New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

intermediate accounting volume 2

Intermediate Accounting 2007 FASB Update Volume 2 12th Edition Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield - Solutions

(Lessee-Lessor Entries, Balance Sheet Presentation; Sales-Type Lease) Cascade Industries and Hardy Inc. enter into an agreement that requires Hardy Inc. to build three diesel-electric engines to Cascade’s specifications. Upon completion of the engines, Cascade has agreed to lease them for a

(Balance Sheet and Income Statement Disclosure—Lessee) The following facts pertain to a noncancelable lease agreement between Alschuler Leasing Company and McKee Electronics, a lessee, for a computer system.The collectibility of the lease payments is reasonably predictable, and there are no

(Balance Sheet and Income Statement Disclosure—Lessor) Assume the same information as in P21-4.Instructions (Round all numbers to the nearest cent.)(a) Assuming the lessor’s accounting period ends on September 30, answer the following questions with respect to this lease agreement.(1) What

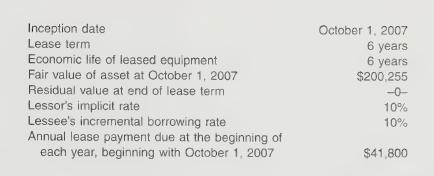

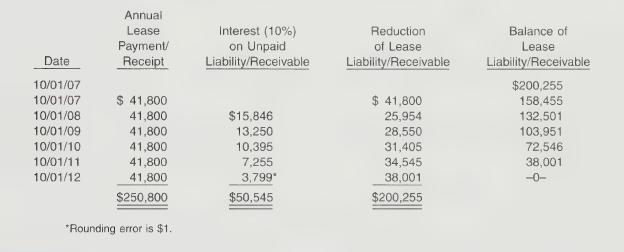

(Lessee Entries with Residual Value) The following facts pertain to a noncancelable lease agreement between Voris Leasing Company and Zarle Company, a lessee.The lessee assumes responsibility for all executory costs, which are expected to amount to $4,000 per year.The asset will revert to the

(Lessee Entries and Balance Sheet Presentation; Capital Lease) Brennan Steel Company as les-9) see signed a lease agreement for equipment for 5 years, beginning December 31, 2007. Annual rental payments of $32,000 are to be made at the beginning of each lease year (December 31). The taxes,

(Lessee Entries and Balance Sheet Presentation; Capital Lease) On January 1, 2008, Charlie Doss Company contracts to lease equipment for 5 years, agreeing to make a payment of $94,732 (including the executory costs of $6,000) at the beginning of each year, starting January 1, 2008. The taxes, the

(Lessee Entries, Capital Lease with Monthly Payments) John Roesch Inc. was incorporated in 2006 to operate as a computer software service firm with an accounting fiscal year ending August 31._ Roesch’s primary product is a sophisticated online inventory-control system; its customers pay a fixed

(Lessor Computations and Entries; Sales-Type Lease with Unguaranteed RV) Hanson Company manufactures a computer with an estimated economic life of 12 years and leases it to Flypaper Airlines for a period of 10 years. The normal selling price of the equipment is $210,482, and its unguaranteed

(Lessee Computations and Entries; Capital Lease with Unguaranteed Residual Value) Assume the same data as in P21-10 with Flypaper Airlines Co. having an incremental borrowing rate of 10%.Instructions(Round all numbers to the nearest dollar.)(a) Discuss the nature of this lease in relation to the

(Basic Lessee Accounting with Difficult PV Calculation) In 2005 Judy Yin Trucking Company negotiated and closed a long-term lease contract for newly constructed truck terminals and freight storage facilities. The buildings were erected to the company’s specifications on land owned by the

(Lessor Computations and Entries; Sales-Type Lease with Guaranteed Residual Value) Laura Jennings Inc. manufactures an X-ray machine with an estimated life of 12 years and leases it to Craig Gocker Medical Center for a period of 10 years. The normal selling price of the machine is $343,734, and its

(Lessee Computations and Entries; Capital Lease with Guaranteed Residual Value) Assume the same data as in P21-13 and that Craig Gocker Medical Center has an incremental borrowing rate of 10%.Instructions(Round all numbers to the nearest dollar.)(a) Discuss the nature of this lease in relation to

(Operating Lease vs. Capital Lease) You are auditing the December 31, 2006, financial statements of Sarah Shamess, Inc., manufacturer of novelties and party favors. During your inspection of the company garage, you discovered that a 2005 Shirk automobile not listed in the equipment subsidiary

(Lessee-Lessor Accounting for Residual Values) Lanier Dairy leases its milking equipment from Zeff Finance Company under the following lease terms.1. The lease term is 10 years, noncancelable, and requires equal rental payments of $25,250 due at the beginning of each year starting January 1,

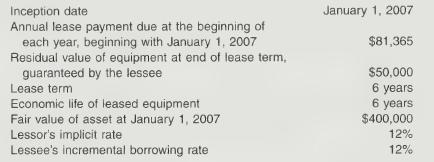

(Lessee Accounting and Reporting) On January 1, 2008, Hayes Company entered into a noncancelable lease for a machine to be used in its manufacturing operations. The lease transfers ownership of the machine to Hayes by the end of the lease term. The term of the lease is 8 years. The minimum lease

(Lessor and Lessee Accounting and Disclosure) Laurie Gocker Inc. entered into a noncancelable lease arrangement with Nathan Morgan Leasing Corporation for a certain machine. Morgan’s primary business is leasing; it is not a manufacturer or dealer. Gocker will lease the machine for a period of 3

(Lessee Capitalization Criteria) On January 1, Shinault Company, a lessee, entered into three noncancelable leases for brand-new equipment, Lease L, Lease M, and Lease N. None of the three leases transfers ownership of the equipment to Shinault at the end of the lease term. For each of the three

(Comparison of Different Types of Accounting by Lessee and Lessor)Part 1 Capital leases and operating leases are the two classifications of leases described in FASB pronouncements from the standpoint of the lessee.Instructions(a) Describe how a capital lease would be accounted for by the lessee

(Lessee Capitalization of Bargain Purchase Option) Brad Hayes Corporation is a diversified company with nationwide interests in commercial real estate developments, banking, copper mining, and metal fabrication. The company has offices and operating locations in major cities throughout the United

(Lease Capitalization, Bargain Purchase Option) Cubby Corporation entered into a lease agreement for 10 photocopy machines for its corporate headquarters. The lease agreement qualifies as an operating lease in all terms except there is a bargain purchase option. After the 5-year lease term, the

(Sale-Leaseback) On January 1, 2007, Laura Dwyer Company sold equipment for cash and leased it back. As seller-lessee, Laura Dwyer retained the right to substantially all of the remaining use of the equipment. The term of the lease is 8 years. There is a gain on the sale portion of the transaction.

(Sale-Leaseback) On December 31, 2007, Laura Truttman Co. sold 6-month old equipment at fair value and leased it back. There was a loss on the sale. Laura Truttman pays all insurance, maintenance, and taxes on the equipment. The lease provides for eight equal annual payments, beginning December 31,

How should consolidated financial statements be re- ported this year when statements of individual compa- nies were presented last year?

Karen Beers controlled four domestic subsidiaries and one foreign subsidiary. Prior to the current year, Beers had excluded the foreign subsidiary from consolidation. During the current year, the foreign subsidiary was in- cluded in the financial statements. How should this change in accounting

Prior to 2008, Mary Boudreau Inc. excluded manufac- turing overhead costs from work in process and finished goods inventory. These costs have been expensed as incurred. In 2008, the company decided to change its accounting methods for manufacturing inventories to full costing by including these

Lou Brady Corp. failed to record accrued salaries for 2005, $2,000; 2006, $2,100; and 2007, $3,900. What is the amount of the overstatement or understatement of Re- tained Earnings at December 31, 2008?

In January 2007, installation costs of $8,000 on new ma- chinery were charged to Repair Expense. Other costs of this machinery of $30,000 were correctly recorded and have been depreciated using the straight-line method with an estimated life of 10 years and no salvage value. At December 31, 2008,

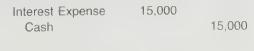

On January 2, 2007, $100,000 of 11%, 20-year bonds were issued for $97,000. The $3,000 discount was charged to Interest Expense. The bookkeeper, John Castle, records interest only on the interest payment dates of January 1 and July 1. What is the effect on reported net income for 2007 of this

An account payable of $13,000 for merchandise pur- chased on December 23, 2007, was recorded in January 2008. This merchandise was not included in inventory at December 31, 2007. What effect does this error have on reported net income for 2007? What entry should be made to correct for this error,

Equipment was purchased on January 2, 2007, for $18,000, but no portion of the cost has been charged to deprecia- tion. The corporation wishes to use the straight-line method for these assets, which have been estimated to have a life of 10 years and no salvage value. What effect does this error

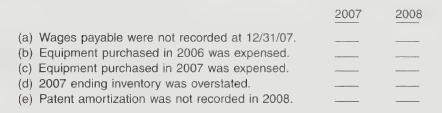

Indicate the effect-Understate, Overstate, No Effect-that each of the following errors has on 2007 net income and 2008 net income. (a) Wages payable were not recorded at 12/31/07 (b) Equipment purchased in 2006 was expensed. (c) Equipment purchased in 2007 was expensed. (d) 2007 ending inventory

Charlene Rydell Manufacturing Co. is preparing its year-end financial statements and is consid- ering the accounting for the following items. 1. The vice president of sales had indicated that one product line has lost its customer appeal and will be phased out over the next 3 years. Therefore, a

Pociek Co. is evaluating the appropriate accounting for the following items. 1. When the year-end physical inventory adjustment was made for the current year, the controller discovered that the prior year's physical inventory sheets for an entire warehouse were mislaid and excluded from last year's

Robocop Corporation owns stock of Terminator, Inc. Prior to 2008, the investment was accounted for using the equity method. In early 2008, Robocop sold part of its investment in Terminator, and began using the fair value method. In 2008, Terminator earned net income of $80,000 and paid dividends of

Rocket Corporation has owned stock of Knight Corporation since 2001. At December 31, 2007, its balances related to this investment were:On January 1, 2008, Rocket purchased additional stock of Knight Company for $445,000 and now has significant influence over Knight. If the equity method had been

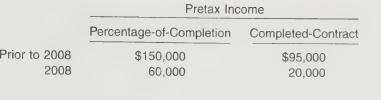

(Change in Principle—Long-term Contracts) Pam Erickson Construction Company changed from the completed-contract to the percentage-of-completion method of accounting for long-term construction contracts during 2008. For tax purposes, the company employs the completed-contract method and will

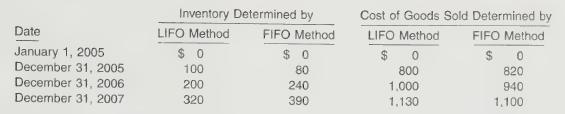

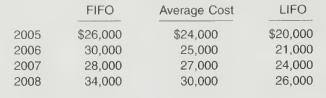

(Change in Principle—Inventory Methods) Holder-Webb Company began operations on January 1, 2005, and uses the average cost method of pricing inventory. Management is contemplating a change in inventory methods for 2008. The following information is available for the years 2005-2007.Instructions

(Accounting Change) Taveras Co. decides at the beginning of 2007 to adopt the FIFO method of inventory valuation. Taveras had used the LIFO method for financial reporting since its inception on January 1, 2005, and had maintained records adequate to apply the FIFO method retrospectively. Taveras

(Accounting Change) Gordon Company started operations on January 1, 2002, and has used the FIFO method of inventory valuation since its inception. In 2008, it decides to switch to the average cost method. You are provided with the following information.Instructions (a) What is the beginning

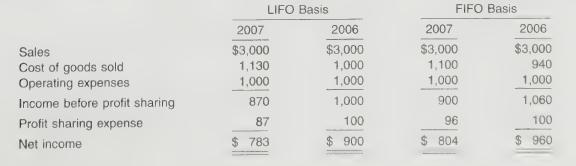

(Accounting Change) Presented below are income statements prepared on a LIFO and FIFO ba- sis for Kenseth Company, which started operations on January 1, 2006. The company presently uses the LIFO method of pricing its inventory and has decided to switch to the FIFO method in 2007. The FIFO income

(Accounting Changes—Depreciation) Kathleen Cole Inc. acquired the following assets in January of 2005.The equipment has been depreciated using the sum-of-the-years’-digits method for the first 3 years for financial reporting purposes. In 2008, the company decided to change the method of

(Change in Estimate and Error; Financial Statements) Presented below are the comparative income statements for Denise Habbe Inc. for the years 2007 and 2008.The following additional information is provided:1. In 2008, Denise Habbe Inc. decided to switch its depreciation method from

(Accounting for Accounting Changes and Errors) Listed below are various types of accounting changes and errors.1. Change in a plant asset’s salvage value.2. Change due to overstatement of inventory.3. Change from sum-of-the-years’-digits to straight-line method of depreciation.4. Change from

(Error and Change in Estimate—Depreciation) Joy Cunningham Co. purchased a machine on January 1, 2005, for $550,000. At that time it was estimated that the machine would have a 10-year life and no salvage value. On December 31, 2008, the firm’s accountant found that the entry for depreciation

(Depreciation Changes) On January 1, 2004, Jackson Company purchased a building and equipment that have the following useful lives, salvage values, and costs.Building, 40-year estimated useful life, $50,000 salvage value, $800,000 cost Equipment, 12-year estimated useful life, $10,000 salvage

(Change in Estimate—Depreciation) Peter M. Dell Co. purchased equipment for $510,000 which was estimated to have a useful life of 10 years with a salvage value of $10,000 at the end of that time. Depreciation has been entered for 7 years on a straight-line basis. In 2008, it is determined that

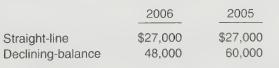

(Change in Estimate—Depreciation) Gerald Englehart Industries changed from the doubledeclining balance to the straight-line method in 2008 on all its plant assets. There was no change in the assets’ salvage values or useful lives. Plant assets, acquired on January 2, 2005, had an original cost

(Change in Principle—Long-term Contracts) Cullen Construction Company changed from the completed-contract to the percentage-of-completion method of accounting for long-term construction contracts during 2008. For tax purposes, the company employs the completed-contract method and will continue

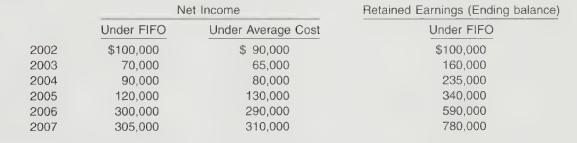

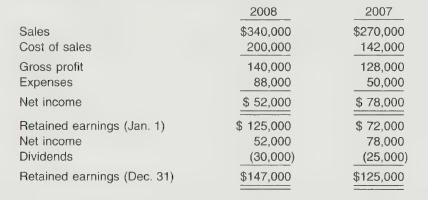

(Various Changes in Principle—Inventory Methods) Below is the net income of Anita Ferreri Instrument Co., a private corporation, computed under the three inventory methods using a periodic system.Instructions (Ignore tax considerations.)(a) Assume that in 2008 Ferreri decided to change from the

(Error Correction Entries) The first audit of the books of Bruce Gingrich Company was made for the year ended December 31, 2008. In examining the books, the auditor found that certain items had been overlooked or incorrectly handled in the last 3 years. These items are:1. At the beginning of 2006,

(Error Analysis and Correcting Entry) You have been engaged to review the financial statements of Gottschalk Corporation. In the course of your examination you conclude that the bookkeeper hired during the current year is not doing a good job. You notice a number of irregularities as follows.1.

_ (Error Analysis and Correcting Entry) The reported net incomes for the first 2 years of Sandra Gustafson Products, Inc., were as follows: 2007, $147,000; 2008, $185,000. Early in 2009, the following errors were discovered.1. Depreciation of equipment for 2007 was overstated $17,000.2.

(Error Analysis) Peter Henning Tool Company's December 31 year-end financial statements contained the following errors.An insurance premium of $66,000 was prepaid in 2007 covering the years 2007, 2008, and 2009. The entire amount was charged to expense in 2007. In addition, on December 31, 2008,

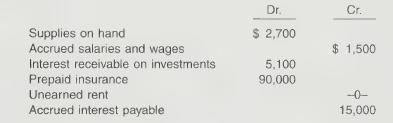

(Error Analysis; Correcting Entries) A partial trial balance of Julie Hartsack Corporation is as follows on December 31, 2008.Additional adjusting data:1. A physical count of supplies on hand on December 31, 2008, totaled $1,100.2. Through oversight, the Accrued Salaries and Wages account was not

(Error Analysis) The before-tax income for Lonnie Holdiman Co. for 2007 was $101,000 and $77,400 for 2008. However, the accountant noted that the following errors had been made: 1. Sales for 2007 included amounts of $38,200 which had been received in cash during 2007, but for which the related

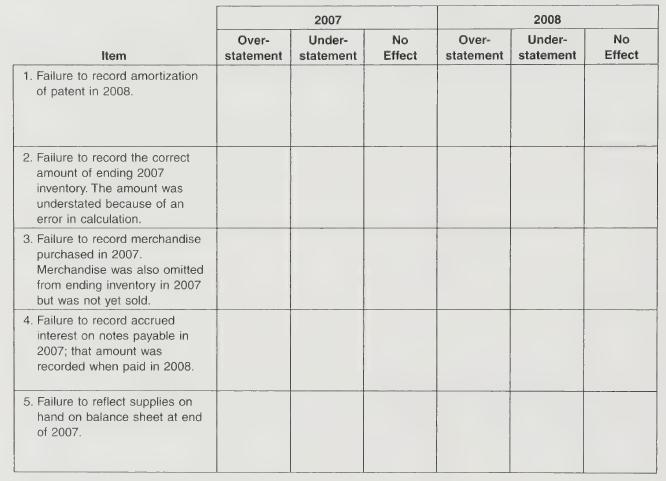

(Error Analysis) When the records of Debra Hanson Corporation were reviewed at the close of 2008, the errors listed below were discovered. For each item indicate by a check mark in the appropriate column whether the error resulted in an overstatement, an understatement, or had no effect on net

(Change from Fair Value to Equity) On January 1, 2007, Barbra Streisand Co. purchased 25,000 shares (a 10% interest) in Elton John Corp. for $1,400,000. At the time, the book value and the fair value of John’s net assets were $13,000,000.On July 1, 2008, Streisand paid $3,040,000 for 50,000

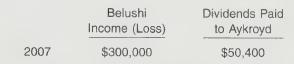

(Change from Equit. y to Fair. Value) Dan Aykroyd Corp. was a 30% owner of John Belushi Company, holding 210,000 shares of Belushi’s common stock on December 31, 2006. The investment account had the following entries.On January 2, 2007, Aykroyd sold 126,000 shares of Belushi for $3,440,000,

(Change in Estimate and Error Correction) Brueggen Company is in the process of preparing its financial statements for 2007. Assume that no entries for depreciation have been recorded in 2007. The following information related to depreciation of fixed assets is provided to you:1. Brueggen purchased

(Comprehensive Accounting Change and Error Analysis Problem) Larry Kingston Inc. was organized in late 2005 to manufacture and sell hosiery. At the end of its fourth year of operation, the company has been fairly successful, as indicated by the following reported net incomes.The company has decided

(Error Corrections and Accounting Changes) Patricia Voga Company is in the process of adjusting and correcting its books at the end of 2008. In reviewing its records, the following information is compiled.1. Voga has failed to accrue sales commissions payable at the end of each of the last 2 years,

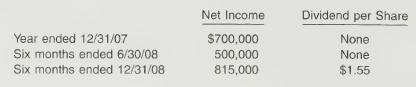

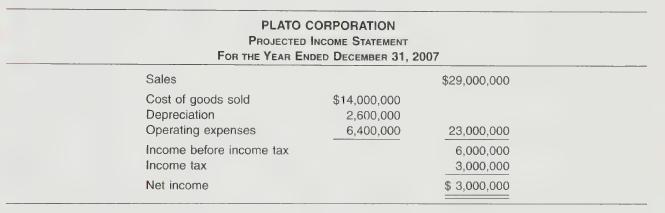

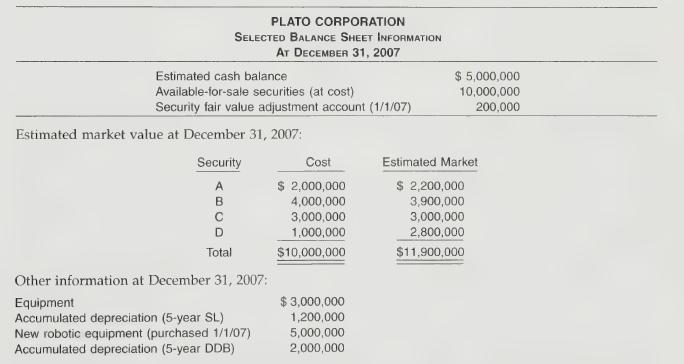

(Accounting Changes) Plato Corporation performs year-end planning in November of each year before their calendar year ends in December. The preliminary estimated net income is $3 million. The CFO, Mary Sheets, meets with the company president, S. A. Plato, to review the projected numbers. She

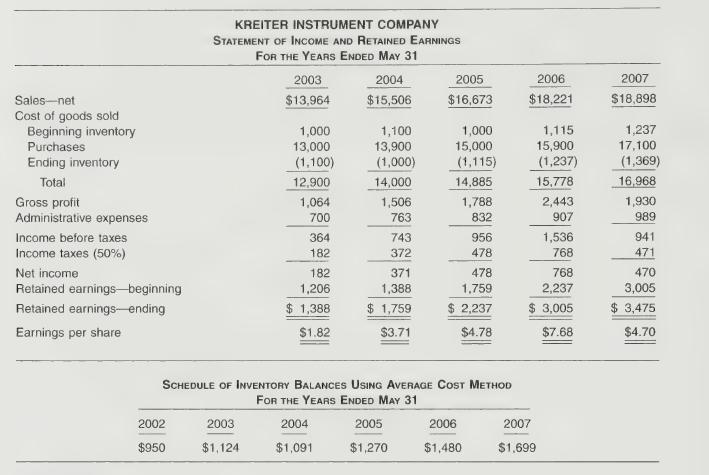

(Change in Principle—LIFO to Average Cost; Income Statements—Periodic) The management of Kreiter Instrument Company had concluded, with the concurrence of its independent auditors, that results of operations would be more fairly presented if Kreiter changed its method of pricing inventory from

(Accounting Change and Error Analysis) On December 31, 2008, before the books were closed, the management and accountants of Keltner Inc. made the following determinations about three depreciable assets.1. Depreciable asset A was purchased January 2, 2005. It originally cost $495,000 and, for

(Error Corrections) You have been assigned to examine the financial statements of Vickie L. Lemke Company for the year ended December 31, 2008. You discover the following situations. 1. Depreciation of $3,200 for 2008 on delivery vehicles was not recorded. 2. The physical inventory count on

(Comprehensive Error Analysis) On March 5, 2008, you were hired by Gretchen Hollenbeck Inc., a closely held company, as a staff member of its newly created internal auditing department. While reviewing the company's records for 2007 and 2008, you discover that no adjustments have yet been made for

(Error Analysis) Mary Keeton Corporation has used the accrual basis of accounting for several years. A review of the records, however, indicates that some expenses and revenues have been handled on a cash basis because of errors made by an inexperienced bookkeeper. Income statements prepared by the

(Error Analysis and Correcting Entries) You have been asked by a client to review the records of Larry Landers Company, a small manufacturer of precision tools and machines. Your client is interested in buying the business, and arrangements have been made for you to review the accounting

(Fair Value to Equity Method with Goodwill) On January 1, 2006, Latoya Inc. paid $700,000 for 10,000 shares of Jones Company’s voting common stock, which was a 10% interest in Jones. At that date the net assets of Jones totaled $6,000,000. The fair values of all of Jones’ identifiable assets

(Change from Fair Value to Equity Method) On January 3, 2005, Calvin Company purchased for $500,000 cash a 10% interest in Hobbes Corp. On that date the net assets of Hobbes had a book value of $3,750,000. The excess of cost over the underlying equity in net assets is attributable to undervalued

(Analysis of Various Accounting Changes and Errors) Erin Kramer Inc. has recently hired a e new independent auditor, Jodie Larson, who says she wants “to get everything straightened out.” Consequently, she has proposed the following accounting changes in connection with Erin Kramer Inc.’s

(Analysis of Three Accounting Changes and Errors) Listed below are three independent, unrelated sets of facts relating to accounting changes.Situation 1 Penelope Millhouse Company is in the process of having its first audit. The company has used the cash basis of accounting for revenue recognition.

(Analysis of Various Accounting Changes and Errors) Mischelle Reiners, controller of Lisa Terry Corp., is aware that a standard on accounting changes has been issued. After reading the standard, she is confused about what action should be taken on the following items related to Terry Corp. for the

(Change in Principle, Estimate) As a certified public accountant, you have been contacted by Ben Thinken, CEO of Sports-Pro Athletics, Inc., a manufacturer of a variety of athletic equipment. He has asked you how to account for the following changes.1. Sports-Pro appropriately changed its

(Change in Estimates) Andy Frain is an audit senior of a large public accounting firm who has just been assigned to the Usher Corporation’s annual audit engagement. Usher has been a client of Frain’s firm for many years. Usher is a fast-growing business in the commercial construction industry.

The Coca-Cola Company and PepsiCo, Inc.Instructions Go to the KWW website and use information found there to answer the following questions related to The Coca-Cola Company and PepsiCo Inc.(a) Identify the changes in accounting principles reported by Coca-Cola during the 3 years covered by its

Instructions .Use an appropriate source to identify two firms that recently reported a voluntary change in accounting principle. Answer the following questions with regard to each of the companies.(a) What is the name of the company? What source did you use to identify the company?(b) How did the

The May 7, 2002 edition of the Wall Street Journal includes an article by James Bandler and Mark Maremont entitled “KPMG’s Work With Xerox Sets Up a New Test for SEC.”Instructions Read the article and answer the following questions.(a) Achange in estimated residual value is usually reported

At the end of the current period, Jacob Inc. had a pro- jected benefit obligation of $400,000 and pension plan assets (at fair value) of $300,000. What are the accounts and amounts that will be reported on the company's balance sheet as pension assets or pension liabilities?

At the end of the current year, Joshua Co. has prior ser- vice cost of $9,150,000. Where should the prior service cost be reported on the balance sheet?

Why didn't the FASB cover both types of postretirement benefits-pensions and healthcare-in the earlier pen- sion accounting statement?

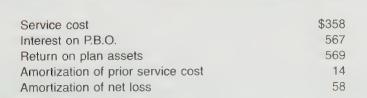

AMR Corporation (parent company of American Airlines) reported the following for 2004 (in millions).Compute AMR Corporation’s 2004 pension expense. Service cost Interest on P.B.O. $358 567 Return on plan assets Amortization of prior service cost Amortization of net loss 569 14 58

At January 1, 2011, Uddin Company had plan assets of $250,000 and a projected benefit obliga- tion of the same amount. During 2011, service cost was $27,500, the settlement rate was 10%, actual and expected return on plan assets were $25,000, contributions were $20,000, and benefits paid were

For 2004, Campbell Soup Company had pension expense of $43 million and contributed $65 million to the pension fund. Prepare Campbell Soup Company's journal entry to record pension expense and funding.

Duesbury Corporation amended its pension plan on January 1, 2011, and granted $120,000 of prior service costs to its employees. The employees are expected to provide 2,000 service years in the fu- ture, with 350 service years in 2011. Compute prior service cost amortization for 2011.

At December 31, 2011, Conway Corporation had a projected benefit obligation of $510,000, plan assets of $322,000, and prior service cost of $127,000 in accumulated other comprehensive income. Determine the pension asset/liability at December 31, 2011.

Hunt Corporation had a projected benefit obligation of $3,100,000 and plan assets of $3,300,000 at January 1, 2011. Hunt also had a net actuarial loss of $475,000 in accumulated OCI at January 1, 2011. The average remaining service period of Hunt's employees is 7.5 years. Compute Hunt's minimum

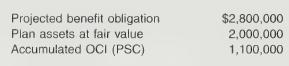

Judy O'Neill Corporation has the following balances at December 31, 2010.How should these balances be reported on O’Neill’s balance sheet at December 31, 2010? Projected benefit obligation Plan assets at fair value Accumulated OCI (PSC) $2,800,000 2,000,000 1,100,000

DeMent Co. had the following amounts related to its pension plan in 2009.Determine for 2009: (a) DeMent’s other comprehensive income, and (b) comprehensive income. Net income for 2009 is $26,000; no amortization of gain or loss is necessary in 2009. Actuarial liability loss for 2009 Unexpected

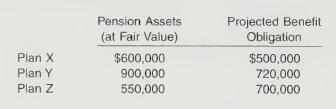

Depp Corp. has three defined-benefit pension plans as follows.How will Depp report these multiple plans in its financial statements? Pension Assets. (at Fair Value) $600,000 900,000 Projected Benefit Obligation $500,000 Plan X Plan Y 720,000 Plan Z 550,000 700,000

Caleb Corporation has the following information available concerning its postretirement ben- efit plan fbr 2011.Compute Caleb’s 2011 postretirement expense. Service cost Interest cost Actual and expected return on plan assets $40,000 52,400 26,900

For 2011, Benjamin Inc. computed its annual postretirement expense as $240,900. Benjamin’s contribution to the plan during 2011 was $160,000. Prepare Benjamin’s 2011 entry to record postretirement expense.

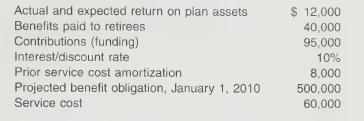

(Pension Expense, Journal Entries) The following information is available for the pension plan of Kiley Company for the year 2010.Instructions (a) Compute pension expense for the year 2010.(b) Prepare the journal entry to record pension expense and the employer’s contribution to the pension plan

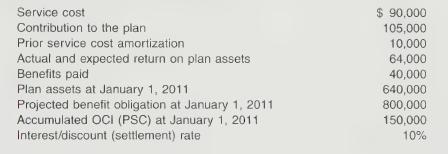

(Computation of Pension Expense) Rebekah Company provides the following information about its defined benefit pension plan for the year 2011.Instructions Compute the pension expense for the year 2011. Service cost Contribution to the plan Prior service cost amortization Actual and expected return

(Preparation of Pension Worksheet) Using the information in E20-2 prepare a pension worksheet inserting January 1, 2011, balances, showing December 31, 2011, balances, and the journal entry recording pension expense.

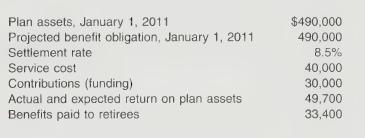

(Basic Pension Worksheet) The following facts apply to the pension plan of Trudy Borke Inc.for the year 2011.Instructions Using the preceding data, compute pension expense for the year 2011. As part of your solution, prepare a pension worksheet that shows the journal entry for pension expense for

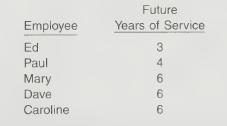

(Application of Years-of-Service Method) Valente Company has five employees participating in its defined benefit pension plan. Expected years of future service for these employees at the beginning of 2011 are as follows.On January 1, 2011, the company amended its pension plan increasing its

(Computation of Actual Return) James Paul Importers provides the following pension plan information.Instructions From the data above, compute the actual return on the plan assets for 2011. Fair value of pension plan assets, January 1, 2011 $2,300,000 Fair value of pension plan assets, December 31,

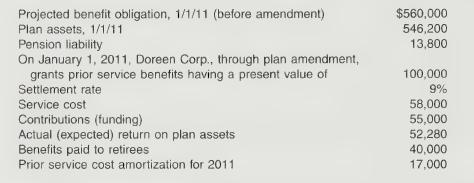

(Basic Pension Worksheet) The following defined pension data of Doreen Corp. apply to the 6) year 2011.Instructions For 2011, prepare a pension worksheet for Doreen Corp. that shows the journal entry for pension expense and the year-end balances in the related pension accounts. Projected benefit

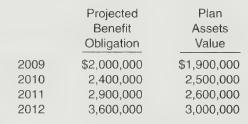

(Application of the Corridor Approach) Dougherty Corp. has beginning-of-the-year present values for its projected benefit obligation and market-related values for its pension plan assets.The average remaining service life per employee in 2009 and 2010 is 10 years and in 2011 and 2012 is 12 years.

Showing 100 - 200

of 2378

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers