New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

engineering

derivatives principles and practice

Derivatives Principles And Practice 2nd Edition Rangarajan Sundaram - Solutions

A European investor in the US equity markets wants to buy a quanto call on the S&P 500 index, where the strike is written in euros. (See the previous question for the definition of a quanto.) Can you explain why the investor wants such an option? Also explain what risks the investor is hedging by

Employee stock options have additional risk over and above standard call options in that the employee may not be able (or allowed) to cash in the option in the event of termination of the employee’s job with the firm if the option is not vested. But if the option is vested, so immediate exercise

Market timers are traders who vary their allocation between equity and bonds so as to optimize the performance of their portfolios by trading off one market versus the other. Rather than physically trade in the two markets, you want to avail yourself of the best return from the bond or stock

Draw the payoff diagram for the following portfolio of options, all with the same maturity: (a) Long a call at strike 75, (b) Long two calls at strike 80,(c) Long three calls at strike 85. What is the view of the stock price change consistent with this portfolio?

You are interested in creating the following gross payoff profile using an options portfolio:What options, at what strikes, would you hold in your portfolio? Assume that the desired payoffs are zero for any stock price less than 50 or greater than 160.

(Difficult) Using the principles of the previous question, create a spreadsheet-based algorithm to generate an option portfolio for any target gross payoff profile, such as the one in the previous question. Assume, as in the previous question, that option payoffs are provided for stock prices taken

You are managing a separate portfolio dedicated to your retirement income. You do not wish to take excessive risk, and would prefer to limit the downside. What common option structure would suffice?

What gross payoff profile do you get if you short a covered call position and go long a protective put position? Would you pay or receive net premiums on this position? What is the view taken on the movement of the stock price if you hold this position? What other options strategy does your

If you had a view opposite to that taken in the previous question, what portfolio structure of options would you choose?Data in Previous question.What gross payoff profile do you get if you short a covered call position and go long a protective put position? Would you pay or receive net premiums on

Microsoft is currently trading at $26. You expect that prices will increase but not rise above $28 per share. Options on Microsoft with strikes of $22.50, $25.00, $27.50, and $30.00 are available. What options portfolio would you construct from these options to incorporate your views?

Suppose your view in the previous question were instead that Microsoft’s shares will fall but a fall below $22 is unlikely. Now what strategy will you use?Data in Previous question.Microsoft is currently trading at $26. You expect that prices will increase but not rise above $28 per share.

Calls are available on IBM at strikes of 95, 100, and 105. Which should cost more, the 95–100 bullish vertical spread, or the 95–100–105 butterfly spread?

A bullish call spread is bullish on direction. Is it also bullish on volatility?

What is the directional view in a long put butterfly spread?

How would your answer to the previous question change if this butterfly spread were constructed using calls instead? Data in previous questionWhat is the directional view in a long put butterfly spread?

How does a horizontal spread exploit time-decay of options?

What is the volatility view implied by a long horizontal call spread? What about a short horizontal put spread?

Assume the current volatility of oil is high. What options portfolio offers you a gain from the high volatility if you do not have a view on direction?

You are planning to trade on the fortunes of a biotech firm that has a drug patent pending FDA approval. If the patent is approved, the stock price is expected to go up sharply. If it is not approved, the stock will drop sharply, In your view, it is unlikely to move more than 20% in either

Firm A is likely to be the target in a takeover attempt by Firm B. The stock price is likely to rise over the next few weeks as the takeover progresses, but if it fails, the stock price of A is likely to fall even more than the rise. What option strategy might exploit this information?

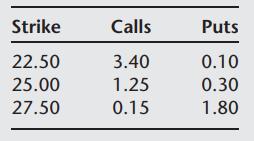

The options for Microsoft (stock price $25.84) are trading at the following prices: State the trading ranges at maturity in which the net payoff of the following option positions is positive: (a) 25.00 straddle, (b) 22.50 strip, (c) 27.50 strap,(d) 22.50– 27.50 Strangle.

What are collars? What is the investor’s objective when using a collar?

Is the price of a collar positive, zero, or negative?

Suppose options trade at two strikes: K1 < K2. You notice that whereas C(K2) − P(K2) = S − PV(K2) (put-call parity) holds for the K2 strike option, it does not hold for the K1 strike option, specifically C(K1) − P(K1) = S − PV(K1) + δ, where δ > 0. Show how you would use a box spread to

What is a ratio spread? Construct one to take advantage of the fact that you expect stock prices S to rise by about $10 from the current price but are not sure of the appreciation of more than $10.

Can the cost of a ratio spread be negative?

What is more expensive to buy: (a) A 100–110–120 butterfly spread using calls(b) A 90–100–110–120 condor? Can you decompose condors in any useful way?

