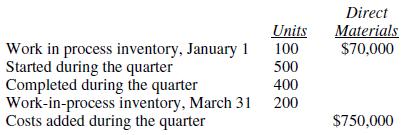

Kerner Manufacturing uses a process cost system to manufacture laptop computers. The following information summarizes operations relating to laptop computer model#KJK20 during the quarter ending March 31:Units Direct Materials Work in process inventory, January 1 100 $50,000 Started during the

Kerner Manufacturing uses a process cost system to manufacture laptop computers. The following information summarizes operations relating to laptop computer model#KJK20 during the quarter ending March 31:Beginning work in process inventory was 50% complete for direct materials. Ending work in

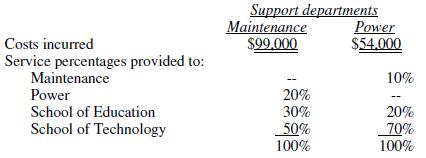

Parat College allocates support department costs to its individual schools using the step method. Information for May 2009 is as follows:What is the amount of May 2009 support department costs allocated to the School of Education?a. $40,500b. $42,120c. $46,100d. $49,125 Costs incurred Service

Worley Company has underapplied variable overhead of $45,000 for the year ended December 31, 2009. Before disposition of the underapplied overhead, selected December 31, 2009 balances from Worley’s accounting records are as follows:Sales $1,200,000 Cost of goods sold 720,000 Inventories:Direct

A job order cost system uses a predetermined fixed factory overhead rate based on normal activity and expected fixed cost. At the end of the year, underapplied fixed overhead might be explained by which of the following situations?Actual volume Actual fixed costsa. Greater than normal Greater than

In developing a predetermined variable factory overhead application rate for use in a process costing system, which of the following could be used in the numerator and denominator?Numerator Denominatora. Actual variable factory overhead Actual machine hoursb. Actual variable factory overhead

A company services office equipment. Some customers bring their equipment to the company’s service shop;other customers prefer to have the company’s service personnel come to their offices to repair their equipment. The most appropriate costing method for the company isa. A job order costing

A direct manufacturing labor overtime premium should be charged to a specific job when the overtime is caused by thea. Increased overall level of activity.b. Customer’s requirement for early completion of job.c. Management’s failure to include the job in the production schedule.d.

Under Pick Co.’s job order costing system manufacturing overhead is applied to work in process using a predetermined annual overhead rate. During January 2009, Pick’s transactions included the following:Direct materials issued to production $ 90,000 Indirect materials issued to production 8,000

In a job cost system, manufacturing overhead is An indirect A necessary element cost of jobs in productiona. No Yesb. No Noc. Yes Yesd. Yes No

Birk Co. uses a job order cost system. The following debits (credit) appeared in Birk’s work in process account for the month of April 2009:April Description Amount 1 Balance $ 4,000 30 Direct materials 24,000 30 Direct manufacturing labor 16,000 30 Factory overhead 12,800 30 To finished goods

Costs are accumulated by responsibility center for control purposes when using Job order costing Process costinga. Yes Yesb. Yes Noc. No Nod. No Yes

In a job-costing system, issuing indirect materials to production increases which account?a. Materials control.b. Work in process control.c. Manufacturing overhead control.d. Manufacturing overhead allocated.

Gram Co. develops computer programs to meet customers’special requirements. How should Gram categorize payments to employees who develop these programs?Direct costs Valueadded costsa. Yes Yesb. Yes Noc. No Nod. No Yes

The fixed portion of the semivariable cost of electricity for a manufacturing plant is a Period cost Product costa. Yes Nob. Yes Yesc. No Yesd. No No

Fab Co. manufactures textiles. Among Fab’s 2009 manufacturing costs were the following salaries and wages:Loom operators $120,000 Factory foreman 45,000 Machine mechanics 30,000 What was the amount of Fab’s 2009 direct manufacturing labor?a. $195,000b. $165,000c. $150,000d. $120,000

During the month of March 2009, Nale Co. used$300,000 of direct material. At March 31, 2009, Nale’s direct materials inventory was $50,000 more than it was at March 1, 2009. Direct material purchases during the month of March 2009 amounted toa. $0b. $250,000c. $300,000d. $350,000

For the month of March 2009, cost of goods manufactured wasa. $218,000b. $224,000c. $230,000d. $236,000

For the month of March 2009, conversion cost wasa. $ 90,000b. $140,000c. $144,000d. $170,000

For the month of March 2009, prime cost wasa. $ 90,000b. $120,000c. $144,000d. $150,000

The following information was taken from Kay Company’s accounting records for the year ended December 31, 2009:Increase in raw materials inventory $ 15,000 Decrease in finished goods inventory 35,000 Raw materials purchased 430,000 Direct manufacturing labor payroll 200,000 Factory overhead

Which statement best describes the objective of the theory of constraints?Throughput contribution Investment Operating costsa. Increase Decrease Decreaseb. Increase Increase Increasec. Decrease Increase Decreased. Increase Increase Decrease

Three of the basic measurements used by the Theory of Constraints (TOC) area. Gross margin (or gross profit), return on assets, and total sales.b. Number of constraints (or subordinates), number of nonconstraints, and operating leverage.c. Throughput (or throughput contribution), inventory(or

Antlers, Inc. produces a single product that sells for$150 per unit. The product is processed through the Cutting and Finishing departments. Additional data for these departments are as follows:Cutting Finishing Annual capacity (36,000 direct labor hours available in each department) 180,000 units

In the theory of constraints, an operation or resource where the work performed approaches or exceeds the available is referred to asa. A bottleneck.b. A time driver.c. Customer-response time.d. Manufacturing lead time.

