New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

financial modeling

Financial Modeling 4th Edition Simon Benninga - Solutions

Use the Black-Scholes model to price the following:• A call option on a stock whose current price is 50, with exercise price X = 50, T = 0.5, r = 10%, σ = 25%.• A put option with the same parameters.

An investment bank is offering a security linked to the price 2 years from today of Bisco stock, which is currently at $3 per share. Denote Bisco’s stock price in two periods by S2. The security being offered pays off max(S32 − 40, 0). You estimate that in each of the next two periods, Bisco

Reconsider the above problem. Show that if the date 1 exercise price is X , the date 2 exercise price is X *(1 + r), and the date 3 exercise price is X*(1 + r )2, you will not exercise the option early.

A call option is written on a stock whose current price is $50. The option has maturity of 3 years, and during this time the annual stock price is expected to increase by 25% or to decrease by − 10%. The annual interest rate is constant at 6%. The option is exercisable at date 1 at a price of

This problem is a continuation of the discussion of section 16.6. Show that as n → ∞, the binomial European put price converges to the Black-Scholes put price. (Note that, as part of the chapter spreadsheet for this chapter, we have included a function called BSPut , which computes the

A prominent securities firm recently introduced a new financial product. This product, called “The Best of Both Worlds” (BOBOW for short), costs $10. It matures in 5 years, at which point it repays the investor the $10 cost plus 120% of any positive return in the S&P 500 index. There are no

A stock is currently selling for 60. The price of the stock at the end of the year is expected either to increase by 25% or to decrease by 20%. The riskless interest rate is 5%. Calculate the price of a European put on the stock with exercise price 55. Use the binomial option pricing model.

All reliable analysts agree that a share of ABC Corp., selling today for $50, will be priced at either $65 or $45 1 year from now. They further agree that the probabilities of these events are 0.6 and 0.4, respectively. The market risk-free rate is 6%. What is the value of a call option on ABC

In a binomial model a call option and a put option are both written on the same stock. The exercise price of the call option is 30 and the exercise price of the put option is 40. The call option’s payoffs are 0 and 5 and the put option’s payoffs are 20 and 5. The price of the call is 2.25 and

A stock selling for $25 today will, in 1 year, be worth either $35 or $20. If the interest rate is 8%, what is the value today of a one-year call option on the stock with exercise price $30? Use the simultaneous equation approach of section 16.2 to price the option.

A share of Formila Corp. is currently trading at $38.50, and a 1-year call option on Formila with X = $40 is trading at $3. The risk-free interest rate is 4.5%.a. What should be the price of a 1-year put option on the stock with X = $40? Why?b. If the price of a put is $2, construct an arbitrage

The current stock price of ABC Corp. is 50. Prices for six-month calls on ABC are given in the table below. Draw a profit diagram of the following strategy: Buy one 40 call, write two 50 calls, buy one 60 call, and write two 70 calls.Call

Prove Proposition 6. Then solve the following problem: Three puts on shares of XYZ with the same expiration date are selling at the following prices:Exercise price 40: 6Exercise price 50: 4Exercise price 60: 1Show an arbitrage strategy which allows you to profit from these prices and prove that it

A European call with a maturity of 6 months and exercise price X = 80 is written on a stock whose current price is 85 is selling for $12.00; a European put written on the same stock with the same maturity and with the same exercise price is selling for $5.00. If the annual interest rate

A share of ABC Corp. sells for $95. A call on the share with exercise price $90 sells for $8.a. Graph the profit pattern from buying one share and one call on the share.b. Graph the profit pattern from buying one share and two calls.c. Consider the profit pattern from buying one share and calls. At

Consider the following two calls:• Both calls are written on shares of ABC Corp. whose current share price is $100. ABC does not pay any dividends.• Both calls have one year to maturity.• One call has X1 = 90 and has price of 30; the second call has X2 = 100 and has price of 20.• The

A put with an exercise price of 50 has a price of 6 and a call on the same stock with an exercise price of 60 has a price of 10. Both put and call have the same expiration date. On the same set of axes, draw the profit diagram for:a. One put bought and one call bought.b. Two puts bought and one

A European call option is written on a stock whose current price S = 80. The exercise price X = 80, the interest rate r = 8%, and the time to option exercise T = 1. The stock is assumed to pay a dividend of 3 at time t = ½. Use Proposition 7 to determine the minimum price of the call option.

