New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

intermediate accounting volume 2

Intermediate Accounting 2007 FASB Update Volume 2 12th Edition Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield - Solutions

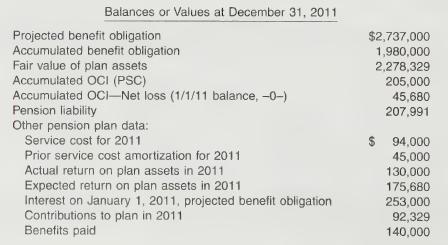

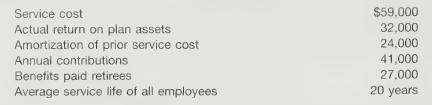

(Disclosures: Pension Expense and Other Comprehensive Income) Mildred Enterprises provides the following information relative to its defined benefit pension plan.Instructions (a) Prepare the note disclosing the components of pension expense for the year 2011.(b) Determine the amounts of other

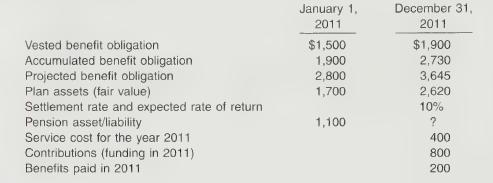

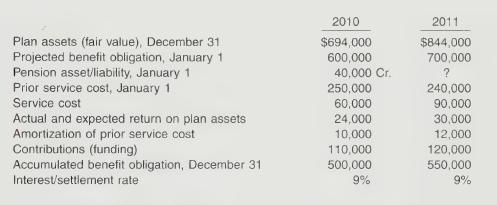

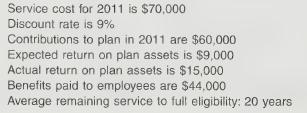

(Pension Worksheet) Buhl Corp. sponsors a defined benefit pension plan for its employees. On January 1, 2011, the following balances relate to this plan.As a result of the operation of the plan during 2011, the following additional data are provided by the actuary.Instructions (a) Using the data

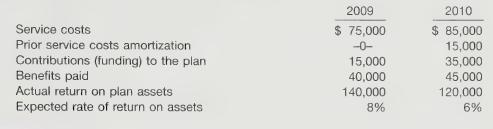

(Pension Expense, Journal Entries, Statement Presentation) Griseta Company sponsors a defined benefit pension plan for its employees. The following data relate to the operation of the plan for the year 2010 in which no benefits were paid.1. The actuarial present value of future benefits earned by

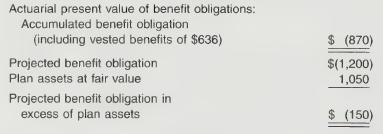

(Pension Expense, Journal Entries, Statement Presentation) Nellie Altom Company received the following selected information from its pension plan trustee concerning the operation of the company’s defined benefit pension plan for the year ended December 31, 2010.The service cost component of

. (Computation of Actual Return, Gains and Losses, Corridor Test, and Pension Expense) Linda Berstler Company sponsors a defined benefit pension plan. The corporation’s actuary provides the following information about the plan.Instructions (a) Compute the actual return on the plan assets in

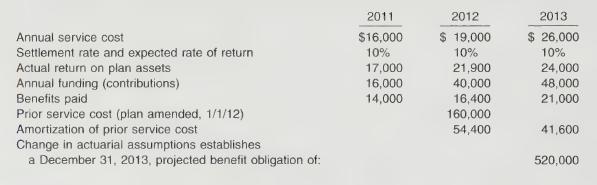

(Worksheet for E20-13) Using the information in E20-13 about Linda Berstler Company’s defined benefit pension plan, prepare a 2011 pension worksheet with supplementary schedules of computations.Prepare the journal entries at December 31, 2011, to record pension expense and related pension

(Pension Expense, Journal Entries) Walker Company provides the following selected information related to its defined benefit pension plan for 2010.Instructions (a) Compute pension expense and prepare the journal entry to record pension expense and the employer’s contribution to the pension plan

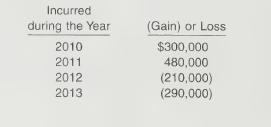

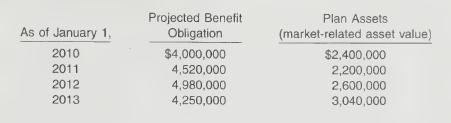

(Amortization of Accumulated OCI (G/L), Corridor Approach, Pension Expense Computation)The actuary for the pension plan of Joyce Bush Inc. calculated the following net gains and losses.Other information about the company’s pension obligation and plan assets is as follows.Joyce Bush Inc. has a

