New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

engineering

derivatives principles and practice

Derivatives Principles And Practice 2nd Edition Rangarajan Sundaram - Solutions

The current value of an index is 585, while three-month futures on the index are quoted at 600. Suppose the (continuous) dividend yield on the index is 3% per year. (a) What is the implied repo rate? (b) Suppose it is possible for you to borrow at 6% for three months. Does this create any

If the spot price of IBM today is $75 and the six-month forward price is $76.89, then what is the implied repo rate assuming there are no dividends? Suppose the six-month borrowing rate in the money market is 4% p.a on a semiannual basis. Is there a repo arbitrage, and how would you construct a

A three-month forward contract on a non-dividend-paying asset is trading at $90, while the spot price is $84. (a) Calculate the implied repo rate. (b) Suppose it is possible for you to borrow at 8% for three months. Does this give rise to any arbitrage opportunities? Why or why not?

Suppose there is an active lease market for gold in which arbitrageurs can short or lend out gold at a lease rate of ℓ = 1%. Assume gold has no other costs/benefits of carry. Consider a three-month forward contract on gold. (a) If the spot price of gold is $360/oz and the three-month interest

Suppose the convenience yield is close to zero for maturities up to six months, then spikes up for the forward period between six and nine months, and then drops back to zero thereafter. What does the oil market seem to be saying about political conditions in the oil-producing countries?

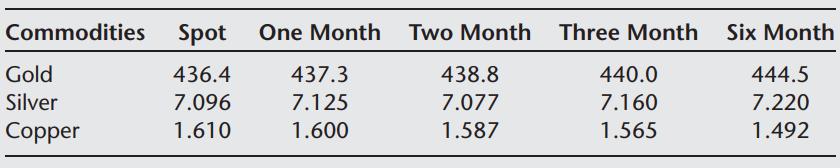

You are given the following information on forward prices (gold and silver prices are per oz, copper prices are per lb): (a) Which of these markets are normal? inverted? neither? (b) Which are in backwardation? in contango? (c) Which market appears prima facie to have the greatest convenience

Copper is currently trading at $1.28/lb. Suppose three-month interest rates are 4% and the convenience yield on copper is c = 3%. (a) What is the range of arbitrage-free forward prices possible using (b) What is the lowest value of c that will create the possibility of the market being in

Suppose that oil is currently trading at $38 a barrel. Assume that the interest rate is 3% for all maturities and that oil has a convenience yield of c. If there are no other carry costs, for what values of c can the oil market be in backwardation?

How do transactions costs affect the arbitrage-free price of a forward contract?

Does the presence of a convenience yield necessarily imply the forward market will be in backwardation? Why or why not?

What is the “implied repo rate”? Explain why it may be interpreted as a synthetic borrowing or lending rate.

Suppose an active lease market exists for a commodity with a lease rate ℓ expressed in annualized continuously compounded terms. Short-sellers can borrow the asset at this rate and investors who are long the asset can lend it out at this rate. Assume the commodity has no other cost of carry.

True or false: An arbitrage-free forward market can be in backwardation only if the benefits of carrying spot (dividends, convenience yields, etc.) exceed the costs (storage, insurance, etc.).

What is meant by the term “convenience yield”? How does it affect futures prices?

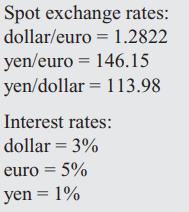

Consider three exchange rates, dollar/euro, yen/euro, and yen/dollar. Provided below are their spot FX rates and one-year interest rates (assume a continuous-compounding convention): (a) Check whether triangular arbitrage exists in the spot FX market. (b) Check whether triangular arbitrage exists

The three-month interest rates in the US and the UK are 3% and 6% in the respective money-market conventions. Suppose the three-month period has 91 days. The spot exchange rate is £1 = $1.83. What is the arbitrage-free three-month forward price of £ 1?

The spot exchange rate is $1.28/euro. The 270-day interest rate in the US is 3.50% and that on euros is 4%, both quoted using the money-market convention. What is the 270-day forward price of the euro?

The three-month interest rate in both the US and the UK is 12% in the respective money market conventions. Suppose the three-month period has 92 days. The spot exchange rate is £1 = $1.80. What is the arbitrage-free three-month forward price of £1?

The 181-day interest rate in the US is 4.50% and that on euros is 5%, both quoted using the money-market convention. What is the 181-day forward price of the euro in terms of the spot exchange rate S?

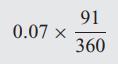

In the US, interest rates in the money market are quoted using an “Actual/360” convention. The word “Actual” refers to the actual number of days in the investment period. For example, if the interest rate for a three-month period is given to be 7% and the actual number of calendar days in

The current level of a stock index is 450. The dividend yield on the index is 4% per year (in continuously compounded terms), and the risk-free rate of interest is 8% for six-month investments. A six-month futures contract on the index is trading for 465. Identify the arbitrage opportunities in

The SPX index is currently trading at a value of $1265, and the FESX index (the Dow Jones EuroSTOXX Index of 50 stocks, subsequently referred to as “STOXX”) is trading at €3671. The dollar interest rate is 3% per year, and the Euro interest rate is 5% per year. The exchange rate is

The spot price of copper is $3.87 per lb, and the forward price for delivery in three months is $3.94 per lb. Suppose you can borrow and lend for three months at an interest rate of 6% (in annualized and continuously compounded terms). Assume you have no copper but can borrow it to short it if you

Consider a forward contract on a non-dividend-paying stock. If the term-structure of interest rates is flat (that is, interest rates for all maturities are the same), then the arbitragefree forward price is obviously increasing in the maturity of the forward contract (i.e., a longer-dated forward

Suppose you are given the following information: • The current price of copper is $383.50 per 100 lbs. • The term-structure is flat at 5%, i.e., the risk-free interest rate for borrowing/investment is 5% per year for all maturities in continuously compounded and annualized terms. • You can

A stock is trading at $24.50. The market consensus expectation is that it will pay a dividend of $0.50 in two months’ time. No other payouts are expected on the stock over the next three months. Assume interest rates are constant at 6% for all maturities. You enter into a long position to buy

An investor enters into a forward contract to sell a bond in three months’ time at $100. After one month, the bond price is $101.50. Suppose the term-structure of interest rates is flat with interest rates equal to 3% for all maturities. (a) Assuming no coupons are due on the bond over the next

Three months ago, an investor entered into a six-month forward contract to sell a stock. The delivery price agreed to was $55. Today, the stock is trading at $45. Suppose the three-month interest rate is 4.80% in continuously compounded terms. (a) Assuming the stock is not expected to pay any

Consider a three-month forward contract on pound sterling. Suppose the spot exchange rate is $1.40/£, the three-month interest rate on the dollar is 5%, and the three-month interest rate on the pound is 5.5%. If the forward price is given to be $1.41/£, identify whether there are any arbitrage

Suppose that the three-month interest rates in Norway and the US are, respectively, 8% and 4%. Suppose that the spot price of the Norwegian krone is $0.155. (a) Calculate the forward price for delivery in three months. (b) If the actual forward price is given to be $0.156, examine if there is an

Suppose that the current price of gold is $1,765 per oz and that gold may be stored costlessly. Suppose also that the term structure is flat with a continuously compounded rate of interest of 6% for all maturities. (a) Calculate the forward price of gold for delivery in three months. (b) Now

A security is currently trading at $97. It will pay a coupon of $5 in two months. No other payouts are expected in the next six months. (a) If the term structure is flat at 12%, what should be the forward price on the security for delivery in six months? (b) If the actual forward price is $92,

The forward price of wheat for delivery in three months is $7.90 per bushel, while the spot price is $7.60. The three-month interest rate in continuously compounded terms is 8% per annum. Is there an arbitrage opportunity in this market if wheat may be stored costlessly?

List the factors that could cause futures prices to deviate from forward prices. How important are these factors in general?

True or false: The theoretical (i.e., arbitrage-free) forward price decreases with maturity. That is, for example, the theoretical price of a three-month forward must be greater than the theoretical price of a six-month forward.

Briefly explain the basic principle underlying the pricing of forward contracts.

Give an example of a security that is not a derivative.

Derivatives may be used for both hedging and insurance. What is the difference in these two motives?

Define forward contract. Explain at what time cash flows are generated for this contract. How is settlement determined?

Explain who bears default risk in a forward contract.

What is the difference between value and payoff in the context of derivative securities?

What is a short position in a forward contract? Draw the payoff diagram for a short position at a forward price of $103 if the possible range of the underlying stock price is $50–150.

Forward prices may be derived using the notion of absence of arbitrage, and market efficiency is not necessary. What is the difference between these two concepts?

Suppose you are holding a stock position and wish to hedge it. What forward contract would you use, a long or a short? What option contract might you use? Compare the forward versus the option on the following three criteria: (a) Uncertainty of hedged position cash flow, (b) Up-front cash

What are the underlyings in the following derivative contracts? (a) A life insurance contract. (b) A home mortgage. (c) Employee stock options. (d) A rate lock in a home loan.

Assume you have a portfolio that contains stocks that track the market index. You now want to change this portfolio to be 20% in commodities and only 80% in the market index. How would you use derivatives to implement your strategy?

What are “delivery options” in a futures contract? Generally, why are delivery options provided to the short but not to the long position?

How do delivery options affect the relationship of futures prices to forward prices?

To what do the following terms refer: initial margin, maintenance margin, and variation margin?

What are price ticks?

Explain price limits and why they exist.

What are position limits in futures markets? Why do we need these? Are they effective for the objective you state, or can you think of better ways to achieve the objective?

What are the different ways in which futures contracts may be settled? Explain why these exist.

What is meant by open interest?

Discuss the liquidity and maturity of futures contracts.

Describe the standard bond in the Treasury Bond futures contract on the CBoT and the delivery option regarding coupons.

Suppose the delivered bond in the Treasury Bond futures contract has a remaining maturity of 20 years and a 7% coupon. Assume the last coupon was just paid. What is its conversion factor?

Suppose there are two deliverable bonds in the Treasury Bond futures contract, a 15-year 8% coupon bond and a 22-year 8% coupon bond. Assume the last coupon on both bonds was just paid. Which bond has the higher conversion factor?

What is meant by the “delivery grade” in a commodity futures contract? What is the problem with defining the delivery grade too narrowly?

Identify the main institutional differences between futures contracts and forward contracts.

Explain the term “delivery options.” What is the rationale for providing delivery options to the short position in futures contracts? What disadvantages for hedging are created by the presence of delivery options? For valuation?

What is the “closing out” of a position in futures markets? Why is closing out of contracts permitted in futures markets? Why is unilateral transfer or sale of the contract typically not allowed in forward markets?

An investor enters into a long position in 10 silver futures contracts at a futures price of $4.52/oz and closes out the position at a price of $4.46/oz. If one silver futures contract is for 5,000 ounces, what are the investor’s gains or losses?

What is the settlement price? The opening price? The closing price?

An investor enters into a short futures position in 10 contracts in gold at a futures price of $276.50 per oz. The size of one futures contract is 100 oz. The initial margin per contract is $1,500, and the maintenance margin is $1,100.(a) What is the initial size of the margin account? (b) Suppose

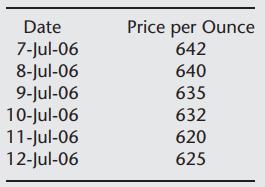

The current price of gold is $642 per troy ounce. Assume that you initiate a long position in 10 COMEX gold futures contracts at this price on 7-July-2006. The initial margin is 5% of the initial price of the futures, and the maintenance margin is 3% of the initial price. Assume the following

When is a futures market in “backwardation”? When is it in “contango”?

Suppose there are three deliverable bonds in a Treasury Bond futures contract whose current cash prices (for a face value of $100,000) and conversion factors are as follows: (a) Bond 1: Price $98,750. Conversion factor 0.9814. (b) Bond 2: Price $102,575. Conversion factor 1.018. (c) Bond 3:

You enter into a short crude oil futures contract at $43 per barrel. The initial margin is $3,375 and the maintenance margin is $2,500. One contract is for 1,000 barrels of oil. By how much do oil prices have to change before you receive a margin call?

You take a long futures contract on the S&P 500 when the futures price is 1,107.40, and close it out three days later at a futures price of 1,131.75. One futures contract is for 250 × the index. Ignoring interest, what are your losses/gains?

An investor enters into 10 short futures contracts on the Dow Jones Index at a futures price of 10,106. Each contract is for 10 × the index. The investor closes out five contracts when the futures price is 10,201, and the remaining five when it is 10,074. Ignoring interest on the margin account,

A bakery enters into 50 long wheat futures contracts on the CBoT at a futures price of $3.52/bushel. It closes out the contracts at maturity. The spot price at this time is $3.59/bushel. Ignoring interest, what are the bakery’s gains or losses from its futures position?

An oil refining company enters into 1,000 long one-month crude oil futures contracts on NYMEX at a futures price of $43 per barrel. At maturity of the contract, the company rolls half of its position forward into new one-month futures and closes the remaining half. At this point, the spot price of

Define the following terms in the context of futures markets: market orders, limit orders, spread orders, one-cancels-the-other orders.

Distinguish between market-if-touched orders and stop orders.

You have a commitment to supply 10,000 oz of gold to a customer in three months’ time at some specified price and are considering hedging the price risk that you face. In each of the following scenarios, describe the kind of order (market, limit, etc.) that you would use. (a) You are certain you

The spot price of oil is $75 a barrel. The volatility of oil prices is extremely high at present. You think you can take advantage of this by placing a limit order to buy futures at $70 and a limit order to sell futures at $80 per barrel. Explain when this strategy will work and when it will not.

The spread between May and September wheat futures is currently $0.06 per bushel. You expect this spread to widen to at least $0.10 per bushel. How would you use a spread order to bet on your view?

The spread between one-month and three-month crude oil futures is $3 per barrel. You expect this spread to narrow sharply. Explain how you would use a spread order given this outlook.

Suppose you anticipate a need for corn in three months’ time and are using corn futures to hedge the price risk that you face. How is the value of your position affected by a strengthening of the basis at maturity?

A short hedger is one who is short futures in order to hedge a spot cash-flow risk. A long hedger is similarly one who goes long futures to hedge an existing risk. How does a weakening of the basis affect the positions of short and long hedgers?

Suppose you deliver a grade other than the cheapest-to-deliver grade on a futures contract. Would the amount you receive (the conversion factor times the futures price) exceed, equal, or fall short of the spot price of the grade you deliver?

Showing 800 - 900

of 882

1

2

3

4

5

6

7

8

9

Step by Step Answers