An American call option is written on a stock whose price today is S = 50. The exercise price of the call is X = 45.a. If the call price is 2, explain how you would use arbitrage to make an immediate profit.b. If the option is exercisable at time T = 1 year and if the interest rate is 10%, what is

When you looked at the newspaper quotes for options on ABC stock, you saw that a February call option with X = 37.5 is priced at 6.375, whereas the April call option with the same exercise price is priced at 6. Can you devise an arbitrage out of these prices? Do you have an explanation for the

Another analyst believes that HD will return only 0.5% per month over the next year. What are her recommended portfolio proportions?

You are an analyst investing in the high-beta DJ30 portfolio from the previous problem. You believe that the monthly return of MMM will be 1%. What are your recommended optimal portfolio proportions?

Using the efficient portfolio instead of the S&P 500:a. Compute the monthly returns on the efficient portfolio.b. Regress the average monthly returns of the stocks on their betas with respect to the efficient portfolio.c. Explain your results in light of Propositions 3 and 4 from Chapter 9.

Perform the second-pass regression: Regress the monthly average returns on the betas of the assets. Does this confirm that the S&P 500 is efficient?

Compute the GMVP using the constant correlation covariance matrix.

Compute the global minimum variance portfolio (GMVP) using the sample variance covariance matrix.

Use the function SIM defined in the chapter to compute the single-index variance-covariance matrix.

Compute the sample variance-covariance matrix and the correlation matrix for the six stocks.

In the previous problem find two portfolios whose standard deviation is 45%. (There is an analytical solution to this problem, but it can also be solved by Solver.)

The exercise disk for this chapter contains monthly data for stock prices of Kellogg and IBM. Compute the return statistics and graph a frontier of combinations of the two stocks.

Perform a sensitivity analysis (using Data|Table) on the certainty-equivalence factor in Section 7.5, showing how the IRR of the differential cash flows varies with the CE factor.

In the project finance pro forma of section 5.8 it is assumed that the firm pays off its initial debt of 1,000 in equal installments of principal over 5 years. Change this assumption and assume instead that the firm pays off its debt in equal payments of interest and principal over 5 years.

Repeat the above exercise, but this time replace the terminal value by an EBITDA (earnings before interest, taxes, depreciation, and amortization) ratio times year-5 anticipated EBITDA. Show a graph of the equity value of the firm as a function of the assumed year 5 EBITDA ratio, varying this ratio

In the valuation exercise of section 5.4, the terminal value is calculated using a Gordon dividend model on the cash flows. Replace this terminal value by the year 5 book value of debt + equity. This means that you are essentially assuming that the book value correctly predicts the market value.

In the model of section 5.6, assume that the firm needs to have minimum cash balances of 25 at the end of each year. Introduce this constraint into the model.

Consider the model in section 5.6 (where debt is the plug).a. Suppose that the firm has 1,000 shares and that it decides to pay, in year 1, a dividend per share of 15 cents. In addition, suppose that it wants this dividend per share to grow in subsequent years by 12% per year. Incorporate these

Suppose that in the model of section 5.1 the fixed assets at cost for years 1–5 are 100% of sales (in the current model, it is net fixed assets which are a function of sales). Change the model accordingly. Show the resulting profit and loss statements, balance sheets, and free cash flows for

Here’s a basic exercise that will help you understand what’s going on in the modeling of financial statements. Replicate the model in section 5.1. That is, enter the correct formulas for the cells and see that you get the same results as the book. (This turns out to be more of an exercise in

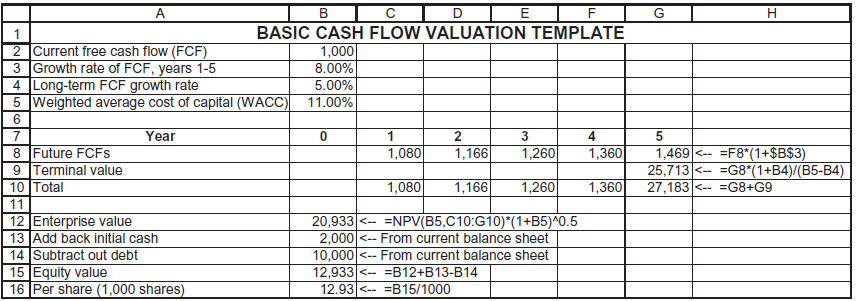

The files that accompany this book contains information for Kellogg. Use this information and the template of section 4.1 to value Kellogg. B C D E I F BASIC CASH FLOW VALUATION TEMPLATE A 2 Current free cash flow (FCF) 3 Growth rate of FCF, years 1-5 4 Long-term FCF growth rate 5 Weighted average

The template for exercise 14 gives the 10-year history of Intel’s quarterly dividends. Compute Intel’s cost of equity rE using the Gordon dividend model. Compare the cost of equity computed on the basis of 10 years of growth with that computed on the last 5 years of growth.

