New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

accounting

Advanced Accounting 11th Edition Floyd A. Beams, Joseph H. Anthony, Bruce Bettinghaus, Kenneth Smith - Solutions

Describe the computation of noncontrolling interest share for an 80%-owned subsidiary with both preferred and common stock outstanding.

Under what conditions will the procedures used in computing a parent’s EPS be the same as those for a company without equity investments?

Potentially dilutive securities of a subsidiary may be converted into parent common stock or subsidiary common stock. Describe how these situations affect the parent’s EPS procedures.

In computing diluted earnings for a parent, it may be necessary to replace the parent’s equity in subsidiary realized income with the parent’s equity in the subsidiary’s diluted earnings. Does this replacement calculation involve unrealized profits that are included in the parent’s income

Are consolidated income tax returns required for all consolidated entities? Discuss.

What are the primary advantages of filing a consolidated tax return?

Does a parent/investor provide for income taxes on the undistributed earnings of a subsidiary by adjusting investment and investment income accounts? Explain.

1. [Preferred stock] Pin Corporation owns 20% of Sob Corporation's preferred stock and 80% of its common stock. Sob's stock outstanding on December 31, 2011, is as follows: 10% cumulative preferred stock .. $ 200,000 Common stock .......... 1,400,000 Sob reported net income of $120,000 for the year

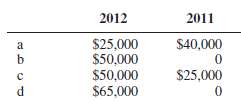

The stockholders’ equity of Sir Corporation at December 31, 2011, was as follows (in thousands):10% cumulative preferred stock, $100 par, callable at $105,20,000 shares issued and outstanding, with one year’s dividends in arrears .. $2,000Common stock, $10 par, 200,000 shares issued and

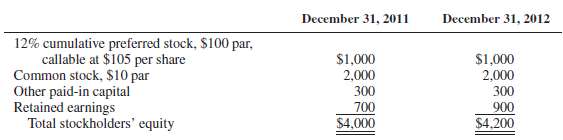

The stockholders’ equity of Sol Corporation at December 31, 2010, was as follows (in thousands):12% preferred stock, cumulative, nonparticipating,$100 par, callable at $105 ........... $ 600Common stock, $10 par .............. 1,000Other paid-in capital ................ 140Retained earnings

Pen Corporation owns 80 percent of San Corporation's common stock, having acquired the interest at a fair value equal to book value on December 31, 2011. During 2012, Pen's separate income is $3,000,000 and San's net income is $500,000. Pen and San declare dividends in 2012 of $1,000,000 and

The stockholders’ equity of Son Corporation on December 31, 2011, was as follows (in thousands):15% preferred stock, $100 par, cumulative, nonparticipating, withone year’s dividends in arrears ........... $1,000Common stock, $10 par .................. 2,000Other paid-in capital

Pay Corporation purchased 60 percent of Set Corporation’s outstanding preferred stock for $6,500,000 and 70 percent of its outstanding common stock for $35,000,000 on January 1, 2012. Set’s stockholders’ equity on December 31, 2011, consisted of the following (in thousands):10% cumulative,

1. A parent company and its 100%-owned subsidiary have only common stock outstanding (10,000 shares for the parent and 3,000 shares for the subsidiary), and neither company has issued other potentially dilutive securities. The equation to compute consolidated EPS for the parent company and its

Pal Corporation’s net income for 2011 is $316,000, including $160,000 income from Sod Corporation, its 80 percentowned subsidiary. The income from Sod consists of $176,000 equity in income less $16,000 patent amortization. Pal has 300,000 shares of $10 par common stock outstanding, and Sod has

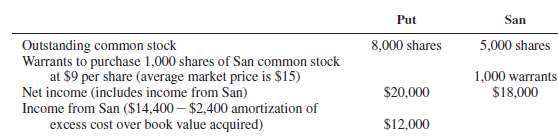

The following information is available regarding Put Corporation and its 80 percent-owned subsidiary, San Corporation, at and for the year ended December 31, 2011: REQUIRED: Determine consolidated earnings per share (both basic anddiluted).

