New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

engineering

derivatives principles and practice

Derivatives Principles And Practice 2nd Edition Rangarajan Sundaram - Solutions

From the solution to the preceding question what can you say about the instantaneous volatility of a put option when the stock price increases?

Intuitively, by inspection, in relation to the previous questions, what is the formula for the volatility of a call? Does the volatility of a call increase or decrease as the stock price increases?Data in previous questions.From the solution to the preceding question what can you say about the

In this chapter, we developed the following approaches to solving the option pricing problem: (a) The PDE approach: In this method, we found that the call option value was the solution to the following differential equation: (b) The risk-neutral approach: In this method, we solved for the option

Suppose the beta of a stock is 1.2, and the stock price is S = 40. Let the volatility be σ = 0.4, the risk-free rate be r = 0.04, and assume no dividends are paid. What is the beta of a put option with maturity one year and strike K = 40?

(Cash-or-Nothing Option) What is the value of an option that pays $100 if the stock price exceeds a prespecified strike at maturity? Assume that the initial stock price is $100, maturity is one year, volatility is 50%, and the strike is $110. Assume also that the risk-free rate of interest is zero.

(Corridor Options) What is the price of an option that has a maturity of 60 days and pays $1 for each day that the stock price lies in the range (50,60)? The current stock price is S = 55, volatility σ = 0.4, interest rate r = 0.03, and dividends d = 0.

What are the shortcomings of the geometric Brownian motion for stock prices that underlies the Black-Scholes option pricing model? For each deficiency, state what modification to the model is likely to provide an improvement.

(Difficult) In a jump model for returns, what determines the skewness and kurtosis of the statistical distribution?

In a model of stock returns with geometric Brownian motion, where the volatility is assumed to be stochastic, what determines the type of skewness that emerges? What determines the kurtosis?

(Very Difficult) Suppose you want to model stock returns r as being driven purely by jumps. The jumps arrive at rate λ = 0.1 per time interval. When they do arise, they are normally distributed with mean μ = −0.05 and variance γ2 = 0.502. What is the variance, skewness, and kurtosis of returns?

What is the option smile? Why does it arise from fat-tailed stock return distributions?

Suppose the S&P index options demonstrate a left-skewed smile. You are an options trader and believe that the smile is steeper than it should be because the market has overestimated the extent of crash risk. You believe that the market will correct its view within the next month. What options

(Requires Writing Code) Using the following parameters, price call options for a range of seven strike prices with the Merton jump model. Now with the seven option prices (one for each strike price), find out what the implied volatility is in the Black-Scholes model. You will need to write program

(a) What happens empirically to the option smile with increasing maturity? (b) How is the smirk typically different from the smile? (c) Which markets are characterized by smiles, and which ones display smirks? (d) What is the volatility surface?

What is the leverage effect? How does it impact option prices? How would you account for the leverage effect in a stochastic volatility equity option model? In a jump-diffusion model?

State at least three reasons why the Black-Scholes model has warranted extension in the past decades. What is the impact of these extensions on the stock return distribution. What impact does this have on the prices of calls and puts?

In the jump-diffusion model, what parameter needs to be set to develop a sharp negative smirk (asymmetric skew)? What is your answer to this question in the case of the stochastic volatility model?

One of the early extensions to the Black-Scholes model was the constant elasticity of variance (CEV) model for equities. The CEV model assumes the following form of stochastic process for the stock price: where the parameters are defined as usual except that 0 (a) What parameter value for β

Why is the gamma of an ATM option that is about to expire large in magnitude?

If the delta of a European call is 0.6, what is the delta of the European put for the same strike and maturity?

Can you derive the delta of a European call from the delta of the corresponding European put with no knowledge of the strike price?

Is it possible to determine the strike price of a pair of a call and a put on the same stock with the same strike if you know the deltas of both the call and the put? Assume the options are European.

If the gamma of a European call is 0.03, what is the gamma of the corresponding European put at the same strike and maturity?

In the Black-Scholes model, what is higher, the delta of a one-year call or that of a two-year call on the same stock if the respective strikes are at-the-money forward? Show the result algebraically and then discuss the intuition.

Does your answer to the preceding question change if the call is deep out-of-the-money (OTM)? What about if it is deep in-the-money (ITM)?

In the Black-Scholes model, how does the delta of an ATM call change as volatility increases?

Intuitively speaking, how does the delta of a deep OTM call change as volatility increases?

For an at-the-money-forward (ATMF) call in the Black-Scholes model, how does ΔC change when interest rates rise?

Intuitively speaking, how does the delta of a put (at fixed strike) change when interest rates rise?

How does the gamma of an OTM option behave as we approach maturity? What about the gamma of an ITM option? Derive the answers in the context of the Black-Scholes model and explain the intuition.

How does the vega of an OTM option behave as we approach maturity? What about the vega of an ITM option? Derive the answers in the context of the Black-Scholes model and explain the intuition.

Gamma is often thought of as representing a view on volatility, while vega measures the dollar impact on option values of a change in volatility. Do they measure the same thing? Is it possible for gamma to increase and vega to decrease simultaneously?

You hold a portfolio that is short 2,000 puts, each with a delta of −0.63. What would you do to delta-hedge the portfolio?

A stock has a volatility of 40%. An at-the-money call on the stock has a vega of +21.45. By how much will the call value change if volatility falls to 39%? Assuming the options are European, what about the corresponding put?

The theta of a put with 23 days left to maturity is −17.50. Other things being equal, by how much does the value of the put change if a day passes?

You hold two types of calls and two types of puts on a given stock. The deltas and gammas of the respective types are (+0.40, +0.03), (+0.55, +0.036), (−0.63, +0.028), and (−0.40, +0.032). You have a long position in 1,000 of the first type of call, a short position in 500 of the second type of

You hold a portfolio that is short 800 calls, each with a rho of +21.50, and long 800 puts, each with a rho of −16.70. By how much does your portfolio value change if interest rates move down by 20 basis points?

A stock is currently trading at $22.50. The delta of an at-the-money call on the stock is +0.56 and the gamma is +0.035. If the stock price were to change to $22.25, by how much would the call price change (using the delta alone)? What is the approximate new value of the call delta?

What is the sign of the delta of a call option on a put option? Why? What about a put on a call?

Why does a call on a put cost less than the put?

Consider a digital call option, i.e., one that pays a dollar if at maturity the stock price ST is greater than the strike K. (a) What is the sign of the delta of this option? (b) When will the delta of this option be the highest?

Are ordinary American-style options path-independent?

Consider a stock with current price S = 50 whose price process can be represented by a binomial tree with parameters u = 1.221 and d = 0.819. Suppose the per-period gross interest rate is R = 1.005. (a) Find the value of a two-period European put option with a strike of K = 50. (b) Using

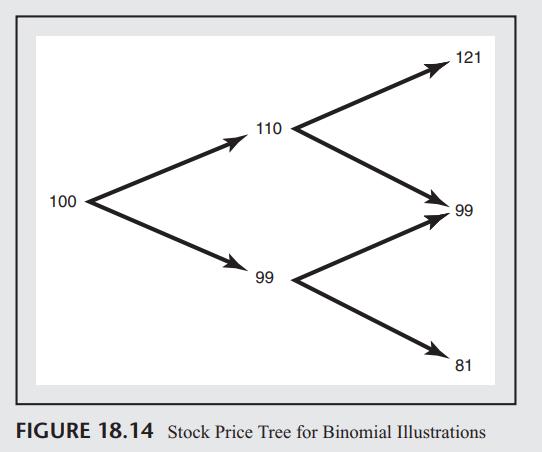

Consider the binomial tree of Figure 18.14. Suppose that the per-period interest rate is R = 1.02.(a) Show that the price of a call on a put in this model with a strike of k = 4 and a maturity of one period is 1.58, where the underlying put has a strike of 100 and a maturity of 2 periods. (b) Show

Describe a put-call parity relationship for compound options, i.e., one that connects calls-on-calls to puts-on-calls (or calls-on-puts to puts-on-puts).

Price a chooser option using the Black-Scholes formula with the following inputs: S = 100, K = 100, the choice date on which the holder has to opt for a call or a put is τ = 1 year, the final maturity of the option is T = 2 years, volatility is 30%, the risk-free rate is r = 0.10, and the dividend

Consider an option that pays the holder the amount At maturity where ST is the terminal price of the stock and K the option’s strike price. Such an option is one example of a power option. Consider a binomial tree with initial stock price S = 60 and parameters u = 1.20 and d = 0.833. Suppose the

A corridor option is one that pays a fixed sum M if the price at maturity lies between two specified levels K1 and K2 but nothing otherwise. Consider a two-period binomial tree with parameters u = 1.10 and d = 0.91. Suppose the initial stock price is S = 100 and r = 1.01. (a) Find the initial

Find a closed-form expression for the price of a corridor option in a Black-Scholes setting.

Given the following parameters, price a gap call option: S = 100, K = 100, T = 1, σ = 0.3,r = 0.10, and M = 90. Dividends are δ = 0.02. Remember, K is the strike price of both calls, and M is the payoff for the cash-or-nothing call if it finishes in the money.

What is the value of a one-year option on the maximum of two assets when both assets are trading at $100 each, their volatilities are 50% and 40%, and the correlation between their returns is +0.30? Both assets pay no dividends.

What is the value of a one-year option on the maximum of two assets when both assets are trading at $100 each, their volatilities are 50% and 40%, and the correlation between their returns is −0.30? Both assets pay no dividends. Compare the value against the case where the correlation is positive

What is the value of a one-year option on the minimum of two assets when both assets are trading at $100 each, their volatilities are 50% and 40%, and the correlation between their returns is +0.30? Both assets pay no dividends.

Explain the difference between the following terms: (a) Payoff to an FRA. (b) Price of an FRA. (c) Value of an FRA

What characteristic of the eurodollar futures contract enabled it to overcome the settlement obstacles with its predecessors?

How are eurodollar futures quoted?

It is currently May. What is the relation between the observed eurodollar futures price of 96.32 for the November maturity and the rate of interest that is locked-in using the contract? Over what period does this rate apply?

What is the price tick in the eurodollar futures contract? To what price move does this correspond?

What are the gains or losses to a short position in a eurodollar futures contract from a 0.01 increase in the futures price?

You enter into a long eurodollar futures contract at a price of 94.59 and exit the contract a week later at a price of 94.23. What is your dollar gain or loss on this position?

What is the cheapest to deliver in a Treasury bond futures contract? Are there other delivery options in this contract?

Describe the standard bond in each of the following contracts: (a) Treasury bond futures, (b) 10-year Treasury note futures, (c) 5-year Treasury note futures, (d) Treasury bill futures.

Describe the conversion factor that applies if the delivered bond in a Treasury bond futures contract is different from the standard bond.

Explain the notion of duration of a bond. Under what conditions is this measure reasonably accurate?

Explain the principles involved in duration-based hedging. How does the computation of the hedge ratio here differ from that of the minimum-variance hedge computation?

On a $1,000,000 principal, 91-day investment, what is the interest payable if we use an Actual/365 basis? What is the interest if the basis is Actual/360?

If the six-month interest rate is 6% and the one-year interest rate is 8%, what is the rate for an FRA over the period from six months to one year? Assume that the number of days up to six months is 182 and from six months to one year is 183.

If the three-month (91 days) Libor rate is 4% and the six-month (183 days) rate is 5%, what should be the 3 × 6 FRA rate? If, at the end of the contract, the three-month Libor rate turns out to be 5%, what should the settlement amount be?

In Japan, if the three-month (91 days) interbank rate is 1% and the six-month (183 days) interbank rate is 0.25%, what is the 3 × 6 FRA rate? Is this an acceptable rate? Why or why not?

If you expect interest rates to rise over the next three months and then fall over the three months succeeding that, what positions in FRAs would be appropriate to take? Would your answer change depending on the current shape of the forward curve?

A firm plans to borrow money over the next two half-year periods and is able to obtain a fixed-rate loan calling for semi-annual payments at 6% per annum (i.e., at 3% every 6 months). It can also borrow money at the floating rate of Libor + 0.50%. Libor is currently at 4%. If the 6 × 12 FRA is at

You enter into an FRA of notional 6 million to borrow on the three-month underlying Libor rate six months from now and lock in the rate of 6%. At the end of six months, if the underlying three-month rate is 6.6% over an actual period of 91 days, what is your payoff given that the payment is made

You have entered into the 69 FRA of Question 20 at the rate of 6%. After three months, the FRA is now a 3 × 6 FRA. If the three-month Libor rate is 5%, and the six-month Libor rate is 7%, what is the current value of the FRA? Assume that the number of days in the first three months is 92.Data in

Given a 3 × 6 FRA with a rate of 10% and a time interval between three and six months of 92 days, plot the settlement amount if the three-month rate after three months ends up anywhere from 1% to 20%. Is your plot linear, convex, or concave? Why?

You anticipate a need to borrow USD 10 million in six-months’ time for a period of three months. You decide to hedge the risk of interest-rate changes using eurodollar futures contracts. Describe the hedging strategy you would follow. What if you decided to use an FRA instead?

The “standard bond” in the Treasury bond futures contract has a coupon of 6%. If, instead, delivery is made of a 5% bond of maturity 18 years, what is the conversion factor for settlement of the contract? Assume the last coupon was just paid.

Suppose we have a flat yield curve of 3%. What is the price of a Treasury bond of remaining maturity seven years that pays a coupon of 4%? (Coupons are paid semiannually.) What is the price of a six-month Treasury bond futures contract? Make any assumption you require concerning the maturity of the

Suppose you own a zero-coupon bond with face value $3 million that matures in one year. The bond is priced off the continuously compounded zero-coupon rate that is currently at r = 7%. Suppose you want to hedge the price of the bond six months from now using the three-month eurodollar futures

If we wish to hedge a bond that pays a cash flow of 2 million after six months and another cash flow of 102 million after twelve months, suggest a hedging scheme using eurodollar futures contracts. Assume that the bond is priced on a semiannual compounding basis and has a current yield to maturity

Qualitatively discuss how you would hedge a portfolio of bonds using eurodollar futures contracts.

(Difficult) Assume that the yield curve is flat at 6%. All bonds pay semiannually. Bond A has a coupon of 5.5% and a maturity of seven years. Bond B has a coupon of 6.2% and a maturity of five years. We wish to short bond B to offset the risk (duration-based hedging) of a long position in bond A.

We are given a portfolio of bonds with value P = 100 and duration DP = 1. There are two securities available for hedging this portfolio, the first with a price of F1 = 95 and duration DF1 = 0 : 8 and the second with a price of F2 = 92 and duration DF2 = 1 : 2. Suggest a duration-based hedging

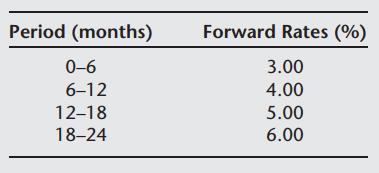

The following market-based FRA rates are provided. Answer the following questions: (a) Find the price of a two-year maturity security with a coupon of 4.5%. (b) Find the price of a six-month bond future on this bond. (c) What is the price of a twelve-month bond future on this bond? (d) Find

Explain the following terms in the context of options: long, short, call, put, American, European, in-the-money, out-of-the-money, at-the-money, strike, holder, buyer, writer, seller, expiry, premium, over-the-counter, and exchange-traded.

What is a “Bermudan” option?

Why is being long a put option somewhat analogous to being in a short stock position?

What is the main difference between a forward and an option?

What is the difference between over-the-counter (OTC) contracts and exchange-traded contracts?

Make a list of securities that you can think of that contain embedded options. For each embedded option, state the underlying source of risk.

Give an example of an option contract that is both exchange-traded and provided over the-counter.

Explain why an option is like an insurance contract. How is it different from a futures contract? Can an option, like a future, be used for hedging?

What position in naked options would you adopt if you believe that the price of the stock is going to drop and the volatility of the stock is going to decrease?

Why do options usually increase in value with volatility? What essential feature of the payoff diagram leads to this result?

Explain the difference between the payoff and price of an option. Write down the payoff formula for a call option and for a put option. What is the difference between the “gross” and “net” payoffs of an option (as widely applied in common usage)? Which concept do you think is the more

Draw a gross payoff diagram for a short position in a call at strike 100. Also draw the gross payoff diagram for a long position in a put option at the same strike and maturity as the call. Overlay these plots on the same axis to get an aggregate payoff diagram for the portfolio of call and put.

Explain what kind of option is embedded in a callable bond. Who benefits from this option? Based on your answer, is a callable bond priced higher or lower than an otherwise identical noncallable bond?

Explain what options exist in a convertible-callable corporate bond.

If you hold a callable bond and the volatility of interest rates increases, what do you think usually happens to the value of your bond?

If you hold a convertible bond and the volatility of equity prices declines, what is the effect on bond value, assuming nothing else changes?

A quanto (quantity) option is one in which the option contains price risk from two sources. Quantos are discussed in the chapter on exotic options. An example is where you buy a put option on the Nikkei stock index (which is yen denominated), but the strike price of the option is stated in dollars.

Showing 600 - 700

of 882

1

2

3

4

5

6

7

8

9

Step by Step Answers