The template for exercise 12 gives the prices of the Vanguard Index 500 Fund (symbol: VFINX). This fund’s prices replicate the S&P 500 with dividends reinvested. Use these data to estimate the expected return on the S&P 500 in two variations: All the data, the last 2 years. (This exercise

Use the template for the ABC Corp. valuation in section 2.7 to value Cisco stock. Assume that the weighted average cost of capital for Cisco is 12.6%, the growth rate for years 1–5 is 4%, and that the long-term growth rate is 0%. (Details and template on the disk that accompanies this book.)

Examine Cisco’s consolidated statement of cash flows (on the disk that accompanies this book) and transform this into a free cash flow.

Three years of balance sheets for Cisco are given on the disk with this book. Restate these balance sheets so that the accounting enterprise value is on the left side.

The disk for these exercises gives 5 years of monthly prices for two Vanguard funds—the Vanguard Index 500 fund (symbol VFINX) and the Vanguard High-Yield Corporate Bond fund (VWEHX). The first of these funds tracks the Standard and Poor’s 500, and VWEHX is a junk-bond fund. Compute the monthly

Continuing with the above example: Find the maximum rental which ABC will pay and the minimum rental which XYZ will accept.

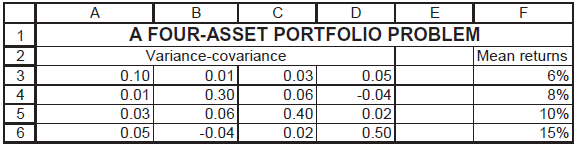

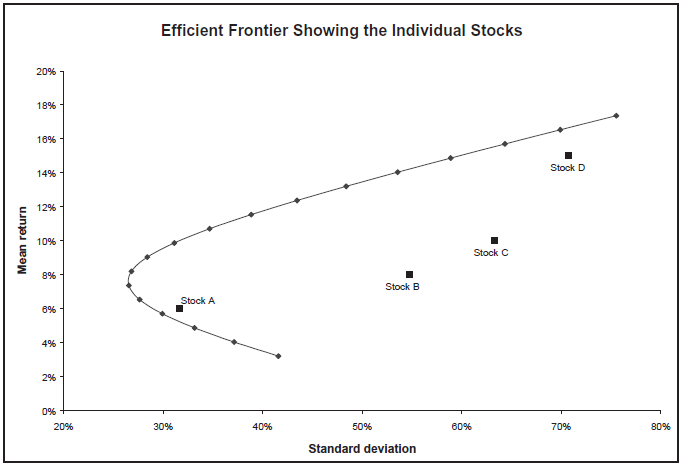

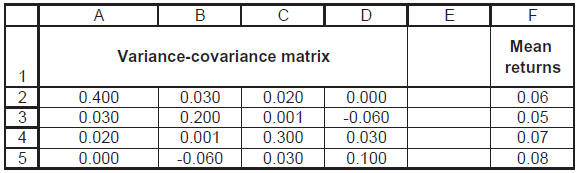

Calculate the envelope set for the four assets below and show that the individual assets all lie within this envelope set. You should get a graph which looks something like the following: B A FOUR-ASSET PORTFOLIO PROBLEM Variance-covariance 0.01 A Mean returns 6% 8% 10% 3 4 5 0.05 0.03 0.06 0.10

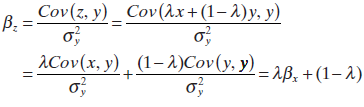

In the example below, use Excel to find an envelope portfolio whose β with respect to the efficient portfolio y is zero. Notice that because the covariance is linear, so is β: Suppose that z = λx + (1 - λ) y is a convex combination of x and y, and that we are trying to find the βz. Then Cov

A sufficient condition to produce positively weighted efficient portfolios is that the variance- covariance matrix be diagonal: That is, that ?ij = 0, for i ? j. By continuity, positively weighted portfolios will result if the off-diagonal elements of the variance covariance matrix are suffi

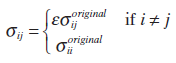

Consider the data below for six furniture companies. a. Given this matrix, and assuming that the risk-free rate is 0%, calculate the efficient portfolio of these six firms. b. Repeat, assuming that the risk-free rate is 10%. c. Use these two portfolios to generate an efficient frontier for the

