New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

engineering

derivatives principles and practice

Derivatives Principles And Practice 2nd Edition Rangarajan Sundaram - Solutions

Find the value of a first-to-default basket option with a maturity of one year. Assume that the payoff is $100.

What would happen to the price of this first-to-default security if there were no correlation of default between issuers?

The explicit finite-differencing model may be reinterpreted as a lattice model. What type of lattice model does it conform to?

In an explicit finite-differencing lattice, what is required for the model to be stable and convergent?

In the model for pricing American options in the Black-Scholes setting with explicit finite-differencing, what is the main advantage of making a logarithmic transformation of the stock price?

The following question relates to the Black-Scholes model, which is based on a geometric Brownian motion. You are asked to price a one-year range option where the option pays off $100 at the end of each month if the price of the stock lies between $90 and $110. If you set this problem up on a

Given a setting in which the range option in the previous question pays off when the stock price at the end of each month lies outside the specified range rather than inside it, what is the modification you would impose on the boundaries of the lattice? Data in previous questionThe following

Given the following parameters, compute the {p1, p2, p3} values in the implicit finite differencing scheme.The time step is h = 1/48, and the log stock price step is k = 0.10. S = 100, K100, o = 0.3, r = 0.10

Generate 1000 random standard normal numbers. Write out the command used, and state the mean and variance.

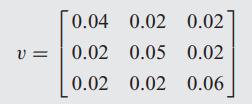

You are given the following covariance matrix for three random normal variates: Compute from Cholesky decomposition the matrix L (lower diagonal matrix) and state your code and the result. V = 0.04 0.02 0.02 0.02 0.05 0.02 0.02 0.02 0.06

Simulate 10,000 paths of monthly stock prices for one year using the geometric Brownian motion stock model. Since the simulation is monthly, you need a time step of 1/12 of a year. Assume an interest rate of 5% per annum and a stock return variance of 35% per annum. Assume the starting price is S0

What is the yield-to-maturity (ytm)?

What is the zero-coupon rate?

Explain the difference between the spot (zero-coupon rate) curve and the yield curve.

How are forward rates different from yields-to-maturity and zero-coupon rates?

Can forward rates be negative? Explain with a numerical example.

Graph the relationship of bond prices to ytm. Take a zero-coupon bond of maturity 0.1 years, and vary the ytm from 1% to 20%. Plot the bond price if continuous discounting is applied for pricing the bond.

What is the value of a dollar at the end of a year if it earns 10% per annum, semiannually compounded?

What is the present value of $225 received at the end of one year at a discount rate of 12%? Assume interest rates are quoted on a semiannual basis.

What is the present value of $225 received at the end of three years at a discount rate of 12%? Assume interest rates are quoted on a semiannual basis.

What is the present value of $225 received at the end of one year at a discount rate of 12%? Assume interest rates are quoted on an annual basis.

Bond A has a maturity of $1 1/2 years. It pays a coupon of 10% with coupons paid semiannually. Draw the time line with the correct cash flows. Its current price is $99. What is the bond’s ytm?

Bond B has maturity one year. Its coupon is 8% per annum. The ytm is 8.5%. What is the correct price of the bond if the semiannual convention is followed?

Coupon Bond Q trades at par. It has a maturity of one year. Its ytm (semiannual basis) is 11%. What is the coupon rate of this bond?

A bond is currently trading at $99.50. The bond has nine months left to maturity and carries a coupon of 3%. Coupons are paid semiannually (so the first coupon is due in three months). If the bond’s face value is $100, what is its ytm expressed with semiannual compounding? With continuous

Consider a bond that pays annual coupons of 7% on a face value of $100. The bond has two years to maturity. If the ytm of the bond (expressed with annual compounding) is 6.80%, what is its current price? What is the bond’s ytm under continuous compounding?

A six-month zero-coupon bond is trading at $98, while a one-year 6% coupon bond is trading at $99. Assume coupons are paid semiannually and that both bonds have a face value of $100. What are the six-month and one-year discount functions implied by these prices?

A six-month zero-coupon bond has a ytm of 5%, while a one-year 5% coupon bond has a ytm of 5.50%. Assume ytm’s are expressed with semiannual compounding, coupons are paid semiannually, and the face value of the bonds is $100. (a) What are the six-month and one-year discount functions implied by

Suppose six-month and one-year discount functions are 0.9804 and 0.96, respectively. What are the corresponding zero-coupon rates? What is the forward rate f (0.50, 1)? (Assume all rates are expressed with continuous compounding.)

You are given the following information: the one-year spot rate is 6.50%, the forward rate f(1,2) is 7.50%, and the forward rate f(1,3) is 9%. All rates are expressed in continuously compounded terms. (a) What are the two- and three-year spot rates? (b) What is the forward rate f (2,3)? (c) What

If the (continuously compounded) yield curve is flat at a rate of 5%, answer the following questions: (a) Price a 10-year semiannual pay bond, with a 5% coupon. (b) Compute the duration of this bond. (c) What is the convexity of this bond?

Write down the Nelson-Siegel model for fitting the forward rate curve. Explain what the intuition is for each of the parameters of the model.

If the yield curve is monotonically increasing with maturity, will the forward curve increase as well?

What are more variable across maturity: zero-coupon rates or forward rates? Explain.

The Neslon-Siegel (NS) model was extended by the Nelson-Siegel-Svensson (NSS) model. What additional feature was provided by the NSS model over the NS model?

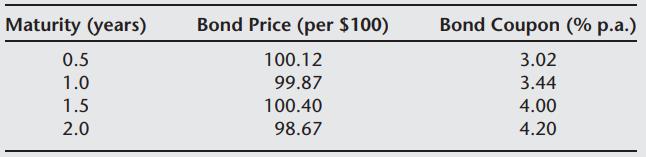

Using the following data on bond prices, bootstrap the spot rate curve for each half-year. Assume that the semiannual compounding convention is followed. Maturity (years) 0.5 1.0 1.5 2.0 Bond Price (per $100) 100.12 99.87 100.40 98.67 Bond Coupon (% p.a.) 3.02 3.44 4.00 4.20

Given two spot rates six months apart, 3% and 4%, interpolate the spot rate four months after the first spot rate, assuming that each month is uniformly 1/12 of a year. Use three different interpolation schemes to do so, and present your answer under each one: (a) Linear interpolation. (b)

In practice, bond prices are never available at conveniently spaced intervals. Some interpolation scheme is called for. However, by making an assumption of constant forward rates between non-standard maturities, we can develop a spot rate curve even for unequal time intervals. In this question, you

If you receive a cash flow of $100 at time 1.25 years, explain how you would allocate this cash flow into two cash flows, cash flow A received at one year, and cash flow B received at 1.5 years. Assume that the zero-coupon rate for 1 year is 6% and that for 1.5 years is 6.5%. Assume continuous

Fit a cubic splines framework to the following discount function values assuming two knot points at t = 0.5 and t = 1 years.Explain your equations and the number of parameters you need to find. t 0.35 0.70 1.05 1.40 1.75 d(t) 0.97 0.93 0.88 0.82 0.75

Write a general program to compute the coefficients of an exponential cubic spline fitting model given a parameter m. Then apply this program to a fitting of the following discount functions with knot points at t = 0.5, 1.0.Refit the discount functions to the model and compare your answers against

You are provided the following discount function data. Fit it to a cubic exponential system with knot points every half year until and including t = 4.5 years. t 0.25 0.50 0.75 1.00 1.25 1.50 1.75 2.00 2.25 2.50 2.75 3.00 3.25 3.50 3.75 4.00 4.25 4.50 4.75 5.00 d(t) 0.97092 0.95886 0.94881

The table below presents the forward curve for a range of maturities. Fit the Nelson Siegel-Svensson model to this forward curve. t (in years) 1/12 1/2 1.0 2.0 3.0 5.0 7.0 10.0 f(t) (in % p.a.) 1.39 3.02 3.77 3.94 4.10 4.23 4.46 4.58

Why is the Black-Scholes model inappropriate for pricing options on bonds?

You are given a two-period tree of zero-coupon interest rates with each period on the tree of half-year and a semiannual compounding convention applies in the model. Find the initial (at t = 0) yield-to-maturities for half- and one-year maturities if the current half-year spot rate is 6%. The

In the previous question, find the initial curve of zero-coupon rates and of the forward rates for periods of one-half year and one year.Data in previous question. You are given a two-period tree of zero-coupon interest rates with each period on the tree of half-year and a semiannual compounding

Given the tree of spot rates and probabilities, is it possible to find the entire tree of forward rates or is additional information required?

Explain why modeling the movement of the term structure is different than modeling the movement of equity prices.

You are a trader in a bond fund. The current yield curve is flat at 6%. Assume you decide to model the yield curve movement as a discrete annual process. Hence, at the end of one year, the yield curve moves up or down. Your in-house economist tells you that the yield curve will become either a flat

Is it possible that from some node on a binomial tree of interest rates the ensuing two nodes both have higher interest rates than the current node? Construct an example to show that this is possible or explain why it is impossible.

If the initial rate at any node at time t on a binomial interest rate tree is r1 and the two ensuing nodes after time h = 1 year are ru (with probability p) and rd (with probability 1 − p), then given that the two-period zero-coupon rate is r2, write down the analytic expression for the

The current one-year and two-year spot rates are 6% and 7%, respectively. Compounding is annual. The model you are using prescribes that in a risk-neutral setting, the next period’s one-year interest rates will be either 8% or 5%. No risk-neutral probabilities are given. Does the modeling

The initial spot rate curve (annual compounding) for three years is given as After an assessment of volatilities and interest rate propagation in the future, your quant team provides the following tree of spot rates at times 0, 1, 2 years: This means that from a starting rate of 6%, one-year spot

Can you explain what happens to the tree model in the previous two questions if we lift the restriction that pt must be the same at all nodes in time period t? This means that we do not require p(t, j) = pt for all nodes j. Does this result in an arbitrage violation?

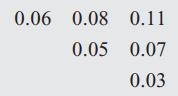

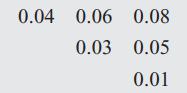

You are given the following annual step, discrete-time interest rate tree, where all branches on the tree occur with probability of one-half. Find the initial spot rate curve for three years. 0.04 0.06 0.03 0.08 0.05 0.01

A popular equilibrium model of interest rates is the Cox, Ingersoll, and Ross (1985) model: Answer the following questions: (a) How many free parameters are available to fit the model to the term structure of interest rates? (b) As a trader, would this model be suitable for yield curve

Can the mean-reversion rate κ in an interest-rate model be (a) Less than 0? (b) Greater than 1?

Bond pricing in the Vasicek (1977) model: assume an interest rate processWhere base parameter levels are r = k = θ = σ = 0.1, T = 1, and d B is a standard Brownian motion. Assume also that the market price of risk λ = 0. In each of the following three cases, compute the bond price for each value

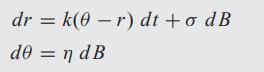

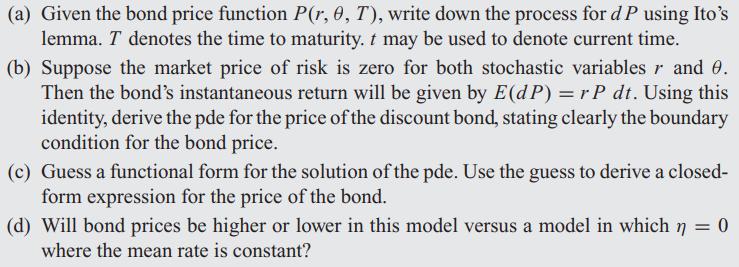

In this problem we extend the Vasicek model to allow the mean rate θ to become stochastic. Think of a situation in which the Federal Reserve makes minor adjustments to short-term market rates to manage the temperature of the economy. The model comprises the following two equations: The Brownian

Write a function in Octave for the Cox, Ingersoll, and Ross (CIR 1985) model and price the bond when the values are r = k = θ = σ = λ = 0.10, and T = 5 years.

In the CIR model, compute the yield curve from 1 to 10 years when r = k = θ = σ = λ = 0.10.

Find a set of parameters in the CIR model such that the yield curve from 1 to 10 years is of upward-sloping shape.

State at least three differences between the HJM model and the model of Black-DermanToy (BDT).

Denote the forward rates in the HJM model by f (t, T), where t is current time, and the forward rate is for the future period [T, T + h], where h = 1 year is the discrete time interval. Suppose you are given the following binomial evolution of forward rates:Finally, suppose you are also provided

Assume the following process for HJM forward rates: Let the current forward curve be given by f(t+h, T) = f(t, T)+a(T)ho (T)h

There are six half-year periods on a forward curve. The curve is currently flat at 6%, and you are given the following declining volatility curve: (a) What feature of interest rates might result in the volatility curve declining so sharply? (b) Solve for the two forward curves a half-year ahead,

Suppose that the time interval on an HJM tree is h and the forward rate process is binomial: Show that for T = t + h f(t+h, T) = f(t, T) +ah oh = -In[cosh(o h/)] h

In the previous question, what can you say about the expression for the drift in terms of its representation of the interest-rate risk premium? What is it uniquely a function of? Data in previous question,Suppose that the time interval on an HJM tree is h and the forward rate process is

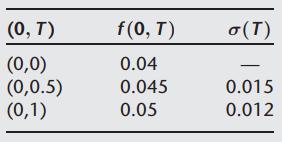

The following table summarizes the initial forward curve for three half-year periods and the initial volatility curve at t = 0. Compute the two forward curves at time t = 0.5 and the three forward curves at time t = 1. (0, T) (0,0) (0,0.5) (0,1) f(0, T) 0.04 0.045 0.05 o (T) 0.015 0.012

Based on the same input parameters as the previous question, price a cap option contract with exercise dates at t = 0.5 and t = 1, at a strike rate of the half-year interest rate of 5%. Assume the notional on the contract to be $100. Data in previous question,The following table summarizes the

What claimed deficiencies of the HJM model are ameliorated by using the Libor Market Model (LMM)?

What is the “forward” measure? Explain its importance in the pricing of interest rate derivatives.

If you are an equity asset manager and wish to diversify away from stocks, what credit derivative would you choose?

What are some of the advantages to a seller and a buyer in a credit spread option contract?

What is a credit-sensitive note (CSN)? How does it work? What is the advantage to the issuer? To the investor? What are the drawbacks to the investor?

What is an n-th to default contract? How does credit correlation impact this contract?

You expect that the market’s expectation of recovery rates of a given issuer will be higher in a few weeks. There are two reference instruments for the same issuer: senior (S) and junior (J). Which of the following strategies would you prefer? Explain why. (a) Long S, long J. (b) Long S, short

In a CDO, suppose there are three tranches: A gets first claim to all cash flows from the collateral, B gets second claim, and there is a residual equity tranche E. Suppose the level of default risk in the economy declines but the correlations of default increase. What would be the likely impact of

A credit default swap provides protection against the default of the reference issuer in the contract. Does it provide protection against the deterioration of the credit quality of the reference name before default occurs?

A bond fund wishes to speculate on the value of a five-year B-rated junk bond. It believes that, conditional on the bond surviving the next two years, it will rise in quality and be worth more. Suggest a risk management strategy for this trade.

EZFund can raise financing at six-month Libor plus 25 bps for five years. It finds that five-year Ampco bonds (BB rated) are trading at a yield to maturity of 10%. If total return swaps linked to the BB index are currently returning 9.50% versus six-month Libor, what arbitrage trade may be

The credit default swap on a three-year bond is trading at a spread (premium) of 1%. If the credit spread on the bond is at 1.1%, suggest a trade to take advantage of this. Why do you think there might be a difference in spreads on the CDS and the bond?

You expect credit correlations to increase. If so, which of the following strategies is appropriate: (a) Long a first-to-default (FTD) contract and long a second-to-default (STD) contract. (b) Long FTD, short STD contracts. (c) Short FTD, long STD contracts. (d) Short FTD, short STD contracts.

Suppose you have a model for pricing convertible bonds that accounts for equity risk, interest-rate risk, and credit risk and is calibrated using observable stock prices, bonds, and credit default swaps. If the model price of the convertible bond exceeds that of the market and you believe the model

How might you convert a mortgage-backed securities (MBS) portfolio into a creditrisk-based CDO using CDS contracts? What should the CDS have as underlyings?

Can you suggest another credit contract that may be used to construct a synthetic CDO from a portfolio of MBS?

A CDO structure comes with a special clause for the A tranche whereby early amortization occurs if more than three issuers default within the first two years of the CDO. What happens to the value of the A tranche as we increase the number of issuers in the collateral?

Suppose we wish to price the spread on a two-year annual payment credit default swap. The constant interest rate is 10%. Suppose the conditional probability of default each year is also constant and is denoted p. Write down an expression that expresses the two-year fair value of the CDS spread (s)

If the correlation of default remains the same but the correlation of recovery between two issuers increases, what is the impact (ceteris paribus) on the price of a second-todefault contract?

In a synthetic CDO, does the issuer of the CDO tranches hold CDS contracts in long or short positions? Explain.

The Merton (1974) model may be used to value bonds with default risk in a company. Explain how debt is viewed as an option in this framework.

What information do structural models deliberately ignore in the valuation of debt in a firm?

In the Merton model, why do we obtain very low short-term spreads?

The volatility of a firm’s assets is 20%. The firm’s assets are worth $200 million and are normally distributed. The risk-free rate of interest is 2% and the expected rate of return on the firm is 10%. The firm has $100 million in face value of debt maturing in one year. Compute both the

Explain why for small distance to default, the spread curve in the Merton model is hump-shaped.

The volatility of company ABC’s assets is 30%. The current value of its assets is $50 million. The risk-free rate of interest is 3%. If the face value of two-year maturity debt is $30 million, what is the value of the firm’s equity? Use the Merton (1974) model. What is the value of debt?

If the risk-free rate of interest is 4%, firm value is 75 million, and equity is 50 million, what is the credit spread on the bonds of the firm if they are of zero-coupon form with face value 30 million and expire in one year? (Assume continuous compounding.)

If the value of the firm is $100 million, the value of equity in the firm is $40 million, the risk-free rate is 4%, and debt has a face value of $70 million with zero coupons and a maturity of three years, what is the firm’s volatility of returns on its assets? What is the risk-neutral

Express the distance to default in terms of the risk-neutral probability of default.

Assuming that you have good historical data, how would you convert the risk-neutral default probabilities from the Merton model into default probabilities under the realworld measure?

Showing 300 - 400

of 882

1

2

3

4

5

6

7

8

9

Step by Step Answers

![Show that for T = t + h f(t+h, T) = f(t, T) +ah oh = -In[cosh(o h/)] h](https://dsd5zvtm8ll6.cloudfront.net/images/question_images/1704/9/6/1/775659fa6ef37d011704961775575.jpg)