New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

engineering

derivatives principles and practice

Derivatives Principles And Practice 2nd Edition Rangarajan Sundaram - Solutions

You are able to borrow on a floating basis at a rate of Libor + 100 bps for two years. In addition, you can contract on a 6 × 12 FRA in which you can exchange Libor for a fixed rate of 3%. Similarly, you can contract on a 12 × 18 FRA at 3.5% and the 18 × 24 FRA at 4%. Assume the money market

You have an FRA to borrow at 5% that has six months to run until maturity and is for the period (6,12) containing 183 days. The current forward rate for the period (6,12) is 5.2%. What is the mark-to-market value of the FRA? What is the PVBP of this contract? Explain the sign of the PVBP. Assume

What is the price of a five-year floating-rate note that has coupons at the rate of Libor + 100 bps when the current yield curve is flat at 6%? Assume that the conventions in the market are 30/360 for coupons and discounting instead of the usual Actual/360.

Two firms X and Y are able to borrow funds as follows: A: Fixed-rate funding at 4% and floating rate at Libor − 1%. B: Fixed-rate funding at 5% and floating rate at Libor + 1%. Show how these two firms can both obtain cheaper financing using a swap. What swap would you suggest to the two firms

Firm A can borrow fixed rate at 10%. It can also borrow floating at Libor + 1%. The market swap rate at the bid is Libor versus 8.9% and is Libor versus 9.1% at the ask (i.e., the firm can enter into a swap by paying fixed at 9.1% or receiving at 8.9%). Find the cheapest form of financing for the

The student loan association raises floating-rate financing and makes loans of maturity 5–10 years at fixed rates. Can you describe the nature of the risks on the balance sheet? What financial contract should the association undertake to mitigate these risks?

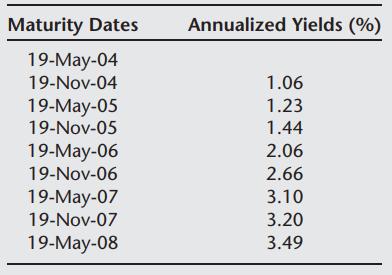

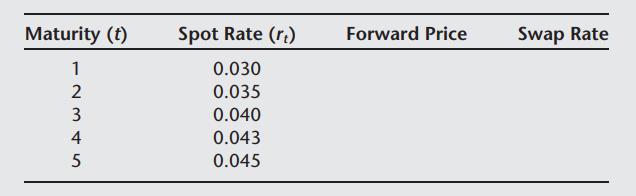

You are given the following data on Libor yields at six monthly intervals. The current date is 19-May-04. All swaps in this question have a four-year maturity and a notional principal of 100,000. Assume the fixed-rate side of the swap is on a 30/360 basis, and the floating side is on an Actual/360

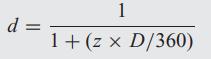

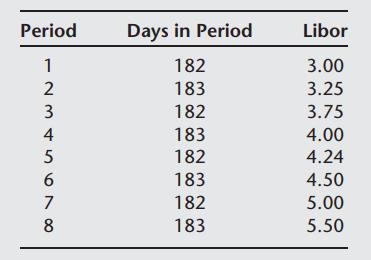

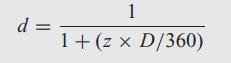

You are given the following table for the next eight half-year periods. The zero-coupon rates are converted into discount factors with the following formula: Where z is the zero-coupon rate and D is the number of days to the payment from inception. Find the fixed rate at which a four-year swap

Who bears more credit risk in a five-year fixed-for-floating interest rate swap when the yield curve is upward sloping, the fixed rate payer or receiver? Assume that both parties have the same credit quality.

How would you hedge a portfolio of swaps using zero-coupon swaps? Explain the logic you would follow to set up the appropriate set of swaps.

There is a cash flow of $125 at time 1.68 years to be allocated to two time points: 1.5 years and 2 years. The zero-coupon rates for these two points are 3% and 4%, and compounding is continuous. Find the allocation that preserves value and risk.

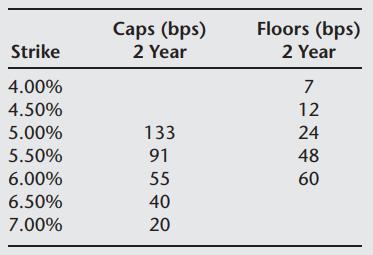

Major investor IwanItall has a portfolio of 100 million USD two-year semiannual floating-rate notes, based on six-month Libor. This is a standard floating-rate note with coupons being set every six months. He wants to ensure that he receives a minimum Libor yield of 6.00% in the future. The current

An inverse floater is a security that is an FRN where the coupon rate varies inversely to the indexed rate. An example of an inverse floater is as follows. Consider a three-year semiannual pay FRN where the coupon rate equals: Where ℓ is the six-month Libor rate. The further condition on this

Describe the standard features of an equity swap contract. What are the differences between an equity swap and an interest rate swap?

If you were a fund manager with special expertise in the mortgage markets but were advertising yourself as an equity index fund, explain how you might be able to generate extra returns (alpha) for the fund from your expertise in mortgage trading.

A market timer switches between stock and cash (i.e., Libor) depending on which market is expected to perform better. If you are a market-timing investment manager, explain how you would use equity swaps to time the market.

Why are cash flows from equity swaps more volatile than from interest rate swaps?

What is the interest-rate sensitivity of an equity-for-Libor swap?

How would you synthesize an equity swap using bonds and futures?

State one example of a case when you would want to implement (a) A fixed interest rate versus equity swap. (b) A floating interest rate versus equity swap.

Explain why, in a floating interest rate versus equity swap with a fixed notional principal, all cash flows on the equity side of the swap after the next settlement date have no risk.

Suggest two different ways in which equity swaps are useful to traders and hedgers.

A plain vanilla equity swap comprises the exchange of equity return for the return stipulated by Libor. What particular types of risk are borne by the parties to the contract?

On a $100,000 notional equity swap contract, your firm is the receiver of equity return and the payer of Libor interest. The swap is settled every half year. At the end of the current six-month interval, the equity had appreciated over the past half year by 7.6%, and the six-month Libor rate was

If you anticipate that the equity market will beat the bond market for the next five years, what swap would you find attractive to contract upon?

Assuming that you anticipate that the equity markets will outperform the bond markets in the period three years from today for another three years, what swap is appropriate?

You wish to implement a life cycle investment plan in your retirement portfolio using a special equity swap. Currently, your portfolio comprises 100% equities. Your financial advisor has suggested that over time you slowly move your money into less risky instruments, so that over the life cycle you

Suppose you wish to maintain a portfolio that is exactly 80% in equities and 20% in cash at the end of each quarter. What equity swap structure will enable you to do this?

You currently own a portfolio that is invested in broad equities and is worth $120,000. You wish to diversify some of the equity risk going forward and maintain a portfolio that is only 70% equity and 30% cash (Libor) for the next three years. Hence, you add a variable notional equity swap to the

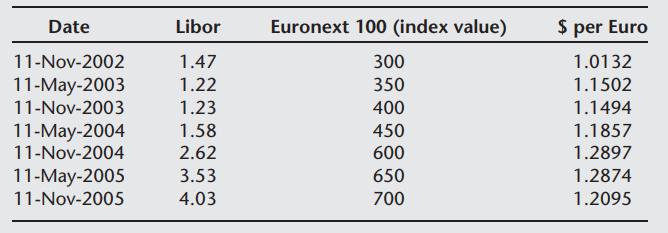

You are the asset manager for an international fund. Suppose you enter into an unhedged currency swap in which you receive the return on the Euronext 100 index and pay the Libor rate. The swap is on a half yearly basis for three years and is unhedged, i.e., payments will reflect current exchange

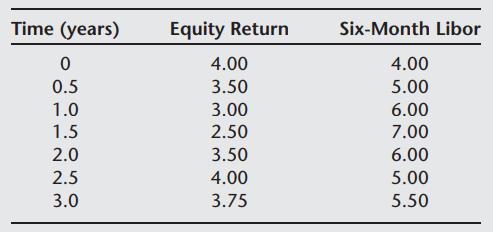

Consider a five-year semiannual pay fixed notional equity swap in which you receive Libor and pay the equity index return. The current period is of 182 days, and the swap has run exactly 91 days into the period. The six-month Libor rate on the previous reset was 7% and the equity index was at 1050.

What is covered interest-rate parity?

If the US dollar is trading at a discount to the yen in the forward currency markets, what can you say about the relationship of the dollar and yen interest rates?

If the yen/dollar exchange rate is 130 and the dollar/euro rate is 1.20, what is the yen/euro exchange rate?

As a currency trader, what would you do to your quoted foreign exchange rates in the $/€ market if you wanted to sell down your position in euros? Assume that the current bid-ask in $/€ is 1.20–1.25.

In the previous question, what do you do to the bid-ask spread to induce more trading volume in your $/€ currency book?Data in previous question,As a currency trader, what would you do to your quoted foreign exchange rates in the $/€ market if you wanted to sell down your position in euros?

If the spot $/€ rate is 1.20 and the interest rates are r$ = 0.03 and r€ = 0.05 for T = 1 year (in continuously compounded terms), then what are the forward points for one year?

What is more appropriate to use to hedge a borrowing in euros for two years: a currency forward or a currency swap?

What type of commodity swap is ideal for a hedge fund that invests heavily in commodities if it wishes to diversify into the equities market?

The gas-electricity swap is one that receives the return on electricity prices and pays the return on natural gas prices. What business entity does this swap mimic?

Explain how you would construct multiple maturity forward contracts in oil if all you could trade were oil-equity swaps (i.e., a swap in which you exchange the return on oil prices for the equity index return) and stock market futures.

The spot exchange rate between the euro and the dollar is $1.2/€. If the dollar interest rate is 2% for two years, the euro rate is 3% for the same maturity, and both rates are annually compounded, what is the two-year forward FX rate?

In the previous question, if rates are continuously compounded and the forward exchange rate is $1.10/€, then what is the interest differential between the two currencies?Data in previous question,The spot exchange rate between the euro and the dollar is $1.2/€. If the dollar interest rate is

Using the forward FX curve from the preceding problem, convert an annual five-year stream of 75 basis points received in dollars into a similar stream received in euros. You need to express your answer in a number of euro basis points.Data in preceding problemIn the preceding problem, suppose you

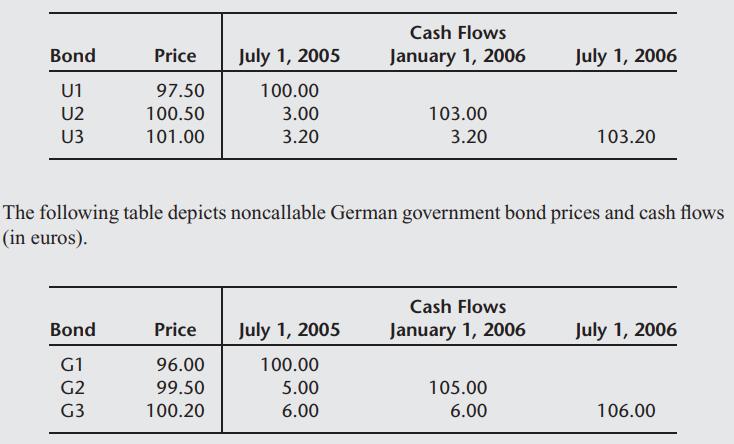

The following is a table of noncallable US government bond prices and cash flows (in US dollars, i.e., $). Assume that the current date is January 1, 2005. The spot exchange (FX) rate today is $1.5/€. Find the forward FX rates for the next three half-year maturities.

The following table presents the spot rates from the risk-free interest-rate market. The spot price of gold is $425 per ounce. If the storage cost of gold is 0.15% per year and the convenience yields are flat at 1% per year, complete the table below for forward prices of gold and commodity swap

Keeping all other parameters the same, if the dividend rate on the stock increases, which option depreciates less, the American call or the European call? Why?

What condition is required on the movement of stock prices for the binomial tree to be recombining?

Why does the payment of dividends usually render the binomial tree into a nonrecombining one? What type of dividends causes the failure of recombination? What type of dividends does not?

Holding all else constant, if dividends increase, does the difference between American calls and puts increase or decrease? Why? What about the difference between European calls and puts?

How would you know from examining the risk-neutral probabilities on a binomial tree if the model is free from arbitrage?

Explain what is meant by a “self-financing” replicating strategy.

Suppose we used a trinomial tree with three replicating securities instead of a binomial tree with two securities. Would the dynamic replication be “self-financing”?

Suppose you have two states of the world and two assets. The prices of both assets in each of the two states are known. What conditions are needed for a derivative security that is a function of the two assets to be replicable?

The initial stock price is $100. The stock moves up each period by a factor of 1.3 and down by a factor of 0.8. If the simple interest rate per period is 1%, what is the risk-neutral probability of an up move in the stock price? Draw the stock price tree for three periods and find the price of a

The initial stock price is $100. The stock moves up each period by a factor of 1.3 and down by a factor of 0.8. If the simple interest rate per period is 1%, find the prices of three-period European and American puts, and so identify the early exercise premium amount.

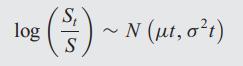

Suppose the distribution of St is given to be lognormal:Where μ = 0.10 and σ = 0.20. Given that S = 60, calculate 95% confidence intervals for the price of St three months from today.

Repeat Question 1 with μ = 0.10 and σ = 0.10. Data in Repeat QuestionSuppose the distribution of St is given to be lognormal:Where μ = 0.10 and σ = 0.20. Given that S = 60, calculate 95% confidence intervals for the price of St three months from today.

Suppose you wish to approximate the distribution of a stock price three months from now using a binomial tree with 100 steps. Suppose also that the stock price distribution is given to be lognormal with μ = 0.04 and σ = 0.40. What values would you use for the parameters of the binomial model?

Repeat Question 3 but with μ = 0.20 and σ = 0.20. Repeat Question 3Suppose you wish to approximate the distribution of a stock price three months from now using a binomial tree with 100 steps. Suppose also that the stock price distribution is given to be lognormal with μ = 0.04 and σ = 0.40.

Suppose the price St of a stock follows a lognormal distribution with μ = 0.07 and σ = 0.30. What are the expected simple returns on the stock over a three-month horizon?

Assume the S&P 500 index follows a lognormal distribution with a volatility of 25%. Suppose the expected simple returns on the index over a one-year horizon are 8%. What is the value μ of the annual expected log-return?

If the continuously compounded return on a stock is normal, then why is the stock price distribution lognormal?

If the continuously compounded return on a stock worth $1 currently for a preset interval of time is distributed normally as follows: r ∼ N(μ, σ2) ≡ N(0.1, 0.22), then what are (a) The expected price of the stock after one interval. (b) The variance of the stock price?

(Technical) Suppose that the continuously compounded returns in each period are normal but are not always independent from period to period. Will the final stock price after all periods be lognormal?

(Technical) In binomial tree models, as we shrink the time interval on the tree, will the final return distribution of the stock price always converge to the normal distribution?

For a binomial tree with the probability of 0.01 of an outcome of 1 and a probability of 0.99 of an outcome of 0, what are the mean and variance of the payoff?

Suppose the annualized volatility of a stock is σ = 0.30. The mean return is μ = 0.10. The risk-free rate is constant for all maturities at 2%. Letting the time interval h increase in monthly increments (1/12 of a year), how does the risk-neutral probability of an up move in the stock price

If the standard deviation of daily stock returns is 2%, what is the volatility of annual stock returns?

You are constructing a 100-period binomial tree to represent a 91-day (≈ 0.2493-year) horizon. The risk-free rate for the given horizon is 4% in annualized continuously compounded terms. The underlying asset has a volatility of 38%. What are the parameters of the binomial tree if you use the JR

Derive the risk-neutral probability in the JR model using general algebra. Is the probability exactly 1/2 ?

This problem will require a spreadsheet or programming effort. The initial stock price is given to be $100. We wish to price European calls and puts with strike price $100. The option maturity is T = 1 year, and the risk-free rate of interest is 5% per annum. If the volatility is σ = 0.40, then

You are given the following parameter values and are required to price calls using both the JR model and the CRR model for different values of n, the number of periods on the tree. The given values are S = 100, K = 100, T = 1, σ = 0.4, and r = 0.05. For varying values of n, running from 5 to 100,

Is it possible to build a recombining tree if the interest rate is not constant, nor stochastic, but a deterministic function of time, i.e., r(t)?

Explain why the Black-Scholes model is inappropriate if the stock can gap.

Is assuming a constant (nonstochastic) interest rate in the Black-Scholes model a major deficiency of the model?

The Black-Scholes model assumes constant volatility. How serious a shortcoming is this?

Compute the three-month (T = 1/4) forward price F of a stock currently trading at $40 when the risk-free rate for this period is r = 4%. Then, set the strike price K = F and calculate call and put values from the Black-Scholes model if the volatility is σ = 0.4, assuming the stock pays no

(We repeat the previous question allowing for nonzero dividends.) Assume a stock has a dividend yield of d = 2%. Compute the three-month (T = 1/4) forward price F of a stock currently trading at $40 when the risk-free rate for this period is r = 4%. Then, set the strike price K = F and calculate

Plot the price of a Black-Scholes call for a range of volatility from 5% to 40%. Use the following parameters: S = 30, K = 33, T = 1/3, r = 0.03, and d = 0. Does the function appear concave or convex?

Plot the price of a Black-Scholes call for declining maturity from three years to zero years. Does the function appear concave or convex? Use the following parameters: S = 30, K = 33, σ = 0.3, r = 0.03, and d = 0.

Plot the price of a Black-Scholes call for a range of interest rates from 1% to 20%. Use the following parameters: S = 30, K = 33, T = 3, σ = 0.3, and d = 0.

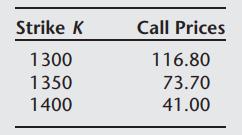

On December 1, the S&P 500 index (SPX) is trading at 1396.71. The prices of call options on the index expiring on March 16 (i.e., in a bit over three months) are as follows: Assuming the interest rate for that period is 4.88% and the annual dividend rate on the SPX is 1.5%, compute the implied

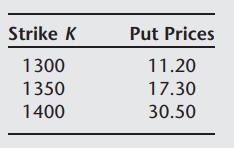

(Repeat for puts) On December 1, the S&P 500 index (SPX) is trading at 1396.71. The prices of put options on the index expiring on March 16 (i.e., a little over three months) are as follows: Assuming the interest rate for that period is 4.88%, and the annual dividend rate on the SPX is 1.5%,

Show that the delta of an at-the-money European call option in the Black-Scholes model is at least 1/2. What about the delta of an at-the-money put?

What happens to the delta of an at-the-money call as the time-to-maturity declines? What about a put?

Let S = K = 100, σ = 0.25, and T − t = 1 month. Create a spreadsheet to value a call and a put for the following values of r: (a) R = 0.08. (b) R = 0.06. (c) R = 0.04.

Microsoft stock is currently trading at $24.35. Consider call and put options with a strike of $25.00 expiring in 12 trading days (= 0.0476 years). Suppose that the volatility of Microsoft stock is 40% and that the interest rate is 3%. What are the Black-Scholes prices of the call and the put? What

GE stock is currently trading at $26.15. A call option with a strike of $25.00 and 12 trading days (= 0.0476 years) to expiry costs $1.56. Assuming an interest rate of 3%, what is the implied volatility?

The S&P 500 index is currently at 1101. A call option with a strike of 1075 and 17 trading days (= 0.067 years) to maturity costs 36.20. Assume an interest rate of 3%. For simplicity, assume also that the dividend yield on the index is zero.(a) What is the implied volatility? (b) If implied

The spot USD-EUR exchange rate is USD1.24/EUR. Consider a one-month (= 0.083 years) put option on the EUR with a strike of USD1.25/EUR. Assume that the volatility of the exchange rate is 12%, the one-month interest rate on the USD is 3.1%, and the one-month interest rate on the EUR is 3.7%, both in

The spot USD-EUR exchange rate is USD1.50/EUR. Consider a six-month (= 0.5 years) call option on the EUR with a strike of USD1.50/EUR. Suppose the volatility of the exchange rate is 20%, the six-month interest rate on the USD is 1.5%, and the six-month interest rate on the EUR is 2.5%, both in

A stock index is currently at 858. A call option with a strike of 850 and 17 days (= 0.047 years) to maturity costs 23.50. Assume an interest rate of 3%. For simplicity, assume also that the dividend yield on the index is zero. (a) What is the implied volatility? (b) If implied volatility went up

If xt = at + bWt where Wt is a Wiener process and W0 = 0, then write down the equation in differential form.

If xt = at + bWt , and y = ex (time subscripts suppressed), what is the differential process for y?

In the previous question, what is the expected value of y at time t? Data in previous questionIf xt = at + bWt , and y = ex (time subscripts suppressed), what is the differential process for y?

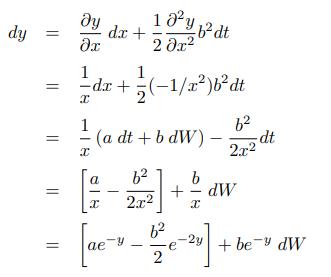

If dx = a dt + b dW and y = ln(x), find dy.

Show that, in the Black-Scholes model, stock prices are lognormal.

(Requires Numerical Analysis) (a) Write down the probability density function of the risk-neutral terminal distribution of returns for stocks in the Black-Scholes model. (b) Then write down the expression for the value of a call option on a stock in integral (expectation) form under the

Consider the usual Black-Scholes setting: Suppose we have μ = 0.20 and σ = 0.40. What is the expected value of the stock price after two years if the current price is $100? What is the standard deviation of the stock price value after two years?

Showing 500 - 600

of 882

1

2

3

4

5

6

7

8

9

Step by Step Answers