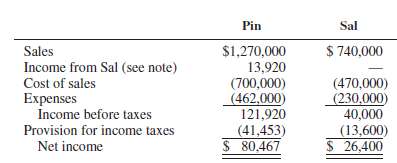

The income statements of Pin Corporation and its 80 percent-owned subsidiary, Sal Corporation, for 2011 are as follows: Note: Income from Sal is computed as [($26,400 reported income * 80%) - $2,000 patent amortization - $5,200 unrealized profit in Sal's inventory].Pin had 10,000 shares of

Pow Corporation owns an 80 percent interest in Soy Corporation. Pow does not have common stock equivalents or other potentially dilutive securities outstanding, so it calculated its EPS for 2011 as follows: An examination of Pow's income from Soy shows that it is determined correctly as 80

1. Income taxes are currently due on intercompany profits when:(a) Profits originate from upstream sales(b) Separate-company tax returns are filed(c) Consolidated tax returns are filed(d) Affiliates are accounted for as consolidated subsidiaries2. The right of a consolidated entity to file a

1. When Pet Corporation acquired its 100% interest in Sin Corporation in a tax-free reorganization, Sin’s equipment had a fair value of $6,000,000 and a book value and tax basis of $4,000,000. If Pet’s effective tax rate is 34%, how much of the purchase price should be allocated to equipment

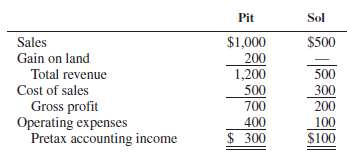

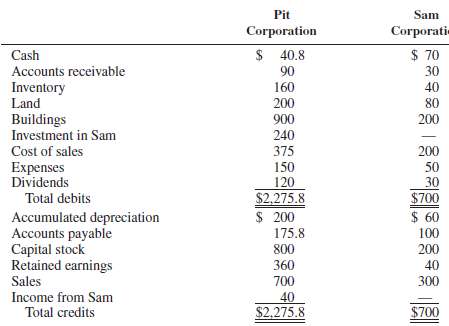

The pretax accounting incomes of Pit Corporation and its 100 percent-owned subsidiary, Sol Company, for 2011 are as follows (in thousands): The only intercompany transaction during 2011 was a gain on land sold to Sol. Assume a 34 percent flat income tax rate.REQUIRED1. What amount should be

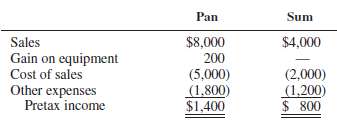

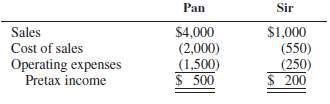

Pan Corporation and its 70 percent-owned subsidiary, Sum Corporation, have pretax operating incomes for 2011 as follows (in thousands): Pan received $280,000 dividends from Sum during 2011. A previously unrecorded patent from Pan's investment in Sum is being amortized at a rate of $50,000 per

Sun Corporation is a 100 percent-owned subsidiary of Ped Corporation. During the current year, Ped sold merchandise that cost $50,000 to Sun for $100,000. A 34 percent income tax rate is applicable, and 80 percent of the merchandise remains unsold by Sun at year-end.REQUIRED1. Prepare comparative

Son Corporation, an 80 percent-owned subsidiary of Pin Corporation, sold equipment with a book value of $150,000 to Pin for $250,000 at December 31, 2011. Separate income tax returns are filed, and a 34 percent income tax rate is applicable to both Pin and Son.REQUIRED1. Prepare a one-line

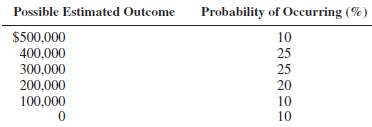

Pax Corporation recognizes a deferred tax asset (benefit) of $500,000 related to its acquisition of Son Company. Pax has determined that the tax position qualifies for recognition and should be measured. Pax has determined the amounts and the probabilities of the possible outcomes, as

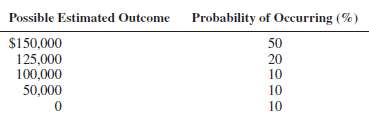

Pun Corporation recognizes a deferred tax asset (benefit) of $150,000 related to its acquisition of Sew Company. Pun has determined that the tax position qualifies for recognition and should be measured. Pun has determined the amounts and the probabilities of the possible outcomes, as

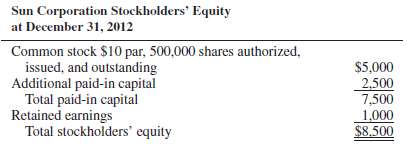

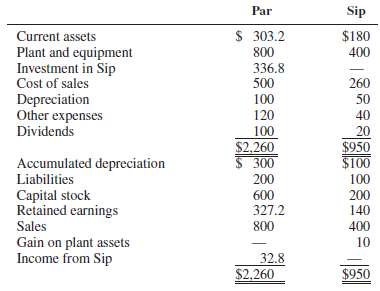

Par Corporation paid $7,200,000 for 360,000 shares of Sun Corporation’s outstanding voting common stock on January 1, 2011, when the stockholders’ equity of Sun consisted of (in thousands):10% cumulative, preferred stock, $100 par. Liquidationpreference is $105 per share, and 20,000 shares are

Pun Corporation acquired 80 percent of Set Corporation’s preferred stock for $175,000 and 90 percent of Set’s common stock for $630,000 on July 1, 2011. Set’s stockholders’ equity on December 31, 2011, was as follows (in thousands):Stockholders’ Equity9% preferred stock, cumulative,

Financial statements for Pat and Sal Corporations for 2011 are summarized as follows (in thousands): Pat owns 90,000 shares of Sal's outstanding voting common stock at December 31, 2011.These shares were acquired in two lots as follows: The stockholders' equity of Sal at year-end 2009, 2010,

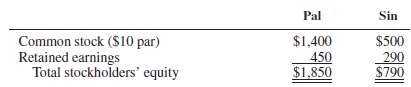

Par Corporation acquired an 80 percent interest in Sam Corporation common stock for $240,000 on January 1, 2010, when Sam's stockholders' equity consisted of $200,000 common stock, $100,000 preferred stock, and $25,000 retained earnings. The excess was due to goodwill. Intercompany sales of

Pal Corporation has $108,000 income from its own operations for 2011, and $42,000 income from Sir Corporation, its 70 percent-owned subsidiary. Sir’s net income of $60,000 consists of $66,000 operating income less $6,000 net-of-tax interest on its outstanding 10 percent convertible debentures.

Pen Corporation owns an 80 percent interest in She Company. Throughout 2011, Pen had 20,000 shares of common stock outstanding. She had the following securities outstanding: ??? 10,000 shares of common stock ??? Options to purchase 2,000 shares of She common at $15 per share ??? 1,000 shares of

Pro Corporation owns 80 percent of Sit Corporation's outstanding common stock. The 80 percent interest was acquired in 2011 at $40,000 in excess of book value due to undervalued equipment with an eight-year remaining useful life. Outstanding securities of the two companies throughout 2012 and at

Pin Company owns 40,000 of 50,000 outstanding shares of Sum Company, and during 2011, it recognizes income from Sum as follows:Share of Sum net income ($500,000 * 80%) .... $ 400,000Patent amortization ....................... (50,000)Unrealized profit—downstream sales ........ (40,000)Unrealized

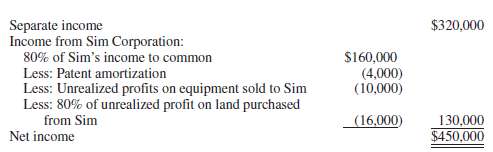

Pit Corporation's net income for 2011 consists of the following: ADDITIONAL INFORMATION1. Pit has 100,000 shares of common stock, and Sim has 50,000 shares of common and 10,000 shares of $10 cumulative, convertible, preferred stock outstanding throughout 2011. The preferred stock is convertible

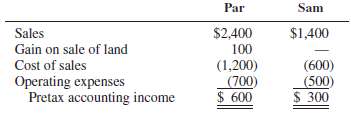

Par Corporation and its 100 percent-owned subsidiary, Sam Corporation, are members of an affiliated group with pretax accounting incomes as follows (in thousands): The gain reported by Par relates to land sold to Sam during the current year. A flat 34 percent income tax rate is

Pan Corporation paid $577,500 cash for a 70 percent interest in Sir Corporation's outstanding common stock on January 2, 2011, when the equity of Sir consisted of $500,000 common stock and $300,000 retained earnings. The excess fair value is due to goodwill. In December 2011, Sir sold inventory

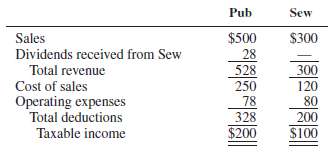

Taxable incomes for Pub Corporation and Sew Corporation, its 70 percent-owned subsidiary, for 2011 are as follows (in thousands): ADDITIONAL INFORMATION1. Pub acquired its interest in Sew at a fair value equal to book value on December 31, 2010.2. Sew paid dividends of $40,000 in 2011.3. Pub

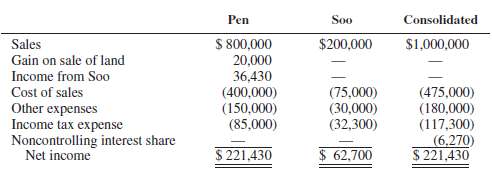

Pen Corporation acquired a 90 percent interest in Soo Corporation in a taxable transaction on January 1, 2011, for $900,000, when Soo had $500,000 capital stock and $400,000 retained earnings. The $90,000 excess cost over book value is due to goodwill. Pen and Soo are an affiliated group for tax

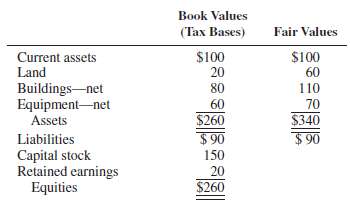

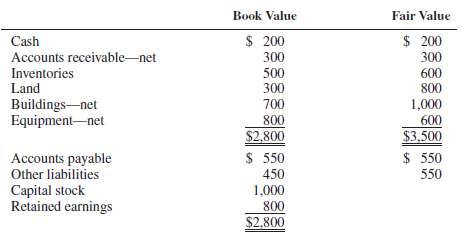

Par Corporation acquired all the stock of Sad Corporation on January 1, 2011, for $280,000 cash, when the book values and fair values of Sad's assets and liabilities were as follows (in thousands): Sad's buildings have a remaining life of 10 years, and the equipment has a useful life of 2 years

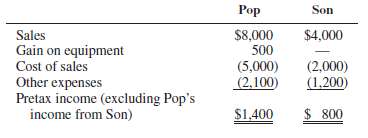

The pretax operating incomes of Pop Corporation and Son Corporation, its 70 percent-owned subsidiary, for 2011 are as follows (in thousands): ADDITIONAL INFORMATION1. Pop received $280,000 dividends from Son during 2011.2. Goodwill from Pop's investment in Son is not amortized.3. Pop sold

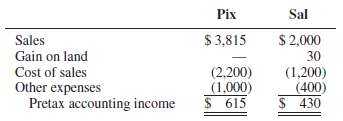

On January 3, 2011, Pix Corporation purchased a 90% interest in Sal Corporation at a price $120,000 in excess of book value and fair value. The excess is goodwill. During 2011, Pix sold inventory items to Sal for $100,000, and $15,000 in profit from the sale remained unrealized at year-end. Sal

Compare the traditional, parent-company, and entity theories of consolidated financial statements.

Which, if any, of the consolidation theories would be changed by FASB pronouncements? (For example, assume that a new FASB statement requires noncontrolling interest share to be computed as the noncontrolling interest share of subsidiary dividends declared.)

Under the entity theory, a total valuation of the subsidiary is imputed on the basis of the price paid by the parent company for its controlling interest. Do you see any practical or conceptual problems with this approach?

Assume that Pat Corporation acquires 60% of the voting common stock of Sir Corporation for $6,000,000 and that a consolidated balance sheet is prepared immediately after the acquisition. Would total consolidated assets be equal to their fair values if the parent-company theory were applied? If the

Why might the traditional practice of valuing the equity of noncontrolling shareholders at book value overstate the value of the noncontrolling interest?

Cite the conditions under which consolidated net income under parent-company theory would equal income to controlling stockholders under entity theory.

If income from a subsidiary is measured under the equity method and the statements are consolidated under entity theory, will consolidated net income equal parent net income?

Why are the income statement amounts under entity theory and traditional theory the same if the subsidiary investment is made at book value? (Do not consider the different income statement presentations of controlling and noncontrolling interests in responding to this question.)

Does traditional theory correspond to parent-company or entity theory in matters related to unrealized and constructive gains and losses on intercompany transactions?

To what extent does push-down accounting facilitate the consolidation process?

What is a joint venture and how are joint ventures organized?

What accounting and reporting methods are used by investor-venturers in accounting for their joint venture investments?

1. The classification of noncontrolling interest share as an expense and noncontrolling interest as a liability is preferred under:(a) Parent-company theory(b) Entity theory(c) Traditional theory(d) None of the above2. Traditional theory is most similar to parent-company theory in matters relating

1. A joint venture would not be organized as a(an):(a) Corporation(b) Proprietorship(c) Partnership(d) Undivided interest2. Corporate joint ventures should be accounted for by the equity method, provided that the joint venturer:(a) Cannot exercise significant influence over the joint venture(b) Can

1. Pet Company pays $1,440,000 for an 80% interest in Sit Corporation on December 31, 2011, when Sit’s net assets at book value and fair value are $1,600,000. Under entity theory, the noncontrolling interest at acquisition is:(a) $288,000(b) $320,000(c) $360,000(d) $400,0002. Sat Corporation sold

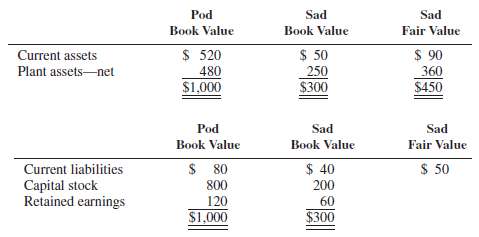

Balance sheet information of Pod and Sad Corporations at December 31, 2011, is summarized as follows (in thousands): On January 2, 2011, Pod purchases 80 percent of Sad's outstanding shares for $500,000 cash.REQUIRED1. Determine goodwill from the acquisition under(a) Parent-company theory and(b)

On January 1, 2011, Par Corporation pays $300,000 for an 80 percent interest in Sal Company, when Sal’s net assets have a book value of $275,000 and a fair value of $350,000. The $75,000 excess fair value is due to undervalued equipment with a five-year remaining useful life. Any goodwill is not

Sal Corporation’s recorded assets and liabilities are equal to their fair values on July 1, 2011, when Pub Corporation purchases 72,000 shares of Sal common stock for $1,800,000. Identifiable net assets of Sal on this date are $1,710,000, and Sal’s stockholders’ equity consists of $800,000 of

Pal Company acquired an 80 percent interest in Sal Corporation at book value equal to fair value on January 1, 2011.During the year, Sal sold $100,000 inventory items to Pal, and at December 31, 2011, unrealized profits amounted to $30,000. Separate incomes of Pal and Sal for 2011 were $500,000 and

Pad Corporation acquired an 80 percent interest in Sot Company at book value a number of years ago.Separate incomes of Pad and Sot for 2011 were $120,000 and $60,000, respectively. The only transactions betweenPad and Sot during 2011 were as follows:1. Pad sold inventory items to Sot for $60,000.

On January 1, 2011, Pin Corporation acquired a 90 percent interest in Set Corporation for $2,520,000. The book values and fair values of Set's assets and equities on this date are as follows (in thousands): REQUIRED1. Prepare the journal entries on Set Corporation's books to push down the values

Sun Corporation is a corporate joint venture that is jointly controlled and operated by five investor-venturers, four with 15 percent interests each and one with a 40 percent interest. Each of the five venturers is active in venture management. Land sales and other important venture decisions

Pat Corporation is the primary beneficiary in a VIE, even though Pat owns only 10 percent of the outstanding voting shares. In the year following the initial consolidation, the VIE earns net income of $1,000,000. Included in income is a fee paid by Pat for $80,000. What amount of noncontrolling