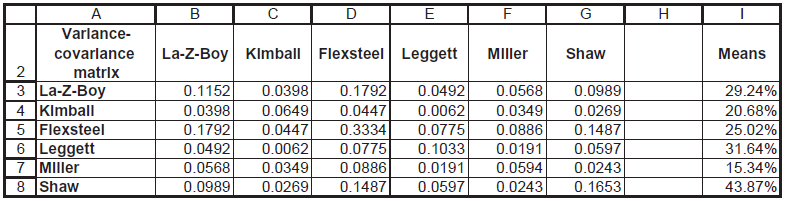

Consider the data below and find the portfolio weights so that the expected return of the portfolio is 14%. What is the corresponding portfolio standard deviation? A B Standard deviation of return 35% Mean return 2 Stock 1 3 Stock 2 4 Covariance(r,r2) 12% 18% 50% 0.08350

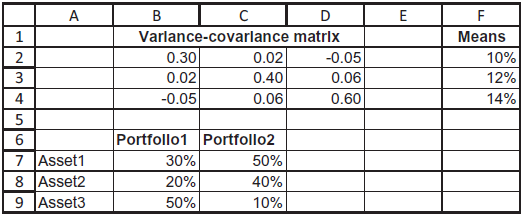

Three assets have the following means and variance-covariance matrix: a. Calculate the statistics?mean, variance, standard deviation, covariance, correlation? for the portfolios. b. Create a chart of the mean and standard deviation of combinations of the portfolios. c. Add the individual asset

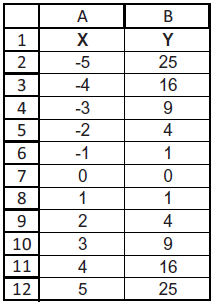

Consider the two random variables X and Y whose values are given below. Note that X and Y are perfectly correlated, though perhaps not linearly correlated. Compute their correlation coefficient. 25 -5 -4 16 3 -3 4 -2 4 -1 2 4 3 9. 10 11 4 16 25 12 567 00

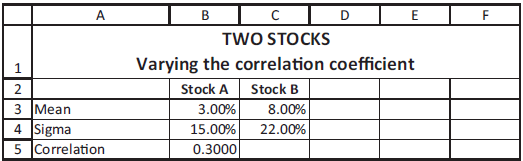

Consider the two stocks below. Graph the frontier of combinations of the two stocks. Show the effect on the frontier of varying the correlation from ? 1 to + 1. в с TWO STOCKS Varying the correlation coefficient Stock B A. Stock A 3.00% 3 Mean 4 Sigma 5 Correlation 8.00% 22.00% 15.00% 0.3000

Hemp Airlines (HA, “we fly high”) is about to buy 5 CFA3000 commuter jets. Each airplane costs $50 million. A friendly bank has put together a consortium to finance the deal. The consortium includes a 20% equity investment and an 80% debt component. The debt has an interest rate of 8% annually,

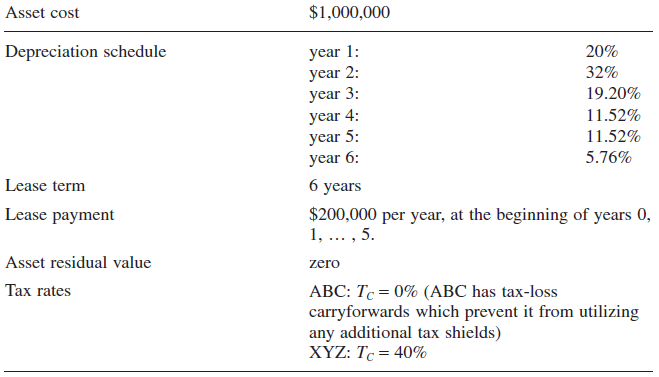

ABC Corp. is considering leasing an asset from XYZ Corp. Here are the relevant facts: ABC?s interest costs are 10% and XYZ ? s interest costs are 7%. Show that it will be advantageous both for ABC to lease the asset and for XYZ to purchase the asset in order to lease it out to ABC. $1,000,000

Your company is considering either purchasing or leasing an asset which costs $1,000,000. The asset, if purchased, will be depreciated on a straight-line basis over 6 years to a zero residual value. A leasing company is willing to lease the asset for $300,000 per year; the first payment on the

