New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

accounting

Advanced Accounting 11th Edition Floyd A. Beams, Joseph H. Anthony, Bruce Bettinghaus, Kenneth Smith - Solutions

How are the workpaper procedures for the investment in subsidiary, income from subsidiary, and subsidiary’s stockholders’ equity accounts alike?

If a parent uses the equity method but does not amortize the difference between fair value and book value on its separate books, its net income and retained earnings will not equal its share of consolidated net income and consolidated retained earnings. How does this affect consolidation workpaper

Are workpaper adjustments and eliminations entered on the parent’s books? The subsidiary’s books? Explain.

The financial statement and trial balance workpaper approaches illustrated in the chapter generate comparable information, so why learn both approaches?

In what way do the adjustment and elimination entries for consolidation workpapers differ for the financial statement and trial balance approaches?

When is it necessary to adjust the parent’s retained earnings account in the preparation of consolidation workpapers? In answering this question, explain the relationship between parent retained earnings and consolidated retained earnings.

What approach would you use to check the accuracy of the consolidated retained earnings and noncontrolling interest amounts that appear in the balance sheet section of completed consolidation workpapers?

Explain why noncontrolling interest share is added to the controlling share of consolidated net income in determining cash flows from operating activities.

Controlling share of consolidated net income is a measurement of income to the stockholders of the parent, but does a change in cash as reflected in a statement of cash flows also relate to other stockholders of the parent?

1. Workpaper entries normally:a. Are posted to the general ledger accounts of one or more of the affiliatesb. Are posted to the general ledger accounts only when the financial statement approach is usedc. Are posted to the general ledger accounts only when the trial balance approach is usedd. Do

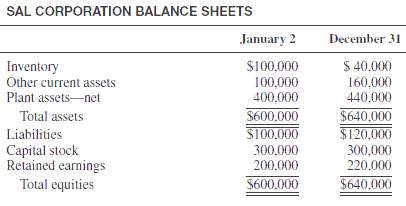

Pan Corporation purchased 80 percent of the outstanding voting common stock of Sal Corporation on January 2, 2011, for $600,000 cash. Sal's balance sheets on this date and on December 31, 2011, are as follows: ADDITIONAL INFORMATION1. Pan uses the equity method of accounting for its investment in

1. Peg Corporation owns a 70 percent interest in San Corporation, acquired several years ago at book value. On December 31, 2011, San mailed a check for $20,000 to Peg in part payment of a $40,000 account with Peg. Peg had not received the check when its books were closed on December 31. Peg

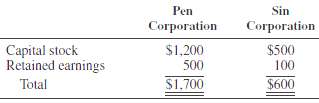

The stockholder's equity accounts of Pen Corporation and Sin Corporation at December 31, 2010, were as follows (in thousands) On January 1, 2011, Pen Corporation acquired an 80 percent interest in Sin Corporation for $580,000. The excess fair value was due to Sin Corporation's equipment being

1. In preparing a statement of cash flows, the cost of acquiring a subsidiary is reported:a. As an operating activity under the direct methodb. As an operating activity under the indirect methodc. As an investing activityd. As a financing activity2. In computing cash flows from operating activities

Information needed to prepare the Cash Flow from Operating Activities section of Par Corporation’s consolidated statement of cash flows is included in the following list:Amortization of patents.............$ 16,000Consolidated net income........... 150,000Decrease in accounts payable..........

The information needed to prepare the Cash Flow from Operating Activities section of Pro Corporation’s consolidated statement of cash flows is included in the following list:Cash received from customers........ $322,500Cash paid to suppliers............ 182,500Cash paid to employees............

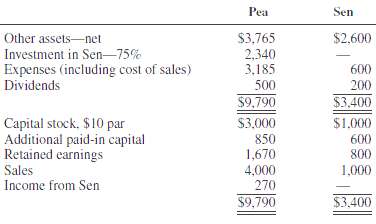

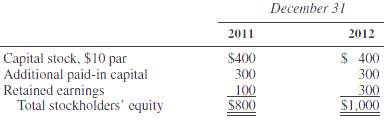

Pea Corporation purchased 75 percent of the outstanding voting stock of Sen Corporation for $2,400,000 on January 1, 2011. Sen's stockholders' equity on this date consisted of the following (in thousands): Capital stock, $10 par........$1,000 Additional paid-in capital........ 600 Retained earnings

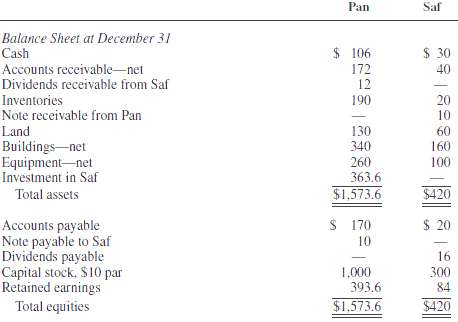

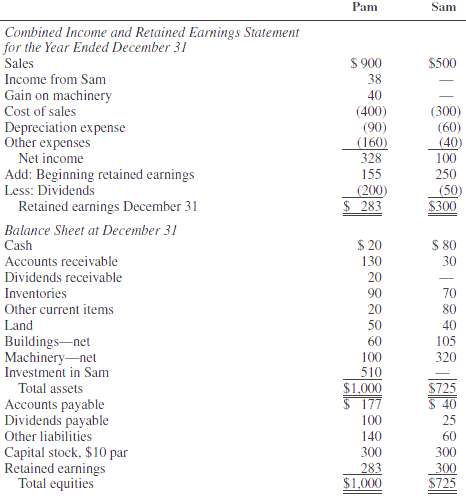

Pan Corporation acquired a 75 percent interest in Saf Corporation on January 1, 2011. Financial statements of Pan and Saf Corporations for the year 2011 are as follows (in thousands): REQUIRED: Prepare consolidation workpapers for Pan Corporation and Subsidiary for the year ended December 31,