. (Amortization of Accumulated OCI Balances) Lowell Company sponsors a defined benefit pension plan for its 600 employees. The company’s actuary provided the following information about the plan.The average remaining service life per employee is 10.5 years. The service cost component of net

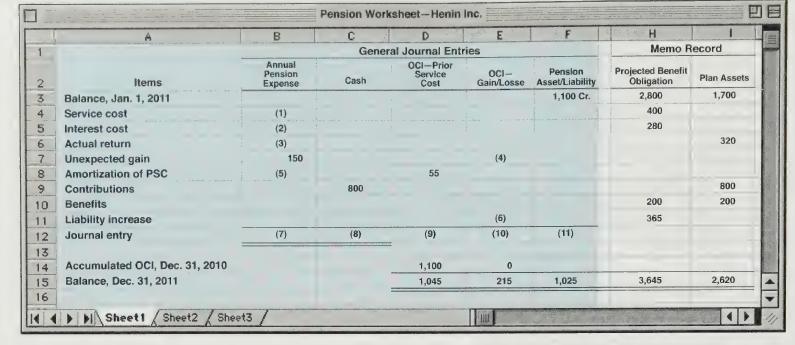

(Pension Worksheet—Missing Amounts) The accounting staff of Henin Inc. has prepared the following pension worksheet. Unfortunately, several entries in the worksheet are not decipherable. The company has asked your assistance in completing the worksheet and completing the accounting tasks related

(Postretirement Benefit Expense Computation) Ankiel Co. provides the following information 11) about its postretirement benefit plan for the year 2010.Instructions Compute the postretirement benefit expense for 2010. Service cost Contribution to the plan Actual and expected return on plan assets

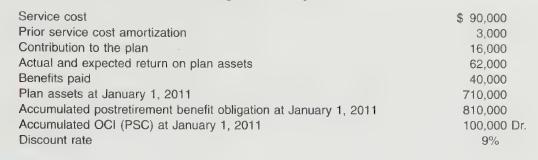

(Postretirement Benefit Expense Computation) Chance Inc. provides the following information related to its postretirement benefits for the year 2012.Instructions Compute postretirement benefit expense for 2012. Accumulated postretirement benefit obligation at January 1, 2012 $810,000 Actual and

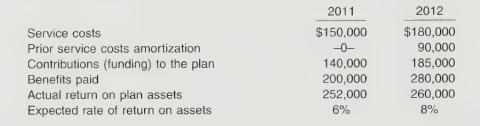

(Postretirement Benefit Expense Computation) Marvelous Marvin Co. provides the following information about its postretirement benefit plan for the year 2011.Instructions Compute the postretirement benefit expense for 2011. Service cost Prior service cost amortization Contribution to the plan Actual

(Postretirement Benefit Worksheet) Using the information in *E20-22 prepare a worksheet in- serting January 1, 2011, balances, showing December 31, 2011, balances, and the journal entry recording postretirement benefit expense.

(Postretirement Benefit Worksheet—Missing Amounts) The accounting staff of Hewitt Inc. has prepared the following postretirement benefit worksheet. Unfortunately, several entries in the worksheet are not decipherable. The company has asked your assistance in completing the worksheet and

(2-Year Worksheet) On January 1, 2011, Diana Peter Company has the following defined benefit pension plan balances.The interest (settlement) rate applicable to the plan is 10%. On January 1, 2012, the company amends its pension agreement so that prior service costs of $500,000 are created. Other

(3-Year Worksheet, Journal Entries, and Reporting) Katie Day Company adopts acceptable accounting for its defined benefit pension plan on January 1, 2011, with the following beginning balances:plan assets $200,000; projected benefit obligation $200,000. Other data relating to 3 years’ operation

. (Pension Expense, Journal Entries, Amortization of Loss) Paul Dobson Company sponsors a defined benefit plan for its 100 employees. On January 1, 2010, the company’s actuary provided the following information.The average remaining service period for the participating employees is 10.5 years.

(Pension Expense, Journal Entries for 2 Years) Mantle Company sponsors a defined benefit pen- ve - sion plan. The following information related to the pension plan is available for 2010 and 2011.Instructions (a) Compute pension expense for 2010 and 2011.(b) Prepare the journal entries to record the

(Computation of Pension Expense, Amortization of Net Gain or Loss—Corridor Approach, Journal Entries for 3 Years) Dubel Toothpaste Company initiates a defined benefit pension plan for its 50 employees on January 1, 2010. The insurance company which administers the pension plan provided the

(Computation of Prior Service Cost Amortization, Pension Expense, Journal Entries, and Net Gain or Loss) Widjaja Inc. has sponsored a noncontributory-defined benefit pension plan for its employees since 1987. Prior to 2010, cumulative net pension expense recognized equaled cumulative contributions

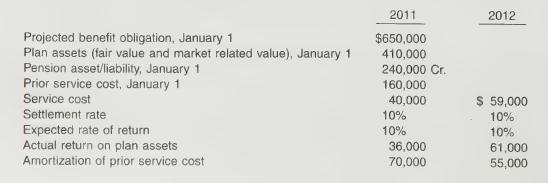

(Pension Worksheet) Farber Corp. sponsors a defined benefit pension plan for its employees.On January 1, 2012, the following balances related to this plan.As a result of the operation of the plan during 2012, the actuary provided the following additional data at December 31, 2012.Instructions Using

(Comprehensive 2-Year Worksheet) Glesen Company sponsors a defined benefit pension plan for its employees. The following data relate to the operation of the plan for the years 2011 and 2012.Instructions (a) Prepare a pension worksheet presenting both years 2011 and 2012 and accompanying

(Comprehensive 2-Year Worksheet) Mount Co. has the following defined benefit pension plan balances on January 1, 2009.The interest (settlement) rate applicable to the plan is 10%. On January 1, 2010, the company amends its pension agreement so that prior service costs of $600,000 are created. Other

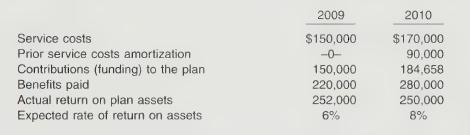

(Pension Worksheet — Missing Amounts) Enyart Co. has prepared the following pension worksheet.Unfortunately, several entries in the worksheet are not decipherable. The company has asked your assistance in completing the worksheet and completing the accounting tasks related to the pension plan for

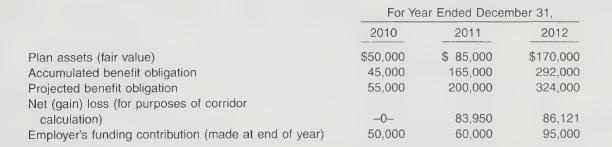

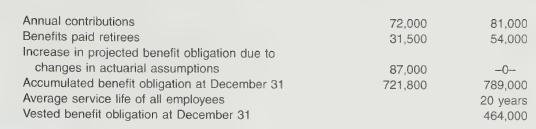

(Pension Worksheet) The following data relate to the operation of Enyart Co.’s pension plan in 2012. The pension worksheet for 2011 is provided in P20-10.For 2012, Enyart will use the same assumptions as 2011 for the settlement rate and the expected rate of return on plan assets.Instructions (a)

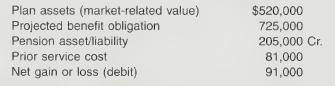

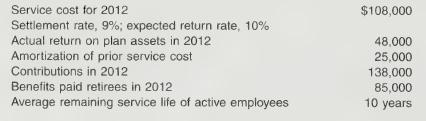

(Pension Worksheet) Cramer Corp. sponsors a defined-benefit pension plan for its employees.On January 1, 2012, the following balances related to this plan.As a result of the operation of the plan during 2012, the actuary provided the following additional data at December 31, 2012.Instructions (a)

(Postretirement Benefit Worksheet) Dusty Hass Foods Inc. sponsors a postretirement medical and dental benefit plan for its employees. The company adopts the provisions of Statement No. 106 beginning January 1, 2011. The following balances relate to this plan on January 1, 2011.As a result of the

(Postretirement Benefit Worksheet—2 Years) Embry Co. has the following postretirement ben- efit plan balances on January 1, 2009.The interest (settlement) rate applicable to the plan is 10%. On January 1, 2010, the company amends the plan so that prior service costs of $175,000 are created. Other

(Pension Terminology) The following items appear on Hollingsworth Company’s financial statements.1. Under the caption Assets:Pension asset/liability.2. Under the caption Liabilities:Pension asset/liability.3. Under the caption Stockholders’ Equity:Prior service cost as a component of

(Basic Terminology) In examining the costs of pension plans, Leah Hutcherson, CPA, encounters certain terms. The components of pension costs that the terms represent must be dealt with appropriately if generally accepted accounting principles are to be reflected in the financial statements of

(Major Pension Concepts) Lyons Corporation is a medium-sized manufacturer of paperboard containers and boxes. The corporation sponsors a noncontributory, defined benefit pension plan that covers its 250 employees. Tim Shea has recently been hired as president of Lyons Corporation. While reviewing

(Implications of FASB Statement No. 87) Ruth Moore and Carl Nies have to do a class presentation on the pension pronouncement “Employers’ Accounting for Pension Plans.” In developing the class presentation, they decided to provide the class with a series of questions related to pensions and

(Gains and Losses, Corridor Amortization) Rachel Avery, accounting clerk in the personnel office of Clarence G. Avery Corp., has begun to compute pension expense for 2010 but is not sure whether or not she should include the amortization of unrecognized gains/losses. She is currently working with

. (Nonvested Employees—An Ethical Dilemma) Cardinal Technology recently merged with College Electronix, a computer graphics manufacturing firm. In performing a comprehensive audit of CE’s accounting system, Richard Nye, internal audit manager for Cardinal Technology, discovered that the new

Jackie Remmers Co. is expanding its operations and is in the process of selecting the method of financing this program. After some investigation, the company deter- mines that it may (1) issue bonds and with the proceeds purchase the needed assets or (2) lease the assets on a long-term basis.

Use the information for Rick Kleckner Corporation from BE21-3. Assume that at December 31, 2008, Kleckner made an adjusting entry to accrue interest expense of $19,686 on the lease. Prepare Kleck- ner's January 1, 2009, journal entry to record the second lease payment of $35,947.

Jana Kingston Corporation enters into a lease on January 1, 2008, that does not transfer owner- ship or contain a bargain purchase option. It covers 3 years of the equipment's 8-year useful life, and the present value of the minimum lease payments is less than 90% of the fair market value of the

Jennifer Brent Corporation owns equipment that cost $72,000 and has a useful life of 8 years with no salvage value. On January 1, 2008, Jennifer Brent leases the equipment to Donna Havaci Inc. for one year with one rental payment of $15,000 on January 1. Prepare Jennifer Brent Corporation's 2008

Indiana Jones Corporation enters into a 6-year lease of equipment on January 1, 2008, which requires 6 annual payments of $30,000 each, beginning January 1, 2008. In addition, Indiana Jones guar- antees the lessor a residual value of $20,000 at lease-end. The equipment has a useful life of 6 years.

Use the information for Indiana Jones Corporation from BE21-9. Assume that for Lost Ark Com- pany, the lessor, collectibility is reasonably predictable, there are no important uncertainties concerning costs, and the carrying amount of the machinery is $155,013. Prepare Lost Ark's January 1, 2008,

On January 1, 2008, Acme Animation sold a truck to Coyote Finance for $35,000 and immedi- ately leased it back. The truck was carried on Acme's books at $28,000. The term of the lease is 5 years, and title transfers to Acme at lease-end. The lease requires five equal rental payments of $9,233 at

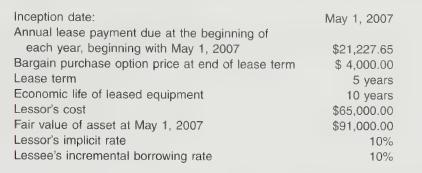

(Lessee Entries; Capital Lease with Unguaranteed Residual Value) On January 1, 2007, Burke Corporation signed a 5-year noncancelable lease for a machine. The terms of the lease called for Burke to make annual payments of $8,668 at the beginning of each year, starting January 1, 2007. The machine

(Lessee Computations and Entries; Capital Lease with Guaranteed Residual Value) Pat Delaney Company leases an automobile with a fair value of $8,725 from John Simon Motors, Inc., on the following terms:1. Noncancelable term of 50 months.2. Rental of $200 per month (at end of each month). (The

(Lessee Entries; Capital Lease with Executory Costs and Unguaranteed Residual Value)Assume that on January 1, 2008, Kimberly-Clark Corp. signs a 10-year noncancelable lease agreement to lease a storage building from Sheffield Storage Company. The following information pertains to this lease’

(Lessor Entries; Direct-Financing Lease with Option to Purchase) Castle Leasing Company signs a lease agreement on January 1, 2008, to lease electronic equipment to Jan Way Company. The term of the noncancelable lease is 2 years, and payments are required at the end of each year. The following

(Type of Lease; Amortization Schedule) Mike Macinski Leasing Company leases a new machine that has a cost and fair value of $95,000 to Sharrer Corporation on a 3-year noncancelable contract.Sharrer Corporation agrees to assume all risks of normal ownership including such costs as insurance, taxes,

(Lessor Entries; Sales-Type Lease) Crosley Company, a machinery dealer, leased a machine to Dexter Corporation on January 1, 2007. The lease is for an 8-year period and requires equal annual payments of $35,013 at the beginning of each year. The first payment is received on January 1, 2007. Crosley

(Lessee-Lessor Entries; Sales-Type Lease) On January 1, 2007, Bensen Company leased equipment to Flynn Corporation. The following information pertains to this lease.1. The term of the noncancelable lease is 6 years, with no renewal option. The equipment reverts to the lessor at the termination of

(Lessee Entries with Bargain Purchase Option) The following facts pertain to a noncancelable lease agreement between Mooney Leasing Company and Rode Company, a lessee.The collectibility of the lease payments is reasonably predictable, and there are no important uncertainties surrounding the costs

(Lessor Entries with Bargain Purchase Option) A lease agreement between Mooney Leasing Company and Rode Company is described in E21-8.instructions(Round all numbers to the nearest cent.)Refer to the data in E21-8 and do the following for the lessor.(a) Compute the amount of the lease receivable at

(Computation of Rental; Journal Entries for Lessor) Morgan Leasing Company signs an agreement on January 1, 2007, to lease equipment to Cole Company. The tollowing information relates to this agreement.1. The term of the noncancelable lease is 6 years with no renewal option. The equipment has an

(Amortization Schedule and Journal Entries for Lessee) Laura Leasing Company signs an agreement on January 1, 2007, to lease equipment to Plote Company. The information at the top of page 1136 relates to this agreement.1. The term of the noncancelable lease is 5 years with no renewal option. The

(Accounting for an Operating Lease) On January 1, 2007, Doug Nelson Co. leased a building to Patrick Wise Inc. The relevant information related to the lease is as follows.1. The lease arrangement is for 10 years.2. The leased building cost $4,500,000 and was purchased for cash on January 1, 2007.3.

(Accounting for an Operating Lease) On January 1, 2008, a machine was purchased for $900,000 by Young Co. The machine is expected to have an 8-year life with no salvage value. It is to be depreciated on a straight-line basis. The machine was leased to St. Leger Inc. on January 1, 2008, at an annual

(Operating Lease for Lessee and Lessor) On February 20, 2007, Barbara Brent Inc., purchased a machine for $1,500,000 for the purpose of leasing it. The machine is expected to have a 10-year life, no residual value, and will be depreciated on the straight-line basis. The machine was leased to Rudy

(Sale and Leaseback) Assume that on January 1, 2007, Elmer’s Restaurants sells a computer system to Liquidity Finance Co. for $680,000 and immediately leases the computer system back. The relevant information is as follows.1. The computer was carried on Elmer’s books at a value of $600,000.2.

(Lessee-Lessor, Sale-Leaseback) Presented below are four independent situations. (a) On December 31, 2008, Zarle Inc. sold computer equipment to Daniell Co. and immediately leased it back for 10 years. The sales price of the equipment was $520,000, its carrying amount is $400,000, and its estimated

The book basis of depreciable assets for Getty Co. is $900,000, and the tax basis is $700,000 at the end of 2007. The enacted tax rate is 34% for all periods. Determine the amount of deferred taxes to be reported on the bal- ance sheet at the end of 2007.

Borg Inc. has a deferred tax liability of $68,000 at the be- ginning of 2007. At the end of 2007, it reports accounts receivable on the books at $80,000 and the tax basis at zero (its only temporary difference). If the enacted tax rate is 34% for all periods, and income tax payable for the period

Pretax financial income for Mott Inc. is $300,000, and its taxable income is $100,000 for 2007. Its only temporary difference at the end of the period relates to a $90,000 difference due to excess depreciation for tax purposes. If the tax rate is 40% for all periods, compute the amount of income

At the end of the year, North Carolina Co. has pretax financial income of $550,000. Included in the $550,000 is $70,000 interest income on municipal bonds, $30,000 fine for dumping hazardous waste, and depreciation of $60,000. Depreciation for tax purposes is $45,000. Com- pute income taxes

Raleigh Co. has one temporary difference at the beginning of 2007 of $500,000. The deferred tax liability established for this amount is $150,000, based on a tax rate of 30%. The temporary difference will provide the following tax- able amounts: $100,000 in 2008; $200,000 in 2009, and $200,000 in

Murphy Corporation began operations in 2007 and reported pretax financial income of $225,000 for the year. Murphy's tax depreciation exceeded its book depreciation by $30,000. Murphy's tax rate for 2007 and years thereafter is 30%. In its December 31, 2007 balance sheet, what amount of deferred tax

At December 31, 2006, Yserbius Corporation had a deferred tax liability of $25,000. At Decem- ber 31, 2007, the deferred tax liability is $42,000. The corporation's 2007 current tax expense is $43,000. What amount should Yserbius report as total 2007 tax expense?

At December 31, 2006, Next Generation Inc. had a deferred tax asset of $35,000. At December 31, 2007, the deferred tax asset is $59,000. The corporation's 2007 current tax expense is $61,000. What amount should Next Generation report as total 2007 tax expense?

Terminator Corporation has a cumulative temporary difference related to depreciation of $630,000 at December 31, 2007. This difference will reverse as follows: 2008, $42,000; 2009, $294,000; and 2010, $294,000. Enacted tax rates are 34% for 2008 and 2009, and 40% for 2010. Compute the amount Ter-

At December 31, 2006, Tick Corporation had a deferred tax liability of $680,000, resulting from future taxable amounts of $2,000,000 and an enacted tax rate of 34%. In May 2007, a new income tax act is signed into law that raises the tax rate to 38% for 2007 and future years. Prepare the journal

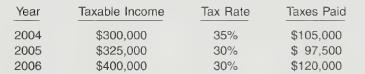

Valis Corporation had the following tax information.In 2007 Valis suffered a net operating loss of $450,000, which it elected to carry back. The 2007 enacted tax rate is 29%. Prepare Valis's entry to record the effect of the loss carryback. Year Taxable Income Tax Rate Taxes Paid 2004 $300,000 35%

Zoop Inc. incurred a net operating loss of $500,000 in 2007. Combined income for 2005 and 2006 was $400,000. The tax rate for all years is 40%. Zoop elects the carryback option. Prepare the journal en- tries to record the benefits of the loss carryback and the loss carryforward.

Use the information for Zoop Inc. given in BE19-13. Assume that it is more likely than not that the entire net operating loss carryforward will not be realized in future years. Prepare all the journal en- tries necessary at the end of 2007.

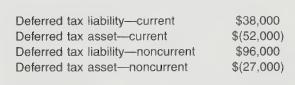

Vectorman Corporation has temporary differences at December 31, 2007, that result in the fol- lowing deferred taxes.Indicate how these balances would be presented in Vectorman’s December 31, 2007, balance sheet. Deferred tax liability-current Deferred tax asset-current Deferred tax

(One Temporary Difference, Future Taxable Amounts, One Rate, No Beginning Deferred Taxes)South Carolina Corporation has one temporary difference at the end of 2007 that will reverse and cause taxable amounts of $55,000 in 2008, $60,000 in 2009, and $65,000 in 2010. South Carolina’s pretax

. (Two Differences, No Beginning Deferred Taxes, Tracked through 2 Years) The following information is available for Wenger Corporation for 2006.1. Excess of tax depreciation over book depreciation, $40,000. This $40,000 difference will reverse equally over the years 2007-2010.2. Deferral, for book

(One Temporary Difference, Future Taxable Amounts, One Rate, Beginning Deferred Taxes)Bandung Corporation began 2007 with a $92,000 balance in the Deferred Tax Liability account. At the end of 2007, the related cumulative temporary difference amounts to $350,000, and it will reverse evenly over the

(Three Differences, Compute Taxable Income, Entry for Taxes) Zurich Company reports pretax financial income of $70,000 for 2007. The following items cause taxable income to be different than pretax financial income.1. Depreciation on the tax return is greater than depreciation on the income

(Two Temporary Differences, One Rate, Beginning Deferred Taxes) The following facts relate to Krung Thep Corporation.1. Deferred tax liability, January 1, 2007, $40,000.2. Deferred tax asset, January 1, 2007, $0.3. Taxable income for 2007, $95,000.4. Pretax financial income for 2007, $200,000.5.

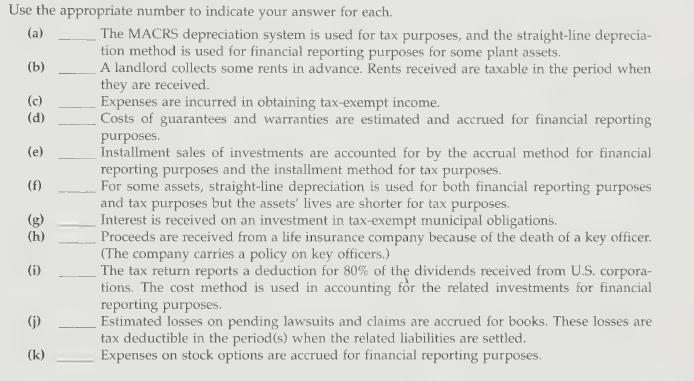

(Identify Temporary or Permanent Differences) Listed below are items that are commonly accounted for differently for financial reporting purposes than they are for tax purposes.Instructions For each item below, indicate whether it involves:(1)(2)(3)A temporary difference that will result in future

(Terminology, Relationships, Computations, Entries) Instructions Complete the following statements by filling in the blanks. (a) In a period in which a taxable temporary difference reverses, the reversal will cause taxable in- come to be (less than, greater than) pretax financial income. (b) If a

(Two Temporary Differences, One Rate, 3 Years) Button Company has two temporary differences between its income tax expense and income taxes payable. The information is shown on page 1004.Instructions (a) Prepare the journal entry to record income tax expense, deferred income taxes, and income tax

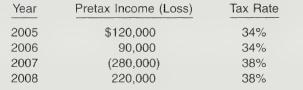

(Carryback and Carryforward of NOL, No Valuation Account, No Temporary Differences) The pretax financial income (or loss) figures for Jenny Spangler Company are as follows.Pretax financial income (or loss) and taxable income (loss) were the same for all years involved. Assume a 45% tax rate for

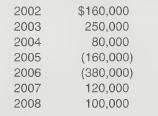

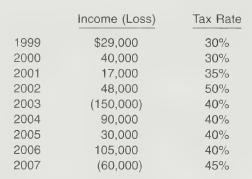

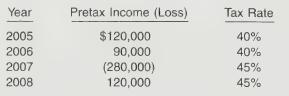

(Two NOLs, No Temporary Differences, No Valuation Account, Entries and Income Statement)Felicia Rashad Corporation has pretax financial income (or loss) equal to taxable income (or loss) from 1999 through 2007 as follows.Pretax financial income (loss) and taxable income (loss) were the same for all

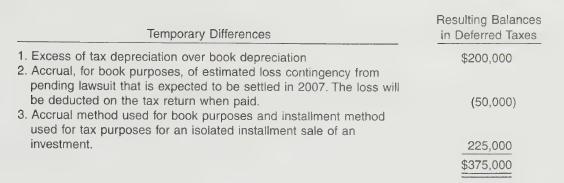

(Three Differences, Classify Deferred Taxes) At December 31, 2006, Belmont Company had a net deferred tax liability of $375,000. An explanation of the items that compose this balance is as follows.In analyzing the temporary differences, you find that $30,000 of the depreciation temporary difference

(Two Temporary Differences, One Rate, Beginning Deferred Taxes, Compute Pretax Financial Income) The following facts relate to Duncan Corporation.1. Deferred tax liability, January 1, 2007, $60,000.Deferred tax asset, January 1, 2007, $20,000.Taxable income for 2007, $105,000.Cumulative temporary

(One Difference, Multiple Rates, Effect of Beginning Balance versus No Beginning Deferred Taxes) At the end of 2006, Lucretia McEvil Company has $180,000 of cumulative temporary differences that will result in reporting future taxable amounts as follows.Tax rates enacted as of the beginning of 2005

(Deferred Tax Asset with and without Valuation Account) Jennifer Capriati Corp. has a deferred tax asset account with a balance of $150,000 at the end of 2006 due to a single cumulative temporary difference of $375,000. At the end of 2007 this same temporary difference has increased to a cumulative

(Deferred Tax Asset with Previous Valuation Account) Assume the same information as E19-14, except that at the end of 2006, Jennifer Capriati Corp. had a valuation account related to its deferred tax asset of $45,000.Instructions(a) Record income tax expense, deferred income taxes, and income taxes

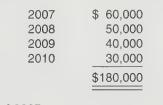

(Deferred Tax Liability, Change in Tax Rate, Prepare Section of Income Statement) Novotna Inc.’s only temporary difference at the beginning and end of 2006 is caused by a $3 million deferred gain for tax purposes for an installment sale of a plant asset, and the related receivable (only one-half

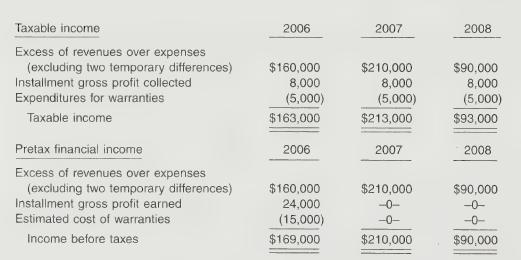

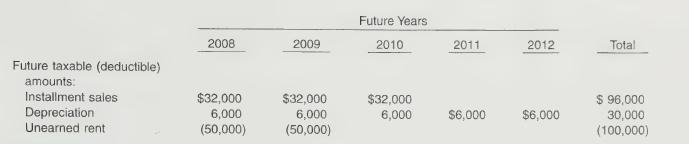

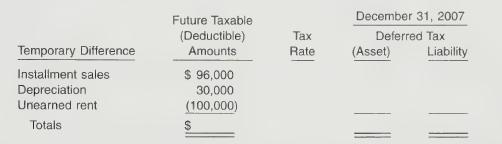

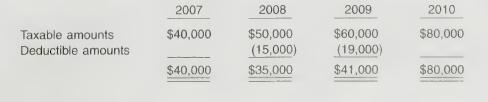

(Two Temporary Differences, Tracked through 3 Years, Multiple Rates) Taxable income and pretax financial income would be identical for Huber Co. except for its treatments of gross profit on installment sales and estimated costs of warranties. The following income computations have been prepared.The

(Three Differences, Multiple Rates, Future Taxable Income) During 2007, Kate Holmes Co.’s first year of operations, the company reports pretax financial income at $250,000. Holmes’s enacted tax rate is 45% for 2007 and 40% for all later years. Holmes expects to have taxable income in each of

(Two Differences, One Rate, Beginning Deferred Balance, Compute Pretax Financial Income) Andy McDowell Co. establishes a $100 million liability at the end of 2007 for the estimated site-cleanup costs at two of its manufacturing facilities. All related closing costs will be paid and deducted on

(Two Differences, No Beginning Deferred Taxes, Multiple Rates) Teri Hatcher Inc., in its first year of operations, has the following differences between the book basis and tax basis of its assets and liabilities at the end of 2006.0OIt is estimated that the warranty liability will be settled in

(Two Temporary Differences, Multiple Rates, Future Taxable Income) Nadal Inc. has two tem- porary differences at the end of 2006. The first difference stems from installment sales, and the second one results from the accrual of a loss contingency. Nadal's accounting department has developed a

(Two Differences, One Rate, First Year) The differences between the book basis and tax basis of the assets and liabilities of Castle Corporation at the end of 2006 are presented below.It is estimated that the litigation liability will be settled in 2007. The difference in accounts receivable will

(NOL Carryback and Carryforward, Valuation Account versus No Valuation Account)Spamela Hamderson Inc. reports the following pretax income (loss) for both financial reporting purposes and tax purposes. (Assume the carryback provision is used for a net operating loss.)The tax rates listed were all

(NOL Carryback and Carryforward, Valuation Account Needed) Beilman Inc. reports the following pretax income (loss) for both book and tax purposes. (Assume the carryback provision is used where possible for a net operating loss.)The tax rates listed were all enacted by the beginning of

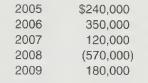

(NOL Carryback and Carryforward, Valuation Account Needed) Meyer reported the following pretax financial income (loss) for the years 2005-2009.Pretax financial income (loss) and taxable income (loss) were the same for all years involved. The enacted tax rate was 34% for 2005 and 2006, and 40% for

(Three Differences, No Beginning Deferred Taxes, Multiple Rates) The following information is available for Swanson Corporation for 2006.1. Depreciation reported on the tax return exceeded depreciation reported on the income statement by $100,000. This difference will reverse in equal amounts of

(One Temporary Difference, Tracked for 4 Years, One Permanent Difference, Change in Rate)The pretax financial income of Parker-Gregory Company differs from its taxable income throughout each of 4 years as follows.Pretax financial income for each year includes a nondeductible expense of $30,000

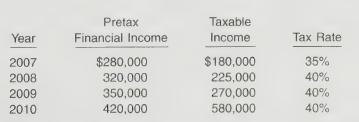

(Second Year of Depreciation Difference, Two Differences, Single Rate, Extraordinary Item)The following information has been obtained for the Kerdyk Corporation.1. Prior to 2006, taxable income and pretax financial income were identical.Pretax financial income is $1,700,000 in 2006 and $1,400,000

Showing 200 - 300

of 2378

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers