New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

accounting

Financial Accounting and Reporting 14th Edition Barry Elliott, Jamie Elliott - Solutions

On 1 October year 1, RPS plc issued one million £1 5% redeemable preference shares. The shares were issued at a discount of £50,000 and are due to be redeemed on 30 September Year 5. Dividends are paid on 30 September each year.Required:Show the accounting treatment of the preference shares

October 20X1, Little Raven plc issued 50,000 debentures, with a par value of £100 each, to investors at £80 each. The debentures are redeemable at par on 30 September 20X6 and have a coupon rate of 6%, which was significantly below the market rate of interest for such debentures issued at

On 1 January 2009 Henry Ltd issued a convertible debenture for €200 million carrying a coupon interest rate of 5%. The debenture is convertible at the option of the holders into 10 ordinary shares for each €100 of debenture stock on 31 December 2013. Henry Ltd considered borrowing the €200

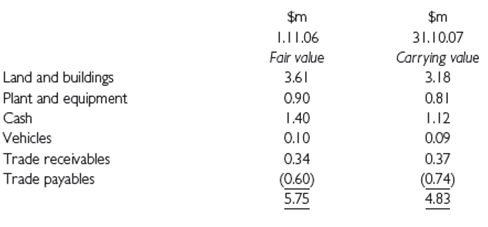

George plc adopted IFRS for the first time on 1 January 2008 and has three different instruments whose accounting George is concerned will change as a result of the adoption of the standard. The three instruments are:1. An investment in 15% of the ordinary shares of Joshua Ltd, a private company.

Isabelle Limited borrows £100,000 from a bank on the following terms:(i) Arrangement fees of £2,000 are charged by the bank and deducted from the initial proceeds on the loan;(ii) Interest is payable at 5% for the first 3 years of the loan and then increases to 7% for the remaining 2 years of the

A company borrows on a floating rate loan, but wishes to hedge against interest variations so swaps the interest for fixed rate. The swap should be perfectly effective and has zero fair value at inception. Interest rate increase and therefore the swap becomes a financial asset to the company at

Charles plc is applying IAS 32 and IAS 39 for the first time this year and is uncertain about the application of the standard. Charles plc balance sheet is as follows:Note1. The forward contracts have been revalued to fair value in the balance sheet. They do not qualify as hedging

KathrynKathryn plc, a listed company, provides a defined benefit pension for its staff, the details of which are given below.Pension schemeAs at the 30 April 2004, actuaries valued the company’s pension scheme and estimated that the scheme had assets of £10.5 million and obligations of £10.2

Donna IncDonna Inc operates a defined benefit pension scheme for staff. The pension scheme has been operating for a number of years but not following IAS 19. The finance director is unsure of which accounting policy to adopt under IAS 19 because he has heard very conflicting stories. He went to one

The following information (in £m) relates to the defined benefit scheme of Basil plc for the year ended 31 December 20X7:Fair value of plan assets at 1 January 20X7 £3,150 and at 31 December 20X7 £2,384; contributions £26; current service cost £80; benefits paid £85; past service cost £150;

C plc wants to reward its directors for their service to the company and has designed a bonus package with two different elements as follows. The directors are informed of the scheme and granted any options on 1 January 20X7.1. Share options over 300,000 shares that can be exercised on 31 December

The following information is available for the year ended 31 March 20X6 (values in $m):Present value of scheme liabilities at 1 April 20X5 $1,007; Fair value of plan assets at 1 April 20X5 $844; Benefits paid $44; Expected return on plan assets $67; Contributions paid by employers $16; Current

(a) IAS 19 Employee Benefits was amended in December 2004 to allow a choice of methods for the recognition of actuarial gains and losses.Required:Explain the treatments of actuarial gains and losses currently permitted by IAS 19.(b) The following information relates to the defined benefit employees

On 1 October 2005 Omega granted 50 employees options to purchase 500 shares in the entity.The options vest on 1 October 2007 for those employees who remain employed by the entity until that date. The options allow the employees to purchase the shares for $10 per share. The market price of the

On 1 January 20X1 the company obtained a contract in order to keep the factor y in work but had obtained it on a very tight profit margin. Liquidity was a problem and there was no prospect of offering staff a cash bonus. Instead, the company granted its 80 production employees share options for

In your capacity as chief assistant to the financial controller, your managing director has asked you to explain to him the differences between tax planning, tax avoidance and tax evasion.He has also asked you to explain to him your feelings as a professional accountant about these topics.Write

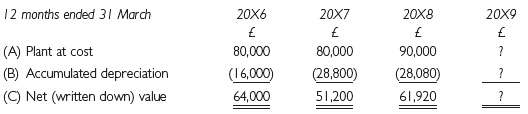

A fixed asset (a machine) was purchased by Adjourn plc on 1 July 20X2 at a cost of £25,000. The company prepares its annual accounts to 31 March in each year. The policy of the company is to depreciate such assets at the rate of 15% straight line (with depreciation being charged pro rata on a time

The move from the preparation of accounts under UK GAAP to the users of IFRS by United Kingdom quoted companies for years beginning 1 January 2005 had an effect on the level of profits reported. How will those profits arising from the change in accounting standards be treated for taxation purposes?

Discuss the arguments for and against discounting the deferred tax charge.

Austin Mitchell MP proposed an Early Day Motion in the House of Commons on 17 May 2005 as follows: That this House urges the Government to clamp down on artificial tax avoidance schemes and end the . . . tax avoidance loop-holes that enable millionaires and numerous companies trading in the UK to

Dee For has recently qualified as a pilot and is now intending to set up a private company in the near future to run small charter passenger flights from her home town. Most of her business plan has been written but she has recently learned that the company’s forecast statement of comprehensive

The following information is given in respect of Unambitious plc:(a) Non-current assets consist entirely of plant and machinery. The net book value of these assets as at 30 June 2010 is £100,000 in excess of their tax written-down value.(b) The provision for deferred tax (all of which relates to

(a) Discuss why IAS 40 Investment Property was produced.(b) Universal Entrepreneurs plc has the following items on its PPE list:(i) £1,000,000 – the right to extract sandstone from a particular quarry. Geologists predict that extraction at the present rate may be continued for ten years.(ii)

MercuryYou have been given the task, by one of the partners of the firm of accountants for which you work, of assisting in the preparation of a trend statement for a client.Mercury has been in existence for four years. Figures for the three preceding years are known but those for the fourth year

In the year to 31 December 20X9, Amy bought a new machine and made the following payments in relation to it:Required:(a) State and justify the cost figure which should be used as the basis for depreciation.(b) What does depreciation do, and why is it necessary?(c) Briefly explain, without numerical

The finance director of the Small Machine Parts Ltd company is considering the acquisition of a lease of a small workshop in a warehouse complex that is being redeveloped by City Redevelopers Ltd at a steady rate over a number of years. City Redevelopers are granting such leases for five years on

Simple SA has just purchased a roasting/salting machine to produce roasted walnuts. The finance director asks for your advice on how the company should calculate the depreciation on this machine.Details are as follows:Cost of machine ........ SF800,000Residual value ........ SF104,000Estimated life

(a) IAS 16 Property, Plant and Equipment requires that where there has been a permanent diminution in the value of property, plant and equipment, the carrying amount should be written down to the recoverable amount. The phrase ‘recoverable amount’ is defined in IAS 16 as ‘the amount which the

Infinite Leisure Group owns and operates a number of pubs and clubs across Europe and South East Asia. Since inception the group has made exclusive use of the cost model for the purpose of its annual financial reporting. This has led to a number of shareholders expressing concern about what they

The Blissopia Leisure Group consists of three divisions: Blissopia 1, which operates mainstream bars; Blissopia 2, which operates large restaurants; and Blissopia 3, which operates one hotel – the Eden.Divisions 1 and 2 have been trading very successfully and there are no indications of any

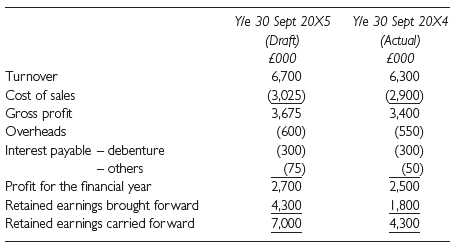

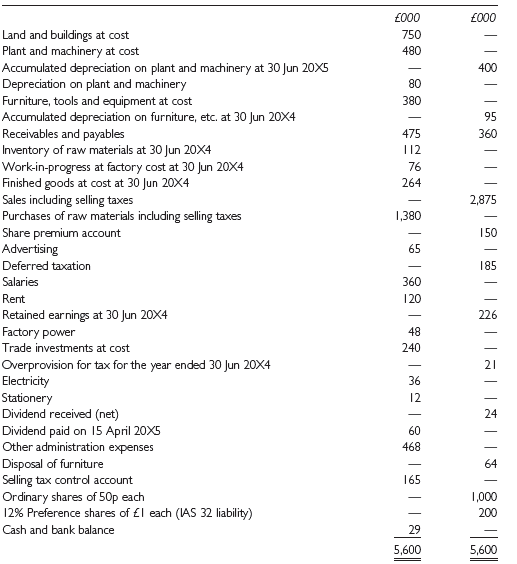

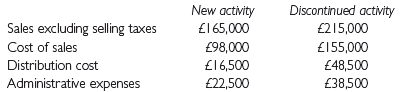

Cryptic plc extracted its trial balance on 30 June 20X5 as follows:The following information is relevant:(i) The company discontinued a major activity during the year and replaced it with another. All noncurrent assets involved in the discontinued activity were redeployed for the new one. The

On 1 January 20X8, Grabbit plc entered into an agreement to lease a widgeting machine for general use in the business. The agreement, which may not be terminated by either party to it, runs for six years and provides for Grabbit to make an annual rental payment of £92,500 on 31 December each year.

(a) When accounting for finance leases, accountants prefer to overlook legal form in favour of commercial substance.Required:Discuss the above statement in the light of the requirements of IAS 17 Leases.(b) State briefly how you would distinguish between a finance lease and an operating lease.(c)

The Mission Company Ltd, whose year-end is 31 December, has acquired two items of machinery on leases, the conditions of which are as follows:Item Y: Ten annual instalments of £20,000 each, the first payable on 1 January 20X0. The machine was completely installed and first operated on 1 January

X Ltd entered into a lease agreement on the following terms:Cost of leased asset ........... £100,000Lease term ............... 5 yearsRentals six-monthly in advance ...... £12,000Anticipated residual on disposal of theassets at end of lease term ......... £10,000Lessee’s interest in residual

At 1 January 20X5 Bridge Finance plc agreed to finance the lease of machinery costing $37,200 to Rapid Growth plc at a lease cost of $10,000 per annum payable at the end of the year, namely 31 December. The period of the lease is five years. Bridge Finance plc incurred direct costs of $708 in

Alpha entered into an operating lease under which it was committed to five annual payments of £50,000 per year. It was subsequently decided to treat the lease as a Right-of-use asset reported on the Statement of financial position. Alpha’s borrowing rate was 10%.Required:Calculate the amount to

Construction first provides finance and financial solutions to companies in the construction industry. On 1 January 2007 the company agreed to finance the lease of equipment costing $145,080 to Bodge Brothers over its useful life of five years at an annual rental of $39,000 payable annually in

Environmental Engineering plc is engaged in the development of an environmentally friendly personal transport vehicle. This will run on an electric motor powered by solar cells, supplemented by passenger effort in the form of pedal assistance.At the end of the current accounting period, the

As chief accountant at Italin NV, you have been given the following information by the director of research:Project Luca €000Costs to date (pure research 25%, applied research 75%) .......... 200Costs to develop product (to be incurred in the year to 30 September

Oxlag plc, a manufacturer of pharmaceutical products, has the following research and development projects on hand at 31 January 20X2:(A) A general survey into the long-term effects of its sleeping pill Chalcedon upon human resistance to infections. At the year-end the research is still at a basic

International Accounting Standards IFRS 3 and IAS 38 address the accounting for goodwill and intangible assets.Required:(a) Describe the requirements of IFRS 3 regarding the initial recognition and measurement of goodwill and intangible assets.(b) Explain the proposed approach set out by IFRS 3 for

The brands debateUnder IAS 22, the depletion of equity reserves caused by the accounting treatment for purchased goodwill resulted in some companies capitalising brands on their statements of financial position. This practice was started by Rank Hovis McDougall (RHM) – a company which has since

Brands plc is preparing its accounts for the year ended 31 October 20X8 and the following information is available relating to various intangible assets acquired on the acquisition of countrywide plc.(a) A milk quota of 2,000,000 litres at 30p per litre. There is an active market trading in milk

IAS 38 – Intangible Assets – was primarily issued in order to identify the criteria that need to be present before expenditure on intangible items can be recognised as an asset. The standard also prescribes the subsequent accounting treatment of Intangible Assets that satisfy the recognition

(a) Explain what is meant by €˜component depreciation€™ and its status under inter national accounting standards.(b) Trin, a limited liability company, owns its business premises. It has just installed extensive specialized machinery and fittings in the premises. The estimated

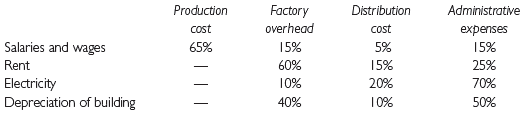

Sunhats Ltd manufactures patent hats. It carries inventor y of these and sells to wholesalers and retailers via a number of salespeople. The following expenses are charged in the profit and loss account:Wages of: Storemen and factor y foremenSalaries of: Production manager, personnel officer,

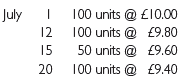

Purchases of a certain product during July were:Units sold during the month were:Required:Assuming no opening inventories:(i) Determine the cost of goods sold for July under three different valuation methods.(ii) Discuss the advantages and/or disadvantages of each of these methods.(iii) A physical

Alpha Ltd makes one standard article. You have been given the following information:1. The inventor y sheets at the year-end show the following items:Raw materials:100 tons of steel:Cost £140 per tonPresent price £130 per tonFinished goods:100 finished units:Cost of materials £50 per unitLabour

Beta Ltd commenced business on 1 January and is making up its first year€™s accounts. The company uses standard costs. The company owns a variety of raw materials and components for use in its manufacturing business. The accounting records show the following:Raw materials control account

The statement of comprehensive income of Bottom, a manufacturing company, for the year ending 31 January 20X2 is as follows:Bottom$000Revenue ......... 75,000Cost of sales ...... (38,000)Gross profit ....... 37,000Other operating expenses . (9,000)Profit from operations ... 28,000Investment

Agriculture is a key business activity in many parts of the world, particularly in developing countries. Following extensive discussions with, and funding from, the World Bank, the International Accounting Standards Committee (IASC) developed an accounting standard relating to agricultural

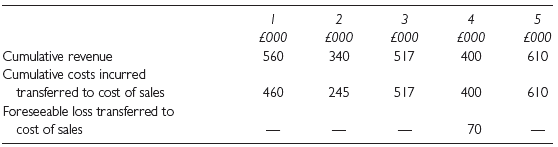

MACTAR have a series of contracts to resurface sections of motor ways. The scale of the contract means several years’ work and each motor way section is regarded as a separate contract.Required:From the following information, calculate for each contract the amount of profit (or loss) you would

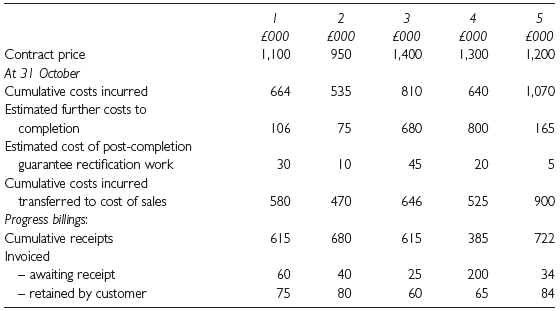

At 31 October 20X0, Lytax Ltd was engaged in various contracts including five long-term contracts, details of which are given below:It is not expected that any customers will default on their payments.Up to 31 October 20X9, the following amounts have been included in the revenue and cost of sales

During its financial year ended 30 June 20X7 Beavers, an engineering company, has worked on several contracts. Information relating to one of them is given below:Contract X201Date commenced ............. 1 July 20X6Original estimate of completion date 30 September .. 20X7Contract price

Newbild SA commenced work on the construction of a block of flats on 1 July 20X0.During the period ended 31 March 20X1 contract expenditure was as follows: €Materials issued from stores ... 13,407Materials delivered direct to site ..

Good Progress SpA entered into a contract on 1.1.20X0 at a contract price of 1,000,000 and an estimated total profit of 250,000. The contract was due for completion on 31.12.20X4.The following information was available.As at 31.12.20X0:The contract was 25% complete and an architect’s certificate

(a) A concession company, WaterAway, has completed the construction of a wastewater plant. The plant will be transferred to the public sector unconditionally after 25 years. The public sector (the grantor) makes payments related to the volume of wastewater processed.Discuss how this will be dealt

Quickbuild Ltd entered into a two-year contract on 1 January 20X7 at a contract price of 250,000. The estimated cost of the contract was 150,000. At the end of the first year the following information was available:● Contract costs incurred totalled 70,000;● Inventories still unused at the

(a) During 2006, Jack Matelot set up a company, JTM, to construct and refurbish marinas in various ports around Europe. The company’s first accounting period ended on 31 October 2006 and during that period JTM won a contract to refurbish a small marina in St Malo, France. During the year

(a) Assume that on 1 January 20X7 Parent Ltd acquired all the ordinary shares in Daughter Ltd for £10,800 cash. The fair value of the net assets in Daughter Ltd was their book value.(b) The purchase consideration was satisfied by the issue of 5,400 new ordinary shares in Parent Ltd. The fair

(a) On 1 January 20X7 Parent Ltd acquired all the ordinary shares in Daughter Ltd for £16,200 cash. The fair value of the net assets in Daughter Ltd was their book value.(b) The purchase consideration was satisfied by the issue of 5,400 new ordinary shares in Parent Ltd. The fair value of a

(a) On 1 January 20X7 Parent Ltd acquired all the ordinary shares in Daughter Ltd for £16,200 cash. The fair value of the net assets in Daughter Ltd was £12,000.(b) The purchase consideration was satisfied by the issue of 5,400 new ordinary shares in Parent Ltd. The fair value of a

On 1 January 20X7 Parent Ltd acquired all the ordinary shares in Daughter Ltd for £6,000 cash. The fair value of the net assets in Daughter Ltd was their book value.Required:Prepare the statements of financial position of Parent Ltd and the consolidated statement of financial position as at 1

On 1 January 20X7 Parent Ltd acquired 75% of the ordinary shares in Daughter Ltd for £9,000 cash. The fair value of the net assets in Daughter Ltd was their book value. Assume in each case that the non-controlling interest is measured using method 1.Required:Prepare the statements of

The following accounts are the consolidated statement of financial position and parent company statement of financial position for Alpha Ltd as at 30 June 20X2.Notes:(i) There was only one subsidiary called Beta Ltd.(ii) There were no capital reserves in the subsidiary.(iii) Alpha produced

Rouge plc acquired 100% of the common shares of Noir plc on 1 January 20X0 and gained control. At that date the statements of financial position of the two companies were as follows:Required: Prepare a consolidated statement of financial position for Rouge plc as at 1 January20X0.

Ham plc acquired 100% of the common shares of Burg plc on 1 January 20X0 and gained control. At that date the statements of financial position of the two companies were as follows:Notes:1 The fair value is the same as the book value.2 £15,000 of the negative goodwill arises because the net

Set out below is the summarized statement of financial position of Berlin plc at 1 January 20X0. £000ASSETS Non-current assets Property, plant and equipment ...... 250Current assets ............ 150Total assets

Bleu plc acquired 80% of the common shares of Verte plc on 1 January 20X0 and gained control. At that date the statements of financial position of the two companies were as follows:Note: The fair values are the same as the book values.Required: Prepare a consolidated statement of financial position

Base plc acquired 60% of the common shares of Ball plc on 1 January 20X0 and gained control. At that date the statements of financial position of the two companies were as follows:Note:The fair value of the property, plant and equipment in Ball at 1/1/20X0 was £120,000. The fair value of the

On 1 January 20X0 Hill plc purchased 70% of the ordinary shares of Valley plc for £1.3 million. The fair value of the non-controlling interest at that date was £0.5 million. At the date of acquisition, Valley€™s retained earnings were £0.6 million.The statements of

Sweden acquired 100% of the equity shares of Oslo on 1 March 20X1 and gained control. At that date the balances on the reserves of Oslo were as follows:The Revaluation reserve – Kr10 millionRetained earnings – Kr70 millionThe statements of financial position of the two companies at

Summer plc acquired 60% of the common shares of Winter Ltd on 30 September 20X1 and gained control. At the date of acquisition, the balance of retained earnings of Winter was £35,000. At 31 December 20X1 the statements of financial position of the two companies were as follows:Notes:1 The fair

On 30 September 20X0 Gold plc acquired 75% of the equity shares, 30% of the preferred shares and 20% of the bonds in Silver plc and gained control. The balance of retained earnings on 30 September 20X0 was £16,000. The fair value of the land owned by Silver was £3,000 above book value.

Prop and Flap have produced the following statements of financial position as at 31 October 2008:The following information is relevant to the preparation of the financial statements of the Prop Group:(i) Prop acquired 80% of the issued ordinary share capital of Flap many years ago when the

Bill plc acquired 80% of the common shares and 10% of the preferred shares in Ben plc on 31 December three years ago when Ben€™s accumulated retained profits were £45,000. During the year Bill sold Ben goods for £8,000 plus a mark-up of 50%. Half of these goods were still in

Morn Ltd acquired 90% of the shares in Eve Ltd on 1 January 20X1 for £90,000 when Eve Ltd€™s accumulated profits were £50,000. On 10 January 20X1 Morn Ltd received a dividend of £10,800 from Eve Ltd out of the profits for the year ended 31/12/20X0. On 31/12/20X1 Morn

River plc acquired 90% of the common shares and 10% of the 5% bonds in Pool Ltd on 31 March 20X1. All income and expenses are deemed to accrue evenly through the year. On 31 January 20X1 River sold Pool goods for £6,000 plus a markup of one-third. 75% of these goods were still in stock at the

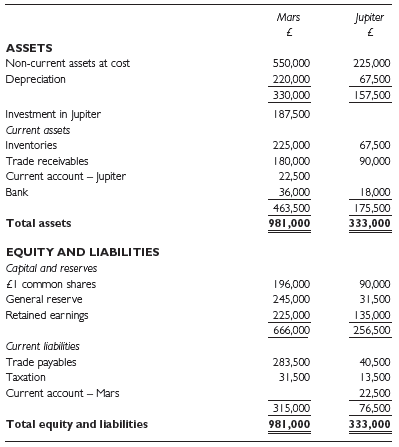

The statements of financial position of Mars plc and Jupiter plc at 31 December 20X2 are as follows:Statements of comprehensive income for the year ended 31 December 20X2Mars acquired 80% of the shares in Jupiter on 1 January 20X0 when Jupiter’s retained earnings were £80,000 and the

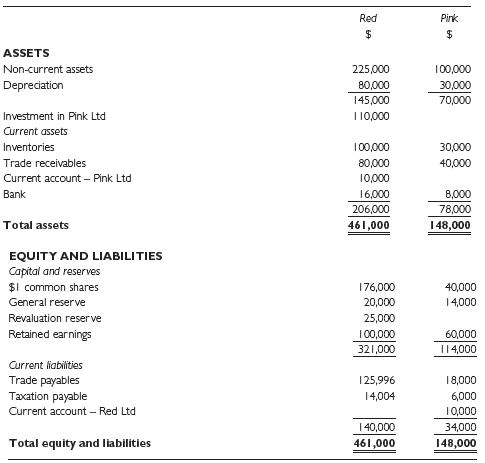

The statements of financial position of Red Ltd and Pink Ltd at 31 December 20X2 are as follows:Statements of comprehensive income for the year ended 31 December 20X2Red Ltd acquired 75% of the shares in Pink Ltd on 1 January 20X0 when Pink Ltd’s retained earnings were $30,000 and the

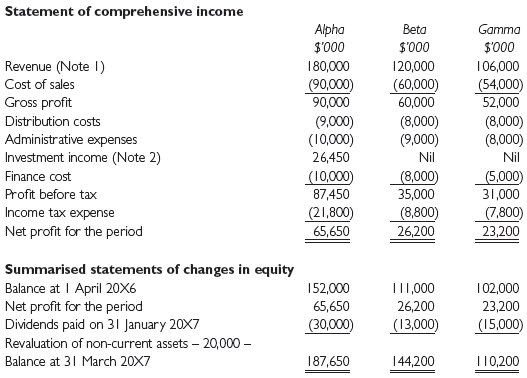

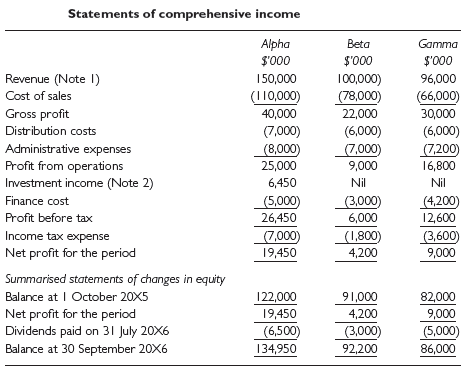

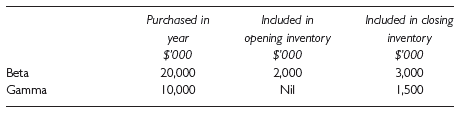

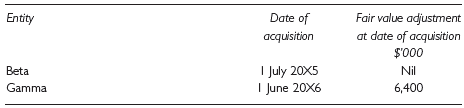

Alpha has owned 80% of the equity shares of Beta since the incorporation of Beta. On 1 July 20X6 Alpha purchased 60% of the equity shares of Gamma. The statements of comprehensive income and summarized statements of changes in equity of the three entities for the year ended 31 March 20X7 are given

H Ltd has one subsidiary, S Ltd. The company has held a controlling interest for several years. The latest financial statements for the two companies and the consolidated financial statements for the H Group are as shown below:Goodwill of £410,000 was written off at the date of acquisition

The following are the financial statements of White and its subsidiary Brown as at 30 September 20X9The following information is also available:(i) White purchased its ordinary shares in Brown on 1 September 20X4 when Brown had credit balances on reserves of £0.5 million and on retained

Hyson plc acquired 75% of the shares in Green plc on 1 January 20X0 for £6 million when Green plc€™s accumulated profits were £4.5 million. At acquisition, the fair values of Green€™s non-current assets were £1.2 million in excess of their carrying value. The

Forest plc acquired 80% of the ordinary shares of Bulwell plc some years ago. At acquisition, the fair values of the assets of Bulwell plc were the same as their carrying value. Bulwell plc manufactures plant and equipment.On 1 January 20X3, Bulwell sold an item of plant & equipment to Forest plc

The following are the financial statements of the parent company Swish plc, a subsidiary company Broom and an associate company Handle.Statement of comprehensive income for the year ended 31 December 20X3Swish acquired 90% of the shares in Broom on 1 January 20X1 when the balance on the retained

Set out below are the financial statements of Ant Co., its subsidiary Bug Co. and an associated company Nit Co. for the accounting year-end 31 December 20X9.Statements of comprehensive income for the year ended 31 December 20X9Ant Co. acquired 80% of the shares in Bug Co. on 1 January 20X7 when

Alpha has owned 75% of the equity shares of Beta since the incorporation of Beta. Therefore, Alpha has prepared consolidated financial statements for some years. On 1 July 20X6 Alpha purchased 40% of the equity shares of Gamma. The statements of comprehensive income and summarised statements of

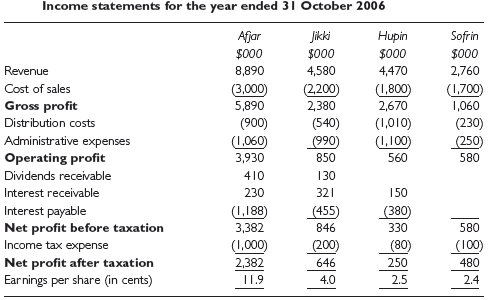

The following are the statements of comprehensive income of four companies for the year ended 31 October 2006, the end of their most recent financial year.The following additional information is available:(a) All shares issued by the companies have a face value of $1.(b) The companies made the

The statements of comprehensive income for Continent plc, Island Ltd and River Ltd for the year ended 31 December 20X9 were as follows:Continent plc acquired 80% of Island Ltd for ‚¬27,500 on 1 January 20X3, when Island Lid€™s retained earnings were ‚¬22,000 and share

The statements of comprehensive income for Highway plc, Road Ltd and Lane Ltd for the year ended 31 December 20X9 were as follows:Highway plc acquired 80% of Road Ltd for $160,000 on 1.1.20X6 when Road Ltd€™s share capital was $64,000 and reserves were $16,000.Highway plc acquired 30% of

The following are the financial statements of the parent company Alpha plc, a subsidiary company Beta and an associate company Gamma.On 1 January 20X5 Alpha plc acquired 80% of Beta plc for £216,000 when Beta plc€™s share capital and reserves were £81,000 and 30% of Gamma Ltd

The following are the statements of financial position of Garden plc, its subsidiary Rose Ltd and its associate Petal Ltd:On 1 January 20X3 Garden plc acquired 75% of Rose Ltd for £300,000 when Rose€™s share capital and reserves were £252,000. At the date of acquisition, the

Fr y Ltd has the following foreign currency transactions in the year to 31/12/20X0:15/11 Buys goods for $40,000 on credit from Texas Inc15/11 Sells goods for $60,000 on credit to Alamos Inc20/11 Pays Texas Inc $40,000 for the goods purchased20/11 Receives $30,000 on account from Alamos Inc in

Alpha plc had an issued share capital of 2,000,000 ordinary shares at 1 January 20X1. The nominal value was 25p and the market value £1 per share. On 30 September 20X1 the company made a rights issue of 1 for 4 at a price of 80p per share. The post-tax earnings were £4.5m and £5m for 20X0 and

Beta Ltd had the following changes during 20X1:1 January 1,000,000 shares of 50c each31 March 500,000 shares of 50c each issued at full market price of $5 per share30 April Bonus issue made of 1 for 231 August 1,000,000 shares of 50c each issued at full market price of $5.50 per share31 October

The computation and publication of earnings per share (EPS) figures by listed companies are governed by IAS 33 Earnings per Share.Notes:1 Called-up share capital of Nottingham Industries plc:In issue at 1 April 20X5:16,000,000 ordinary shares of 25p each1,000,000 10% cumulative preference shares of

The following information relates to Simrin plc for the year ended 31 December 20X0:Simrin plc had 100,000 ordinary shares of £1 each in issue throughout the year. Simrin plc has in issue warrants entitling the holders to subscribe for a total of 50,000 shares in the company. The warrants may

Gamma plc had an issued share capital at 1 April 20X0 of:● £200,000 made up of 20p shares.● 50,000 £1 convertible preference shares receiving a dividend of £2.50 per share:– These shares were convertible in 20X6 on the basis of 1 ordinary share for 1 preference share.There was also loan

Showing 27800 - 27900

of 107766

First

272

273

274

275

276

277

278

279

280

281

282

283

284

285

286

Last

Step by Step Answers

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)