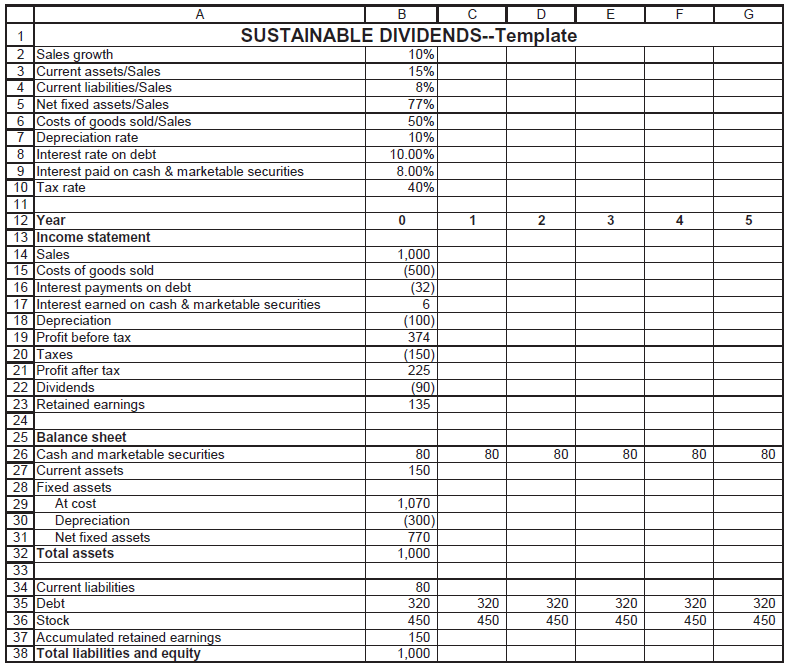

This problem introduces the concept of ?sustainable dividends?: The firm whose financials are illustrated below wishes to maintain cash balances of 80 over the next 5 years. It also desires to issue neither additional stock nor make any changes in its current level of debt. This means that

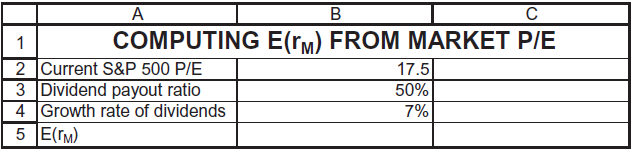

Suppose that the S&P 500 price/earnings ratio is 17.5, the dividend payout ratio of the S&P is 50%, and that you estimate a future growth of dividends of 7%. What is E (rM)? COMPUTING E(rM) FROM MARKET P/E 2 Current S&P 500 P/E 17.5 3 Dividend payout ratio 4 Growth rate of dividends 5

At the end of June 2007, the price/earnings ratio of the S&P 500 was 17.5. Assume that the index proxies for the market, that it has a 50% dividend payout ratio, and that dividends are expected to grow at 7%. Compute E(rM).

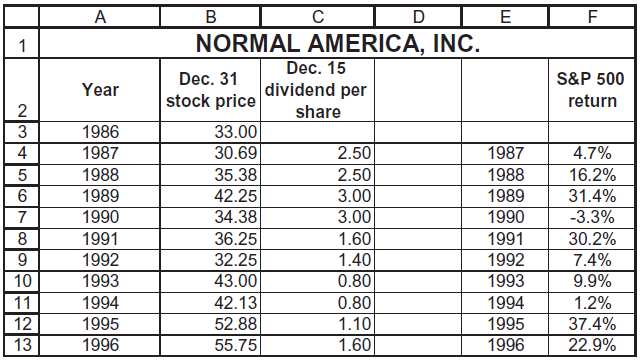

It is 1 January 1997. Normal America, Inc. (NA) has paid a year-end dividend in each of the last 10 years, as shown by the table below: a. Calculate NA?s ? with respect to the S&P 500. b. Suppose that the Treasury bill rate is 5.5% and that the expected return on the market is E(rM) = 13%.

You are considering buying the bonds of a very risky company. A bond with a $100 face value, a 1-year maturity, and a coupon rate of 22% is selling for $95. You consider the probability that the company will actually survive to pay off the bond 80%. With 20% probability, you think that the company

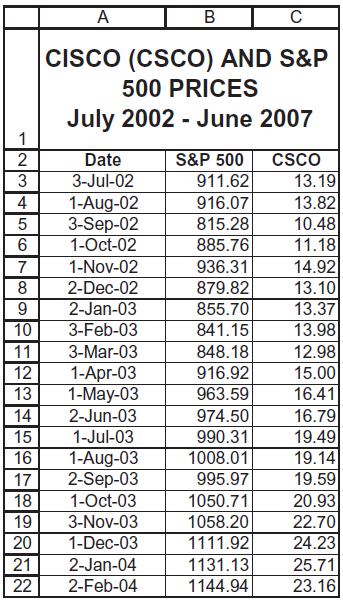

On the spreadsheet with this chapter you will find the following monthly data for Cisco?s stock price and the S&P 500 index. Compute the equation rCSCO, t = ?CSCO + ?CSCO rSP,t and include the R2 and t -statistics for the equation and its coefficients.22 CISCO (CSCO) AND S&P 500 PRICES July

