New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

accounting

Advanced Accounting 11th Edition Floyd A. Beams, Joseph H. Anthony, Bruce Bettinghaus, Kenneth Smith - Solutions

Comparative income statements of Stu Corporation for the calendar years 2011, 2012, and 2013 are as follows (in thousands): ADDITIONAL INFORMATION1. Stu was a 75 percent-owned subsidiary of Pli Corporation throughout the 2011???2013 period. Pli's separate income (excludes income from Stu) was

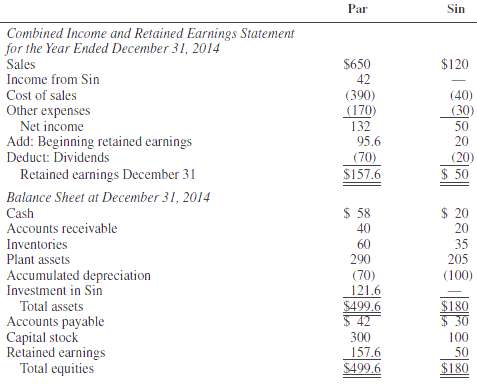

Pan Corporation acquired 100 percent of Sal Corporation's outstanding voting common stock on January 1, 2011, for $660,000 cash. Sal's stockholders' equity on this date consisted of $300,000 capital stock and $300,000 retained earnings. The difference between the price paid by Pan and the

Pay Corporation acquired a 75 percent interest in Sue Corporation for $600,000 on January 1, 2011, when Sue's equity consisted of $300,000 capital stock and $100,000 retained earnings. The fair values of Sue's assets and liabilities were equal to book values on this date, and goodwill is not

Pol Corporation purchased a 90 percent interest in San Corporation on December 31, 2010, for $2,700,000 cash, when San had capital stock of $2,000,000 and retained earnings of $500,000. All San's assets and liabilities were recorded at their fair values when Pol acquired its interest. The excess of

Pan Corporation acquired 100 percent of Sal Corporation's outstanding voting common stock on January 1, 2011, for $660,000 cash. Sal's stockholders' equity on this date consisted of $300,000 capital stock and $300,000 retained earnings. The difference between the fair value of Sal and the

What is the objective of eliminating the effects of intercompany sales of plant assets in preparing consolidated financial statements?

In accounting for unrealized profits and losses from intercompany sales of plant assets, does it make any difference if the parent is the purchaser or the seller? Would your answer be different if the subsidiary were 100 percent owned?

When are unrealized gains and losses from intercompany sales of land realized from the viewpoint of the selling affiliate?

How is the computation of noncontrolling interest share affected by downstream sales of land? By upstream sales of land?

Consolidation workpaper entries are made to eliminate 100 percent of the unrealized profit from the land account in downstream sales of land. Is 100 percent also eliminated for upstream sales of land?

How are unrealized gains and losses from intercompany transactions involving depreciable assets eventually realized?

Describe the computation of noncontrolling interest share in the year of an upstream sale of depreciable plant assets.

How does a parent eliminate the effects of unrealized gains on intercompany sales of plant assets under the equity method?

What is the effect of intercompany sales of plant assets on parent and consolidated net income in years subsequent to the year of sale?

Explain the sequence of workpaper adjustments and eliminations for unrealized gains and losses on depreciable plant assets. Is your answer affected by whether the intercompany transaction occurred in the current year or in prior years?

Use the following information in answering questions 1 and 2: Par Company sells land with a book value of $5,000 to Sub Company for $6,000 in 2011. Sub Company holds the land during 2012. Sub Company sells the land for $8,000 to an outside entity in 2013. 1. In 2011 the unrealized gain: a. To be

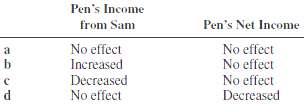

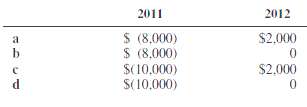

Sam Corporation is a 90 percent-owned subsidiary of Par Corporation, acquired by Par in 2011. During 2014 Par sells land to Sam for $50,000 for which it paid $25,000. Sam owns this land at December 31, 2014.REQUIRED1. How and in what amount will the sale of land affect Par’s income from Sam and

Sir Corporation is a 90 percent-owned subsidiary of Pit Corporation, acquired several years ago at book value equal to fair value. For 2011 and 2012, Pit and Sir report the following: The only intercompany transaction between Pit and Sir during 2011 and 2012 was the January 1, 2011, sale of land.

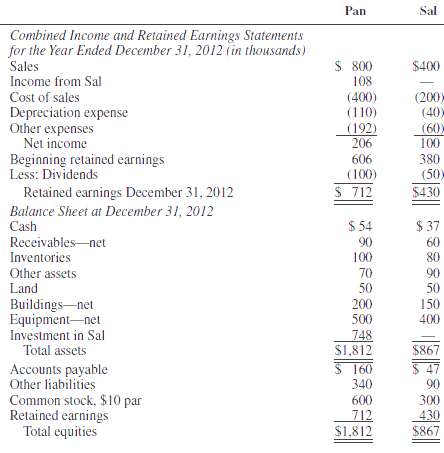

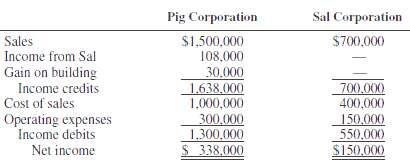

Sal is a 90 percent-owned subsidiary of Pig Corporation, acquired at book value several years ago. Comparative separate-company income statements for the affiliates for 2011 are as follows: On January 5, 2011, Pig sold a building with a 10-year remaining useful life to Sal at a gain of $30,000.

1. On January 1, 2011, Pan Company sold equipment to its wholly-owned subsidiary, Sun Company, for $1,800,000. The equipment cost Pan $2,000,000. Accumulated depreciation at the time of sale was $500,000. Pan was depreciating the equipment on the straight-line method over 20 years with no salvage

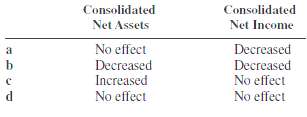

1. Son Corporation is an 80 percent-owned subsidiary of Pin Corporation. In 2011, Son sold land that cost $15,000 to Pin for $25,000. Pin held the land for eight years before reselling it in 2019 to Roy Company, an unrelated entity, for $55,000. The 2019 consolidated income statement for Pin and

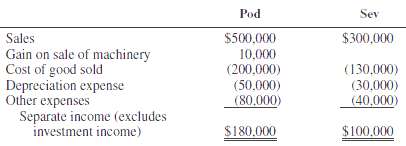

A summary of the separate income of Pod Corporation and the net income of its 75 percent-owned subsidiary, Sev Corporation, for 2011 is as follows: Sev Corporation sold machinery with a book value of $40,000 to Pod Corporation for $65,000 on January 2, 2009. At the time of the intercompany sale,

Pep Corporation owns 40 percent of the outstanding voting stock of Sat Corporation, acquired for $100,000 on July 1, 2011, when Sat’s common stockholders’ equity was $200,000. The excess of investment fair value over book value acquired was due to valuable patents owned by Sat that were

Pan Corporation has an 80 percent interest in Sip Corporation, its only subsidiary. The 80 percent interest was acquired on July 1, 2011, for $400,000, at which time Sip's equity consisted of $300,000 capital stock and $100,000 retained earnings. The excess of fair value over book value was

Ped Industries manufactures heavy equipment used in construction and excavation. On January 3, 2011, Ped sold a piece of equipment from its inventory that cost $180,000 to its 60 percent-owned subsidiary, Spa Corporation, at Ped’s standard price of twice its cost. Spa is depreciating the

Income data from the records of Par Corporation and Sum Corporation, Par's 80 percent-owned subsidiary, for 2011 through 2014 follow (in thousands): Par acquired its interest in Sum on January 1, 2011, at a price of $40,000 less than book value. The $40,000 was assigned to a reduction of plant

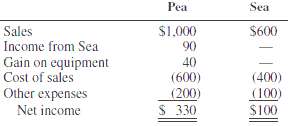

The separate income statements of Pea Corporation and its 90 percent-owned subsidiary, Sea Corporation, for 2011 are summarized as follows (in thousands): Investigation reveals that the effects of certain intercompany transactions are not included in Pea's income from Sea. Information about those

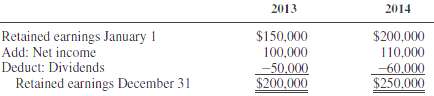

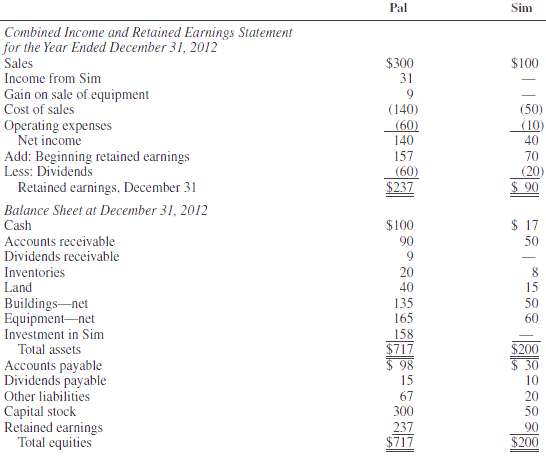

Sim Corporation, a 90 percent-owned subsidiary of Pal Corporation, was acquired on January 1, 2011, at a price of $45,000 in excess of underlying book value. The excess was due to goodwill. Separate financial statements for Pal and Sim for 2012 follow (amounts in thousands): ADDITIONAL

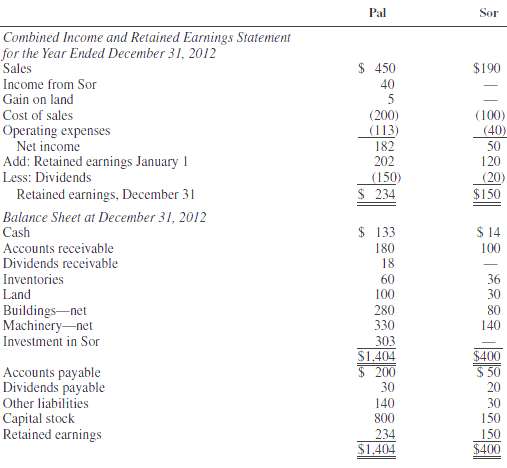

Pal Corporation acquired a 90 percent interest in Sor Corporation on January 1, 2011, for $270,000, at which time Sor's capital stock and retained earnings were $150,000 and $90,000, respectively. The fair value/book value differential is goodwill. Financial statements for Pal and Sor for 2012 are

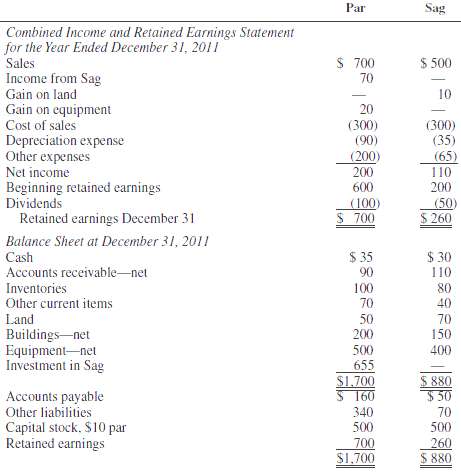

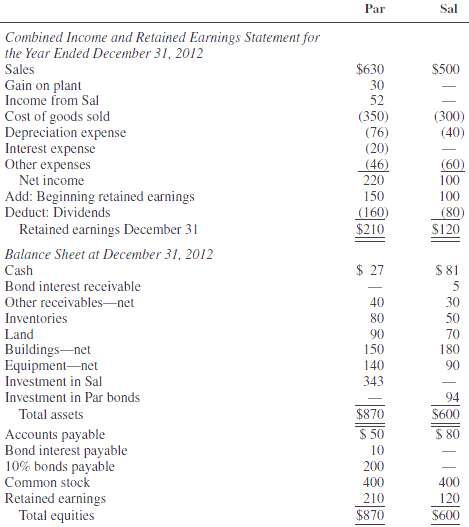

Par Corporation acquired a 90 percent interest in Sag Corporation's outstanding voting common stock on January 1, 2011, for $630,000 cash. The stockholders' equity of Sag on this date consisted of $500,000 capital stock and $200,000 retained earnings. The financial statements of Par and Sag at and

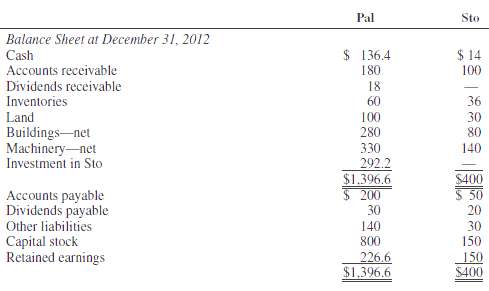

Pal Corporation acquired a 90 percent interest in Sto Corporation on January 1, 2011, for $270,000, at which time Sto's capital stock and retained earnings were $150,000 and $90,000, respectively. The fair value cost/book value differential is due to a patent with a 10-year amortization period.

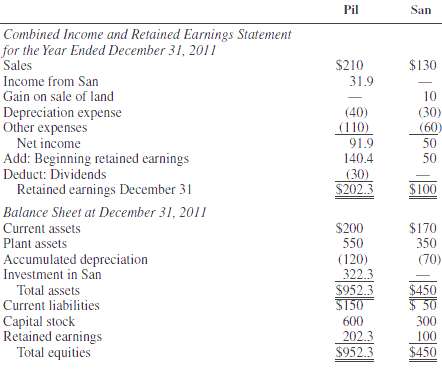

Financial statements for Pil and San Corporations for 2011 are as follows (in thousands): ADDITIONAL INFORMATION1. Pil acquired an 80 percent interest in San on January 2, 2009, for $290,000, when San's stockholders' equity consisted of $300,000 capital stock and no retained earnings. The excess

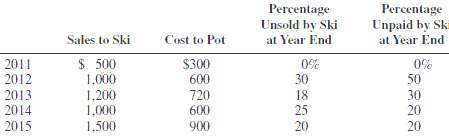

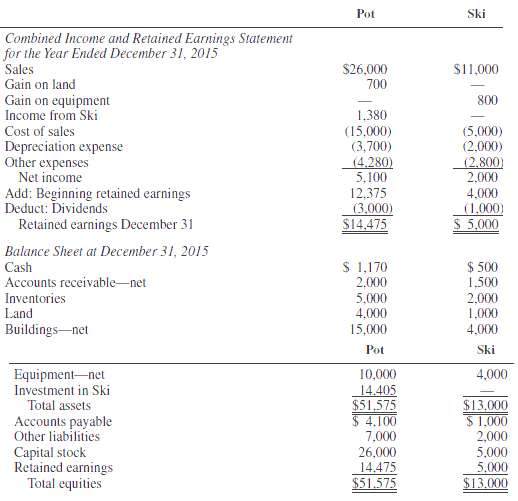

Pot Corporation acquired all the outstanding stock of Ski Corporation on April 1, 2011, for $15,000,000, when Ski's stockholders' equity consisted of $5,000,000 capital stock and $2,000,000 retained earnings. The price reflected a $500,000 undervaluation of Ski's inventory (sold in 2011) and a

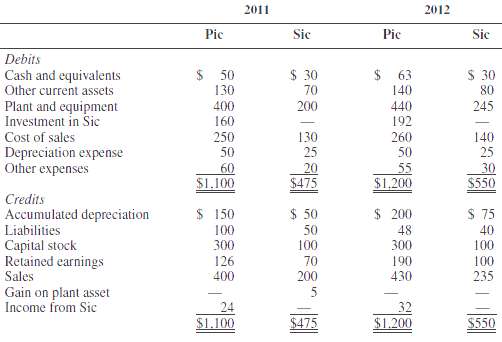

Pic Corporation acquired an 80 percent interest in Sic Company on January 1, 2011, for $136,000, when Sic's capital stock and retained earnings were $100,000 and $70,000, respectively. At the beginning of 2011, Sic sold a machine to Pic for $10,000. The machine had cost Sic $7,000, had depreciated

Par Corporation acquired an 80 percent interest in Sin Corporation on January 1, 2011, for $108,000 cash, when Sin's capital stock was $100,000 and retained earnings were $10,000. The difference between investment fair value and book value acquired is due to a patent being amortized over a 10- year

Financial statements for Pal and Sun Corporations for 2011 are as follows (in thousands):ADDITIONAL INFORMATION1. Pal acquired an 80 percent interest in Sun on January 2, 2009, for $290,000, when Sun’s stockholders’ equity consisted of $300,000 capital stock and no retained earnings. The

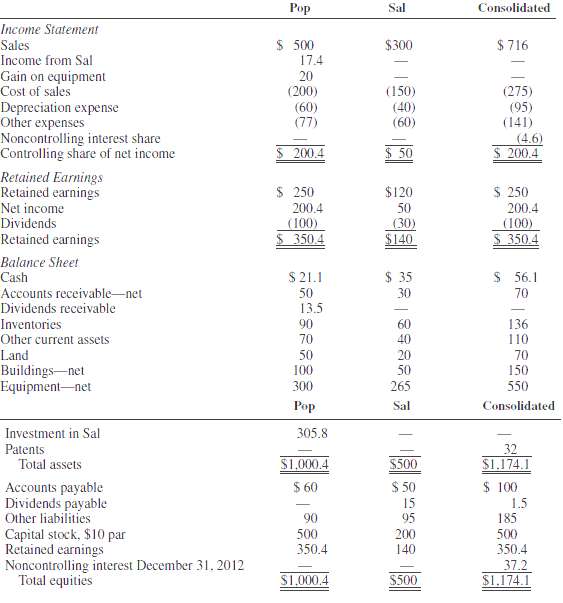

Separate company and consolidated financial statements for Pop Corporation and its only subsidiary, Sal Corporation, for 2012 are summarized here. Pop acquired its interest in Sal on January 1, 2011, at a price in excess of book value, which was due to an unrecorded patent. REQUIRED: Answer the

What reciprocal accounts arise when one company borrows from an affiliate?

Do direct lending and borrowing transactions between affiliates give rise to unrealized gains or losses? To unrecognized gains or losses?

What are constructive gains and losses? Describe a transaction having a constructive gain.

A company has a $1,000,000 bond issue outstanding with unamortized premium of $10,000 and unamortized issuance cost of $5,300. What is the book value of its liability? If an affiliate purchases half the bonds in the market at 98, what is the gain or loss? Is the gain or loss actual or constructive?

Compare a constructive gain on intercompany bonds with an unrealized gain on the intercompany sale of land.

Describe the process by which constructive gains on intercompany bonds are realized and recognized on the books of the affiliates. Does recognition of a constructive gain in consolidated financial statements precede or succeed recognition on the books of affiliates?

If a subsidiary purchases parent bonds at a price in excess of recorded book value, is the gain or loss attributed to the parent or the subsidiary? Explain.

The following information related to intercompany bond holdings was taken from the adjusted trial balances of a parent and its 90 percent-owned subsidiary four years before the bond issue matured: Construct the consolidation workpaper entries necessary to eliminate reciprocal balances (a) Assuming

Prepare a journal entry (or entries) to account for the parent’s investment income for the current year if the reported income of its 80 percent-owned subsidiary is $50,000 and the consolidated entity has a $4,000 constructive gain from the subsidiary’s acquisition of parent bonds.

Calculate the parent’s income from its 75 percent-owned subsidiary if the reported net income of the subsidiary for the period is $100,000 and the consolidated entity has a constructive loss of $8,000 from the parent’s acquisition of subsidiary bonds.

If a parent reports interest expense of $4,300 with respect to bonds held intercompany and the subsidiary reports interest income of $4,500 for the same bonds, (a) Was there a constructive gain or loss on the bonds? (b) Is the gain or loss attributed to the parent or the subsidiary? and (c) What

1. Which of the following is not a characteristic of a constructive retirement of bonds from an intercompany bond transaction?a. Bonds are retired for consolidated statement purposes only.b. The reciprocal intercompany bond investment and liability amounts are eliminated in the consolidation

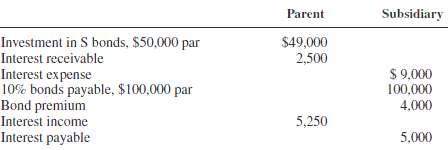

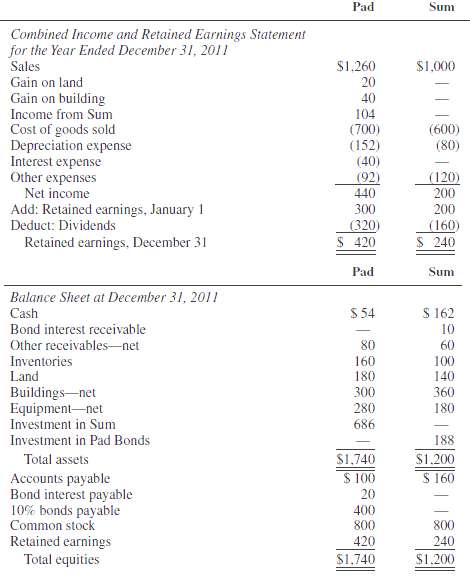

Sow Corporation is a 70 percent-owned subsidiary of Pan Corporation. On January 2, 2011, Sow purchased $600,000 par of Pan’s $900,000 outstanding bonds for $602,000 in the bond market. Pan’s bonds have an 8 percent interest rate, pay interest on January 1 and July 1, and mature on January 1,

Pat Company acquired an 80 percent interest in Sal Company on January 1, 2011, for $400,000 in excess of book value and fair value. On January 1, 2014, Pat had $1,000,000 par, 8 percent bonds outstanding with $40,000 unamortized discount. On January 2, 2014, Sal purchased $400,000 par of Pat’s

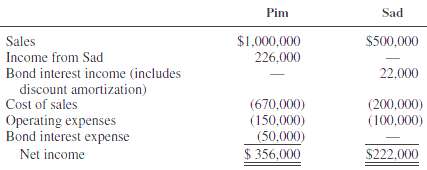

Comparative income statements for Pim Corporation and its 100 percent-owned subsidiary, Sad Corporation, for the year ended December 31, 2019, are summarized as follows: Pim purchased its interest in Sad at fair value equal to book value on January 1, 2011. On January 1, 2012, Pim sold $500,000

