New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

engineering

derivatives principles and practice

Derivatives Principles And Practice 2nd Edition Rangarajan Sundaram - Solutions

In the Geske-Delianedis model, there are two tranches of debt, short term and long term, hence allowing for short-term and long-term risk-neutral probabilities of default. If short-term debt has a maturity of one year, the probability of default is p1 = 2%, long-term debt has a maturity of two

If short-term debt has a maturity of one year, the probability of default is p1 = 2%, long-term debt has a maturity of five years, and the cumulative probability of default is p2 = 10%, what is the annualized forward probability of default between one and five years?

In order to stay within the Merton model framework, one way to accommodate firms with multiple debt issues in their capital structures is to collapse all debt into zerocoupon form at some representative maturity (e.g., one year). For example, one approach is to treat the debt face value at maturity

Write down the cumulative risk-neutral probability of default up to time T in the Merton model.

If default intensity λ = 3, what is the probability of two or more defaults in a quarter of a year?

If λ = 2, what is the probability of survival for three years?

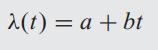

Suppose that the default intensity of a firm varies over time t and is given by the following function: What is the probability of the firm defaulting in two years? = 0.5 0.017

State a few important differences between reduced-form models and structural models of default risk.

Assume continuous compounding. Suppose the firm has a constant default intensity λ = 2. The risk-free rate of interest is r = 0.02. The recovery rate is φ = 0.5, and all recovery of a defaulted security is assumed to occur at the original maturity of the security. Price a two-year zero-coupon

You are given that the intensity of default is λ = 0.5, and recovery rate is φ = 0.5. The risk-free rate of interest is r = 0.01. In contrast to the previous question, the recovery amount is obtained at the time of default, not at the stated maturity of the security. Find the price of a one-year

The intensity of default is constant, λ = 0.5. What is the conditional probability of default at time t?

You are given that the cumulative probability of default for one year is 6% and for two years is 10%. The intensity is given by the following function of time What are the values of a, b? a bt 19 + 0 = (1) Y

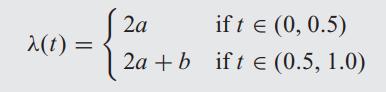

We examine the pricing of a semiannual pay, one-year credit default swap (CDS). The premium payments are made at the beginning of each semiannual period, and default payments are made at the end of each period. The default intensity is given by the following function The CDS spreads for a half

Given that λ = 0.2, the risk-free rate r = 0, and the recovery rate φ = 0.5, price a CDS contract with maturity for two years, with semiannual premium payments made at the start of each period. Default payments are made at the end of each period.

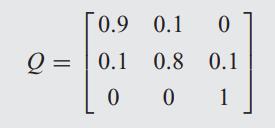

Assume there are three debt ratings: A, B, and D, where D stands for default. The one-period risk-neutral transition probability matrix for ratings is given as: What is the probability of default of an A-rated firm in one period, two periods, and ten periods? 0.9 0.1 0 0.1 0.8 0.1 01 Q = 0.1 0

The default intensity is given as λ = 0.1 per period. The recovery rate is φ = 0.5. The risk-free rate of interest isr = 0.10 per period. Compute the price of a zero coupon bond with a maturity of two periods under the following assumptions:• No default risk (i.e., Treasury). • Default risk

The risk-free rate of interest is constant and is 10%. The credit spread for an issuer is also constant and is 2%. If the recovery rate is 50%, all componding and discounting is continuous, and default is assumed to occur at the end of the year, (a) What is the probability of default in one

The risk-free rate of interest is constant and is 10%. The credit spread for an issuer is also constant and is 3%. If the recovery rate is 40%, then given continuous compounding, (a) What is the probability of default over a two-year period? (b) What is the price of a two-year $1 zero-coupon bond

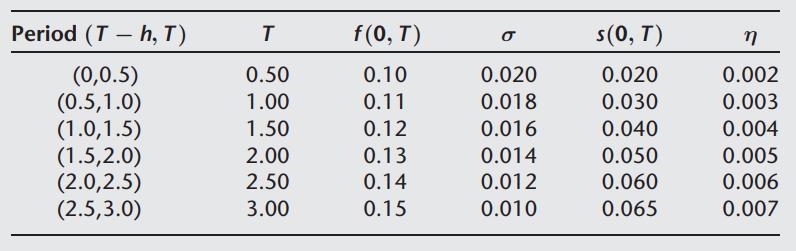

This question requires you to implement the Das-Sundaram (DS) model presented in the chapter. The notation is the same as that used in the chapter. You are given the following table of forward rates and spreads along with their volatilities: The correlation between spreads and interest rates is

What makes an exotic option path-dependent? Think of an example of such an option that is not covered in this chapter. Explain why you consider it path-dependent.

If an option is path-dependent, do we need to use a nonrecombining binomial tree for pricing it? That is, do we need to evaluate the option payoff along each path of stock prices separately rather than being able to price it by backwards recursion using the original stock price tree?

Are American options path-dependent? Why or why not?

Why are Asian options popular? State some uses of Asian options.

Is an Asian option cheaper or more expensive than a plain vanilla option? Why? Is this always true?

Explain the difference between an Asian average-price option and an Asian averagestrike option.

Distinguish between a lookback price option and a lookback strike option.

Consider an initially at-the-money knock-out put option with the knock-out price H set above the strike K. Will the price of the put be greater, smaller, or equal to that of a vanilla put? Why?

Why does a knock-out call cost less than the corresponding vanilla call?

If you want to invest in the upside potential of a stock but are afraid of overpaying for options that favor your view, suggest two ways in which you may buy a single barrier option that implements your view more cheaply.

You are the holder of an up-and-out put option. Now you want to replace it with a plain vanilla put at the same strike and maturity. What option should you purchase to achieve this?

Which has greater value, an arithmetic-average-price Asian option or a geometricaverage-price one?

What is the sign of the delta of an up-and-out call option? Explain how the delta depends on the closeness of the current stock price to the barrier.

Consider a two-period binomial tree with the following parameters: S = 100, u = 1.10, d = 0.90, and R = 1.03. Find the prices of: (a) A knock-out call option with a strike of 95 and a barrier of 90. (b) A knock-in call option with a strike of 95 and a barrier of 90. (c) A vanilla call option

Using a three-period binomial tree, value a down-and-out call option. The parameters you are given are the following: the initial stock price is $100, the strike price is $105, the barrier is $90, the risk-free rate per-period is 5%, the option maturity is three years, and the volatility of the

In the above question, what would we do to the model to make it default to a vanilla call option? Would the vanilla call be worth more or less than the barrier option?Data in above question,Using a three-period binomial tree, value a down-and-out call option. The parameters you are given are the

A reverse cliquet with quarterly resets pays an annual coupon of 15% less the return during any quarter in which the return is negative. The index is at 1000 at the beginning of the year and takes values of 900, 1000, 1100, and 1050 at the end of each of the succeeding quarters. What is the final

The current stock price is $100. Price a half-year average strike Asian call option if the stock volatility is 30%, and the annual risk-free rate is 10%. Use a tree model with six monthly steps. Compare the price you arrive at with the price of an otherwise identical average price Asian call at a

What is Value-at-Risk (VaR)? What is the minimal information you need to compute VaR? What are its advantages and its limitations?

How is Value-at-Risk (VaR) different as a measure of risk than the variance of return?

What, if any, is the relationship of variance and VaR?

Which moments of the return distribution are measures of risk? State some of them, and explain what the nature of the risk measure is, and what insight one might be aiming for with your chosen measure of risk.

If the mean, variance, and skewness remain the same, but the kurtosis of returns on a portfolio increases, will the VaR increase or decrease, keeping all else the same?

If the mean and variance remain the same but the skewness of returns on a portfolio becomes more negative than before, what do you think will happen to the VaR of the portfolio?

What is the relationship of the trading horizon used for calculating VaR and the level of VaR? What do you think is an optimal horizon for VaR calculations?

Is it feasible to compute the risk contribution of individual assets to the total risk of a portfolio under the VaR measure if the distribution of returns is not normal and the delta-normal approach is not available?

VaR has been criticized for not being a “coherent” risk measure. Why is this?

Suppose the average profit of FOF Inc. is $1 million per week. The standard deviation of profits per week is $1 million as well. Calculate the 99% and 90% VaR for FOF. Assume profits are normally distributed.

In the preceding problem, suppose the distribution of returns is not normal but Student’s t with 5 degrees of freedom. What is the 99% VaR under the new assumption? What happens to the VaR when the t distribution has 20 degrees of freedom instead? Explain the difference in results.Data in

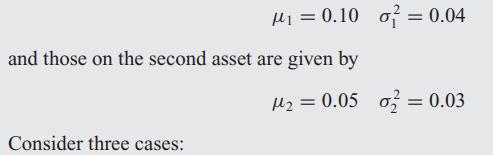

Consider a portfolio that has equal amounts of $10 invested in two assets. Suppose returns on the two assets are jointly normally distributed. The annual expected returns and variance of returns on the first asset are given by Consider three cases: (a) The correlation between the returns is ρ =

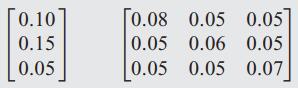

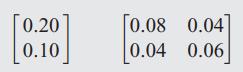

You are given a portfolio of three assets with mean vector and covariance matrix of returns as follows: Compute the 95% VaR for a portfolio that is invested in $1 in each asset using the delta-normal method.

You are managing a portfolio that tracks the S&P 500 index. You consider two ways in which you might calculate the VaR: (a) Using the delta-normal approach by calibrating the mean and variance of the portfolio to the historical data. (b) Using historical simulation based on the same data.Which

You are given a portfolio of three assets whose returns are jointly normally distributed with the following mean vector and covariance matrix: (a) Compute the 95% VaR for the portfolio if we invest $1 in the first asset, $2 in the second asset, and $3 in the third asset. (b) How much does each

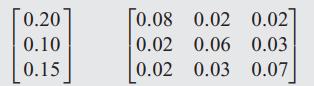

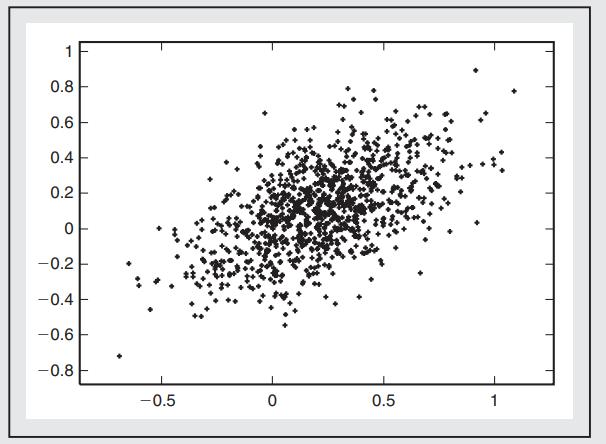

Examine the following plots of bivariate return distributions closely. Pay special attention to the values on the axes. Both plots are joint distributions of returns of stocks. The first Plot is from a Student’st distribution and the second one from a normal distribution. Both have the same

You are given a portfolio of two assets whose returns are jointly normally distributed with the following mean vector and covariance matrix: (a) Compute the 95% VaR of the portfolio if $1 is invested in the first asset and $1 is invested in the second. (b) Compute the risk-contribution of each

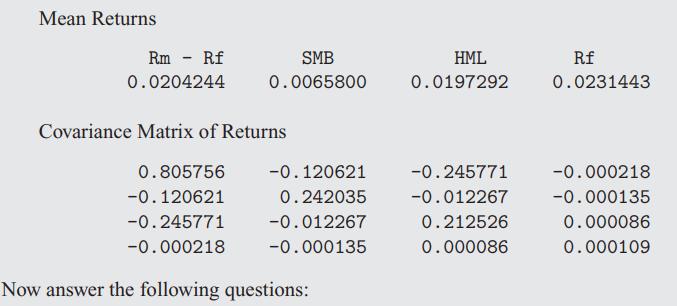

The following asset-pricing factor returns are downloaded from the FamaFrench database: the excess market return, the SMB portfolio return, the HML portfolio return, and the risk-free return. From the downloaded data, which is for the period 1963–2003, we get the following mean and covariance

This question talks about adjustments you may need to make in the computation of VaR. (a) In a historical simulation algorithm for VaR, suppose the portfolio’s historical mean return is anticipated to be understated by 2%. What adjustment would you make in the simulation for determining the VaR

Define and quantify the following terms related to convertible bonds: (a) Conversion ratio, (b) Callability, (c) Fair premium, (d) Parity, (e) Breakeven,

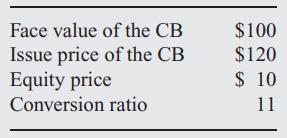

You are given the following input information: (a) What is the parity value per bond? (b) What is the premium over parity per bond? (c) Express the same results on a per-share basis.

What are the different types of embedded options within a convertible bond? Explain whether they benefit the investor or the issuer.

What incentive issue has been commonly resolved by the issuance of a convertible bond by the management of a firm?

The face value of a convertible bond is $100, and the issue price is $150, with a conversion ratio of 5. The market price of the equity shares is $25. Compute the.(a) Conversion price, (b) Parity,(c) Premium of the bond.

XYZ Co. has issued convertibles with face value $100, and the issue price is $100. The market price per share is $20 and the conversion ratio is 4. The bond pays a coupon of 5%, and the dividend rate on equity is 1%. What is the premium on the bond? What is the breakeven period to recover the

Assume the current stock price is $100. Next period it can take a value of either 120 or 80. If the return on $1 invested today for one period is 3%, then how much will a zero-coupon convertible bond be worth today if the conversion ratio is 1?

Assume the current stock price is $100. Next period it can take a value of either 130 or 90. If the return on $1 invested today for one period is 5%, then how much will a 6% coupon convertible bond be worth today if the conversion ratio is 1? Can you construct an arbitrage in this situation that

Assume the current stock price is $100. Next period it can take a value of either 1.2 or 0.8 times the stock price. If the return on $1 invested today for one period is 2%, then how much will a zero-coupon convertible bond (face value $1000) be worth today if the conversion ratio is 10? What are

Using a semiannual CRR binomial tree, price a convertible bond with a face value of $100, conversion ratio of 1, and a coupon rate of 10%. The maturity of the bond is three years. Assume that the stock volatility is 25%. The risk-free rate of interest is 4%. All calculations may be based on

In the preceding question, assume that the convertible bond is also callable at a price of $110 (cum-coupon). Rework the price of the convertible bond. Explain your answer.Data in preceding question,Using a semiannual CRR binomial tree, price a convertible bond with a face value of $100, conversion

Using the program you wrote for the callable-convertible bond, modify it to compute the delta of the bond for a range of stock prices from 80 to 120. Let the coupon rate be 10%, the risk free rate be 4%, and the volatility 25%. The call strike is $100. Explain your results. On conversion, the

(Advanced Question; Goes beyond Text) Think of five trading strategies that you may wish to implement using convertible bonds. For each of these ideas, what risks would you need to eliminate from the bonds in order to implement your trading views?

The current equity price of firm XYZ is $10. The equity trades at a volatility of 20%. The firm issues a five-year convertible bond at a face value of $100 and a coupon of 6%. This bond may be converted into eight shares of equity at any time in the next five years. The risk-free interest rate in

A convertible bond is sensitive to both stock price movements and interest-rate changes. Which of the following scenarios is likely to result in the greatest price increase of a convertible? (a) Stock price rises; interest rates fall. (b) Stock price rises; interest rates rise. (c) Stock price

Which of the following scenarios is most likely to result in the greatest increase in the price of a convertible bond? (a) Stock volatility increases; interest-rate volatility increases. (b) Stock volatility increases; interest-rate volatility declines. (c) Stock volatility declines;

What is the expected impact of an increase in maturity on convertible bond values, holding all other conditions the same?

Why does traditional NPV analysis break down in the presence of real options within an investment opportunity?

State three different forms of real options and discuss possible real-world cases in which such options are likely to be manifest.

You have the option to invest in a project at any time in the future. If the riskiness of the project increases, does it increase or decrease the average waiting time to making the investment?

The option to wait to invest in a risky project is a valuable one. The risk of waiting to invest is a possible loss in market share to other early movers into the market. How would you use the option pricing framework to model the possible loss of market share? What parameter in the option model

What does the option of waiting to invest do to the following features of the project versus making a project choice based on NPV alone? (a) Riskiness of the project, (b) Effective hurdle rate for the project,(c) Probability that the project will be undertaken.

Shining Metal Inc. has invested in a gold mine. The company needs to decide whether to drill for gold at the beginning of the year or wait until next year. Gold drilled this year will be sold at end-of-year market prices. The mine generates 15,000 ounces of gold per year. The current price of gold

In a gold mine, the price of gold is a major determinant of the value of the project. (a) When the price of gold drops, what real option in the mine may be exercised? (b) When the price of gold rises, what real option in the mine may be exercised? (c) If the volatility of gold increases and all

In real options analysis, what discount rate should be used in the model for valuing the option?

You invest in an oil exploration project with a public company. What are the two main risks you face? How do you hedge these risks?

Based on real options analysis, would you expect to see more or less oil exploration as oil price volatility increases?

The current price of silver is $7 per ounce. You are a maker of silver jewelry and wish to obtain a guaranteed supply of silver at the end of the year at a maximum price of $8 per ounce. If the volatility of silver is 20%, how much would you be willing to pay for the guarantee? The risk-free

You are the purchasing manager of a major health-care provider. A certain generic drug is selling at a price of $10 per unit. To ensure that costs for this drug do not exceed $12 per unit the following year, you arrange a guaranteed maximum price with the supplier for a commitment fee of $0.15 per

How does the option of waiting to invest impact project values? When is it worth the wait? What is the implicit effect of the option of waiting to invest on the project’s hurdle rate?

How is the option of waiting to invest different from the option to abandon the project? What exotic options are these optionalities analogous to?

Contrast the state-space approach to valuing real options with the traditional discounted cash-flow approach. Highlight three advantages of the state-space approach over the DCF one. What are the possible disadvantages?

In this problem, you will download market data and generate a state space for valuation purposes. Please carry out the following set of steps: (a) Download five years of monthly stock price data from the web. You may use a convenient source such as Yahoo! Finance. Do this for 10 stocks. (b)

You have current wealth of $100. You are offered a venture in which you may with equal probability double your money or halve it. If your utility is the square root of your wealth, would you take this venture?

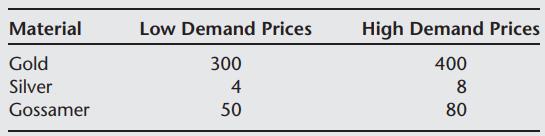

You have developed a new material called gossamer, which has demand characteristics closely related to the markets for gold and silver. The prices of these commodities at the end of the year are forecast to be as follows: The input raw materials to make gossamer cost $65. Do you think this is a

Explain why a swap is a collection of forward rate agreements (FRAs).

Show that a swap in which one receives fixed and pays floating is equivalent to a portfolio of caps and floors. Present the specific relationship.

What is the relationship of a swap to fixed- and floating-rate bonds?

What is the duration of a floating-rate note (FRN)?

You hold a Libor FRN with a coupon rate that is capped at 10%. Explain whether the price is increasing or decreasing as a function of Libor.

A swaption is an option on a swap. A cap is a portfolio of options on FRAs. Given that swaps are portfolios of FRAs, what has greater value, (a) A swaption(b) A cap?

What is the impact on the value of a swap if, ceteris paribus, the volatility of interest rates rises?

The six-month Libor rate is given to be 3% and the twelve-month rate to be 4%. The 6 × 12 FRA is trading at 4.2%. Show how you would construct a sure arbitrage to take advantage of these market rates. Assume the first six-month period is 181 days and the second is 184 days. The interest-rate

Consider a long position in a 6 × 12 FRA contract at a fixed rate of 4.2% Compute the payoff to this contract for a range of interest rates from 1% to 10%. Is the slope of this payoff function positive or negative? Explain. Assume the first half of the year is 181 days and the second half is 184

Showing 400 - 500

of 882

1

2

3

4

5

6

7

8

9

Step by Step Answers