If you are long futures and long a straddle, what is your view on direction? On volatility?

How would your answer to the previous question change if you were short futures instead?Previous question If you are long futures and long a straddle, what is your view on direction? On volatility?

If you take the view that volatility will drop over the next three months and then increase thereafter, what options strategy would you like to execute? Would the value of this portfolio today be positive or negative?

Compute the gross payoffs for the following two portfolios in separate tables: • Calls (strikes in parentheses): C(90) − 2C(100) + C(110). • Puts (strikes in parentheses): P(90) − 2P(100) + P(110).What is the relationship between the two portfolios? Can you explain why?

Draw the payoff diagrams at maturity for the following two portfolios: • A: Long a call at strike K and short a put at strike K, both options for the same maturity. • B: Long the stock plus a borrowing of the present value of the strike K. The payoff of this portfolio is the cash flow

What is meant by payout protection? Are options payout protected?

How does the payment of an unexpected dividend affect (a) Call prices.(b) Put prices?

As we have seen, options always have non-negative value. Give an example of a derivative whose value may become negative.

What are the upper and lower bounds on call option prices?

What are the upper and lower bounds on put option prices?

What is meant by the insurance value of an option? Describe how it may be measured.

What does the early-exercise premium measure?

What is meant by convexity of option prices in the strike price?

There are call and put options on ABC stock with strikes of 40 and 50. The 40-strike call is priced at $13, while the 50-strike put is at $12.8. What are the best bounds you can find for (a) The 40-strike put(b) The 50-strike call?

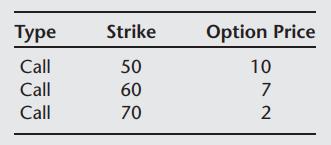

The following three call option prices are observed in the market, for XYZ stock: Are these prices free from arbitrage? How would you determine this? If they are incorrect, suggest a strategy that you might employ to make sure profits.

The current price of a stock is $60. The one-year call option on the stock at a strike of $60 is trading at $10. If the one-year rate of interest is 10%, is the call price free from arbitrage, assuming that the stock pays no dividends? What if the stock pays a dividend of $5 one day before the

The current price of ABC stock is $50. The term structure of interest rates (continuously compounded) is flat at 10%. What is the six-month forward price of the stock? Denote this as F. The six-month call price at strike F is equal to $8. The six-month put price at strike F is equal to $7. Explain

The prices of the following puts P(K) at strike K are given to you: The current stock price is $50. What is inconsistent about these prices? How would you create arbitrage profits?

The price of a three-month at-the-money call option on a stock at a price of $80 is currently $5. What is the maximum possible continuously compounded interest rate in the market for three-month maturity that is consistent with the absence of arbitrage?

The six-month continuously compounded rate of interest is 4%. The six-month forward price of stock KLM is 58. The stock pays no dividends. You are given that the price of a put option P(K) is $3. What is the maximum possible strike price K that is consistent with the absence of arbitrage?

(Difficult) Suppose there are five call options C(K), i.e.,{C(80), C(90), C(100), C(110), C(120)}. The prices of two of these are C(110) = 4, C(120) = 2. Find the best possible lower bound for the call option C(80).

In the previous problem, also find the minimum prices of C(90) and C(100). Previous problem(Difficult) Suppose there are five call options C(K), i.e.,{C(80), C(90), C(100), C(110), C(120)}. The prices of two of these are C(110) = 4, C(120) = 2. Find the best possible lower bound for the call

The one-year European put option at strike 100 (current stock price = 100) is quoted at $10. The two-year European put at the same strike is quoted at $4: The term structure of interest rates is flat at 10% (continuously compounded). Is this an arbitrage?

Given the following data, construct an arbitrage strategy: S = 100, K = 95, T = 1/2 year, D = 3 in three months, r = 0.05, and CE = 4.

Given the following data, construct an arbitrage strategy: S = 95, K = 100, T = 1/2 year, D = 3 in three months, r = 0.05, and PE = 4.

We are given that S = 100, K = 100, T = 1/4, r = 0.06, and CA = 1. Is there an arbitrage opportunity?

Given that there are two put options with strikes at 40 and 50, with prices 3 and 14, respectively, show the arbitrage opportunity if the option maturity is T and interest rates are r for this maturity.

Given the price of three calls, construct an arbitrage strategy: C(10) = 13, C(15) = 8, C(20) = 2.

A stock is trading at $100. The interest rate for one year is 5% continuously compounded. If a European call option on this stock at a strike of $99 is priced at $8.50, break down the call option value into (a) Instrinsic value. (b) Time value. (c) Insurance value.

Explain why a European call on a stock that pays no dividends is never exercised early. What would you do instead to eliminate the call option position?