Pal, Inc., holds an interest in Pot Corporation. Pal has determined that Pot qualifies as a VIE and that Pal’s contractual position makes Pal the primary beneficiary. Den Corporation also holds a significant financial interest in Pot. What are the financial reporting and disclosure requirements

Jenn Corporation and Laura Company participate in a business classified as a VIE. Under terms of their contractual arrangement, Jenn and Laura share equally in expected residual returns of the VIE. However, expected losses are allocated 70 percent to Laura and 30 percent to Jenn. Laura serves as

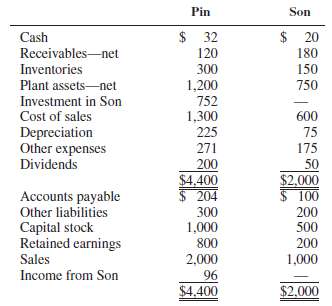

The adjusted trial balances of Pin Corporation and its 80 percent-owned subsidiary, Son Corporation, at December 31, 2012, are as follows (in thousands): Pin acquired its interest in Son for $640,000 on January 1, 2011, when Son's stockholders' equity consisted of $500,000 capital stock and

Par Corporation acquires an 80 percent interest in Sip Company on January 3, 2011, for $320,000. On this date Sip's stockholders' equity consists of $200,000 capital stock and $140,000 retained earnings. The fair value/book value differential is assigned to undervalued equipment with a 6-year

Pal Corporation paid $595,000 cash for 70 percent of the outstanding voting stock of Sin Corporation on January 2, 2011, when Sin's stockholders' equity consisted of $500,000 of $10 par common stock and $250,000 retained earnings. The book values of Sin's assets and liabilities were equal to their

At December 31, 2011, when the fair values of Sam Corporation's net assets were equal to their book values of $240,000, Pit Corporation acquired an 80 percent interest in Sam for $224,000. One year later, at December 31, 2012, the comparative adjusted trial balances of the two corporations appear

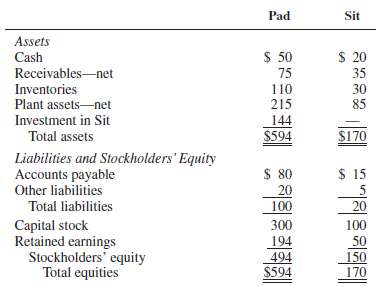

Balance sheets for Pad Corporation and its 80 percent-owned subsidiary, Sit Company, at December 31, 2012, are summarized as follows (in thousands): ADDITIONAL INFORMATION1. Pad Corporation paid $128,000 for its 80% interest in Sit on January 1, 2011, when Sit had capital stock of $100,000 and

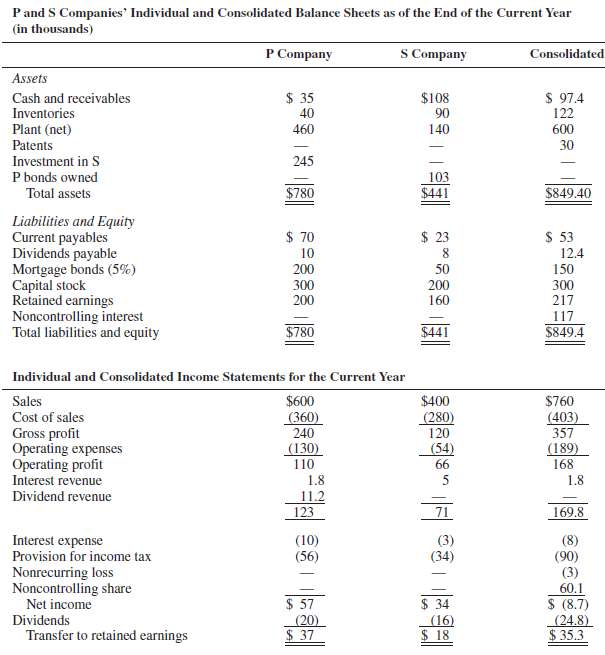

The individual and consolidated balance sheets and income statements of P and S Companies for the current year are presented in the accompanying table. The entity theory is used. ADDITIONAL INFORMATION 1. P Company purchased its interest in S Company several years ago. 2. P Company sells products

Pay Corporation paid $480,000 cash for a 100 percent interest in Sap Corporation on January 1, 2012, when Sap's stockholders' equity consisted of $200,000 capital stock and $80,000 retained earnings. Sap's balance sheet on December 31, 2011, is summarized as follows (in thousands): Pay uses the

Par Corporation paid $3,000,000 for an 80 percent interest in Son Corporation on January 1, 2011, when the book values and fair values of Son's assets and liabilities were as follows (in thousands): REQUIRED1. Prepare a journal entry on Son's books to push down 80% of the values reflected in the

Paw Corporation paid $180,000 cash for a 90 percent interest in Sun Corporation on January 1, 2012, when Sun's stockholders' equity consisted of $100,000 capital stock and $20,000 retained earnings. Sun Corporation's balance sheets at book value and fair value on December 31, 2011, are as follows

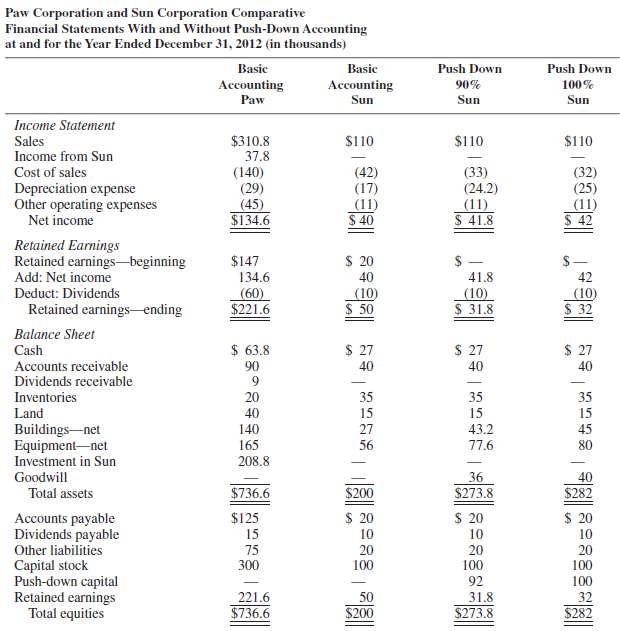

Use the information and assumptions from Problem P 11-9 for this problem. The accompanying financial statements are for Paw and Sun Corporations, one year after the acquisition. Note that Sun's statements are presented first under contemporary theory with no push-down accounting, then under 90

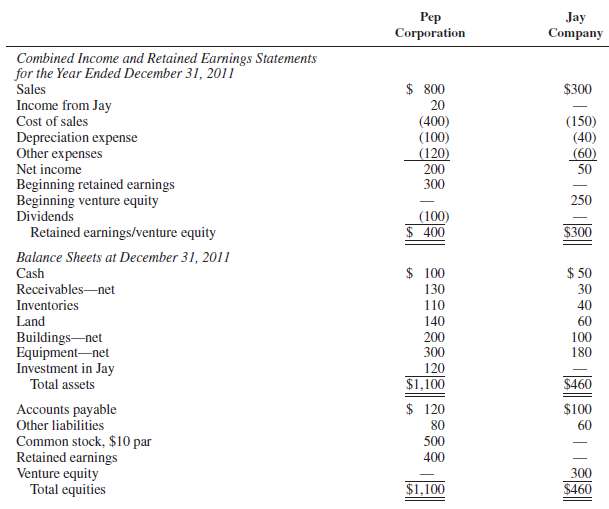

Pep Corporation owns a 40 percent interest in Jay Company, a joint venture that is organized as an undivided interest. In its separate financial statements, Pep accounts for Jay under the equity method, but for reporting purposes, the proportionate consolidation method is used. Separate financial

Define the term derivative and provide examples of risks that derivative contracts are designed to reduce.

Explain the differences between forward contracts and futures contracts and the potential benefits and potential costs of each type of contract.

Explain the differences between options and swaps and the potential benefits and potential costs of each type of contract.

What does “Net Settlement” mean?

Assume that one euro can be exchanged for 1.20 U.S. dollars. What is the exchange rate if the exchange rate is quoted directly? Indirectly?

What is the difference between official and floating foreign exchange rates? Does the United States have floating exchange rates?

What is a spot rate with respect to foreign currency transactions? Could a spot rate ever be a historical rate? Could a spot rate ever be a fixed exchange rate? Discuss.

Assume that a U.S. corporation imports electronic equipment from Japan in a transaction denominated in U.S. dollars. Is this transaction a foreign currency transaction? A foreign transaction? Explain the difference between these two concepts and their application here.

How are assets and liabilities denominated in foreign currency measured and recorded at the transaction date? At the balance sheet date?

Criticize the following statement: “Exchange losses arise from foreign import activities, and exchange gains arise from foreign export activities.”

When are exchange gains and losses reflected in a business’s financial statements?

A U.S. corporation imported merchandise from a British company for £1,000 when the spot rate was $1.45. It issued financial statements when the current rate was $1.47, and it paid for the merchandise when the spot rate was $1.46. What amount of exchange gain or loss will be included in the U.S.

1. What is a characteristic of a forward?(a) Traded on an exchange(b) Negotiated with a counterparty(c) Covers a stream of future payments(d) Must be settled daily2. What is a characteristic of a swap?(a) Traded on an exchange(b) Only interest rates can be the underlying(c) Covers a stream of

1. Which is true about the seller of a put option?(a) They have the right to buy the underlying(b) They have the right to sell the underlying(c) They have the obligation to buy the underlying(d) They have the obligation to sell the underlying2. Which is true about the holder of a call option?(a)

1. If $1.5625 can be exchanged for 1 British pound, the direct and indirect exchange rate quotations are:(a) $1.5625 and 1 British pound, respectively(b) $1.5625 and 0.64 British pounds, respectively(c) $1.00 and 1.5625 British pounds, respectively(d) $1.00 and 0.64 British pounds, respectively2.

Zimmer Corporation, a U.S. firm, purchased merchandise from Taisho Company of Japan on November 1, 2011, for 10,000,000 yen, payable on December 1, 2011. The spot rate for yen on November 1 was $0.0075, and on December 1 the spot rate was $0.0076.REQUIRED1. Did the dollar weaken or strengthen

On December 16, 2011, Aviator Corporation, a U.S. firm, purchased merchandise from Wing Company for 30,000 euros to be paid on January 15, 2012. Relevant exchange rates for euros are as follows:December 16, 2011 ... $1.20December 31, 2011 ... $1.25January 15, 2012 .... $1.24REQUIRED: Prepare all

On November 16, 2011, Wick Corporation of the United States sold inventory items to Candle Ltd. of Canada for 90,000 Canadian dollars, to be paid on February 14, 2012. Exchange rates for Canadian dollars on selected dates are as follows:November 16, 2011 .... $0.80December 31, 2011 ....

Door Corporation, a U.S. company, sold inventory items to Royal Cabinets Ltd. of Great Britain for £200,000 on May 1, 2011, when the spot rate was 0.6000 pounds. The invoice was paid by Royal on May 30, 2011, when the spot rate was 0.6050 pounds.REQUIRED: Prepare Door’s journal entries for the

1. On September 1, 2011, Bain Corporation received an order for equipment from a foreign customer for 300,000 euros, when the U.S. dollar equivalent was $400,000. Bain shipped the equipment on October 15, 2011, and billed the customer for 300,000 euros when the U.S. dollar equivalent was $420,000.

Monroe Corporation imports merchandise from some Canadian companies and exports its own products to other Canadian companies. The unadjusted accounts denominated in Canadian dollars at December 31, 2011, are as follows:Account receivable from the sale of merchandise onDecember 16 to Carver

American TV Corporation had two foreign currency transactions during December 2011, as follows:December 12 Purchased electronic parts from Toko Company of Japan atan invoice price of 50,000,000 yen when the spot rate for yenwas $0.00750. Payment is due on January 11, 2012.December 15 Sold

Showing 6500 - 6600

of 107766

First

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

Last

Step by Step Answers