Consider a company which has βequity = 1.5 and βdebt = 0.4. Suppose that the risk-free rate of interest is 6%, the expected return on the market E(rM) = 15%, and that the corporate tax rate is 40%. If the company has 40% equity and 60% debt in its capital structure, calculate its weighted

ABC Corp. has just paid a dividend of $3 per share. You—an experienced analyst—feel quite sure that the growth rate of the company’s dividends over the next 10 years will be 15% per year. After 10 years you think that the company’s dividend growth rate will slow to the industry average,

The current stock price of TransContinentalAirways is $65 per share. TCA currently pays an annual per-share dividend of $3. Over the past 5 years this dividend has grown annually at a rate of 23%. A respected analyst assumes that the current growth rate of dividends will hold up for the next 5

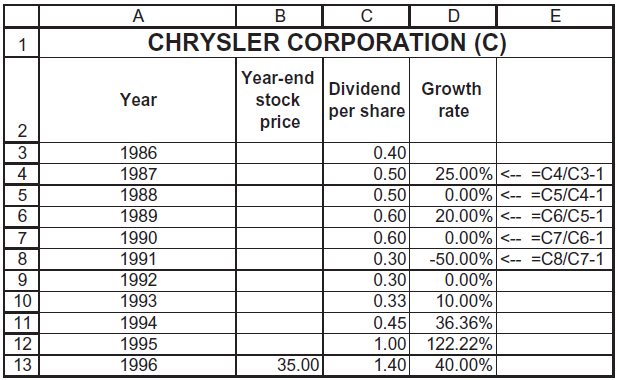

Consider the following dividend and price data for Chrysler: Use the Gordon model to calculate Chrysler ? s cost of equity at end-1996 on the basis of dividends only. в с CHRYSLER CORPORATION (C) D Year-end Dividend Growth stock Year per share rate price 3 1986 0.40 1987 4 0.50 25.00%

Dismal.Com is a producer of depressing Internet products. The company is currently not paying dividends, but its chief financial officer thinks that starting in 3 years it can pay a dividend of $15 per share, and that this dividend will grow by 20% per year. Assuming that the cost of equity of

Unheardof, Inc., has just paid a dividend of $5 per share. This dividend is anticipated to increase at a rate of 15% per year. If the cost of equity for Unheardof is 25%, what should be the market value of a share of the company?

ABC Corp. has a stock price P0 = 50. The firm has just paid a dividend of $3 per share, and intelligent shareholders think that this dividend will grow by a rate of 5% per year. Use the Gordon dividend model to calculate the cost of equity of ABC.

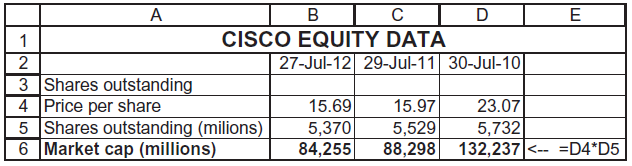

Below are some year-end numbers for Cisco?s equity. Restate the enterprise value in market terms. в с A CISCO EQUITY DATA 27-Jul-12 29-Jul-11 30-Jul-10 2 3 Shares outstanding 4 Price per share 5 Shares outstanding (milions) 6 Market cap (millions) 15.69 15.97 5,529 88,298 132,237

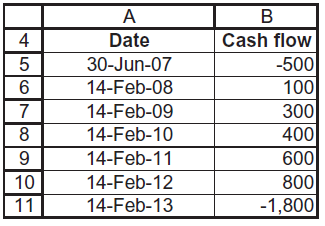

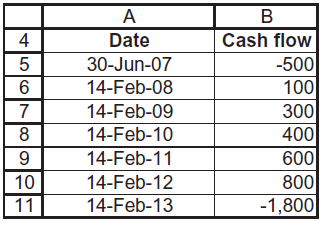

Identify the two internal rates of return of the investment in exercise 16. A Date Cash flow -500 30-Jun-07 14-Feb-08 100 14-Feb-09 300 400 600 800 -1,800 14-Feb-10 14-Feb-11 10 14-Feb-12 11 14-Feb-13

Use XNPV to value the following investment. Assume that the annual discount rate is 15%. A Date Cash flow -500 30-Jun-07 14-Feb-08 100 14-Feb-09 300 400 600 800 -1,800 14-Feb-10 14-Feb-11 10 14-Feb-12 11 14-Feb-13

