New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

data analytics accounting

ISE Data Analytics For Accounting 3rd Edition Ryan A. Teeter, Vernon Richardson, Katie L. Terrell - Solutions

Click the top supplier group in the first visualization to filter the data. How many purchase orders were made to that group?

Click the top supplier group in the first visualization to filter the data. What is the total amount of purchases from that group?

(LO 6-4) Analysis: How do you think sentiment analysis of the 10-K might assess the level of bias (positive or negative) of the annual reports? If management is too positive about the results of the company, can that be viewed as being neutral or impartial?

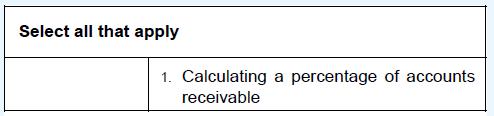

(LO 6-4) Analysis: How could artificial intelligence be used to help with the evaluation of the estimate for the allowance for doubtful accounts? Could past allowances be tested for their predictive ability that might be able to help set allowances in the current period?

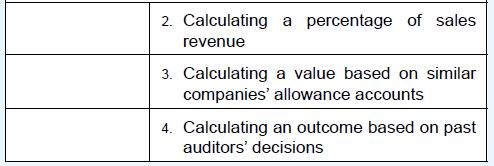

(LO 6-4) Which of the following methods illustrate the use of artificial intelligence to evaluate the allowance for doubtful accounts? Select all that apply 1. Calculating a percentage of accounts receivable

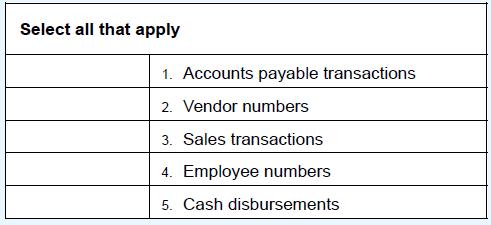

(LO 6-3) Analysis: What would a Benford’s law evaluation of sales transaction amounts potentially show? What would a test of vendor numbers or employee numbers show? Anything different from a test of invoice or check numbers? Are there any cases where Benford’s law wouldn’t work?

(LO 6-3) Which distributions would you recommend be tested using Benford’s law? Select all that apply 1. Accounts payable transactions 2. Vendor numbers 3. Sales transactions 4. Employee numbers 5. Cash disbursements

(LO 6-2, 6-3) In a certain company, one accountant records most of the adjusting journal entries at the end of the month. What type of analysis could be used to identify that this happens, as well as the cumulative size of the transactions the accountant records? Select all that apply 1.

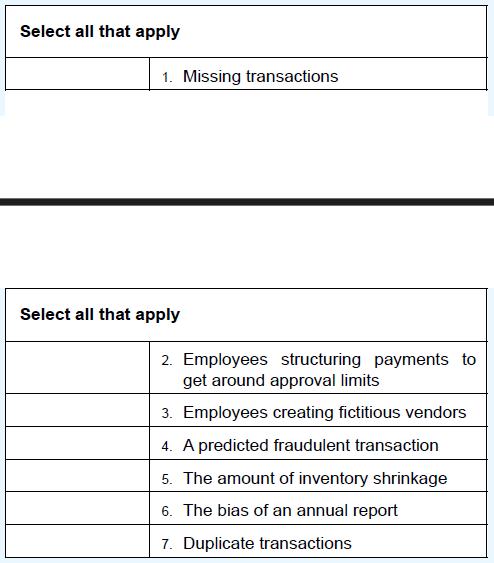

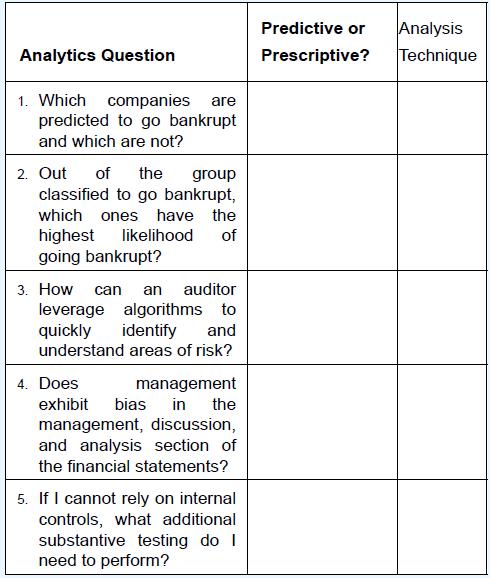

(LO 6-3) What are some patterns that could be found using diagnostic analysis? Select all that apply 1. Missing transactions Select all that apply 2. Employees structuring payments to get around approval limits 3. Employees creating fictitious vendors 4. A predicted fraudulent transaction 5. The

(LO 6-3) Analysis: How is a Z-score greater than 3.0 (or –3.0) useful in finding extreme values? What type of analysis should we do when we find extreme or outlier values?