At which phase in the business process management life-cycle does management simulate performance of the process in a test environment?a. Design.b. Modeling.c. Execution.d. Optimization.

Management of organizations that engage in business process management view business processes asa. Requirements for good control over the organization.b. Systems that provide information for good management.c. Strategic assets that must be understood, managed and improved.d. Mechanisms that keep

In an attempt to improve operations, companies often go through analyses and redesign of the way processes are performed. Which of the following is not considered to be an aspect of a business process that may be focused on to achieve improvement?a. Technology.b. Human performance.c. The

In the cost of quality, costs incurred in detecting individual units of product that do not conform to specifications area. Prevention costs.b. Appraisal costs.c. Internal failure costs.d. External failure costs.

Delta Manufacturing Co. has had a problem with its product quality. The company has had a large amount of costs related to product recalls. In considering cost of quality methodology, if the company wants to reduce these costs, the most likely place to incur costs would be fora. Prevention.b.

In the cost of quality, which of the following is an example of a “prevention cost”?a. Cost of inspecting products on the production line by quality inspectors.b. Labor cost of product designers whose task is to design components that will not break under extreme temperature conditions.c. Cost

In the cost of quality, which of the following is an example of an “internal failure”?a. Cost of inspecting products on the production line by quality inspectors.b. Labor cost of product designers whose task is to design components that will not break under extreme temperature conditions.c.

In considering cost of quality methodology, quality circles are associated witha. Prevention.b. Appraisal.c. Internal failure.d. External failure.

Which of the following quality tools is another term for continuous improvement?a. Theory of constraints.b. Kaizen.c. Six-sigma.d. Lean manufacturing.

Which of the statements best describes the concept of six-sigma quality?a. 10 defects per million.b. 3.4 defects per million.c. 6.0 defects per million.d. 100 defects per million.

A tool which identifies potential causes for failures or defects isa. Control chart.b. Pareto diagram.c. Cause-and-effect diagram.d. Strategy map.

A tool which indicates how frequently each type of defect occurs is aa. Control chart.b. Pareto diagram.c. Cause-and-effect diagram.d. Fishbone diagram.

Which measures would be useful in evaluating the performance of a manufacturing system?I. Throughput time.II. Total setup time for machines/Total production time.III. Number of rework units/Total number of units completed.a. I and II only.b. II and III only.c. I and III only.d. I, II, and III.

Southwest Airlines benchmarked the process of turning around an airplane with the pit stop process for formula racecars. This is an example ofa. Internal benchmarking.b. Generic benchmarking.c. Competitor benchmarking.d. Functional benchmarking.

The early liquidation of a long-term note with cash affects thea. Current ratio to a greater degree than the quick ratio.b. Quick ratio to a greater degree than the current ratio.c. Current and quick ratio to the same degree.d. Current ratio but not the quick ratio.

The issuance of serial bonds in exchange for an office building, with the first installment of the bonds due late this year,a. Decreases net working capital.b. Decreases the current ratio.c. Decreases the quick ratio.d. Affects all of the answers as indicated.

The issuance of new shares in a five-for-one split of common stocka. Decreases the book value per share of common stock.b. Increases the book value per share of common stock.c. Increases total shareholders’ equity.d. Decreases total shareholders’ equity.

Obsolete inventory of $125,000 was written off during the year. This transactiona. Decreased the quick ratio.b. Increased the quick ratio.c. Increased net working capital.d. Decreased the current ratio.

The collection of a current accounts receivable of$29,000 woulda. Increase the current ratio.b. Decrease the current ratio and the quick ratio.c. Increase the quick ratio.d. Not affect the current or quick ratios.

The purchase of raw materials for $85,000 on open account woulda. Increase the current ratio.b. Decrease the current ratio.c. Increase net working capital.d. Decrease net working capital.

Payment of a trade account payable of $64,500 woulda. Increase the current ratio but the quick ratio would not be affected.b. Increase the quick ratio but the current ratio would not be affected.c. Increase both the current and quick ratios.d. Decrease both the current and quick ratios.

The 2009 return on assets for McKeon Company isa. 0.261b. 0.148c. 0.157d. 0.166

McKeon Company’s total asset turnover for 2009 isa. 0.805b. 0.761c. 0.722d. 0.348

Using a 365-day year, McKeon’s inventory turnover isa. 2.133b. 2.281c. 1.995d. 4.615

Showing 600 - 700

of 4678

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers