New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

accounting

Advanced Accounting 11th Edition Floyd A. Beams, Joseph H. Anthony, Bruce Bettinghaus, Kenneth Smith - Solutions

Pat Corporation purchased 40 percent of the voting stock of Sue Corporation on July 1, 2011, for $300,000. On that date, Sue's stockholders' equity consisted of capital stock of $500,000, retained earnings of $150,000, and current earnings (just half of 2011) of $50,000. Income is earned

John Corporation acquired a 70 percent interest in Jojo Corporation on April 1, 2011, when it purchased 14,000 of Jojo's 20,000 outstanding shares in the open market at $13 per share. Additional costs of acquiring the shares consisted of $10,000 legal and consulting fees. Jojo Corporation's balance

When does a corporation become a subsidiary of another corporation?

In allocating the excess of investment fair value over book value of a subsidiary, are the amounts allocated to identifiable assets and liabilities (land and notes payable, for example) recorded separately in the accounts of the parent? Explain.

If the fair value of a subsidiary’s land was $100,000 and its book value was $90,000 when the parent acquired its 100 percent interest for cash, at what amount would the land be included in the consolidated balance sheet immediately after the acquisition? Would your answer be different if the

Define or explain the terms parent company, subsidiary company, affiliates, and associates.

What is a noncontrolling interest?

Describe the circumstances under which the accounts of a subsidiary would not be included in the consolidated financial statements.

A summary of changes in Pen Corporation's Investment in Sam account from January 1, 2011, to December 31, 2013, follows (in thousands): ADDITIONAL INFORMATION1. Pen acquired its 80 percent interest in Sam Corporation when Sam had capital stock of $1,200,000 and retained earnings of $600,000.2.

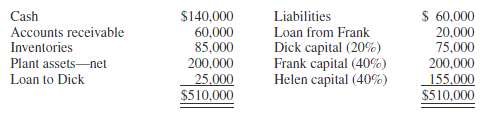

Pop Corporation acquired a 70 percent interest in Stu Corporation on January 1, 2011, for $1,400,000, when Stu's stockholders' equity consisted of $1,000,000 capital stock and $600,000 retained earnings. On this date, the book value of Stu's assets and liabilities was equal to the fair value,

In what general ledger would you expect to find the account “goodwill from consolidation”?

How should the parent’s investment in subsidiary account be classified in a consolidated balance sheet? In the parent’s separate balance sheet?

Name some reciprocal accounts that might be found in the separate records of a parent and its subsidiaries.

Why are reciprocal amounts eliminated in preparing consolidated financial statements?

How does the stockholders’ equity of the parent that uses the equity method of accounting differ from the consolidated stockholders’ equity of the parent and its subsidiaries?

Is there a difference in the amounts reported in the statement of retained earnings of a parent that uses the equity method of accounting and the amounts that appear in the consolidated retained earnings statement?

Is noncontrolling interest share an expense? Explain.

Describe how total noncontrolling interest at the end of an accounting period is determined.

What special procedures are required to consolidate the statements of a parent that reports on a calendar year basis and a subsidiary whose fiscal year ends on October 31?

Does the acquisition of shares held by noncontrolling shareholders constitute a business combination?

1. A 75 percent-owned subsidiary should not be consolidated when:a. Its operations are dissimilar from those of the parent companyb. Control of the subsidiary does not lie with the parent companyc. T here is a dominant noncontrolling interest in the subsidiaryd. M nagement feels that consolidation

1. Under GAAP, a parent company should exclude a subsidiary from consolidation if:a. I t measures income from the subsidiary under the equity methodb. T he subsidiary is in a regulated industryc. T he subsidiary is a foreign entity whose books are recorded in a foreign currencyd. T he parent and

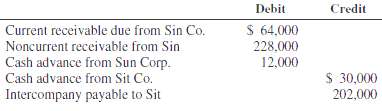

1. Cobb Company's current receivables from affiliated companies at December 31, 2011, are (1) a $75,000 cash advance to Hill Corporation (Cobb owns 30 percent of the voting stock of Hill and accounts for the investment by the equity method), (2) a receivable of $260,000 from Vick Corporation for

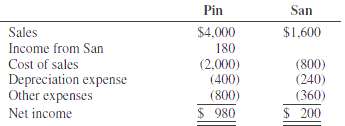

Pin Corporation paid $1,800,000 for a 90 percent interest in San Corporation on January 1, 2011; San's total book value was $1,800,000. The excess was allocated as follows: $60,000 to undervalued equipment with a three-year remaining useful life and $140,000 to goodwill. The income statements of

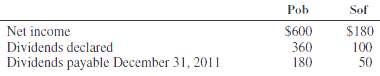

On December 31, 2011, the separate-company financial statements for Pan Corporation and its 70 percent-owned subsidiary, Sad Corporation, had the following account balances related to dividends (in thousands): REQUIRED1. At what amount will dividends be shown in the consolidated retained earnings

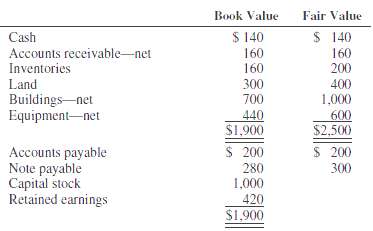

Book values and fair values of Sli Corporation's assets and liabilities on December 31, 2010, are as follows (in thousands): On January 1, 2011, Por Corporation acquires all of Sli's capital stock for $2,500,000 cash. The acquisition is recorded using push-down accounting.REQUIRED1. Prepare the

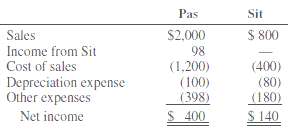

Summary income statement information for Pas Corporation and its 70 percent-owned subsidiary, Sit, for the year 2012 is as follows (in thousands): REQUIRED: 1. Assume that Pas acquired its 70 percent interest in Sit at book value on January 1, 2011, when the fair value of Sits' assets and

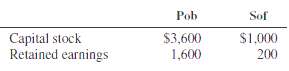

Pob Corporation acquired an 80 percent interest in Sof Corporation on January 2, 2011, for $1,400,000. On this date the capital stock and retained earnings of the two companies were as follows (in thousands): The assets and liabilities of Sof were stated at fair values equal to book values when

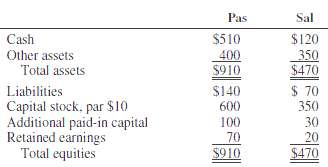

Pas and Sal Corporations' balance sheets at December 31, 2010, are summarized as follows (in thousands): Pas acquired 80 percent of the voting stock of Sal on January 2, 2011, at a cost of $320,000. The fair values of Sal's net assets were equal to book values on January 2, 2011. During 2011, Pas

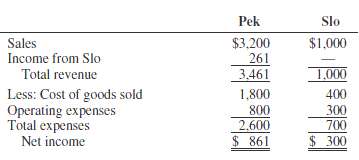

Comparative income statements of Pek Corporation and Slo Corporation for the year ended December 31, 2013, are as follows (in thousands): ADDITIONAL INFORMATION1. Slo is a 90 percent-owned subsidiary of Pek, acquired by Pek for $1,620,000 on January 1, 2011, when Slo's stockholders' equity at

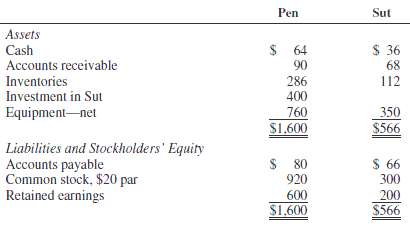

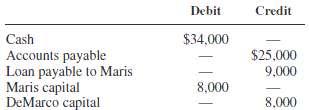

On December 31, 2011, Pen Corporation purchased 80 percent of the stock of Sut Company at book value. The data reported on their separate balance sheets immediately after the acquisition follow. At December 31, 2011, Pen Corporation owes Sut $10,000 on accounts payable. (All amounts are in

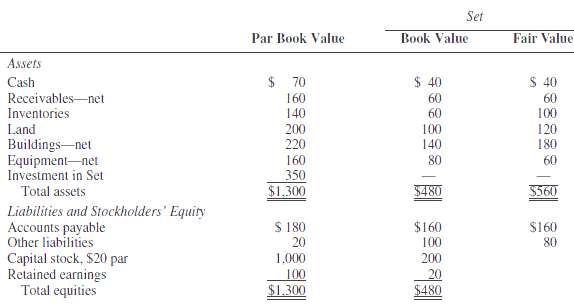

Par Corporation acquired 70 percent of the outstanding common stock of Set Corporation on January 1, 2011, for $350,000 cash. Immediately after this acquisition the balance sheet information for the two companies was as follows (in thousands): REQUIRED1. Prepare a schedule to allocate the

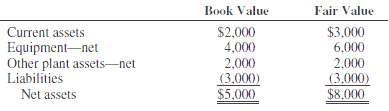

PJ Corporation pays $5,400,000 for an 80 percent interest in Sof Corporation on January 1, 2011, at which time the book value and fair value of Sof's net assets are as follows (in thousands): REQUIRED: Prepare a schedule to allocate the fair value/book value differentials to Sof's netassets.

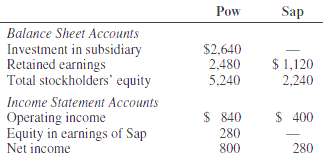

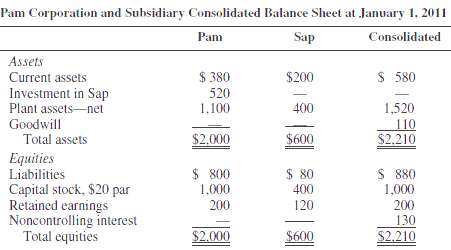

Pam Corporation purchased a block of Sap Company common stock for $520,000 cash on January 1, 2011. Separate-company and consolidated balance sheets prepared immediately after the acquisition are summarized as follows (in thousands): REQUIRED: Reconstruct the schedule to allocate the fair

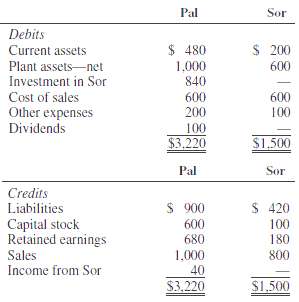

Adjusted trial balances for Pal and Sor Corporations at December 31, 2011, are as follows (in thousands): Pal purchased all the stock of Sor for $800,000 cash on January 1, 2011, when Sor's stockholders' equity consisted of $100,000 capital stock and $180,000 retained earnings. Sor's assets and

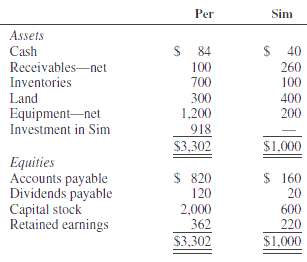

Per Corporation paid $900,000 cash for 90 percent of Sim Corporation's common stock on January 1, 2011, when Sim had $600,000 capital stock and $200,000 retained earnings. The book values of Sim's assets and liabilities were equal to fair values. During 2011, Sim reported net income of $40,000 and

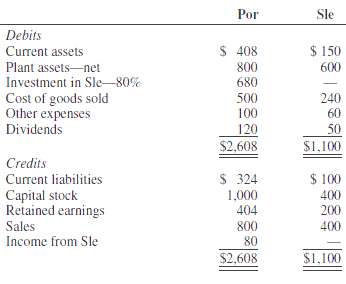

Por Corporation acquired 80 percent of the outstanding stock of Sle Corporation for $560,000 cash on January 3, 2011, on which date Sle's stockholders' equity consisted of capital stock of $400,000 and retained earnings of $100,000. There were no changes in the outstanding stock of either

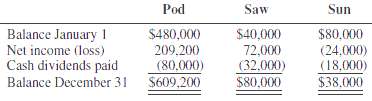

On January 1, 2011, Pod Corporation made the following investments: 1. Acquired for cash, 80 percent of the outstanding common stock of Saw Corporation at $140 per share. The stockholders' equity of Saw on January 1, 2011, consisted of the following: Common stock, par value $100 $100,000 Retained

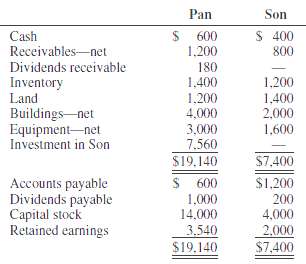

Pan Corporation purchased 90 percent of Son Corporation's outstanding stock for $7,200,000 cash on January 1, 2011, when Son's stockholders' equity consisted of $4,000,000 capital stock and $1,400,000 retained earnings. The excess was allocated $1,600,000 to undervalued equipment with an eight-year

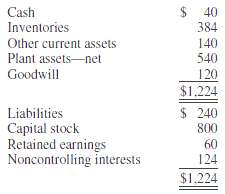

The consolidated balance sheet of Pan Corporation and its 80 percent subsidiary, Sun Corporation, contains the following items on December 31, 2015 (in thousands): Pan Corporation uses the equity method of accounting for its investment in Sun. Sun Corporation stock was acquired by Pan on January

How does partnership liquidation differ from partnership dissolution?

What is a simple partnership liquidation, and how are distributions to partners computed?

UPA specifies a priority ranking for distribution of partnership assets in liquidation. What is the ranking?

What is the right of offset rule? How does it affect the amount to be distributed to partners in a liquidation?

What assumptions are made in determining the amount of distributions (or safe payments) to individual partners prior to the recognition of all gains and losses on liquidation?

What are partner equities? Why are partner equities rather than partner capital balances used in the preparation of safe payments schedules?

How do safe payments computations affect partnership ledger account balances?

What is a statement of partnership liquidation, and how is the statement helpful to partners and other parties involved in partnership liquidation?

A partnership in liquidation has satisfied all of its non-partner liabilities and has cash available for distribution to partners. Under what circumstances would it be permissible to divide available cash in the profit and loss sharing ratios of the partners?

What are vulnerability ranks? How are they used in the preparation of cash distribution plans for partnership liquidations?

If a partnership is insolvent, how is the amount of cash distributed to individual partners determined?

When all partnership assets have been distributed in the liquidation of a partnership, some partners may have debit capital balances and others may have credit capital balances. How are such balances eliminated if the partners with debit balances are personally solvent? If they are personally

The partnership of Folly and Frill is in the process of liquidation. On January 1, 2011, the ledger shows account balances as follows: On January 10, 2011, the lumber inventory is sold for $25,000, and during January, accounts receivable of $21,000 are collected. No further collections on the

After closing entries were made on December 31, 2011, the ledger of Mike, Nan, and Okey contained the following balances: Due to unsuccessful operations, the partners decide to liquidate the business. During January some of the inventory is sold at cost for $10,000, and on January 31, 2012, all

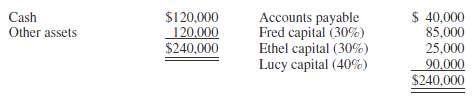

Fred, Ethel, and Lucy have decided to liquidate their partnership. Account balances on January 1, 2011, are as follows: The partners agree to keep a $10,000 contingency fund and to distribute available cashimmediately.

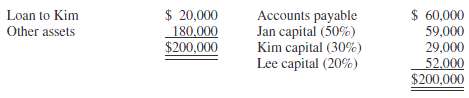

Jan, Kim, and Lee announce plans to liquidate their partnership immediately. The assets, equities, and profit and loss sharing ratios are summarized as follows. The other assets are sold for $120,000, and an overlooked bill for landscaping services of $5,000 is discovered. Kim cannot pay her

The profit and loss sharing agreement of the partnership of Ali, Bart, and Carrie provides a salary allowance for Ali and Carrie of $10,000 each. Partners receive a 10 percent interest allowance on their average capital balances for the year. The remainder is divided 40 percent to Ali, 20 percent

A condensed balance sheet with profit sharing percentages for the Evers, Freda, and Grace partnership on January 1, 2011, shows the following: On January 2, 2011, the partners decide to liquidate the business, and during January they sell assets with a book value of $300,000 for$170,000.

The partnership of Alice, Betty, and Carle became insolvent during 2011, and the partnership ledger shows the following balances after all partnership assets have been converted into cash and all available cash distributed: Profit and loss sharing percentages for the three partners are Alice, 30

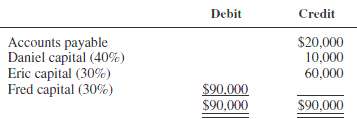

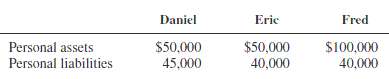

After all partnership assets were converted into cash and all available cash distributed to creditors, the ledger of the Daniel, Eric, and Fred partnership showed the following balances: The percentages indicated are residual profit and loss sharing ratios. Personal assets and liabilities of the

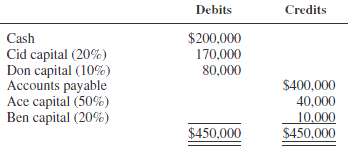

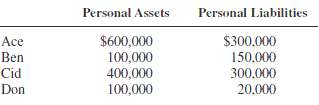

The partnership of Ace, Ben, Cid, and Don is dissolved on January 5, 2011, and the account balances at June 30, 2011, after all non-cash assets are converted into cash, are as follows: 1. The percentages indicated represent the relevant profit and loss sharing ratios.2. Personal assets and

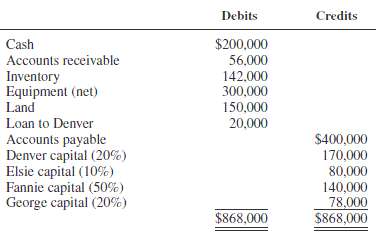

The partnership of Denver, Elsie, Fannie, and George is being liquidated over the first few months of 2011. The trial balance at January 1, 2011, is as follows: 1. The partners agree to retain $20,000 cash on hand for contingencies and to distribute the rest of the available cash at the end of

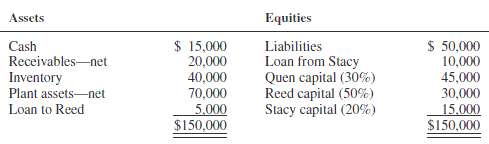

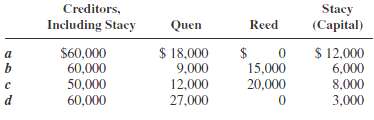

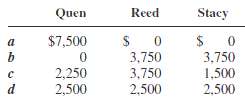

The assets and equities of the Quen, Reed, and Stacy partnership at the end of its fiscal year on October 31, 2011, are as follows: The partners decide to liquidate the partnership. They estimate that the non-cash assets, other than the loan to Reed, can be converted into $100,000 cash over the

1. In a partnership liquidation, the final cash distribution to the partners should be made in accordance with the: a. Partner profit and loss sharing ratios b. Balances of partner capital accounts c. Ratio of the capital contributions by partners d. Safe payments computations 2. In accounting for

Barney, Betty, and Rubble are partners in a business that is in the process of liquidation. On January 1, 2011, the ledger accounts show the balances indicated: The cash is distributed to partners on January 1, 2011. Inventory and supplies are sold for a lump-sum price of $81,000 on February 9,

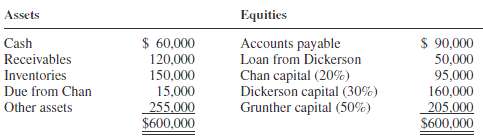

The December 31, 2011, balance sheet of the Chan, Dickerson, and Grunther partnership, along with the partners' residual profit and loss sharing ratios, is summarized as follows: The partners agree to liquidate their partnership as soon as possible after January 1, 2012, and to distribute all

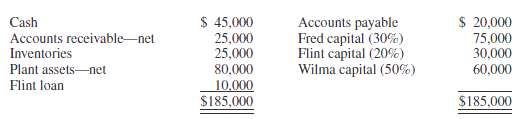

Fred, Flint, and Wilma announced the liquidation of their partnership beginning on January 1, 2011. Profits and losses are divided 30 percent to Fred, 20 percent to Flint, and 50 percent to Wilma. Balance sheet items are summarized as follows: REQUIREDPrepare a cash distribution plan as of

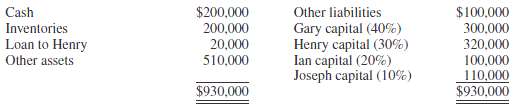

The partnership of Gary, Henry, Ian, and Joseph is preparing to liquidate. Profit and loss sharing ratios are shown in the summarized balance sheet at December 31, 2011, as follows: REQUIRED1. The partners anticipate an installment liquidation. Prepare a cash distribution plan as of January 1,

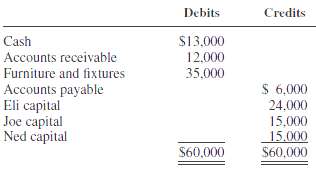

Eli, Joe, and Ned agree to liquidate their consulting practice as soon as possible after the close of business on July 31, 2011. The trial balance on that date shows the following account balances: The partners share profits and losses 20 percent, 30 percent, and 50 percent to Eli, Joe, and Ned,

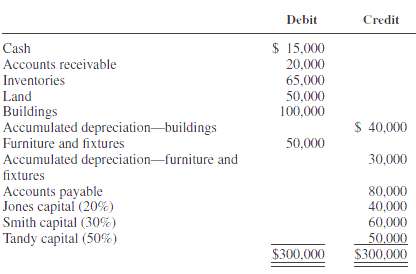

Jones, Smith, and Tandy are partners in a furniture store that began liquidation on January 1, 2011, when the ledger contained the following account balances: The following transactions and events occurred during the liquidation process:January Inventories were sold for $20,000 cash, collections

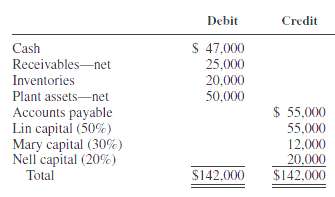

The after-closing trial balance of the Lin, Mary, and Nell partnership at December 31, 2011, was as follows: ADDITIONAL INFORMATION1. The partnership is to be liquidated as soon as the assets can be converted into cash. Cash realized on conversion of assets is to be distributed as it becomes

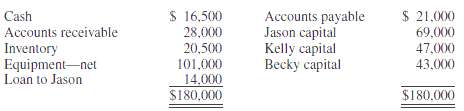

Jason, Kelly, and Becky, who share partnership profits 50 percent, 30 percent, and 20 percent, respectively, decide to liquidate their partnership. They need the cash from the partnership as soon as possible but do not want to sell the assets at fire-sale prices, so they agree to an installment

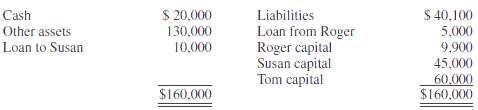

The balance sheet of Roger, Susan, and Tom, who share partnership profits 30 percent, 30 percent, and 40 percent, respectively, included the following balances on January 1, 2011, the date of dissolution: During January 2011, part of the firm's assets are sold for $40,000. In February the

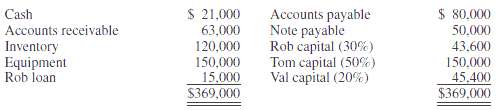

Account balances for the Rob, Tom, and Val partnership on October 1, 2011, are as follows: The partners have decided to liquidate the business. Activities for October and November are as follows:October1. Rob is short of funds, and the partners agree to charge her loan to her capital account.2.

The adjusted trial balance of the Jee, Moore, and Olsen partnership at December 31, 2011, is as follows:Cash ............ $ 50,000Accounts receivable—net .... 100,000Nonmonetary assets ....... 800,000Expenses .......... 400,000Total

The after-closing trial balances of the Beams, Plank, and Timbers partnership at December 31, 2011, included the following accounts and balances:Cash ................. $120,000Accounts receivable—net.......... 140,000Inventory................ 200,000Plant assets—net.............

Bankruptcy proceedings may be designated as voluntary or involuntary . Distinguish between the two types, including the requirements for filing of an involuntary petition.

What are the duties of the U.S. trustee under BAPCPA? Do U.S. trustees supervise the administration of all bankruptcy cases?

What obligations does a debtor corporation have in a bankruptcy case?

Is a trustee appointed in Title 11 cases? In all Chapter 7 cases? Discuss.

Describe the duties of a trustee in a liquidation case under the BAPCPA 1978.

Which unsecured claims have priority in a Chapter 7 liquidation case? Discuss in terms of priority ranks.

Does the BAPCPA establish priorities for holders of unsecured non-priority claims (that is, general unsecured claims)?

What is the purpose of a statement of affairs, and how are assets valued in this statement?

Does filing a case under Chapter 11 of the bankruptcy act mean that the company will not be liquidated? Discuss.

What is a debtor-in-possession reorganization case?

When can a creditors’ committee file a plan of reorganization under a Chapter 11 case?

Discuss the requirements for approval of a plan of reorganization.

Describe prepetition liabilities subject to compromise on the balance sheet of a company operating under Chapter 11 of the bankruptcy act.

The reorganization value of a firm emerging from Chapter 11 bankruptcy is used to determine the accounting of the reorganized company. Explain reorganization value as used in FASB ASC 852.

FASB ASC 852 provides two conditions that must be met for an emerging firm to use fresh-start reporting. What are these two conditions?

A firm emerging from Chapter 11 bankruptcy that does not qualify for fresh-start reporting must still report the effect of the reorganization plan on its financial position and results of operations. How is debt forgiveness reported in the reorganized company’s financial statements?

1. Bankruptcy Insolvency means:a. Book value of assets is greater than liabilitiesb. Fair value of assets is less than liabilitiesc. Inability to meet financial obligations as they come dued. Liabilities are greater than book value of assets2. Aside from liability discharge provided for in the

Use the following information in answering questions 1 and 2:Hal Company filed for protection from creditors under Chapter 11 of the bankruptcy act on July 1, 2011. Hal had the following liabilities at the time of filing: 10% mortgage bonds payable, secured by a buildingwith a book value and

Ram holds a $200,000 note receivable from Pat. It has been learned that Pat filed for Chapter 7 bankruptcy and that the expected recovery of non-secured claims is 35¢ on the dollar. Inventory items with an estimated recoverable value of $50,000 secure Pat’s note payable to Ram.REQUIRED Determine

Bax has been operating under Chapter 11 of the Bankruptcy Code for the past 15 months. On March 31, 2011, just before confirmation of its reorganization plan, Bax’s reorganization value is estimated at $2,000,000. A balance sheet for Bax prepared on the same date is summarized as follows:Current

Hol is in bankruptcy and is being liquidated by a court-appointed trustee. The financial report that follows was prepared by the trustee just before the final cash distribution:AssetsCash..................... $ 200,000Approved ClaimsMortgage payable (secured by property that wassold

The balance sheet of Sco appeared as follows on March 1, 2011, when an interim trustee was appointed by the U.S. trustee to assume control of Sco's estate in a Chapter 7 case. ADDITIONAL INFORMATION1. Creditors failed to elect a trustee; accordingly, the interim trustee became trustee for the

Justin Corporation filed a petition under Chapter 7 of the bankruptcy act in January 2011. On March 15, 2011, the trustee provided the following information about the corporation's financial affairs. REQUIRED1. Determine the amount expected to be available for unsecured claims.2. Determine the

Fabulous Fakes Corporation is being liquidated under Chapter 7 of the bankruptcy act. All assets have been converted into cash, and $374,500 cash is available to pay the following claims:1. Administrative expenses of preserving and liquidating the debtorcorporation’s estate

Showing 6100 - 6200

of 107766

First

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

Last

Step by Step Answers