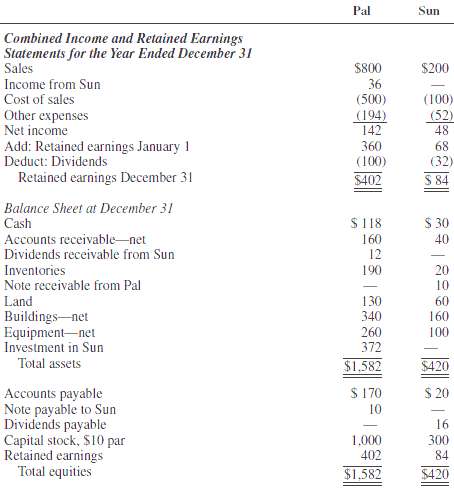

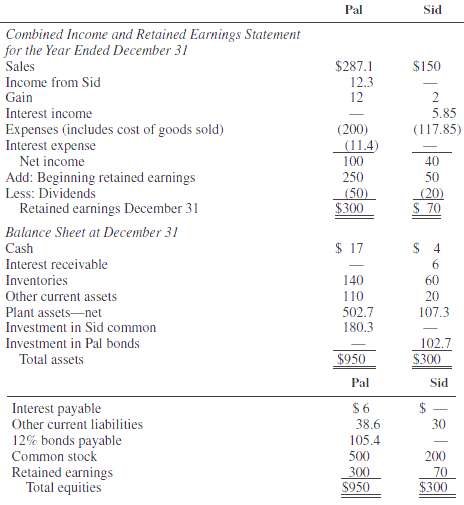

Pal Corporation acquired a 75 percent interest in Sun Corporation on January 1, 2011, for $360,000 in cash. Financial statements of Pal and Sun Corporations for 2011 are as follows (in thousands): REQUIRED: Prepare consolidation workpapers for Pal Corporation and Subsidiary for the year ended

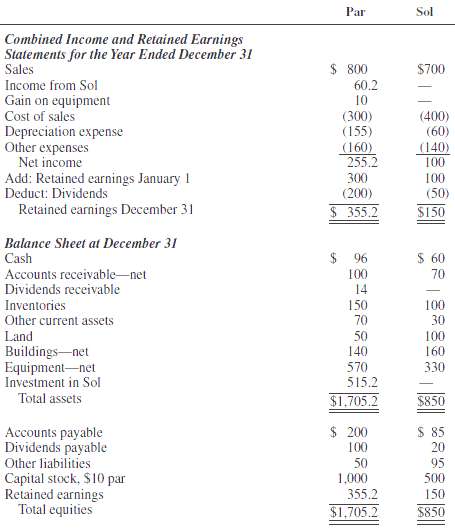

Par Corporation acquired a 70 percent interest in Sul Corporation's outstanding voting common stock on January 1, 2011, for $490,000 cash. The stockholders' equity (book value) of Sul on this date consisted of $500,000 capital stock and $100,000 retained earnings. The differences between the fair

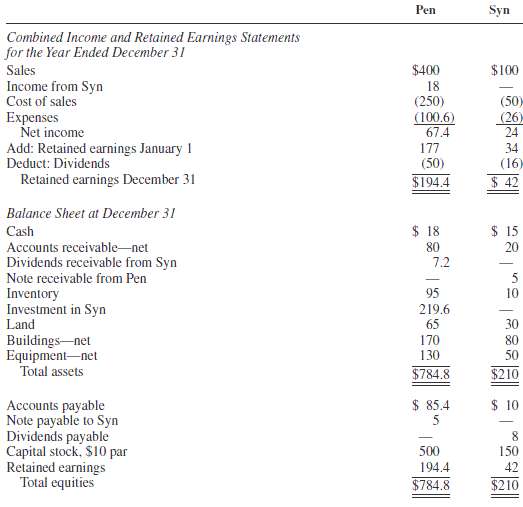

Separate company financial statements for Pen Corporation and its subsidiary, Syn Company, at and for the year ended December 31, 2012, are summarized as follows (in thousands): ADDITIONAL INFORMATION1. Pen Corporation acquired 13,500 shares of Syn Company stock for $15 per share on January 1,

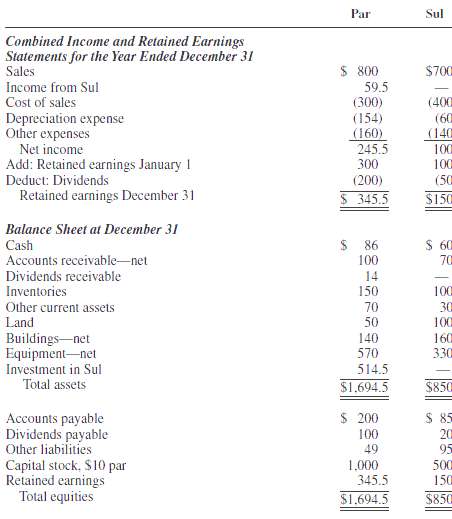

Par Corporation acquired a 70 percent interest in Sol Corporation's outstanding voting common stock on January 1, 2011, for $490,000 cash. The stockholders' equity of Sol on this date consisted of $500,000 capital stock and $100,000 retained earnings. The difference between the fair value of Sol

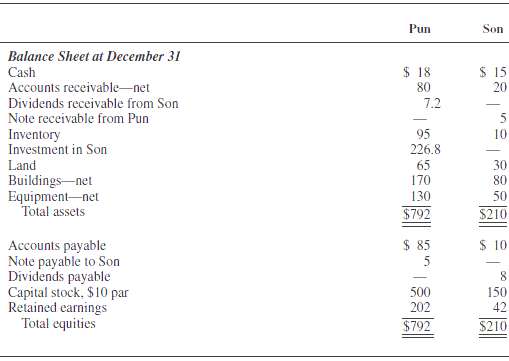

Separate-company financial statements for Pun Corporation and its subsidiary, Son Company, at and for the year ended December 31, 2012, are summarized as follows (in thousands): ADDITIONAL INFORMATION1. Pun Corporation acquired 13,500 shares of Son Company stock for $15 per share on January 1,

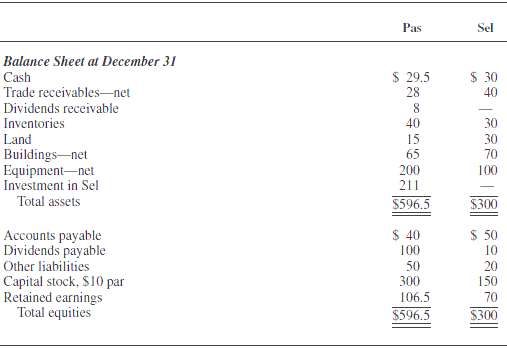

Pas Corporation acquired 80 percent of Sel Corporation's common stock on January 1, 2011, for $210,000 cash. The stockholders' equity of Sel at this time consisted of $150,000 capital stock and $50,000 retained earnings. The difference between the fair value of Sel and the underlying equity

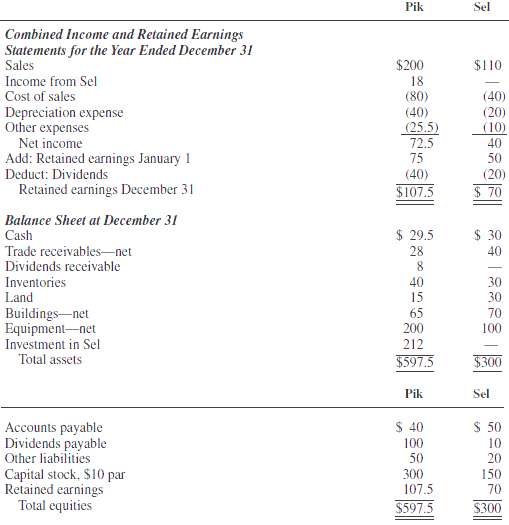

Pik Corporation acquired 80 percent of Sel Corporation's common stock on January 1, 2011, for $210,000 cash. The stockholders' equity of Sel at this time consisted of $150,000 capital stock and $50,000 retained earnings. The difference between the fair value of Sel and the underlying equity

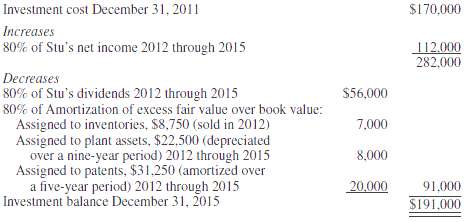

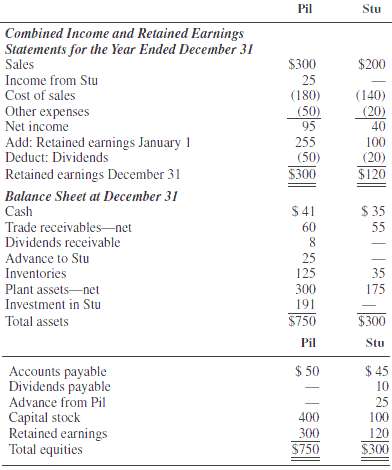

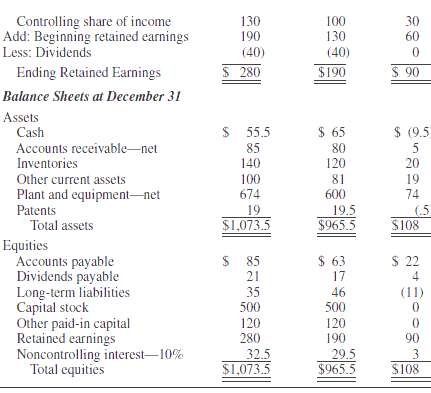

Pil Corporation paid $170,000 for an 80 percent interest in Stu Corporation on December 31, 2011, when Stu's stockholders' equity consisted of $100,000 capital stock and $50,000 retained earnings. A summary of the changes in Pil's Investment in Stu account from December 31, 2011, to December 31,

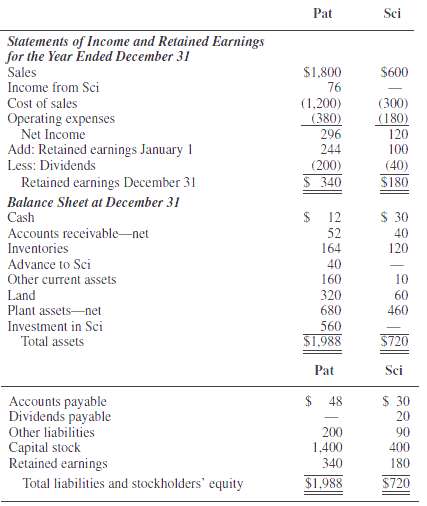

Pat Corporation acquired an 80 percent interest in Sci Corporation for $480,000 on January 1, 2011, when Sci's stockholders' equity consisted of $400,000 capital stock and $50,000 retained earnings. The excess fair value over book value acquired was assigned to plant assets that were undervalued by

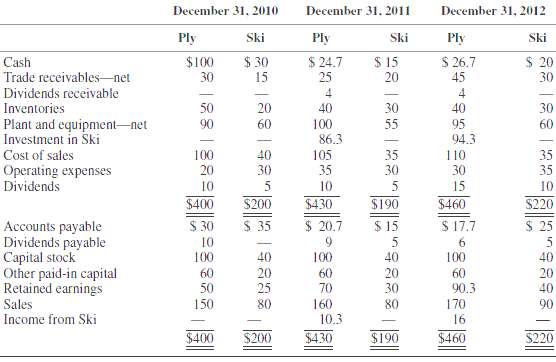

Comparative adjusted trial balances for Ply Corporation and Ski Corporation are given here. Ply Corporation acquired an 80 percent interest in Ski Corporation on January 1, 2011, for $80,000 cash. Except for inventory items that were undervalued by $1,000 and equipment that was undervalued by

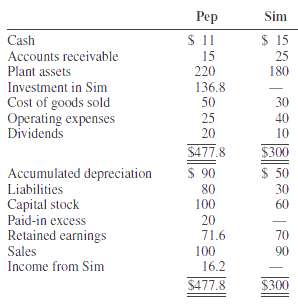

Pep Company paid $99,000 for a 90 percent interest in Sim on January 5, 2011, when Sim's capital stock was $60,000 and its retained earnings $20,000. Trial balances for the companies at December 31, 2014, are as follows (in thousands): The excess fair value over book value acquired was assigned

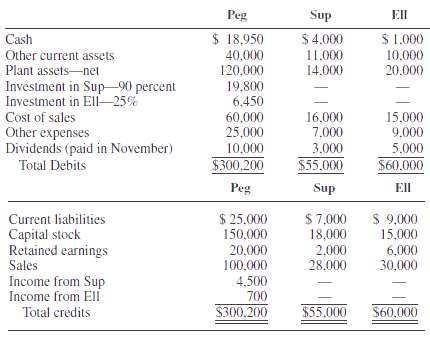

Peg Corporation owns 90 percent of the voting stock of Sup Corporation and 25 percent of the voting stock of Ell Corporation. The 90 percent interest in Sup was acquired for $18,000 cash on January 1, 2011, when Sup's stockholders' equity was $20,000 ($18,000 capital stock and $2,000 retained

The accountant for Pil Corporation collected the following information that he thought might be useful in the preparation of the company’s consolidated statement of cash flows (in thousands):Cash paid for purchase of equipment $ 270Cash paid for other expenses 450Cash paid to suppliers 630Cash

Comparative consolidated financial statements for Pes Corporation and its 90 percent-owned subsidiary, Sun Corporation, at and for the years ended December 31 are as follows: REQUIRED: Prepare a consolidated statement of cash flows for Pes Corporation and Subsidiary for the year ended December

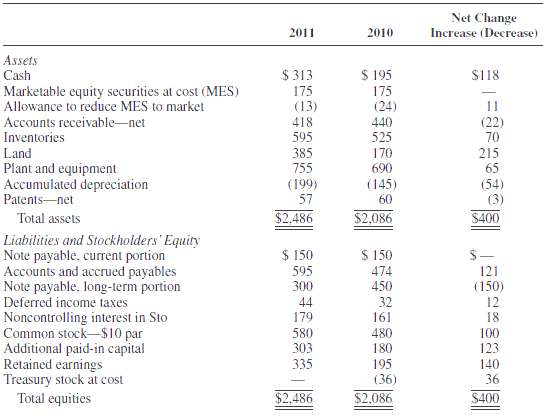

The consolidated workpaper balances of Puh, Inc., and its subsidiary, Sto Corporation, as of December 31 are as follows (in thousands): ADDITIONAL INFORMATION1. On January 20, 2011, Puh issued 10,000 shares of its common stock for land having a fair value of $215,000.2. On February 5, 2011, Puh

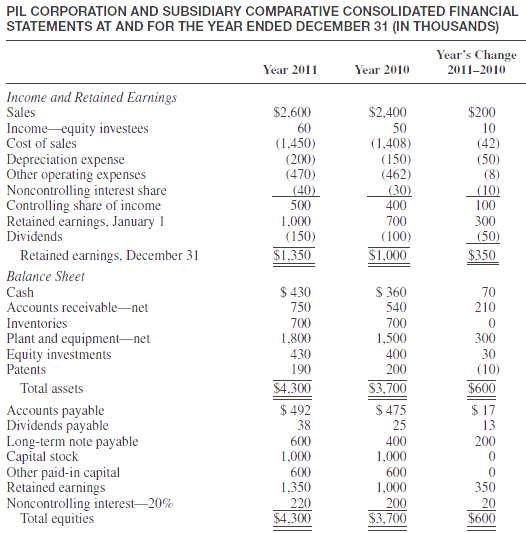

Comparative consolidated financial statements for Pil Corporation and its 80 percent-owned subsidiary at and for the years ended December 31 are summarized as follows: REQUIRED: Prepare a consolidated statement of cash flows for Pil Corporation and Subsidiary for the year ended December 31, 2011.

Explain the terms preacquisition earnings and preacquisition dividends.

How are preacquisition earnings accounted for by a parent under the equity method? How are they accounted for in the consolidated income statement?

Assume that an 80 percent investor of Sub Company acquires an additional 10 percent interest in Sub halfway through the current fiscal period. Explain the effect of the 10 percent acquisition by the parent on noncontrolling interest share for the period and on total noncontrolling interest at the

Isn’t preacquisition income really noncontrolling interest share?

How is the gain or loss determined for the sale of part of an investment interest that is accounted for as a one-line consolidation? Is the amount of gain or loss affected by the accounting method used by the investor?

When a parent sells a part of its interest in a subsidiary during an accounting period, is the income applicable to the interest sold up to the time of sale included in consolidated net income and parent income under the equity method? Explain.

Assume that a subsidiary has 10,000 shares of stock outstanding, of which 8,000 shares are owned by the parent. What equity method adjustment will be necessary on the parent books if the subsidiary sells 2,000 additional shares of its own stock to outside interests at book value? At an amount in

Assume that a subsidiary has 10,000 shares of stock outstanding, of which 8,000 shares are owned by the parent. If the parent purchases an additional 2,000 shares of stock directly from the subsidiary at book value, how should the parent record its additional investment? Would your answer have been

How do the treasury stock transactions of a subsidiary affect the parent’s accounting for its investment under the equity method?

Can gains or losses to a parent/investor result from a subsidiary’s/investee’s treasury stock transactions? Explain.

Do common stock dividends and stock splits by a subsidiary affect the amounts that appear in the consolidated financial statements? Explain, indicating the items, if any, that would be affected.

Pie Corporation increases its ownership interest in its subsidiary, Set Corporation, from 70 percent on January 1, 2011, to 90 percent at July 1, 2011. Set’s net income for 2011 is $100,000, and it declares $30,000 dividends on March 1 and $30,000 on September 1.REQUIRED: Show the allocation

On January 1, 2011, Pin Industries purchased a 40 percent interest in Sip Corporation for $800,000, when Sip’s stockholders’ equity consisted of $1,000,000 capital stock and $1,000,000 retained earnings. On September 1, 2011, Pin purchased an additional 20 percent interest in Sip for $420,000.

Pet Corporation owns 100 percent (300,000 shares) of the outstanding shares of Sap Corporation’s common stock on January 1, 2011. Its Investment in Sap account on this date is $4,400,000, equal to Sap’s $4,000,000 stockholders’ equity plus $400,000 goodwill. During 2011, Sap reports net

The balance of Pal Corporation’s investment in Sag Company account at December 31, 2010, was $436,000, consisting of 80 percent of Sag’s $500,000 stockholders’ equity on that date and $36,000 goodwill. On May 1, 2011, Pal sold a 20 percent interest in Sag (one-fourth of its holdings) for

Pig Corporation paid $1,274,000 cash for 70 percent of the common stock of Set Corporation on June 1, 2011. The assets and liabilities of Set were fairly valued, and any fair value/book value differential is goodwill. Data related to the stockholders’ equity of Set are as follows:Stockholders’

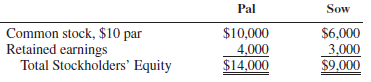

The stockholders’ equities of Pal Corporation and its 80 percent-owned subsidiary, Sow Corporation, on December 31, 2011, are as follows (in thousands):Pal’s Investment in Sow account balance on December 31, 2011, is equal to its underlying book value. On January 2, 2012, Sow issued 60,000

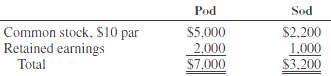

The stockholders' equities of Pod Corporation and its 80 percent-owned subsidiary, Sod Corporation, on December 31, 2011, appear as follows (in thousands): Pod's Investment in Sod account on this date is equal to its underlying book value. On January 1, 2012, Sod issues 30,000 previously unissued

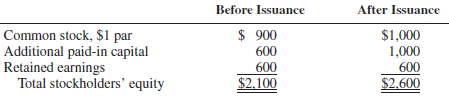

Pam Corporation owns two-thirds (600,000 shares) of the outstanding $1 par common stock of Sat Company on January 1, 2011. In order to raise cash to finance an expansion program, Sat issues an additional 100,000 shares of its common stock for $5 per share on January 3, 2011. Sat’s stockholders’

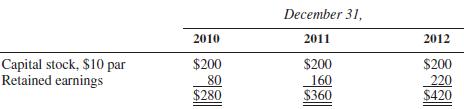

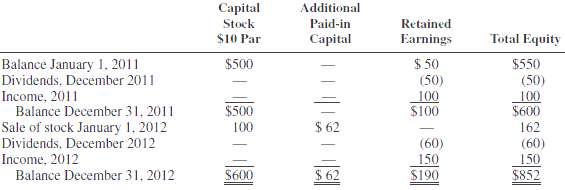

The stockholder’s equity of Sum Corporation at December 31, 2010, 2011, and 2012, is as follows (in thousands):Sum reported income of $80,000 in 2011 and paid no dividends. In 2012, Sum reported net income of $80,000 and declared and paid dividends of $10,000 on May 1 and $10,000 on November 1.

Pit Corporation acquired a 90 percent interest in Sad on July 1, 2012, for $675,000. The stockholders’ equity of Sad at December 31, 2011, was as follows (in thousands):Capital stock $500Retained

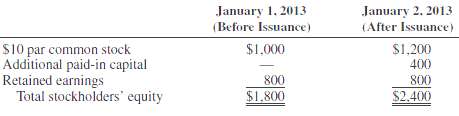

Pan Corporation purchased a 75 percent interest in Soy Corporation in the open market on January 1, 2012, for $690,000. A summary of Soy's stockholders' equity on December 31, 2011 and 2012, is as follows (in thousands): On January 1, 2013, Soy sold an additional 10,000 shares of its own $10 par

Put Corporation’s Investment in Son Company account had a balance of $475,000 at December 31, 2011. This balance consisted of goodwill of $35,000 and 80 percent of Son’s $550,000 stockholders’ equity. On January 2, 2012, Son increased its outstanding shares from 10,000 to 12,000 shares by

Pat Company paid $1,800,000 for 90,000 shares of Sir Company's 100,000 outstanding shares on January 1, 2011, when Sir's equity consisted of $1,000,000 of $10 par common stock and $500,000 retained earnings. The excess fair value over book value was goodwill. On January 2, 2013, Sir sold an

A summary of changes in the stockholders' equity of Sin Corporation from January 1, 2011, to December 31, 2012, appears as follows (in thousands): Par Corporation purchases 40,000 shares of Sin's outstanding stock on July 1, 2011, in the open market for $620,000 and an additional 10,000 shares

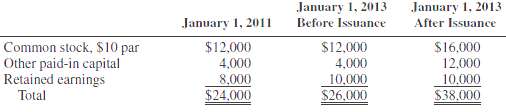

Pin Corporation purchased 960,000 shares of Sit Corporation's common stock (an 80 percent interest) for $21,200,000 on January 1, 2011. The $2,000,000 excess of investment fair value over book value acquired was goodwill. On January 1, 2013, Sit sold 400,000 previously unissued shares of common

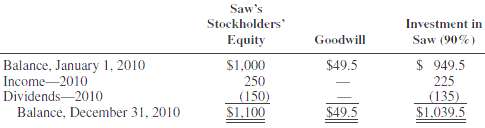

Pat Corporation owned a 90 percent interest in Saw Corporation, and during 2010 the following changes occurred in Saw's equity and Pat's investment in Saw (in thousands): During 2011, Saw's net income was $280,000, and it declared $40,000 dividends each quarter of the year. Pat reduced its

Pan Corporation owns 300,000 of 360,000 outstanding shares of Son Corporation, and its $8,700,000 Investment in Son account balance on December 31, 2011, is equal to the underlying equity interest in Son. Son’s stockholders’ equity at December 31, 2011, is as follows (in thousands):Common

Pal Company purchased 9,000 shares of Sal Corporation’s $50 par common stock at $90 per share on January 1, 2011, when Sal had capital stock of $500,000 and retained earnings of $300,000. During 2011, Sal Corporation had net income of $50,000 but declared no dividends. On January 1, 2012, Sal

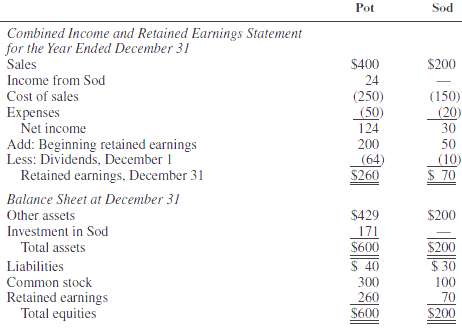

Pot Corporation purchased a 70 percent interest in Sod Corporation on January 2, 2011, for $98,000, when Sod had capital stock of $100,000 and retained earnings of $20,000. On June 30, 2012, Pot purchased an additional 20 percent interest for $37,000. Comparative financial statements for Pot and

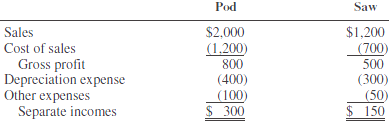

Comparative separate-company and consolidated balance sheets for Pod Corporation and its 70 percent-owned subsidiary, Saw Corporation, at year-end 2011 were as follows (in thousands): Saw's net income for 2012 was $150,000, and its dividends for the year were $80,000 ($40,000 on March 1, and

Pop Corporation acquired an 80 percent interest in Sat Corporation on October 1, 2011, for $82,400, equal to 80 percent of the underlying equity of Sat on that date plus $16,000 goodwill (total goodwill is $20,000). Financial statements for Pop and Sat Corporations for 2011 are as follows (in

Pal Corporation paid $175,000 for a 70 percent interest in Sid Corporation's outstanding stock on April 1, 2011. Sid's stockholders' equity on January 1, 2011, consisted of $200,000 capital stock and $50,000 retained earnings. Accounts and balances at and for the year ended December 31, 2011,

Pam Corporation acquired a 70 percent interest in Sam Corporation on January 1, 2011, for $420,000 cash, when Sam's equity of Sam consisted of $300,000 capital stock and $200,000 retained earnings. On July 1, 2012, Pam acquired an additional 10 percent interest in Sam for $67,500, to bring its

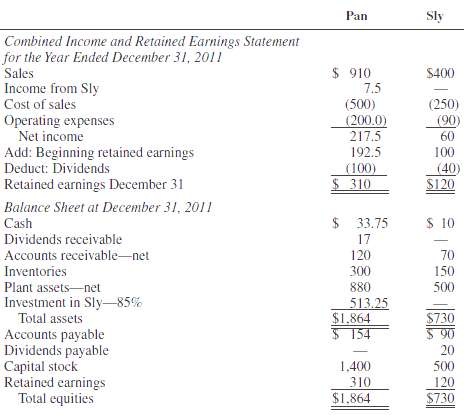

Pan Corporation acquired an 85 percent interest in Sly Corporation on August 1, 2011, for $522,750, equal to 85 percent of the underlying equity of Sly on that date. In August 2011, Sly sold inventory items to Pan for $60,000 at a gross profit of $15,000. Onethird of these items remained in Pan's

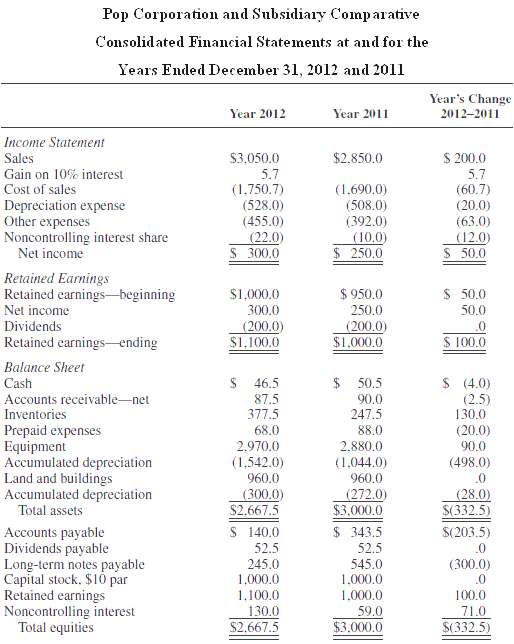

Comparative consolidated financial statements for Pop Corporation and its subsidiary, Sat Corporation, at and for the years ended December 31, 2012 and 2011 follow (in thousands). REQUIRED: Prepare a consolidated statement of cash flows for the year ended December 31, 2012. The changes in

The effect of unrealized profits and losses on sales between affiliated companies is eliminated in preparing consolidated financial statements. When are profits and losses on such sales realized for consolidated statement purposes?

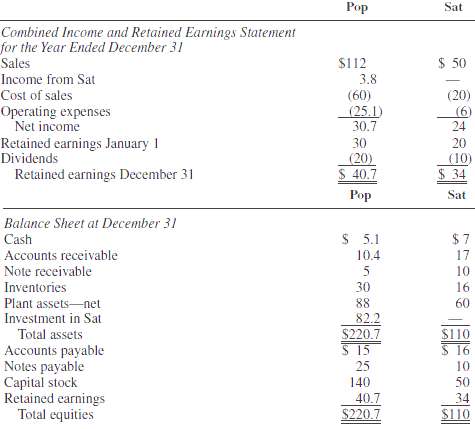

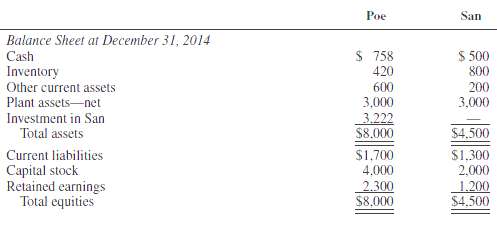

Poe Corporation purchased a 90 percent interest in San Corporation on December 31, 2011, for $2,700,000 cash, when San had capital stock of $2,000,000 and retained earnings of $500,000. All San's assets and liabilities were recorded at fair values when Poe acquired its interest. The excess of fair

Is the amount of intercompany profit to be eliminated from consolidated financial statements affected by the existence of a noncontrolling interest? Explain.

What effect does the elimination of intercompany sales and cost of goods sold have on consolidated net income?

What effect does the elimination of intercompany accounts receivable and accounts payable have on consolidated working capital?

Explain the designations upstream sales and downstream sales. Of what significance are these designations in computing parent and consolidated net income?

Would failure to eliminate unrealized profit in inventories at December 31, 2011, have any effect on consolidated net income in 2012? 2013?

Under what circumstances is noncontrolling interest share affected by intercompany sales activity?

How does a parent adjust its investment income for unrealized profit on sales it makes to its subsidiaries? (a) In the year of the sale and (b) In the year in which the subsidiaries sell the related merchandise to outsiders?

How is the combined cost of goods sold affected by unrealized profit in (a) The beginning inventory of the subsidiary and (b) The ending inventory of the subsidiary?

Is the effect of unrealized profit on consolidated cost of goods sold influenced by (a) The existence of a noncontrolling interest and (b) The direction of intercompany sales?

Unrealized profit in the ending inventory is eliminated in consolidation workpapers by increasing cost of sales and decreasing the inventory account. How is unrealized profit in the beginning inventory reflected in the consolidation workpapers?

Describe the computation of noncontrolling interest share in a year in which there is unrealized inventory profit from upstream sales in both the beginning and ending inventories of the parent.

Consolidation workpaper procedures are usually based on the assumption that any unrealized profit in the beginning inventory of one year is realized through sales in the following year. If the related merchandise is not sold in the succeeding period, would the assumption result in an incorrect

1. Intercompany profit elimination entries in consolidation workpapers are prepared in order to:a. Nullify the effect of intercompany transactions on consolidated statementsb. Defer intercompany profit until realizedc. Allocate unrealized profits between controlling and noncontrolling interestsd.

1. Per, Inc., owns 80 percent of Sen, Inc. During 2011, Per sold goods with a 40 percent gross profit to Sen. Sen sold all of these goods in 2011. For 2011 consolidated financial statements, how should the summation of Per and Sen income statement items be adjusted? a. Sales and cost of goods sold

1. The separate incomes of Pil Corporation and Sil Corporation, a 100 percent-owned subsidiary of Pil, for 2012 are $2,000,000 and $1,000,000, respectively. Pil sells all of its output to Sil at 150 percent of Pil's cost of production. During 2011 and 2012, Pil's sales to Sil were $9,000,000 and

Pid Corporation owns an 80 percent interest in Sed Corporation and at December 31, 2011, Pid's investment in Sed on an equity basis was equal to 80 percent of Sed's stockholders' equity. During 2012, Sed sells merchandise to Pid for $200,000, at a gross profit to Sed of $40,000. At December 31,

Par Corporation owns an 80 percent interest in Sel Corporation acquired several years ago. Sel regularly sells merchandise to its parent at 125 percent of Sel's cost. Gross profit data of Par and Sel for 2012 are as follows: During 2012, Par purchased inventory items from Sel at a transfer price

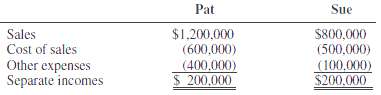

1. Pat Corporation owns 70 percent of Sue Company's common stock, acquired January 1, 2012. Patents from the investment are being amortized at a rate of $20,000 per year. Sue regularly sells merchandise to Pat at 150 percent of Sue's cost. Pat's December 31, 2012, and 2013 inventories include goods

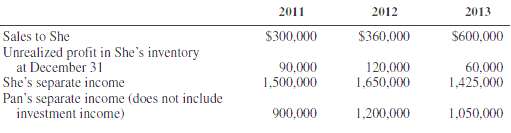

Pan Corporation owns an 80 percent interest in the common stock of She Corporation, acquired several years ago at book value. Pan regularly sells merchandise to She. Information relevant to the intercompany sales and profits of Pan and She for 2011, 2012, and 2013 is as follows: REQUIRED: Prepare

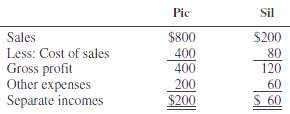

The separate incomes (which do not include investment income) of Pic Corporation and Sil Corporation, its 80 percentowned subsidiary, for 2011 were determined as follows (in thousands): During 2011, Pic sold merchandise that cost $40,000 to Sil for $80,000, and at December 31, 2011, half of these

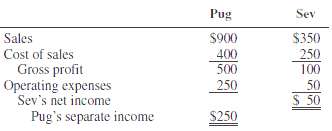

Income statement information for 2011 for Pug Corporation and its 60 percent-owned subsidiary, Sev Corporation, is as follows: Intercompany sales for 2011 are upstream (from Sev to Pug) and total $100,000. Pug's December 31, 2010, and December 31, 2011, inventories contain unrealized profits of

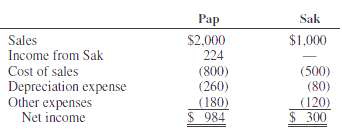

Pap Corporation purchased an 80 percent interest in Sak Corporation for $1,200,000 on January 1, 2012, at which time Sak's stockholders' equity consisted of $1,000,000 common stock and $400,000 retained earnings. The excess fair value over book value was goodwill. Comparative income statements for

On January 1, 2004, Pre Corporation acquired 60 percent of the voting common shares of Sue Corporation at an excess of fair value over book value of $1,000,000. This excess was attributed to plant assets with a remaining useful life of five years. For the year ended December 31, 2011, Sue prepared

The consolidated income statement of Pul and Swa for 2011 was as follows (in thousands):Sales $2,760Cost of sales (1,840)Operating expenses (320)Income to 20 percent noncontrolling interest in Swa (80)Consolidated net income $ 520After the consolidated income

Por Corporation acquired its 90 percent interest in Sam Corporation at its book value of $1,800,000 on January 1, 2011, when Sam had capital stock of $1,500,000 and retained earnings of $500,000. The December 31, 2011 and 2012, inventories of Por included merchandise acquired from Sam of $150,000

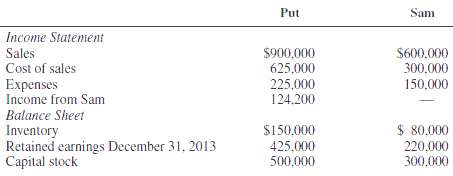

Put Corporation acquired a 90 percent interest in Sam Corporation at book value on January 1, 2011. Intercompany purchases and sales and inventory data for 2011, 2012, and 2013, are as follows: Selected data from the financial statements of Put and Sam at and for the year ended December 31, 2013,

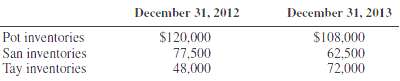

Pot Company owns controlling interests in San and Tay Corporations, having acquired an 80 percent interest in San in 2011, and a 90 percent interest in Tay on January 1, 2012. Pot's investments in San and Tay were at book value equal to fair value. Inventories of the affiliated companies at

Showing 6300 - 6400

of 107766

First

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

Last

Step by Step Answers