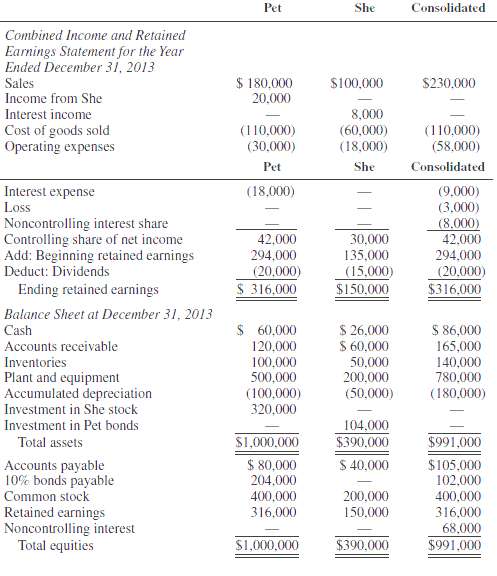

Pat Corporation owns a 70 percent interest in Son Corporation acquired several years ago at book value equal to fair value. On January 1, 2011, Son had outstanding $1,000,000 of 9 percent bonds with a book value of $990,000. On January 2, 2011, Pat purchased $500,000 of Son’s 9 percent bonds for

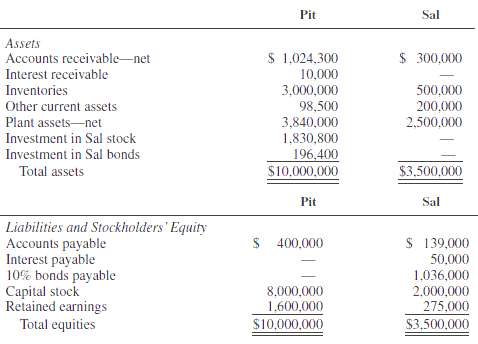

Comparative balance sheets of Pit and Sal Corporations at December 31, 2011, follow: Pit acquired 80 percent of Sal's capital stock for $1,660,000 on January 1, 2009, when Sal's capital stock was $2,000,000 and its retained earnings was $75,000. On January 2, 2011, Pit acquired $200,000 par of

The consolidated balance sheet of Par Corporation and Say (its 80 percent-owned subsidiary) at December 31, 2011, includes the following items related to an 8 percent, $1,000,000 outstanding bond issue: Current LiabilitiesBond interest payable (6 months’ interest due January 1, 2012) $

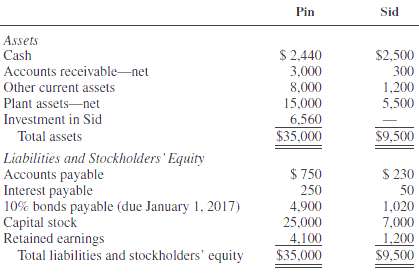

The balance sheets of Pin and Sid Corporations, an 80 percent-owned subsidiary of Pin, at December 31, 2011, are as follows (in thousands): The book value of Pin's bonds reflects a $100,000 unamortized discount. The book value of Sid's bonds reflects a $20,000 unamortized premium.REQUIRED1.

Pad Corporation has $2,000,000 of 12 percent bonds outstanding on December 31, 2011, with unamortized premium of $60,000. These bonds pay interest semiannually on July 1 and January 1 and mature on January 1, 2017. On January 2, 2012, Sal Corporation, an 80 percent-owned subsidiary of Pad,

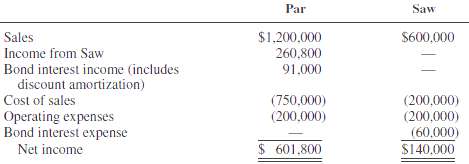

Comparative income statements for Par Corporation and its 80 percent-owned subsidiary, Saw Corporation, for the year ended December 31, 2012, are summarized as follows: Par purchased its 80 percent interest in Saw at book value on January 1, 2011, when Saw's assets and liabilities were equal to

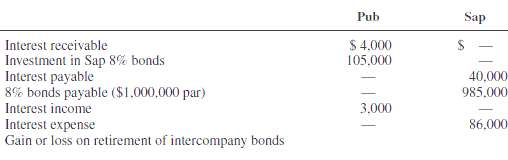

Pub Corporation, which owns an 80 percent interest in Sap Corporation, purchases $100,000 of Sap's 8 percent bonds at 106 on July 2, 2011. The bonds pay interest on January 1 and July 1 and mature on July 1, 2014. Pub uses the equity method for its investment in Sap. Selected data from the December

Pap Corporation acquired an 80 percent interest in Son Corporation at book value equal to fair value on January 1, 2012, at which time Son’s capital stock and retained earnings were $100,000 and $40,000, respectively. On January 2, 2013, Son purchased $50,000 par of Pap’s 8 percent, $100,000

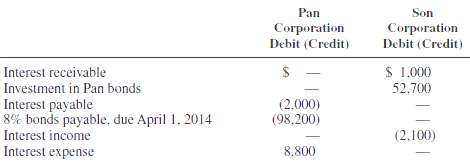

Partial adjusted trial balances for Pan Corporation and its 90 percent-owned subsidiary, Son Corporation, for the year ended December 31, 2011, are as follows: Son Corporation acquired $50,000 par of Pan bonds on April 2, 2011, for $53,600. The bonds pay interest on April 1 and October 1 and

Intercompany transactions between Pew Corporation and Sat Corporation, its 80 percent-owned subsidiary, from January 2011, when Pew acquired its controlling interest, to December 31, 2014, are summarized as follows: 2011 Pew sold inventory items that cost $60,000 to Sat for $80,000. Sat sold

Financial statements for Pad Corporation and its 75 percent-owned subsidiary, Sum Corporation, for 2011 are summarized as follows (in thousands): Pad acquired its interest in Sum at book value during 2008, when the fair values of Sum's assets and liabilities were equal to their recorded book

Pet Corporation acquired an 80 percent interest in She Corporation on January 1, 2011, for $320,000, at which time She had capital stock of $200,000 outstanding and retained earnings of $100,000. The price paid reflected a $100,000 undervaluation of She's plant and equipment. The plant and

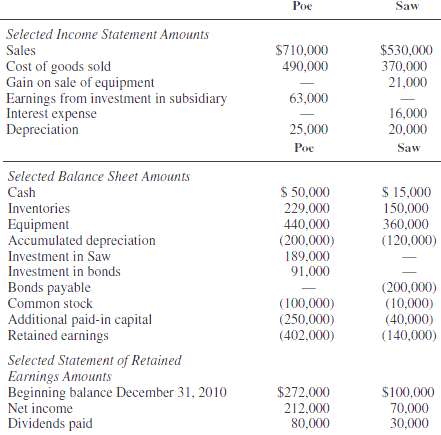

Selected amounts from the separate unconsolidated financial statements of Poe Corporation and its 90 percent-owned subsidiary, Saw Company, at December 31, 2011, are as follows. ADDITIONAL INFORMATION1. On January 2, 2011, Poe purchased 90 percent of Saw's 100,000 outstanding common stock for

Financial statements for Par Corporation and its 75 percent-owned subsidiary, Sal Corporation, for 2012 are summarized as follows (in thousands): Par Corporation acquired its interest in Sal at book value during 2009, when the fair values of Sal's assets and liabilities were equal to recorded

How are enterprise and internal service funds similar? How are they different?

Cite some governmental operations that might be accounted for through an internal service fund.

What fund financial statements are needed for an enterprise fund to meet the requirements for fair presentation in accordance with GAAP? Which government-wide statements include enterprise fund data?

Which fund financial statements include internal service fund data? Which government-wide statements include internal service fund data?

How does the presentation of an enterprise major fund differ from the presentation of an internal service major fund?

Because proprietary funds are accounted for in much the same manner as commercial business organizations, is it appropriate for FASB pronouncements to be used for their accounting?

Why is it important for internal service funds to differentiate between revenues generated by inter-fund transactions and transactions with external parties?

What fund types are included in the fiduciary fund category? Where are they reported in the financial statements?

How might an internal service fund be financed initially? How will the financing appear in the fund financial statements?

How does a private-purpose trust fund differ from a permanent fund?

How many columns (not including total columns) are needed for a government-wide statement of net assets of a governmental unit with a general fund, two special revenue funds, three internal service funds, four enterprise funds, and a component unit? Explain.

Do governmental financial statements indicate whether a pension plan is fully funded? Explain.

How might the enterprise fund amounts on the proprietary fund statement of net assets differ from the amounts reported as “business-type activities” on the government-wide statement of net assets?

1. Internal service funds are reported:a. With governmental funds on the fund financial statementsb. With governmental funds on the government-wide statement of net assetsc. With proprietary funds on the government-wide statement of net assetsd. All of the above2. Which of the following is not a

1. The billings for transportation services provided to other governmental units are recorded by the internal service fund as:a. Interfund exchangesb. Intergovernmental transfersc. Transportation appropriationsd. Operating revenues2. Which of the following transactions would be not allowed in an

1. Charges for services are a major source of revenue for:a. A debt service fundb. A trust fundc. An enterprise fundd. A capital projects fund2. A city provides initial financing for its enterprise fund with the stipulation that the amount advanced be returned to the general fund within five years.

1. Fiduciary funds include four different types of funds. Which of the following is not one of these types?a. Agency fundsb. Tax collection fundsc. Private-purpose trust fundsd. Pension trust funds2. Agency funds maintain accounts for:a. Liabilitiesb. Revenuesc. Fund balanced. Expenditures3. Funds

1. The following revenues were among those reported by Arvida Township in 2012:Net rental revenue (after depreciation) from......... $ 40,000a parking garage owned by ArvidaInterest earned on investments held foremployees’ retirement benefits............. 100,000Property

The City of Laramee established a tax agency fund to collect property taxes for the City of Laramee, Bloomer County, and Bloomer School District. Total tax levies of the three governmental units were $200,000 for 2011, of which $60,000 was for the City of Laramee, $40,000 for Bloomer County, and

Prepare journal entries to record the following grant-related transactions of an enterprise fund activity. Explain how these transactions should be reported in the enterprise fund’s financial statements, including the statement of cash flows.1. Received an operating grant in cash from the state,

For each of the following events or transactions, identify the fund or funds that will be affected.1. A governmental unit operates a municipal pool. Costs are intended to be recovered primarily from user charges.2. A bond offering was issued at par to subsidize the construction of a new convention

For each of the following events or transactions, prepare the necessary journal entry or entries and identify the fund or funds that will be affected.1. A governmental unit collects fees totaling $4,500 at the municipal pool. The fees are charged to recover costs of pool operation and

Note how each of the following transactions affects (a) Net assets invested in capital assets, net of related debt,(b) Restricted net assets, and (c) Unrestricted net assets. (Record N/A if there is no effect on the net asset section.)1. The sale of a building for a gain2. Depreciation of an

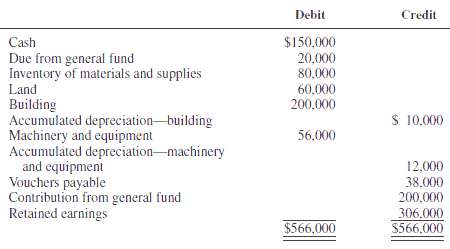

The City of Thomasville established an internal service fund to provide printing services to all city offices and departments. The following transactions related to the fund took place in 2011:1. On January 15 the general fund transferred equipment valued at $550,000 and provided a $500,000 loan to

The following transactions relate to the Fiedler County Utility Plant, a newly established municipal facility financed with debt secured solely by net revenue from fees and charges to external users.1. The general fund made a $30,000,000 contribution to establish the working capital of the new

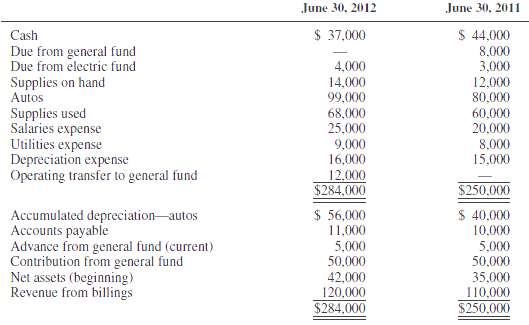

Comparative adjusted trial balances for the motor pool of Douwe County at June 30, 2011, and June 30, 2012, are as follows: REQUIREDPrepare fund financial statements for the motor pool for the year ended June 30, 2012. (The statement of cash flows is to beincluded.)

On January 1, 2011, J. G. Monee created a student aid trust fund to which he donated a building valued at $400,000 (his cost was $250,000), bonds having a market value of $500,000, and $100,000 cash. The trust agreement stipulated that principal was to be maintained intact and earnings were to be

On July 1, 2011, Duchy County receives a $500,000 contribution from the local chapter of Homeless No More. A trust agreement specifying that the income from the contribution be distributed each May 15 to the downtown homeless shelter accompanies the contribution. The principal amount is intended to

The City of Meringen operates a central garage through an internal service fund to provide garage space and repairs for all city-owned and -operated vehicles. The central garage fund was established by a contribution of $200,000 from the general fund, when the building was acquired several years

Caleb County had a beginning cash balance in its enterprise fund of $714,525. During the year, the following transactions affecting cash flows occurred:1. Acquired equity investments totaling $165,0002. Receipts from sales of goods or services totaled $3,276,5003. Payments for materials used in

1. Sam Corporation has 100,000 outstanding shares of $10 par common stock and 5,000 outstanding shares of $100 par, cumulative, 10 percent preferred stock. Sam’s net income for the year is $300,000, and its stockholders’ equity at year end is as follows (in thousands):10% cumulative preferred

Refer to the information in question 1. Assume that Sam pays two years’ preferred dividend requirements during the current year. Would this affect your computation of Par’s investment income for the current year? If so, recompute Par’s investment income.

How should preferred stock of a subsidiary be shown in a consolidated balance sheet in each case?(a) If it is held 100 percent by the parent(b) If it is held 50 percent by the parent and 50 percent by outside interests(c) If it is held 100 percent by outside interests

Showing 6400 - 6500

of 107766

First

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

Last

Step by Step Answers