New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

accounting

Advanced Accounting 11th Edition Floyd A. Beams, Joseph H. Anthony, Bruce Bettinghaus, Kenneth Smith - Solutions

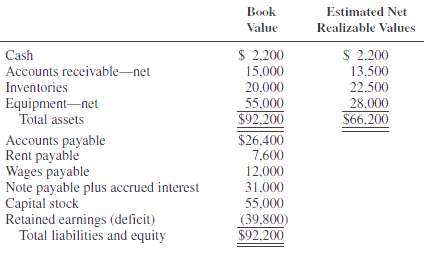

Hanna Corporation filed a petition under Chapter 7 of the bankruptcy act on June 30, 2011. Data relevant to its financial position as of this date are: REQUIRED1. Prepare a statement of affairs assuming that the note payable and interest are secured by a mortgage on the equipment and that wages

The unsecured creditors of Dawn Corporation filed a petition under Chapter 7 of the bankruptcy act on July 1, 2011, to force Dawn into bankruptcy. The court order for relief was granted on July 10, at which time an interim trustee was appointed to supervise liquidation of the estate. A listing of

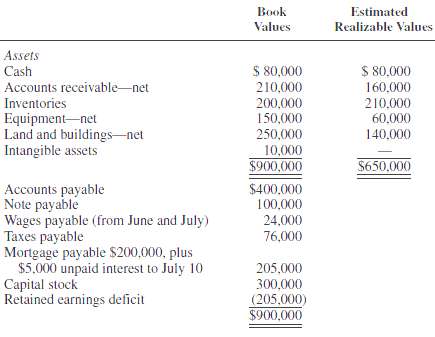

The balance sheet of Everlast Window Corporation at June 30, 2011, contains the following items:AssetsCash................. $ 40,000Accounts receivable—net........ 70,000Inventories.............. 50,000Land................. 30,000Building—net.............. 200,000Machinery—net.............

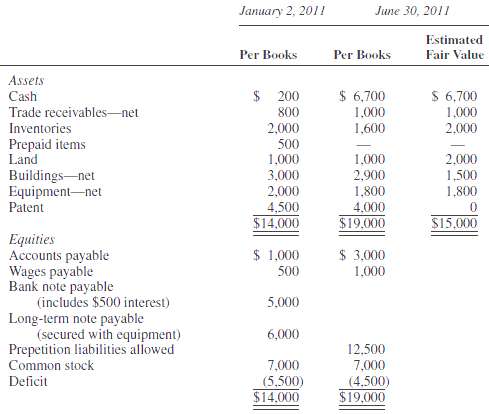

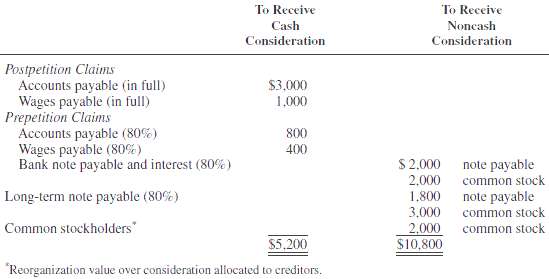

Lowstep Corporation filed for relief under Chapter 11 of the bankruptcy act on January 2, 2011. A summary of Lowstep's assets and equities on this date, and at June 30, 2011, follows. Estimated fair values of Lowstep's assets at June 30 are also shown. The parties in interest agree to a

If a parent in accounting for its subsidiary amortizes patents on its separate books, why do we include an adjustment for patents amortization in the consolidation workpaper?

How is noncontrolling interest share entered in consolidation workpapers?

What organization provides accounting standards for state and local governmental units? What organization or organizations preceded this group?

What is the GAAFR? Who creates the GAAFR?

What are the characteristics of a government?

Why do governmental entities use fund accounting? How many funds might be used by a single governmental unit? How many fund types?

Distinguish between governmental funds, proprietary funds, and fiduciary funds. Which funds are classified as governmental funds?

List the five types of governmental funds. What are the primary distinctions among them?

List the two types of proprietary funds. What distinguishes them from each other?

What is the accounting equation for a proprietary fund?

Why aren’t fixed assets recorded in the accounts of a general fund? Where are they recorded?

What is the modified accrual basis of accounting? Which funds utilize the modified accrual basis of accounting?