Stock ABC pays no dividends. The current price of an American call on the stock at a strike of 41 is $4. The current stock price is $40. Compute the time value of the European put option if it is trading at a price of $3.

Stock XYZ is trading at a price of $105. The American-style call option on XYZ with maturity one year and strike 100 is traded in the market. The term structure of interest rates is flat at 1% and there is a dividend payment in six months of $8. What is the maximum insurance value for the call at

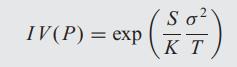

Assume that the true formula for pricing options is unknown, e.g., Black-Scholes is not applicable. Hence, you are asked to use the following approximation for the insurance value of a put option: Where S is the current price of the stock, K is the strike price, σ is the volatility of the stock

In the preceding question, refine the lower bound on the American put if there is a dividend to be received after three months of an amount of $2. Assume that the term structure is flat and the American call with dividends is worth $6.

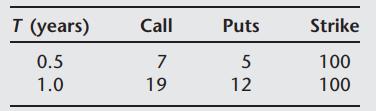

You observe the following European option prices in the OTC market on stock QWY, which does not pay dividends: However, the firm you work for does not subscribe to price quote services for the equity and interest rate markets. All you know is that the term structure of interest rates is flat. You

Stock KLM trades at $100 and pays no dividends. The one-year straddle struck at $102 is trading at a price of $10. The one-year interest rate is 2%. Find the price of the one-year European call and put.

An investor buys a call on ABC stock with a strike price of K and writes a put with the same strike price and maturity. Assuming the options are European and that there are no dividends expected during the life of the underlying, how much should such a portfolio cost?

In the binomial model, the up move of the stock is set by parameter u, i.e., the stock goes from S at the start of the period to uS at the end of the period if it moves up. Likewise, the down-move parameter for the stock is d. The value of 1 plus the interest rate is specified as R. What is the

Explain intuitively why the delta of a call will lie between zero and unity. When will it be close to zero? When will it be close to unity?

A stock is currently trading at 80. You hold a portfolio consisting of the following: (a) Long 100 units of stock. (b) Short 100 calls, each with a strike of 90. (c) Long 100 puts, each with a strike of 70. Suppose the delta of the 90-strike call is 0.45 while the delta of the 70-strike put is

(Difficult) Compare the replication of an option in a binomial model versus replication in a trinomial model by answering the following questions: (a) How many securities do we need to carry out replication in each model? (b) Is the risk-neutral probability defined in each model unique?

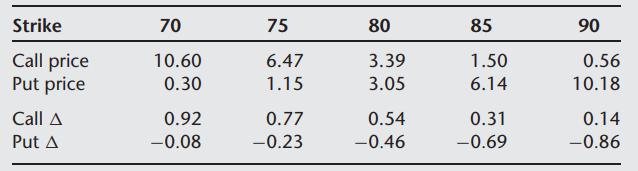

A stock is currenly trading at 80. There are one-month calls and puts on the stock with strike prices of 70, 75, 80, 85, and 90. The price and delta of each of these options are given below:For each of the following portfolios, identify (i) the current value of the portfolio, and (ii) the

ABC stock is currently trading at 100. In the next period, the price will either go up by 10% or down by 10%. The risk-free rate of interest over the period is 5%. (a) Construct a replicating portfolio to value a call option written today with a strike price of 100. What is the hedge ratio?(b)

ABC stock is currently at 100. In the next period, the price will either increase by 10% or decrease by 10%. The risk-free rate of return per period is 2%. Consider a call option on ABC stock with strike K = 100. (a) Set up a replicating portfolio to value the call. (b) Suppose the call is

ABC stock is currently at 100. In the next period, the price will either increase by 5% or decrease by 5%. The risk-free rate of return per period is 3%. Consider a put option on ABC stock with strike K = 100. (a) Set up a replicating portfolio to value the put. (b) Suppose the put is trading for

There are two stocks, A and B, both trading at price $20. Consider a one-period binomial model in which stock A’s price can go to either of {35, 5}. Stock B’s price can take one of the following values after one period: {36, 18}. An investment in $1.00 of bonds at the start of the period

The price of XYZ stock is currently at $100. After one period, the price will move to one of the following two values: {130, 80}. A $1.00 investment in the risk-free asset will return $1.05 at the end of the period. (a) Find the risk-neutral probabilities governing the movement of the stock

The current price of a stock is $50. The one-period rate of interest is 10%. The up-move parameter for the stock movement over one period is u = 1.5, and the down-move parameter is d = 0.5. (a) If the delta of the call at strike K is 0.5, what is the strike of this option? (b) What is the delta

(Difficult) The current price of a stock is $100. After one period, this stock may move to three possible values: {150, 110, 60}. The value of $1.00 invested in the risk-free asset compounds to a value of $1.05 in one period. Find the upper and lower bounds of the call price if its strike is $100.

Portfolio insurance: The current price of the stock we are holding is $100. We want to continue to hold the stock position but modify it so that the portfolio value never drops below $90. If the stock may move up to $130 or down to $80 after one period, how do we modify our holding of $100 so as to

What is a martingale measure? What is the role of the martingale measure in finance?

You are trying to hedge the sale of a forward contract on a security A. Suggest a framework you might use for making a choice between the following two hedging schemes: (a) Buy a futures contract B that is highly correlated with security A but trades very infrequently. Hence, the hedge may not be

You are planning to enter into a long forward hedge to offset a short forward position. If you choose a futures contract over a forward contract, which of the following circumstances do you want? (a) Do you want the term structure of interest rates (i.e., the plot of interest rates against

HoleSale Inc. USA exports manhole covers to Japan and Germany. Over the next six months, the company anticipates sales of 1,000 units to Japan and 500 units to Germany. The price of manhole covers is set at JPY 10,000 and EUR 80 in Japan and Germany, respectively. The following information is

You manage a portfolio of GM bonds and run a regression of your bond’s price changes on the changes in the S&P 500 index futures and changes in the 10-year Treasury note futures. The regression result is as follows: Where the regression above is in changes in index values for all the

Suppose you have the following information: ρ = 0.95, σS = 24, σF = 26, K = 90, R = 1.00018. What is the minimum-variance tailed hedge?

You use silver wire in manufacturing. You are looking to buy 100,000 oz of silver in three months’ time and need to hedge silver price changes over these three months. One COMEX silver futures contract is for 5,000 oz. You run a regression of daily silver spot price changes on silver futures

A US-based corporation has decided to make an investment in Sweden, for which it will require a sum of 100 million Swedish kronor (SEK) in three-months’ time. The company wishes to hedge changes in the US dollar (USD)-SEK exchange rate using forward contracts on either the euro (EUR) or the Swiss

You have a position in 200 shares of a technology stock with an annualized standard deviation of changes in the price of the stock of 30. Say that you want to hedge this position over a one-year horizon with a technology stock index. Suppose that the index value has an annual standard deviation of

Assume that the spot position comprises 1,000,000 units in the stock index. If the hedge ratio is 1.09, how many units of the futures contract are required to hedge this position?

Given the following information on the statistical properties of the spot and futures, compute the minimum-variance hedge ratio: σS = 0.2, σF = 0.25, ρ = 0.96.

The correlation between changes in the price of the underlying and a futures contract is +80%. The same underlying is correlated with another futures contract with a (negative) correlation of −85%. Which of the two contracts would you prefer for the minimum variance hedge?

If the correlation between spot and futures price changes is ρ = 0.8, what fraction of cash-flow uncertainty is removed by minimum-variance hedging?

In the presence of basis risk, is a one-for-one hedge, i.e., a hedge ratio of 1, always better than not hedging at all?

What is tailing the hedge in the context of minimum-variance hedging? Why does one tail the hedge?

How does one obtain the optimal hedge ratio from knowledge of daily price changes in spot and futures markets?

What is meant by basis risk?

You are given two stocks, A and B. Stock A has a beta of 1.5, and stock B has a beta of −0.25. The one-year risk-free rate is 2%. Both stocks currently trade at $10. Assume a CAPM model where the expected return on the stock market portfolio is 10% p.a. Stock A has an annual dividend yield of 1%,

Stock ABC is trading spot at a price of 40. The one-year forward quote for the stock is also 40. If the one-year interest rate is 4% and the borrowing cost for the stock is 2%, show how to construct a riskless arbitrage in this stock.

Redo the previous question if the interest rates for borrowing and lending are not equal, i.e. there is a bid-ask spread for the interest rates, which is 6 − 6.25%.Data in Previous questionYou are given information that the spot price of an asset is trading at a bid-ask quote of 80 − 80.5, and

You are given information that the spot price of an asset is trading at a bid-ask quote of 80 − 80.5, and the six-month interest rate is 6%. What is the bid-ask quote for the six-month forward on the asset if there are no dividends?

The spot US dollar-euro exchange rate is $1.10/euro. The one-year forward exchange rate is $1.0782/euro. If the one-year dollar interest rate is 3%, then what must be the one-year rate on the euro?

A three-month forward contract on an index is trading at 756, while the index itself is at 750. The three-month interest rate is 6%. (a) What is the implied dividend yield on the index? (b) You estimate the dividend yield to be 1% over the next three months. Is there an arbitrage opportunity from

Showing 700 - 800

of 882

1

2

3

4

5

6

7

8

9

Step by Step Answers