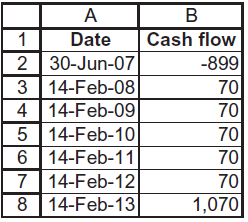

Use XIRR to compute the internal rate of return of the following investment: A Date Cash flow 2 30-Jun-07 3 14-Feb-08 4 14-Feb-09 5 14-Feb-10 6 14-Feb-11 7 14-Feb-12 8 14-Feb-13 -899 70 70 70 70 70 1,070

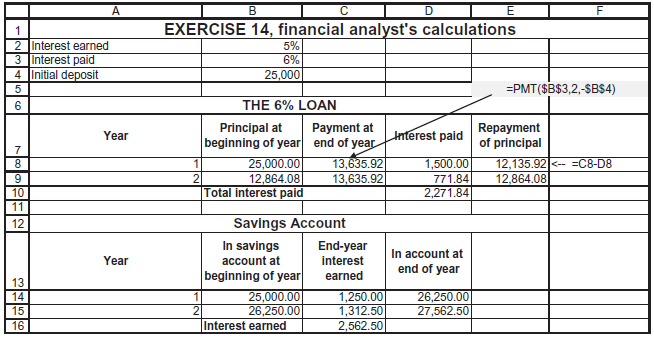

You currently have $25,000 in the bank, in a savings account that draws 5% interest. Your business needs $25,000, and you are considering two options: (a) Use the money in your savings account. (b) Borrow the money from the bank at 6%, leaving the money in the savings account. Your financial

You have just turned 35, and you intend to start saving for your retirement. Once you retire in 30 years (when you turn 65), you would like to have an income of $100,000 per year for the next 20 years. Calculate how much you would have to save between now and age 65 in order to finance your

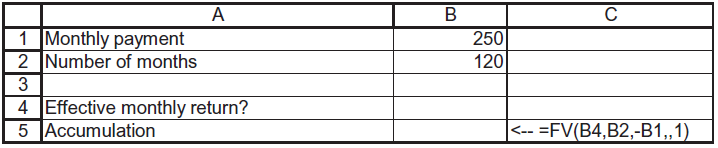

A mutual fund has been advertising that, had you deposited $250 per month in the fund for the last 10 years, you would now have accumulated $85,000. Assuming that these deposits were made at the beginning of each month for a period of 120 months, calculate the effective annual return fund investors

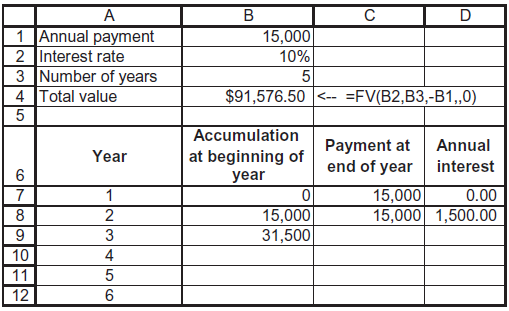

Redo the previous calculation, this time assuming that you make 5 deposits at the beginning of this year and the following 4 years. How much will you accumulate by the end of year 5?

You are considering a savings plan which calls for a deposit of $15,000 at the end of each of the next 5 years. If the plan offers an interest rate of 10%, how much will you accumulate at the end of year 5? Do this calculation by completing the following spreadsheet. This spreadsheet does the

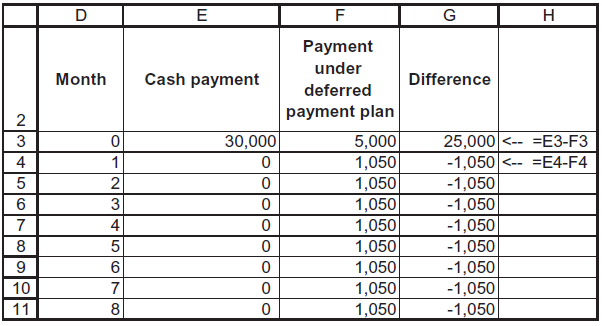

You are considering buying a car from a local auto dealer. The dealer offers you one of two payment options: ? You can pay $30,000 cash. ? The ?deferred payment plan?: You can pay the dealer $5,000 cash today and a payment of $1,050 at the end of each of the next 30 months.? As an alternative to

You have just taken a car loan of $15,000. The loan is for 48 months at an annual interest rate of 15% (which the bank translates to a monthly rate of 15%/12 = 1.25%). The 48 payments (to be made at the end of each of the next 48 months) are all equal.a. Calculate the monthly payment on the loan.b.

Calculate the flat annual payment required to pay off a 13%, 5-year loan of $100,000.

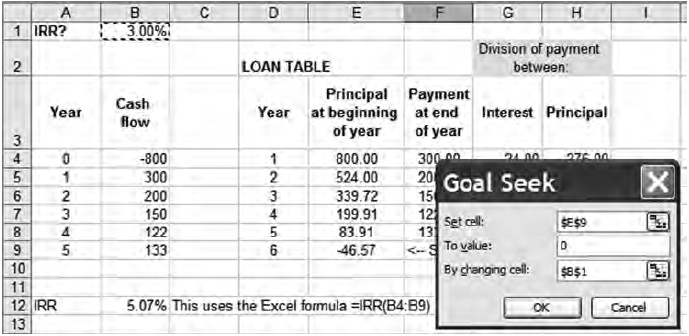

An alternative definition of the IRR is the rate which makes the principal at the beginning of year 6 equal to zero. 9 This is shown in the printout above, in which cell E9 gives the principal at the beginning of year 6. Using the Goal Seek function of Excel, find this rate (below we illustrate how

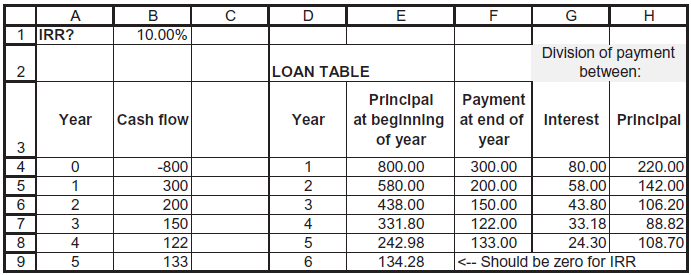

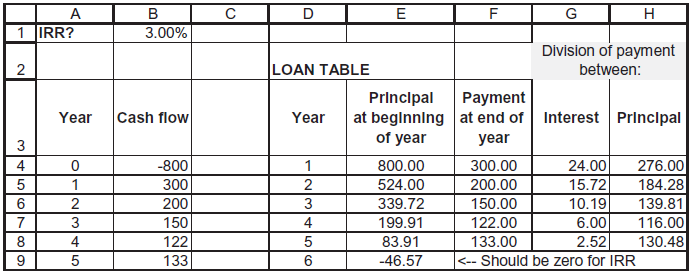

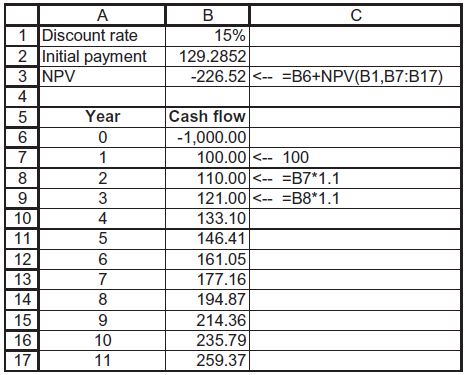

In this exercise we solve iteratively for the internal rate of return. Consider an investment which costs 800 and has cash flows of 300, 200, 150, 122, 133 in years 1?5. Setting up the loan table below shows that 10% is greater than the IRR (since the return of principal at the end of year 5 is

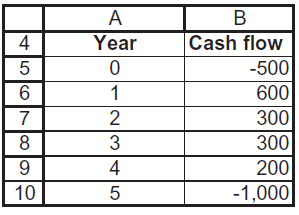

The following cash-flow pattern has two IRRs. Use Excel to draw a graph of the NPV of these cash flows as a function of the discount rate. Then use the IRR function to identify the two IRRs. Would you invest in this project if the opportunity cost were 20%? B Year Cash flow 4 -500 600 300 300 8 3

You are offered an investment with the following conditions: ? The cost of the investment is 1,000. ? The investment pays out a sum X at the end of the first year; this payout grows at the rate of 10% per year for 11 years. If your discount rate is 15%, calculate the smallest X which would entice

You just took a $10,000, 5-year loan. Payments at the end of each year are flat (equal in every year) at an interest rate of 15%. Calculate the appropriate loan table, showing the breakdown in each year between principal and interest.

You are offered an asset costing $600 that has cash flows of $100 at the end of each of the next 10 years.a. If the appropriate discount rate for the asset is 8%, should you purchase it?b. What is the IRR of the asset?

Showing 800 - 900

of 888

1

2

3

4

5

6

7

8

9

Step by Step Answers