New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

engineering

derivatives principles and practice

Derivatives Markets And Analysis 1st Edition R. Stafford Johnson - Solutions

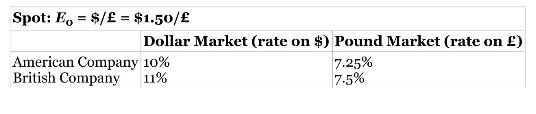

The table shows the annual loan rates that American and British multinational companies can each obtain on a five-year, \(\$ 150\) million loan in dollars and an equivalent five-year, \(£ 100\) million loan in the pounds.Loan Rates for American and British Companies in Dollars and Poundsa. Suppose

Currency swap valuation questions:a. What is the bond equivalent of a currency swap position in which the counterparty agrees to swap a three-year, \(10 \%\) loan of \(\$ 15\) million for a three-year, \(7 \%\) loan of \(£ 10\) million?b. What is the bond equivalent of a currency swap position in

Explain with an example an operational exchange rate hedge or natural hedge. In your example, assume a US-owned company with its operation and sales in the United Kingdom, material expenditures in US dollars, and with the following annual cash flows:- Revenue \(=£ 40\) million- Operating cost

Select a CDS on a company of interest with investment-grade bonds (Ticker CDS ), CDS Ticker ) and analyze it using the following screens: DES, AllQ (Composite Quotes), GP, and CDSW (Valuation).

Select a CDS on a company of interest with non-investment-grade bonds (Ticker CDS , CDS Ticker ) and analyze it using the following screens: DES, AllQ (Composite Quotes), GP, and CDSW (Valuation).

Select a CDS from the WCDS screen (Ticker CDS , CDS Ticker ) and analyze it using the following screens: DES, AllQ (Composite Quotes), GP, and CDSW (Valuation).

Select a CDS on a sovereign country's CDS. From the SECF screen (SECF ), click "Fixed Income" in the "Category" dropdown, click the "CDS" tab, and type in the name of the country (e.g., Greece) in the amber CDS Ticker box. Analyze the CDS (CDS Ticker ) using the following screens: DES, AllQ

On the SWPM screen, create and then evaluate a currency swap. On SWPM screen, click "Cross Currency Swap (Fixed-Fixed)" from the "Products" tab. On the "Main" screen, select currency and interest rates. Evaluate your swap's cash flow ("Cashflow” tab).

Suppose you took a short position in a June Eurodollar futures at \(R_{D}=2.50 \%\).Determine the futures settlement prices and your position's profits and losses given the following LIBOR at the June futures' expiration: \(2.00 \%,2.5 \%\), and \(3.00 \%\). Determine your profits and losses if you

Explain how the clearinghouse would record the futures trades in a-d. Include the clearinghouse's payments and receipts needed to close each position.a. Mr. A buys a September T-bond futures contract from Ms. B for \(\$ 105,000\) on June 20.b. Mr. D buys a September T-bond futures contract from Mr.

Define a forward rate agreement (FRA). Provide your own example of a FRA.

Given a FRA with the following terms:- Notional principal \(=\$ 20\) million- Reference rate \(=\) LIBOR- Contract rate \(=R_{k}=2.00 \%\) (annual)- Time period \(=90\) days- Day-count convention \(=\) Actual \(/ 365\)Show in a table the payments and receipts for long and short positions on the FRA

Kendall National Bank is planning to make a \(\$ 10\) million short-term loan to Two-Dollar General. In the loan contract, Two-Dollar agrees to pay the principal and an interest of \(2.50 \%\) (annual) at the end of 180 days. Since Kendall National sells more 90-day CDs than 180-day CDs, it is

As an alternative to a nine-month, \(4 \%\) fixed-rate loan for \(\$ 10\) million, the O'Brien Beverage Company is considering a synthetic fixed rate loan formed with a \(\$ 10\) million floating-rate loan from First National Bank and a Eurodollar strip. The floating-rate loan has a maturity of 270

Xavier Trust is planning to invest \(\$ 10\) million for one year. As an alternative to a oneyear fixed-rate note paying \(2.5 \%\), XSIF is considering a synthetic investment formed by investing in a Second National Bank one-year floating-rate note (FRN) paying LIBOR plus 100 basis points and

Using the carrying-cost model, determine the equilibrium price of a forward contract on a 90-day zero coupon bond ( \(\mathrm{ZCB}\) ) with a face value of \(\$ 1\) million and expiring in 180 days. Assume the price on a similar 270-day spot ZCB is \(\$ 954,484\) and the risk-free rate on 90-day

Given: (1) 121-day spot T-bill trading 98.318 to yield \(5.25 \%\); (2) 30-day risk-free rate of \(5.15 \%\); (3) a T-bill futures contract with an expiration of \(T=30\) days.a. What is the equilibrium T-bill futures price and its implied futures YTM (annualized)?b. Explain what a money market

Given the following information related to a T-bond futures contract expiring in six months:- The best estimate of the cheapest-to-deliver bond on the T-bond futures contract pays an \(8 \%\) coupon, is currently priced at 108 (clean price), has a conversion factor of 1.21; the bond's last coupon

Select a US Treasury bond or note with an intermediate-term or long-term maturity (5 to 20 years). To find your bond, use the FIT screen or SECF (SECF < Enter>; Category: Fixed-Income; Govt Tab; select Maturity: 4-7 years or greater; select denomination: USD). Evaluate the bond using the following

Evaluate the current yield curve level and structure using the following screens:a. YCRV or GC to access yield curves.b. FWCV to determine implied forward rates.c. USoo03M, USoo06M, USoo09M, and USoo12M (USoo03M < Return>) to see historical 3-month, 6-month, 9-month, and 12-month LIBORs.d.

Access Bloomberg information on a CME Eurodollar futures contract: Type CTM to bring up the "Contract Table Menu," click "Categories" and "Interest Rates," search for CME on the Menu (type CME in the amber Exchange box), find the CME contract of interest, and bring up the contract's menu screen

Examine the historical prices of the Eurodollar futures contract you selected in Exercise 3 (select a time period that the contract was active).a. Select a period in which you would have taken a long position and calculate the profit from opening and closing at the futures prices at the beginning

Access Bloomberg information on a T-bond futures contract: type CTM to bring up the "Contract Table Menu," click "Categories" and "Bonds," search for the CBT on the Menu (type CBT in the amber Exchange box area), find the CBT contract of interest and bring up its menu screen (Ticker ; e.g., USA

Using the GP screen, examine the historical prices of the T-bond futures contract you selected in Exercise 5 (select a time period that the contract was active).a. Select a period in which you would have taken a long position and calculate the profit from opening and closing at the futures prices

Access Bloomberg information on a T-note futures contract: type CTM to bring up the "Contract Table Menu," click "Categories" and "Bonds," search for CBT on the Menu (type CBT in the amber Exchange box area), find the CBT contract of interest, and bring up the contract's menu screen (Ticker ; e.g.,

Using the Chart screen (Chart ), examine an intercommodity Notes-over-Bonds (NOB) spread formed with a T-bond futures and T-note futures contracts similar to the ones you analyzed.Note that the contracts have to have the same expiration.a. Use the Chart screen (Chart ) to create multigraphs for the

Examine an ex-post long hedging position for a future T-bond or T-note purchase.a. Select a futures contract and use one of the cheapest-to-deliver bonds or notes on the contract as the bond or note you plan to purchase, and use the expiration date on the futures contract as the date of your bond

Examine an ex-post short hedging position for a future T-bond or T-note sale.a. Select a futures contract and use one of the cheapest-to-deliver bonds or notes on the contract as the bond or note you plan to sell and use the expiration date on the futures as the date of your bond or note sale.b.

Examine an ex-post short hedging position in which you hedge the value of a holding of 1,000 issues of a selected option-free (bullet), investment-grade corporate bond of interest with a futures contract on a T-note or T-bond with a maturity close to the maturity on your bond. Form your hedge,

Examine an ex-post short hedging position for the portfolio you created.a. Select a futures contract on a CBT T-bond or T-note contract to hedge your portfolio. Use the expiration date on the futures contract as the date of your hedge value.b. Use the Chart screen (Chart ) to create multigraphs for

Examine a duration enhancement or reduction strategy for the portfolio you created.a. Select one futures contract on a T-bond or T-note (e.g., TYA) to go long or short. Use the expiration date on the futures contract as the date for closing the strategy.b. Use the Chart screen (Chart ) to create

Show graphically the profit and stock price relationships at expiration or if the option is exercised for the following fundamental option positions:a. Call Purchaseb. Naked Call Writec. Covered Call Writed. Put Purchasee. Naked Put Writef. Covered Put Write In each case, assume the stock is

Show graphically the profit and stock price relationships at expiration for the following option positions. In each case, show the profit graph for each position at various stock prices and then aggregate the profits for the separate positions at each stock price to generate the profit graph for

Determine the break-even prices at expiration for the following:a. A straddle purchase formed with ABC call and put options, each with exercise prices of \(\$ 60\) and premiums of \(\$ 5\).b. A straddle write formed with \(\mathrm{ABC}\) call and put options, each with exercise prices of \(\$ 40\)

Compare and contrast buying stock with a call purchase strategy.

Compare and contrast selling stock short with a put purchase strategy.

Explain what arbitrageurs would do if the price of an American call on \(\mathrm{ABC}\) stock with an exercise price of \(\$ 50\) were priced at \(\$ 9\) when the underlying price on \(\mathrm{ABC}\) stock were trading at \(\$ 60\). What impact would their actions have in the option market on the

Explain what arbitrageurs would do if the price of an American put on \(A B C\) stock with an exercise price of \(\$ 50\) were priced at \(\$ 9\) when the underlying futures price on \(\mathrm{ABC}\) stock were trading at \(\$ 40\). What impact would their actions have in the option market on the

Explain intuitively why call and put options are more valuable the greater their underlying security's variability.

Given a call and put with an exercise price of \(\$ 60\), a risk-free discount bond with face value of \(\$ 60\) and the same maturity as the options' expiration:a. Construct a table of expiration values (or cash flows) of a stock and put portfolio for stock values of \(\$ 40, \$ 50, \$ 60, \$

Explain the role and functions of the Option Clearing Corporation.

Suppose in February Ms. X sold a June ABC 100 call contract to Mr. Z for \$5, then later closed her position by buying a June ABC 100 for \(\$ 7\) from Mr. Y. Explain how the OCC would handle these contracts.

Explain the various types of option transactions.

Explain why option holders should, in most cases, close their options instead of exercising. Under what condition, would it be beneficial to exercise a call option early?

Find descriptions, recent prices, and other information on the call and put options of a selected stock. From the loaded stock's menu screen, bring up:a. OMONb. CALLc. PUTd. GV, Volatility Graphe. HVT, Historical Volatility Tablef. CT, Contract Table

Examine several of the call and put options you selected in Exercise 1 from screens shown on the option's menu screen: Option Ticker . View screens on the option's menu: DES and GP.Exercise 1.Find descriptions, recent prices, and other information on the call and put options of a selected stock.

Select a stock and bring up its equity screen: Stock Ticker . Using the Bloomberg OSA screen, select a call and put option on the stock and evaluate the following option strategies on the stock with a profit graph:a. Call purchaseb. Call salec. Put purchased. Put salee. Covered call writef. Covered

Evaluate a covered write position for a selected stock using Bloomberg's Covered Option Write screen (CWS) for a loaded stock.

Use the Chart screen (Chart \) ) to create multigraphs for the historical prices of the stock, call, and put options you analyzed.Select a time period that the contract was active. On the Chart Menu screen, select Standard G chart; once you have loaded your securities, go to "Edit" to put your

Use the GV screen for a loaded stock to evaluate its historical volatility, the stock price, and the price of an option on the stock (you can load your option on the screen). Examine the relations between the option price, stock price, and volatility.

Answer the following:a. What right does a September \(\$5.00\) wheat futures call option contract give the holder?b. What right does a September \(\$5.00\) wheat futures put option contract give the holder?c. What conditions are necessary to make the spot options and futures options equivalent?d.

Explain the mechanics of exercising and closing an \(\mathrm{S \& P} 500\) futures call options contract with an exercise price of 2,250 and multiplier of \(\$ 250\) when the underlying futures contract is trading at 2,750. Explain the assigned writer's position and responsibility.

Explain the mechanics of exercising and closing an \(\mathrm{S \& P} 500\) futures put options contract with an exercise price of 2,250 and multiplier of \(\$ 250\) when the underlying futures contract is trading at 2,000. Explain the assigned writer's position and responsibility.

Show graphically the profit and futures price relationships at expiration for the following positions on an S\&P 500 futures options with an exercise price of 2,250 , multiplier of \(\$ 250\), and call and put prices both equal to 75 . Evaluate at futures prices at expiration or when the contract

Explain what arbitrageurs would do if the price of a S\&P 500 futures call with an exercise price of 2,500 ( \(\$ 250\) multiplier) were priced at 45 when the underlying futures price was trading at 2,550. What impact would their actions have in the option market on the call's price?

Explain what arbitrageurs would do if the price of a S\&P 500 futures put with an exercise price of 2,500 ( \(\$ 250\) multiplier) were priced at 45 when the underlying futures price was trading at 2,450. What impact would their actions have in the option market on the put's price?

Explain the mechanics of exercising and closing a five-year T-note futures call options contract with an exercise price of \(\$ 120,000\) (for T-note with \(\$ 100,000\) face value) when the underlying futures contract is trading at \(\$ 125,000\). Explain the assigned writer's position and

Explain the mechanics of exercising and closing a five-year T-note futures put options contract with an exercise price of \(\$ 120,000\) (for T-note with \(\$ 100,000\) face value) when the underlying futures contract is trading at \$115,000. Explain the assigned writer's position and

Show graphically the profit and futures price relationships at expiration for the following positions on five-year T-note futures options with an exercise price of \(\$ 120,000\) (for T-note with \(\$ 100,000\) face value), and a call and a put both priced at \(\$ 2,000\). Evaluate at futures

Explain what arbitrageurs would do if the price of a five-year T-note futures call with an exercise price of \(\$ 120,000\) were priced at \(\$ 1,750\) when the underlying futures price was trading at \(\$ 122,000\). What impact would their actions have in the option market on the call's price?

What is the actual exercise price and premium for a September Eurodollar futures call with an exercise price quoted in terms of the CME index of \(99.00\left(R_{\mathrm{D}}=1.00 \%\right)\) and premium quoted at0.05 ( 5 basis points). Explain the mechanics of exercising and closing the September

What is the actual exercise price and premium for a September Eurodollar futures put with an exercise price quoted in terms of the CME index of \(99.00\left(R_{\mathrm{D}}=1.00 \%\right)\) and premium quoted at 0.Explain the mechanics of exercising and closing the September Eurodollar futures put

Show graphically the profit and futures price relationships at expiration for the following positions on a September euro futures options with an exercise price of \$1.115/euro, contract size of 125,000 euros, and call and put price of \(\$0.02 / €\). Evaluate at futures prices at expiration or

Show graphically the profit and futures price relationships at expiration for the following positions on a November corn futures options with an exercise price of \(\$3.20 /\) bushel, size of 5,000 bushels, and call and put price of \(\$0.20 /\) bushel. Evaluate at futures prices at expiration or

Show graphically and in a table the profit and T-bond price relationships at expiration for the following positions on OTC T-bond options. In each case, assume that the T-bond spot call and put options each have exercise prices of \(\$ 100,000\) and premiums of \(\$ 1,000\), and that there is no

Show graphically and in a table the profit and LIBOR relationships at expiration for the following positions on interest rate options. In each case, assume that the interest rate call and put options each have exercise rates of \(2 \%\), a LIBOR reference rate, notional principals of \(\$ 20\)

Cincy Land Developers is a real estate development company with a shopping mall development project currently valued at \(\$ 20\) million. The Cincy Company financed the project by borrowing fromthe Midwest Bank. The loan calls for a \(\$ 25\) million principal at the end of four years (no coupon

Alcibiades Thoroughbred Inc. is a small horse syndicate that owns a three-year-old racehorse named Butterfly Spread. Based on Butterfly Spread's racing record and potential breeding value, the estimated value of the horse and therefore Alcibiades Thoroughbred Inc. is \$1,000,000. Alcibiades has 10

Brandy Inc. is a \$100 million oil company. The company has one million shares outstanding and no debt. Expecting the price of oil to increase, Brandy Inc. is planning to raise \(\$ 10\) million through a rights offering to finance the purchase of an oil well. The company has decided to make the

Given the following features of the \(\mathrm{ABC}\) convertible bond- Coupon rate (annual) \(=5 \%\)- Face value \(=F=\$ 1,000\)- Maturity \(=10\) years- Callable at \(\$ 1,100\)- YTM on a comparable, nonconvertible bond \(=6 \%\)- Conversion ratio \(=10\) shares- Current stock price \(=S_{0}=\$

Find descriptions, recent prices, and other information on call and put options for some of the following: an equity index, commodity futures options, index futures options, currency futures options, Eurodollar futures options, and T-note futures option. For information on how to find futures and

Evaluate the following option strategies with a profit graph for some of the call and put options you selected:a. Call purchaseb. Call salec. Put purchased. Put salee. Covered call writef. Covered put write g. Straddle purchase h. Straddle sale For a guide on using the OSA screen, see "Bloomberg's

Select several of the options you evaluated and bring up their screens. Using the Bloomberg OSA screen, select a call and put on each of the futures options and create a call price curve and put price curve for the current date and \(I V\) line using the expiration date. For a guide on using the

Find descriptions, recent prices, and other information on an equity warrant. To search for warrants, go to the SECF screen. On the screen, click "Equity" from the "Category" dropdown, click the "Warrants" tab, and select type of warrants from the "Type" download. Using the Bloomberg OSA screen,

Find descriptions, recent prices, and other information on a recent rights offering. To search for warrants, go to the IPO screen. On the screen, Click "Rights" box, and screen by "Offer Stage" (e.g., Trading), "Global Breakdown" (e.g., North America and United States), and "Industry" (e.g., All).

Find descriptions, recent prices, and other information on a convertible bond. Use SECF, SRCH, or CSCH to search for convertible bonds. Upload the convertible's menu screen (convertible's Ticker ). View screen to examine: DES, GP, YAS.

Use the Bloomberg SWPM screen to create and analyze a cap. Tabs to include in your analysis: Details, Resets, Cashflows, and Curves.

Use the Bloomberg SWPM screen to create and analyze a floor. Tabs to include in your analysis: Details, Resets, Cashflows, and Curves.

Evaluate the strategies below in terms of their profit and stock price relationships at expiration. In your evaluation, include a profit table that breaks down each strategy and identify the name of the strategy. Assume each stock position has 100 shares and each option contract represents 100

Evaluate the following index option positions in terms of their profit and spot index relations at expiration. In your evaluation include a profit table and graph that breaks down each strategy.a. A long straddle formed with a 2,500 S\&P 500 call trading at 50 and a \(2,500 \mathrm{S \& P} 500\)

Evaluate the following currency futures option strategies in terms of their profit and exchange rate relations at expiration. In your evaluation include a profit table and graph that breaks down each strategy.a. The purchase of a 150 (cents) British pound September futures call contract for 10

Suppose shortly after you purchased an XYZ September 50 call contract at \(\$ 3\) per call, the price of XYX increased to \(\$ 57\) causing the price of your call to rise to \(\$ 9\) per call. Evaluate in terms of their profit and stock price relations the following follow-up actions you could

Suppose shortly after you purchased an XYZ December 6o call for \(\$ 3\) the price of the stock decreased to \(\$ 56\) per share on speculation of a future announcement of low quarterly earnings for the XYZ Company, which you believe is warranted. Explain how you could profit at expiration by

Suppose after selling an XYZ December 50 call for \(\$ 3\) when the stock was at \(\$ 50\), the price of the stock increases to \(\$ 55\). Assume at the \(\$ 55\) stock price, the December 50 call is trading at \(\$ 6\) and there is an XYX December 55 call available that is trading at \(\$ 2.50\).

Compare and contrast the following strategies:a. Call Purchase and Leveraged Stock Purchaseb. Put Purchase and Synthetic Putc. In-the-Money Covered Call Write and Out-of-the-Money Covered Call Writed. Ratio Call Writes with different ratios of short calls to shares of stocke. Bull Spread and Bear

Suppose after you purchased an XYZ December 40 put at \(\$ 2\) the price of XYZ stock dropped from \(\$ 40\) per share to \(\$ 35\) per share, causing the 40 put to increase to \(\$ 6\). Evaluate in terms of profit and stock price relations the following follow-up strategies:a. Liquidationb. Do

Compare and contrast the following positions:a. Put Purchase and Short Saleb. Naked Put Write and Covered Call Writec. Covered Put Write and Naked Call Writed. Straddle, Strip, and Strap Purchases

List a number of strategies that will yield an Inverted V-shaped profit and stock price relationship at expiration.

List a number of strategies that will yield a V-shaped profit and stock price relationship at expiration.

Select a stock and bring up its equity screen: Stock Ticker . Using the Bloomberg OSA screen, select several call and put options on the stock and evaluate some of the following option strategies on the stock with a profit graph:a. Simulated Put: Long in a call and short in a stock on a 1:1

Examine the historical prices of the stock and one of its call and puts options Select a time period that the options were active.a. Use the Chart screen (Chart ) to create multigraphs for the stock, call, and put. On the Chart Menu screen, select the Standard G chart; once you have loaded your

Select an S\&P 500 futures option and bring up its equity screen: SPA \( to bring up S\&P futures; type EXS to bring up futures with different expirations; select a futures and bring up is menu screen: futures ticker (e.g., SPH7 for March 17 S\&P futures); on the futures screen, type OSA; on the

Examine the historical prices of the S\&P futures and some of the futures call and futures put options you selected. Select a time period that the contracts were active.a. Use the Chart screen (Chart ) to create multigraphs for the futures, call futures, and put futures. On the Chart Menu screen,

Select a CBT T-note futures (e.g., five-year T-note: FVA ; EXS to find expirations; \(\mathrm{FVH} 7 to load March 2017 five-year T-Note futures). On the selected futures screen, type OSA to bring up the OSA screen, and select "Listed Options" on the contract from the red "Positions" dropdown tab

Examine the historical prices of the \(\mathrm{T}\)-note futures and some of the futures call and futures puts options you selected in Exercise 5. Select a time period that the contracts were active.a. Use the Chart screen (Chart ) to create multigraphs for the futures, call futures, and put

Use CTM to identify the currency futures that have option contracts: Enter CTM; select "Currencies" and then select "Yes" on the "Options" tab to see currency futures with options contracts on them. Upload the currency futures contract with the selected options (e.g., BPA for British pound

Examine the historical prices of currency futures and the futures call and futures put options you selected in Exercise 7.Select a time period that the contracts were active.a. Use the Chart screen (Chart ) to create multigraphs for the futures, call futures, and put futures. On the Chart Menu

Select a commodity futures option (e.g., a CBT commodity futures option). Use CTM to identify commodities that have option contracts: Enter CTM; Select commodity futures (e.g., corn) and then select "Yes" on the "Options" tab to see futures with options contracts on them; type EXS to find

Examine the historical prices of commodity futures and the futures call and futures puts options you selected in Exercise 9.Select a time period that the contracts were active.a. Use the "Chart" screen (Chart ) to create multigraphs for the futures, call futures, and put futures. On the Chart Menu

Select a narrow-based spot index (e.g., S\&P Small Cap 600, GNA ). Use SECF to identify indexes that have option contracts: Enter SECF; select index/Stats from "Category" dropdown; click "Opts" tab for a listing of index options and their tickers. Load index options: Ticker \(\). On the selected

Showing 100 - 200

of 882

1

2

3

4

5

6

7

8

9

Step by Step Answers