New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

management accounting

Management Accounting Text Problems And Cases 6th Edition M Y Khan, P K Jain - Solutions

(a) “Certain costs are controllable and certain other costs are non-controllable.” This is a meaningless statement unless we define what portion of the organisation is being discussed. Explain.(b) Write short notes on controllable and uncontrollable costs.

What are the various methods by which you would split semi-variable costs in its fixed and variable elements?

(a) The classification of costs as controllable and non-controllable depends upon a point of reference. Explain.(b) Direct costs and controllable costs are not necessarily the same. Comment.(c) Why are sunk costs not relevant in decision-making?

(a) “All future costs are relevant.” Do you agree? Why?(b) “Fixed costs are really variable. The more you produce the less they become.” Do you agree?Explain.

(a) “All controllable costs are direct costs. Not all direct costs are controllable.” Explain with the help of suitable examples.(b) Distinguish between (i) engineered, (ii) discretionary, and (iii) committed costs. Give suitable examples. Are all these costs controllable?

If the price of the material is ₹15 per unit and the annual consumption is 4,000 units, the interest and store-keeping charges are 20 per cent of the value and the cost of placing of an order and receiving the goods is ₹60, how much material should be ordered at one time?

Two components, A and B are used as follows:Calculate for each component: (a) Re-order level, (b) Minimum level, (c) Maximum level, and (d)Average stock level. Normal usage Minimum usage Maximum usage Re-order quantity Re-order period : 50 units each per week 25 units each per week : 75 units each

The following information pertaining to a firm are available: Annual consumption Cost per unit Cost per order Inventory carrying cost (%) Lead time (maximum, normal and minimum) (days) Daily consumption: (maximum, normal and minimum) (units) Calculate inventory levels. 12,000 units (360 days) 1 12

Peekay Company Ltd has been buying a given item in lots of 1,200 units which is a six months’supply, the cost per unit is ₹12, order cost is ₹8 per order, and carrying cost is 25 per cent. You are required to calculate the savings per year by buying in economical lot quantities.

Ganges Pump Company Ltd. uses about 75,000 valves per year and the usage is fairly constant at 6,250 per month. The valve cost of ₹1.50 per unit when bought in large quantities, and the carrying cost is estimated to be 20 per cent of average inventory investment on an annual basis. The cost to

Precision Engineering Factory Ltd consumes 50,000 units of a component per year. The ordering, receiving and handling cost are ₹3 per order while the trucking costs are ₹12 per order. Further details are as follows: deterioration and obsolescence cost, ₹0.004 per unit per year; storage cost,

A customer has been ordering 5,000 special design metal columns at the rate of 1,000 per order during the past year. The production cost is ₹12 a unit–₹8 for materials and labour and ₹4 for overheads(fixed) cost. It costs ₹1,500 to set up for one run of 1,000 columns, and inventory

Royal Industries Ltd manufacturers plastic lunch boxes in a moulding process. On an annual basis, the industry manufacturers 1,000 plastic lunch boxes at a cost of ₹4 per unit. The industry’s differential costs of carrying the item in the finished goods inventory are 20 per cent of the

IPL Limited uses a small casting in one of its finished products. The castings are purchased from a foundry. IPL Limited purchases 54,000 castings per year at a cost of ₹800 per casting.The castings are used evenly throughout the year in the production process on a 360-day-per-year basis. The

SK Enterprise manufactures a special product “ZE”. The following particulars were collected for the year 2004:Required: (i) Re-order quantity (ii) Re-order level (iii) What should be the inventory level (ideally)immediately before the material order is received? Annual consumption Cost per unit

A company manufactures a product from a raw material, which is purchased at ₹60 per kg. The company incurs a handling cost of ₹360 plus freight of ₹390 per order. The incremental carrying cost of inventory of raw material is ₹0.50 per kg. per month. In addition, the cost of working capital

“Management accounting is a mid-way between financial accounting and cost accounting.” Elucidate.

Fill in the following blanks(i) The accounting information specifically prepared to aid managers is called _______________ information.(ii) _______________ is the process to ensure that employees perform properly.(iii) The highest level management accountant is called the ______________.(iv)

“There are no externally imposed “Generally Accepted Accounting Principles’ for Management Accounting.” In the light of the above statement, discuss, giving illustrations, the nature and scope of management accounting.

Explain the following:(a) “Management accounting is an extension of financial accounting.”(b) “Management accounting assists in corporate planning process.”

The emphasis of financial accounting is different from that of cost accounting.” Comment.

“Management accounting is the presentation of accounting information in such a way as to assist the management in the creation of policy, and in the day-to-day operation of an undertaking.” Elucidate.

In what essential respects is management accounting different from financial accounting?

(a) “There is no single, unified management accounting system, rather there are three different types of information, each used for different purposes.” Elaborate.(b) Mention the differences which exist between financial accounting and management accounting.Also point out the similarities, if

Discuss the three managerial functions in which management accounting information can be used.

What is money measurement concept? State the impact of inflation on the monetary unit assumption.

Describe the accounting principle which explains losses are assets, and profits and capital are liabilities for a business firm.

“Profit and loss account provides only estimated figures of profit earned or loss suffered.” Explain.

“Accrual accounting is superior to cash accounting”. Elaborate.

Name the two major claimants who have claim on the firm’s assets.

List the main elements of balance sheet and income statement.

In preparing balance sheet, would you use the historical cost or current market value while dealing with assets? Explain.

What is the major revenue recognition criterion?

Name the accounting principle involved/violated/affected in the following:(i) The firm changes method of depreciation.(ii) The firm does not consider unused stationery as asset.(iii) The firm follows the policy of expensing all office equipments of less than ₹5,000.(iv) Capital is recorded on

Using accounting equation, answer the following independent questions.(i) New company’s assets are ₹250 lakh and its external liabilities are of ₹100 lakh, determine the amount of owners’ equity.(ii) Royal Industries has total assets of ₹100 lakh and owners’ equity of ₹70 lakh,

Name the 5 major areas in which different accounting policies can be adopted by business enterprises. What is the requirement of the relevant accounting standard in this regard?

Describe in brief the major requirements of accounting standards related to valuation of inventories and depreciation accounting.

What is the criteria of revenue recognition?

Describe in brief disclosure requirements of accounting standards related to accounting for fixed assets and investments.

Explain the concepts of basic earnings per share and diluted earnings per share. How are they computed?

Explain the terms: (i) timing differences, (ii) permanent differences, (iii) deferred tax liability and (iv) deferred tax asset as per accounting standard related to taxes on income.

What is the basis of recognising intangible assets? How are they amortised? What are the major disclosure requirements of accounting standard for such assets?

What is impairment of assets? Is reversal of impairment loss feasible? Explain your answer based on the requirements of accounting standard.

Define provisions, contingent liabilities and contingent assets. State the major requirements of their accounting and disclosure of all the three to conform the needs of accounting standard.

Mr. Ashwin commenced business (in the name of M/s Ashwin Associates) from April 1, 2013 as a garment manufacturer. Following are the transactions for the six months ending September 30, 2013.1. \(\mathrm{M} / \mathrm{s}\) Ashwin Associates commenced business activity with initial capital of ₹

From the trial balance drawn in P.3.1 and from the following adjustment transactions (a) pass adjustment entries and prepare (b) (i) manufacturing account, (ii) trading account, (iii) P\&L account for the period ending September 30, 2013 and (iv) balance sheet as at September 30, 2013.(a) Closing

(a) Record closing entries for P.3.2 and (b) opening entry as on October 1, 2013 in the books of Aswin Associates.P.3.2From the trial balance drawn in P.3.1 and from the following adjustment transactions (a) pass adjustment entries and prepare (b) (i) manufacturing account, (ii) trading account,

Prepare special journal books from the transactions contained in P.3.1.P.3.1 Mr. Ashwin commenced business (in the name of M/s Ashwin Associates) from April 1, 2013 as a garment manufacturer. Following are the transactions for the six months ending September 30, 2013.1. \(\mathrm{M} / \mathrm{s}\)

Small Toy Private Limited (STPC) has been manufacturing toys as well as buying from the market since 2001. The owners of the company are satisfied both with its profit margins its reputation in the market. They are planning for expansion of the business for which a high-tech machine costing ₹30

Name the steps (in sequence form) involved in the accounting cycle.

Debit implies increase and credit implies decrease. Do you agree with the statement? Explain your answer.

What are nominal, real and personal accounts? Give four examples of each of them.

What is balancing of account? What are the two types of balances? Can a cash account have credit balance?

What is journal? State its two broad categories. Name the five special journal.

What is ledger? State its two broad types. Name three special ledger books.

What is a trial balance? Name the errors disclosed as well as not disclosed by trial balance.

“Trial balance is not a conclusive proof as to the absolute accuracy of books of accounts. It may agree and yet there may be some errors in the books that remain undisclosed.” Elaborate. Give concrete examples in support of your answer.

State the procedure of posting from 4 special journal books to ledger books. Explain the procedure with examples. What is the advantage of writing journal folio and ledger folio numbers?

What are adjustment entries? What is their rationale? Name 5 adjustment items and pass their adjustment entries.

What are closing entries? Why are they needed? Name the type of accounts (a) required to be closed and (b) not required to be closed.

What is an ‘opening entry’? Why is it needed? Pass the opening entry with imaginary figures.

“Double entry implies that transaction is recorded in journal and ledger.” Explain.

Distinguish between the following:(i) Long-term assets and Current assets(ii) Tangible assets and Non-tangible assets(iii) Long-term liabilities and Current liabilities(iv) Gross profit and Operating profit

What is a manufacturing account? What is its objectives? Prepare a manufacturing account with appropriate imaginary figures.

What is a trading account? What are its major constituents? What is its major outcome?

What is a profit and loss account? Draw its format with as many items as possible.

“While balance sheet is like a snapshot, profit and loss account is like a moving picture.” Explain.

“While interest payment is an expense, dividend payment, in contrast, is not reckoned expense.”Explain.

“Revenues are positive shareholders equity accounts while expenses are negative accounts in this regard.” Explain.

What is P&L Appropriation Account? What purpose does it serve? Do you require such an account in all type of firms? Draw such an account with imaginary figures.

“Capital expenditures and deferred revenue expenditures need to be apportioned to determine true income.” Explain. Give 3 examples of each.

“Extraordinary items warrant exclusion to judge true operating performance of a business enterprise.”Elaborate. Give 3 examples each of abnormal losses and of abnormal gains.

Write short notes on the following:(i) Account(ii) Rules of debit and credit(iii) Cost of goods sold(iv) Errors of commission

State the rules of debit and credit as applied to (a) expense accounts, (b) asset accounts(c) capital account.

Indicate whether the following accounts would normally possess a debit or credit balance:(a) Salaries, (b) Debtors, (c) Creditors, (d) Plant and machinery, (e) General reserve, (f) Patents,(g) Commission received, (h) Sales return, (i) Purchases, (u) Fuel and power, (k) Drawings, (l) Capital.

Arrange the following information in the sequence of accounting cycle:(a) Posting to the ledger,(b) Trial balance is prepared,(c) Business transaction takes place,(d) Income statement is prepared,(e) Closing entries are recorded, and(f) Information is recorded in journal.

Indicate whether the following statements are true or false:(a) All debit entries are posted on the left side of accounts and are indicative of decrease in the account balances.(b) All credit entries are recorded on the right side of accounts and represent increase in the account balances.(c) P&L

Fill in the following blanks:(i) Cost of goods sold = Opening stock of finished goods (+) __________ (–) Closing stock of finished goods in the case of trading firms.(ii) Gross profit = Sales revenue (–) __________.(iii) Operating profit = __________ (–) Operating expenses.(iv) Cost of raw

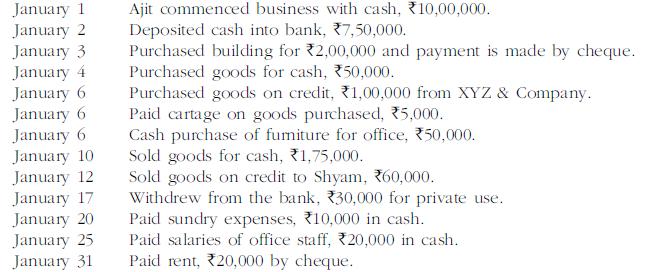

Journalise the following transactions of a hypothetical firm during the period January 1 to January 31. January 11 January 2 January 3 January 4 January 6 January 6 January 6 January 10 January 12 January 17 January 20 January 25 January 31 Ajit commenced business with cash, *10,00,000. Deposited

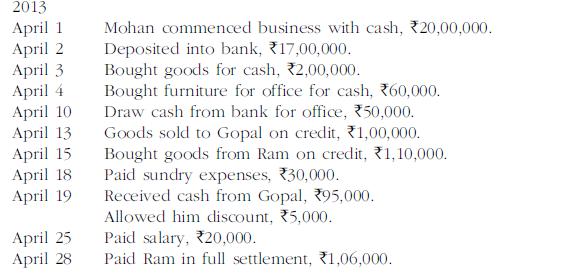

Journalise the following transactions. Post them into ledger and prepare trial balance. 2013 April 1 April 2 April 3 April 4 April 10 April 13 April 15 April 18 April 19 April 25 April 28 Mohan commenced business with cash, 20,00,000. Deposited into bank, 17,00,000. Bought goods for cash, 2,00,000.

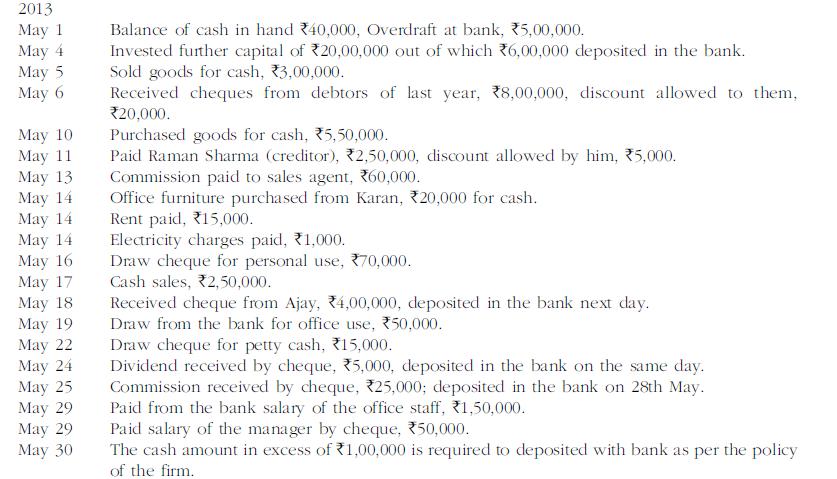

Enter the following transactions in cash book and bank book with discount columns. 2013 May 1 May 4 May 5 May 6 May 10 May 11 May 13 May 14 May 14 May 14 May 16 May 17 May 18 May 19 May 22 May 24 May 25 May 29 May 29 May 30 Balance of cash in hand 40,000, Overdraft at bank, 5,00,000. Invested

Mittal \& Co Pvt Ltd. ('MCPL'), registered on April 5, 2013 as a private limited company, is primarily engaged in fabrication and sale of steel products. For the transactions undertaken during the first quarter of its operation, you are required to pass journal entries.Transactions 1. April 5. MCPL

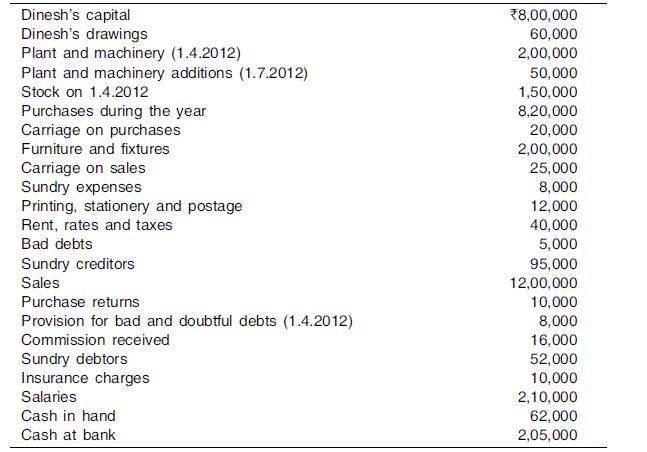

From the following ledger balances of Mr. Dinesh, prepare a trading account, P\&L account for the current year ended 31st March 2013 and a balance sheet as on that day, after making the necessary adjustments:Adjustments are required for the following:(1) Closing stock on 31.3.2013 was valued at

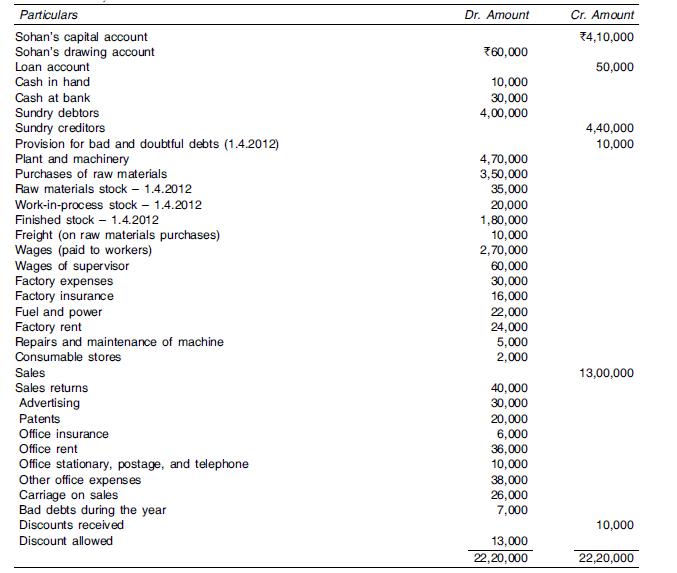

From the following trial balance, prepare manufacturing account, trading account, P&L A/c for the year ending March 2013 and a balance sheet as on that date of small manufacturing firm owned by Sohan.Additional information:(i) Stock on 31st March, 2013 was as follows: Raw materials, ₹35,000,

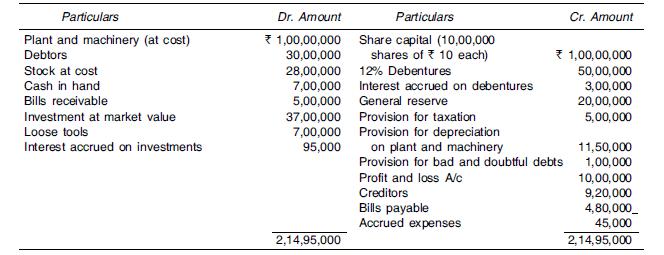

From the following balances extracted from the books of Small Toy Limited as at March 31, 2013(after preparation of the profit and loss account), prepare the balance sheet as at the above data.Additional Information:(1) Debtors include debts of ₹10,00,000, which are outstanding for a period

Show the presentation of the following information under the appropriate heads of the balance sheet of a public limited company.(i) General reserve (beginning) stood at ₹30,00,000, profit and loss account (beginning) at ₹10,00,000.Profit made during the year was ₹60,00,000. Dividend proposed

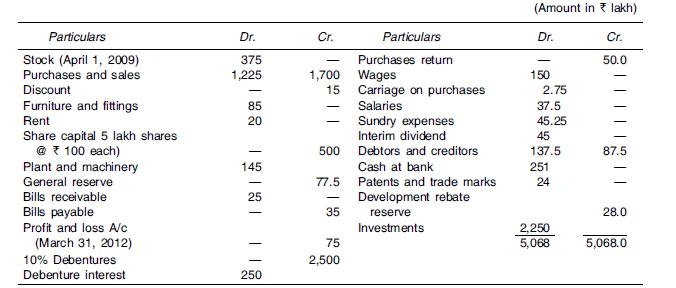

The following is the Trial balance of Amit Ltd., as at March 31, 2013:Prepare profit and loss account for the year ended 31st March, 2013 and balance sheet as at that date after considering the following adjustments:(i) Stock on 31st March 2013 was valued at ₹840 lakh.(ii) Make a provision for

State whether the following statements are true or false.(a) A company must prepare its profit and loss account in the format as prescribed by the Companies Act.(b) It is statutory for the company to prepare its balance sheet in the format prescribed in Part I of Scheduled VI of the Companies

Fill in the blanks:(a) SEBI has mandated corporate governance in the listing requirement in clause____________ of the listing agreement.(b) Apart from mandatory requirements listed in clause 49, the Board has also discretion to make___________________ .(c) Board of director’s report should also

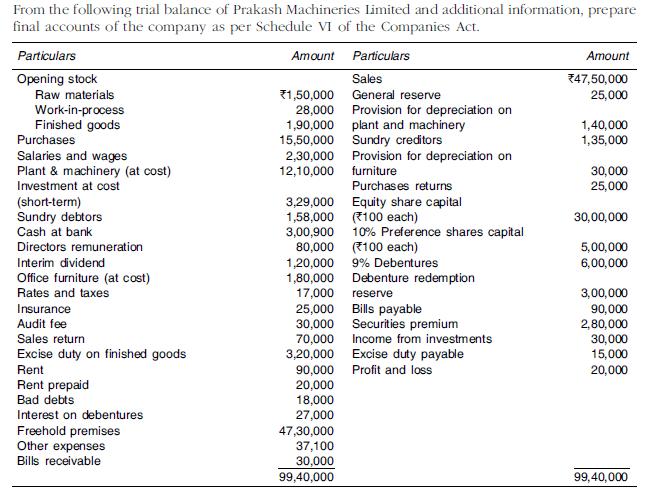

State the particular items to be disclosed in a company’s balance sheet as per Schedule VI of the Companies Act 1956 in respect of (a) fixed assets and (b) share capital.Schedule VI of the Companies Act 1956 From the following trial balance of Prakash Machineries Limited and additional

Name four contingent liabilities which may be shown as a footnote to balance sheet of a company.

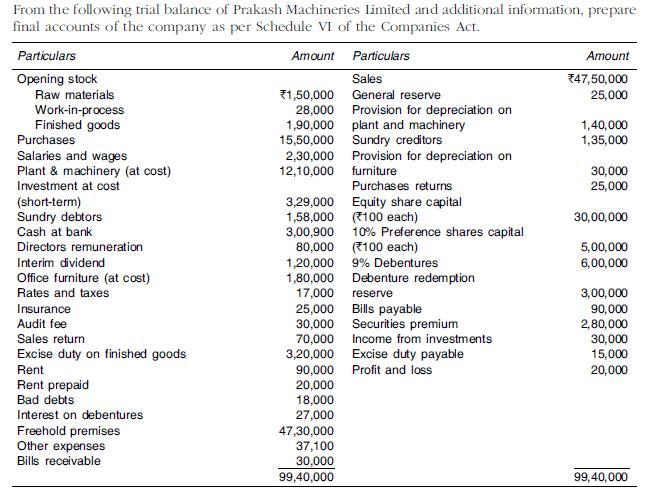

Draw-up pro-forma balance sheet in horizontal form as per the requirements of Schedule VI of the Companies Act 1956. Schedule VI of the Companies Act 1956 From the following trial balance of Prakash Machineries Limited and additional information, prepare final accounts of the company as per

Explain the provisions relating to maintenance of books of account and presentation of financial statements of a company.

Write short notes on the following:(a) Segment reporting (b) Interim financial reporting (c) Related party disclosure.

Enumerate, the mandatory and voluntary contents of Clause 49 of the listing agreement regarding corporate governance.

What is the objective of disclosing information about discontinued operations? Is abandonment of particular product in view of continuous decrease in market demand and diverting the resource to new substitute product is discontinuing operation? Explain your answer based on Accounting Standard -24.

Explain the reporting and recognition requirement in the case of jointly controlled entities in(a) separate financial statement and (b) consolidated financial statements. Your answer is to be based on AS-27.

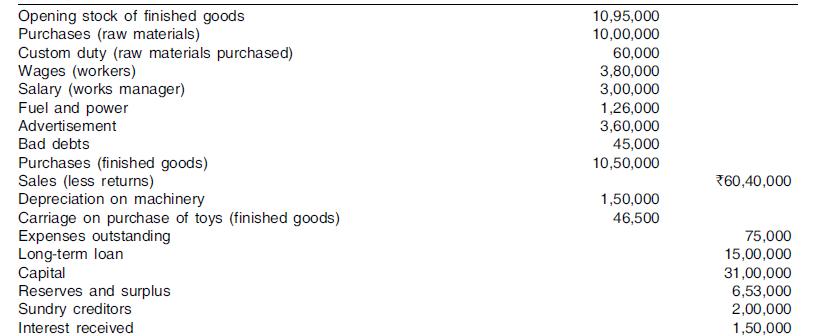

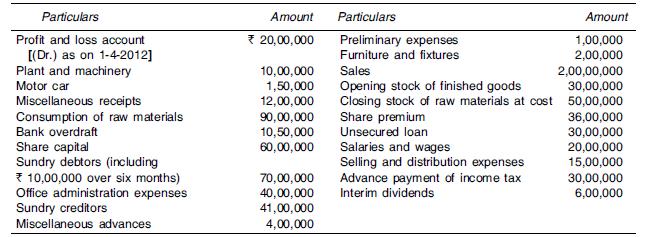

The following balances have been extracted from the books of X Ltd as on March 31, 2013:Additional Information:(i) Closing stock of finished goods at cost is ₹60,00,000.(ii) The original cost of fixed assets was: Plant and machinery ₹20,00,000; Furniture and fixtures ₹3,00,000; and Motor car

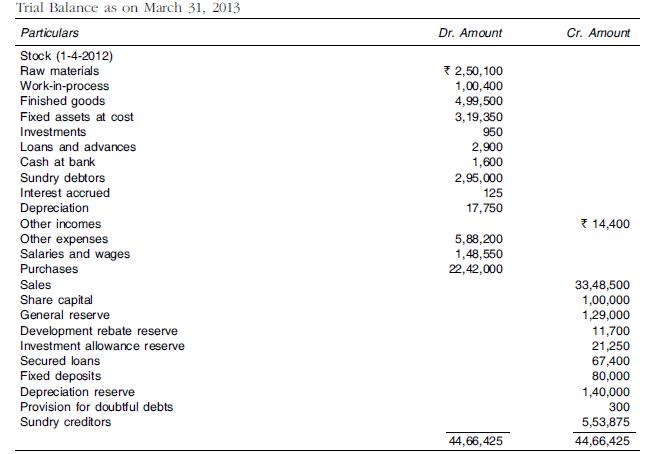

Given below is the Trial Balance (rounded off to rupees thousands) of Supreme Chemical limited as at the end of their financial year 2012–13 and additional information to be considered while preparing the final accounts which you are required to do in details. You may ignore the required format

Answer the following:(a) A company sold building for cash at ₹100 lakh. The profit and loss account has shown ₹40 lakh profit on sale of building. How will you report it in cash flow statement (based on AS-3)?(b) From the following information, determine cash received from debtors during

Showing 4400 - 4500

of 5025

First

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

Step by Step Answers