What does measurement focus mean? What two focuses are used in governmental accounting? Which fund types use each?

What types of revenue do governments have? How do nonexchange transactions differ from exchange transactions?

How does the accounting treatment of a nine-month note payable differ from the accounting treatment of a five-year note payable within a governmental fund? Why?

Are interfund transfers expenditures? Expenses? Explain.

What is an appropriation? How can budgetary approval be arranged to give the legislative body maximum control over the budget? How can it be arranged to give the executive maximum flexibility?

List the required governmental fund and proprietary fund financial statements under GASB 34. On what basis of accounting are these statements prepared?

List the authoritative documents available to financial statement preparers and auditors related to governmental accounting and financial reporting. Which is the most authoritative according to GASB 55?

Distinguish between the various types of interfund activity.

How does an expenditure differ from an expense? Identify the funds that report expenditures and those that report expenses.

What are the three sections of a CAFR? Briefly identify the contents of each section.

How do operational accountability and fiscal accountability differ? In what context are they used?

1. Which of the following items has the greatest GAAP authority under SAS 69?a. GASB implementation guidesb. Consensus positions of GASB’s Emerging Issues Task Forcec. GASB statements and interpretationsd. FASB statements and interpretations2. The primary emphasis in accounting and reporting for

1. Depreciation expense accounts would likely be found in thea. General fundb. Capital projects fundc. Debt service fundd. Enterprise fund2. The government-wide statements of a state governmenta. May not be issued separately from the comprehensive annual financial reportb. Are prepared on both the

1. Which of the following is considered an exchange transaction under GASB 33?a. A city receives a federal grantb. A bus driver collects bus fare from a riderc. Property taxes are collected from a homeownerd. An employer withholds state income tax from employee paychecks2. One would not expect to

1. Which of the following is not a governmental fund?a. Special revenue fundb. Debt service fundc. Trust fundd. General fund2. Which of these funds generally follows the accrual basis of accounting?a. General fundb. Internal service fundc. Debt service fundd. Special revenue fund3 Which of the

1. Which of the following are eliminated from the financial statements under GASB 34?a. General long-term debt account groupb. General fixed asset account groupc. Both a and bd. None of the above2. An expense would be reported in which of the following funds?a. General fundb. Internal service

Identify each of the fund types described.1. A fund that is used to report assets held in a trustee capacity for others and that cannot be used to support the government’s own programs.2. A fund used to report any activity for which a fee is charged to external users for goods and services.3. A

Use transaction analysis to determine the effects of each of the following transactions in the general fund.1. Salaries paid totaled $30,000. Additional salaries incurred, but not paid, totaled $2,500.2. Levied property taxes of $100,000; $98,000 was collected during the year. The balance is

Repeat Exercise 19-7, this time assuming that the transactions involve a proprietary activity instead of a general governmental activity.

For each of the following events or transactions, identify the fund or funds that will be affected.1. The principal, interest, and related charges from a city’s general long-term debt bond issue will be handled in a fund established for that purpose.2. A wealthy citizen donates $10,000,000 for

For each of the following events or transactions, identify the fund or funds that will be affected.1. The Board of County Commissioners approved the construction of a new town band shell.2. A central computing center was established to handle the data processing needs of a municipality.3. A local

For each of the following events or transactions, identify the fund or funds that will be affected.1. A new city government establishes an employee pension program.2. A utility department constructs a new building.3. A truck is purchased for use at the centralized storage center.4. A new fleet of

The City of Sioux Falls entered into a number of transactions for the current fiscal year. Identify the fund or funds affected by each transaction and determine how each transaction will affect the accounting equation of the particular fund.1. Sioux Falls paid salaries to general government

Perez County entered into a number of transactions for the current fiscal year. Identify the fund or funds affected by each transaction and determine how each transaction will affect the accounting equation of the particular fund.1. Perez County issued $10 million of general obligation bonds at par

List the required governmental fund financial statements under GASB 34 . On what basis of accounting are these statements prepared?

What is the purpose of a capital projects fund? Are all general fixed assets of a governmental unit acquired through capital projects funds? Explain.

How are capital projects funds financed, and when would a capital projects fund be terminated?

How do the purchases and consumption methods of accounting for inventory differ?

Are debt service funds used to account for debt service on all long-term obligations of a governmental unit? If not, which long-term debt obligations are excluded?

Describe a transaction that would affect the general fund and the debt service fund at the same time.

How do special assessment levies differ from general tax levies?

Which funds may be used to account for the activities of a general governmental special assessment construction project with long-term financing? Explain.

How are capital leases recorded in governmental funds?

Assume that supplies on hand at the beginning of the year amount to $60,000 and that supply purchases during the year are $400,000. Supplies on hand at year-end are $40,000, and the consumption basis of accounting for supplies is used. What adjusting entry for supplies should be made at year-end?

What is the role of a subsidiary ledger in a governmental entity?

The Village of Lester had appropriations of $250,000 for the current fiscal year. If $175,000 worth of items has been ordered but only $150,000 of the $175,000 has been received, what amount can city officials order prior to year-end? What happens if they have not spent the full $250,000 prior to

How does a permanent fund differ from a special revenue fund? A private-purpose trust fund?

How can you determine whether or not a governmental fund should be considered major?

What is included on a budgetary comparison schedule? Is such a schedule required to be included in a CAFR?

How is a conversion worksheet used? Why is it necessary?

List three items that might appear on the reconciliation between the governmental fund balance sheet and the government-wide statement of net assets. List three items that might appear on the reconciliation between the governmental fund operating statement and the government-wide statement of

1. Which of the following statements regarding budgetary accounting is true?a. When the budget is recorded, estimated revenues are debited.b. Budgetary accounts are never closed.c. Encumbrance is another term for appropriation.d. Budgeted revenues can be classified by source or character class.2.

1. The accounts “estimated revenues” and “appropriations” appear in the trial balance of the general fund. These accounts indicate:a. The use of cash basis accountingb. The use of accrual basis accountingc. The formal use of budgetary accountsd. The informal use of budgetary accounts2. When

1. When equipment was purchased with general fund resources, which of the following accounts would have been increased in the general fund?a. Due from general fixed assets account groupb. Expendituresc. Appropriationsd. No entry should be made in the general fund2. Which of the following funds

1. Howard City should use a capital projects fund to account for:a. Proceeds of a capital grant to finance a new civic center that will not provide services primarily on a user-charge basisb. Construction of sewer lines by the water and sewer utility to be financed by user costsc. The accumulation

1. If numerous funds are maintained, which of the following transactions would typically not be reported in a municipality’s general fund?a. The collection of property taxesb. The purchase of office equipmentc. The receipt of grant funds for local youth programsd. The payment of salaries to

1. The following information pertains to Walnut Corners:2011 governmental fund revenues that became measurable and available in time to be used for payment of 2011 liabilities..... $16,000,000Revenues earned in 2009 and 2010 and included in the$16,000,000 indicated....................

The following events and transactions relate to the levy and collection of property taxes for Jedville Township:March 21, 2011—Property tax bills for $2,500,000 are sent to property owners. An estimated 2% of the property tax levies are uncollectible. The taxes are due on May 1.May 4,

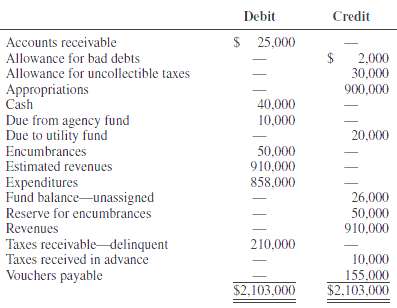

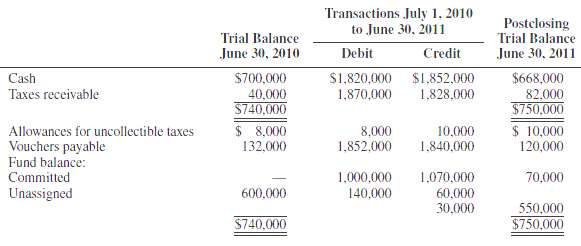

A general ledger trial balance for Any City contained the following balances at June 30, 2011, just before closing entries were made:Due from other funds......... $ 600Fund balance—unassigned........ 3,000Estimated revenues........... 18,000Revenues..............

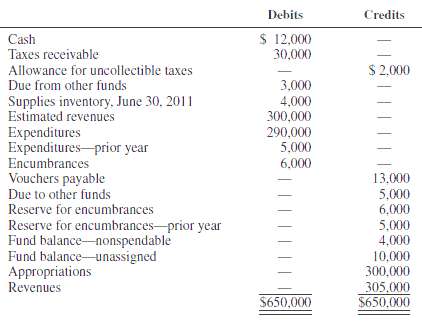

A general ledger trial balance at June 30, 2011, for Millar City is as follows: Millar City uses a purchases basis in accounting for supplies. Open encumbrances are considered constrained by the highest decision-making level of the city.REQUIREDPrepare a fund balance sheet as of June 30,2011.

The trial balance of the general fund of Madelyn City before closing at December 31, 2011, contained the following accounts and balances:Fund balance—unassigned......... $ 25,000Estimated revenues............ 100,000Appropriations............. 95,000Encumbrances.............. 4,000Reserve for

Prepare entries in the general fund to record the following transactions and events:1. Estimated revenues for the fiscal year were $250,000 and appropriations were $248,000.2. The tax levy for the fiscal year, of which 99% is believed to be collectible, was $200,000.3. Taxes collected were

Prepare the journal entries required to record the following transactions in the general fund of Rochester Township.1. Borrowed $75,000 by issuing six-month tax anticipation notes.2. Ordered equipment with an estimated cost of $33,000.3. Received the equipment along with an invoice for its actual

For each of the following transactions, note the fund(s) affected, and prepare appropriate journal entries.1. General obligation bonds with a par value of $750,000 are issued at $769,000 to finance construction of a government office building.2. A Community Block Development Grant in the amount of

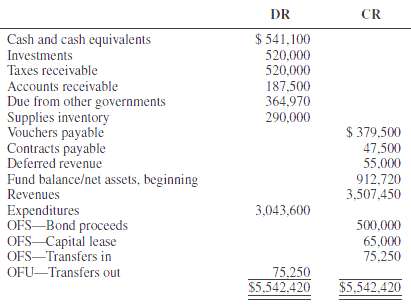

The postclosing trial balance for the Village of Alantown general fund at June 30, 2011, shows the following ledger account balances:DebitsCash......................... $410,000Investments..................... 300,000Tax receivable—delinquent............. 150,000Accounts

The following data are available from the City of Boulder’s financial records on September 30, 2011:a. The net change in fund balance—total governmental funds for the city is $1,408,950.b. The city purchased general fixed assets at a historical cost of $225,000 during the year. No depreciation

The unadjusted trial balance for the general fund of the City of Orchard Park at December 31, 2011, is as follows: Supplies on hand at December 31, 2011, are $3,000. The $50,000 encumbrance relates to equipment ordered November 28 for the Department of Public Works but not received by

The preclosing account balances of the general fund of the City of Batavia on June 30, 2012, were as follows:DebitsCash...................... $ 80,000Taxes receivable—delinquent............ 160,000Due from County................. 18,000Estimated revenues.................

The Town of Tyler approved the following general fund budget for the fiscal year July 1, 2011, to June 30, 2012:TOWN OF TYLER GENERAL FUND BUDGET SUMMARYFOR THE YEAR JULY 1, 2011 TO JUNE 30, 2012Revenue SourcesTaxes.................. $ 250,000Licenses and permits............ 20,000Intergovernmental

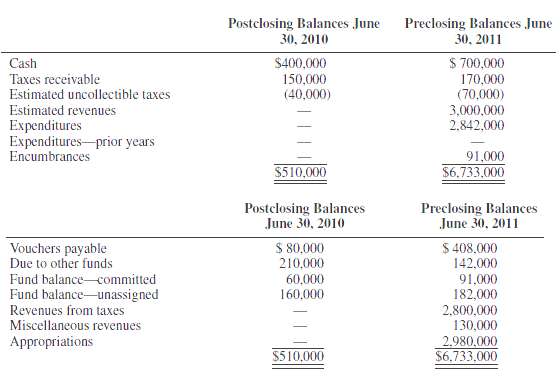

The post-closing trial balance for the City of Fort Collins governmental funds at June 30, 2011, shows the following ledger account balances: ADDITIONAL INFORMATION1. During the year, Fort Collins purchased $9,000 in equipment, which was not depreciated.2. Fort Collins also has other fixed

The following summary of transactions was taken from the accounts of the Oslo School District general fund before the books had been closed for the fiscal year ended June 30, 2011: ADDITIONAL INFORMATION1. The estimated taxes receivable for the year ended June 30, 2011, were $2,870,000, and

The following information was abstracted from the accounts of the general fund of the City of Lahti after the books had been closed for the fiscal year ended June 30, 2011: ADDITIONAL INFORMATION The budget for the fiscal year ended June 30, 2011, provided for estimated revenues of $2,000,000 and

The following information regarding the fiscal year ended December 31, 2011, was drawn from the accounts and records of the Volendam County general fund:Revenues and Other Asset InflowsTaxes................. $10,000,000Licenses and permits........... 2,000,000Intergovernmental grants...........

The Town of Lilehammar has $3,000,000 of 6 percent bonds outstanding. Interest on the general obligation, general government indebtedness is payable semiannually each March 31 and September 30. December 31 is the fiscal year-end. Record the following transactions in the town’s debt service

The City of Stockholm authorized construction of a $600,000 addition to the municipal building in September 2011. The addition will be financed by $200,000 from the general fund and a $400,000 serial bond issue to be sold in April 2012.REQUIREDPrepare journal entries for the capital projects fund

On June 15, 2011, Malmo City authorizes the issuance of $500,000 par of 6 percent serial bonds to be issued on July 1, 2011, and to mature in annual serials of $100,000 beginning on July 1, 2012. The proceeds of the bond issue are to be used to finance a new tourist rest area.During the fiscal year

In a special election held on May 1, 2011, the voters of the City of Cerone approved a $10,000,000 issue of 6 percent general obligation bonds maturing in 20 years. The proceeds of this sale will be used to help finance the construction of a new civic center. The total cost of the project was

The City of Catalina authorized the construction of a new recreation center at a total cost of $1,000,000 on June 15, 2011. On the same date, the city approved a $1,000,000, 8 percent, 10-year general obligation serial bond issue to finance the project. During the year July 1, 2011, to June 30,

What is the accounting concept of a business combination?

Is dissolution of all but one of the separate legal entities necessary in order to have a business combination? Explain.

What are the legal distinctions between a business combination, a merger, and a consolidation?

When does goodwill result from a business combination? How does goodwill affect reported net income after a business combination?

What is a bargain purchase? Describe the accounting procedures necessary to record and account for a bargain purchase.

1. A business combination in which a new corporation is formed to take over the assets and operations of two or more separate business entities, with the previously separate entities being dissolved, is a/an:a Consolidationb Mergerc Pooling of interestsd Acquisition2. In a business combination, the

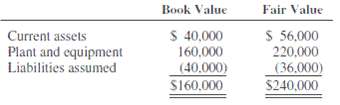

1. Pat Corporation paid $100,000 cash for the net assets of Sag Company, which consisted of the following: Assume Sag Company is dissolved. The plant and equipment acquired in this business combination should be recorded at:a $220,000b $200,000c $183,332d $180,0002. On April 1, Par Company paid

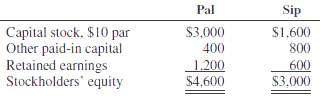

The stockholders' equities of Pal Corporation and Sip Corporation at January 1 were as follows (in thousands): On January 2, Pal issued 300,000 of its shares with a market value of $20 per share for all of Sip's shares, and Sip was dissolved. On the same day, Pal paid $10,000 to register and

Pan Company issued 480,000 shares of $10 par common stock with a fair value of $10,200,000 for all the voting common stock of Set Company. In addition, Pan incurred the following costs: Legal fees to arrange the business combination $100,000 Cost of SEC registration, including accounting and legal

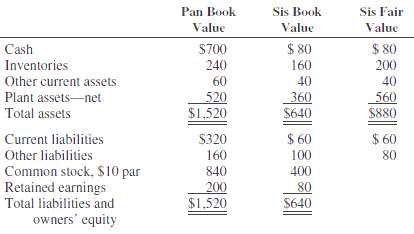

On January 1, Pan Corporation pays $400,000 cash and also issues 36,000 shares of $10 par common stock with a market value of $660,000 for all the outstanding common shares of Sis Corporation. In addition, Pan pays $60,000 for registering and issuing the 36,000 shares and $140,000 for the other

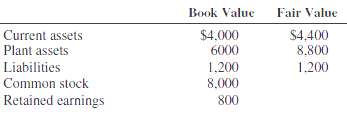

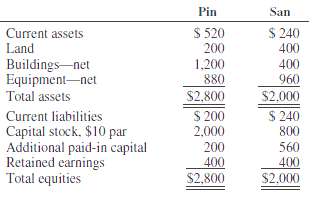

Comparative balance sheets for Pin and San Corporations at December 31, 2010, are as follows (in thousands): On January 2, 2011, Pin issues 60,000 shares of its stock with a market value of $40 per share for all the outstanding shares of San Corporation in an acquisition. San is dissolved. The

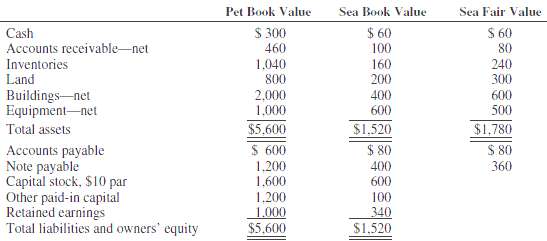

On January 2, 2011, Pet Corporation enters into a business combination with Sea Corporation in which Sea is dissolved. Pet pays $1,650,000 for Sea, the consideration consisting of 66,000 shares of Pet $10 par common stock with a market value of $25 per share. In addition, Pet pays the following

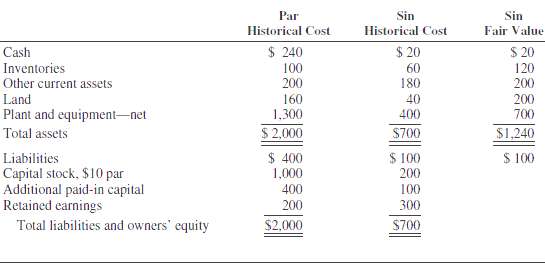

On January 2, 2011, Par Corporation issues its own $10 par common stock for all the outstanding stock of Sin Corporation in an acquisition. Sin is dissolved. In addition, Par pays $40,000 for registering and issuing securities and $60,000 for other costs of combination. The market price of Par's

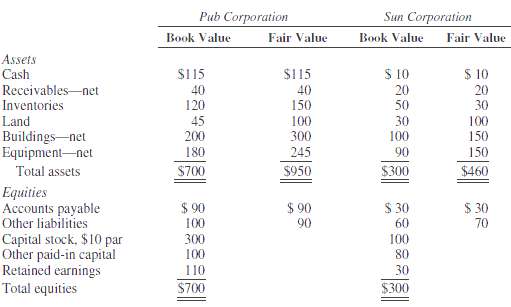

The balance sheets of Pub Corporation and Sun Corporation at December 31, 2010, are summarized with fair value information as follows (in thousands): On January 1, 2011, Pub Corporation acquired all of Sun's outstanding stock for $300,000. Pub paid $100,000 cash and issued a five-year, 12 percent

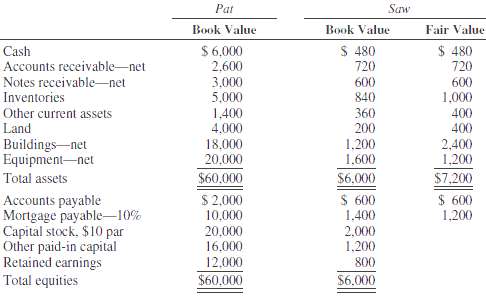

Pat Corporation paid $5,000,000 for Saw Corporation's voting common stock on January 2, 2011, and Saw was dissolved. The purchase price consisted of 100,000 shares of Pat's common stock with a market value of $4,000,000, plus $1,000,000 cash. In addition, Pat paid $100,000 for registering and

Assume that Wal-Mart decided to acquire major retailing rival Target Corporation on January 31, 2010. Target’s fiscal year ended on January 30, 2010, but you may assume that the year ends are identical to keep the calculations simpler. Visit the two firms’ Web sites to acquire their annual

Showing 6200 - 6300

of 107766

First

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

Last

Step by Step Answers