(LO 6-1) Analysis: One of the benefits of Data Analytics is the ability to see and test the full population. In that case, why is sampling still used, and how is it useful?

(LO 6-2) Analysis: Why are auditors particularly interested in the aging of accounts receivable? How does this analysis help evaluate management judgment on collectability of receivables? Would a dashboard item reflecting this aging be useful in a continuous audit?

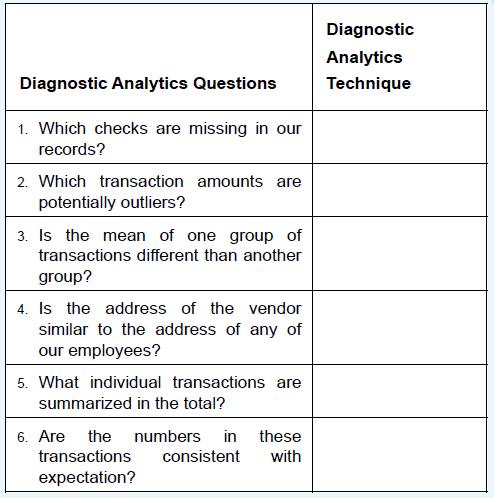

(LO 6-3) Match the analytics question to the following predictive and prescriptive analytics techniques.Classification Regression Probability Sentiment analysis What-if analysis Artificial Intelligence Analytics Question 1. Which companies are predicted to go bankrupt and which are not? 2. Out of

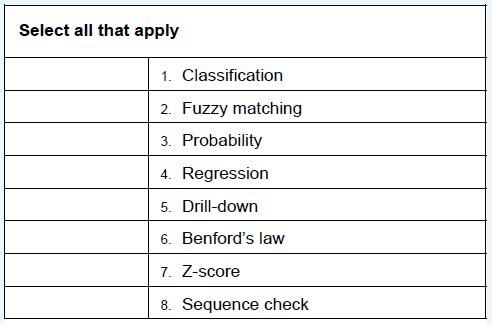

(LO 6-3) Match the diagnostic analytics questions to the following diagnostic analytics techniques.Z-score t-Test Benford’s law Drill-down Fuzzy matching Sequence check Diagnostic Analytics Questions 1. Which checks are missing in our records? 2. Which transaction amounts are potentially

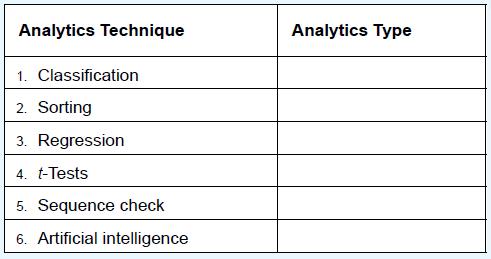

(LO 6-1) Match the analytics type (descriptive, diagnostic, predictive, or prescriptive) to each analytics technique. Analytics Technique 1. Classification 2. Sorting 3. Regression 4. t-Tests 5. Sequence check 6. Artificial intelligence Analytics Type

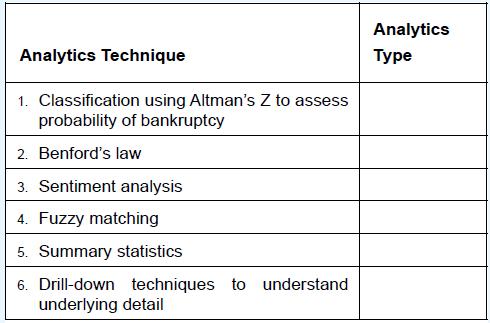

(LO 6-1) Match the analytics type (descriptive, diagnostic, predictive, or prescriptive) to each analytics technique. Analytics Technique 1. Classification using Altman's Z to assess probability of bankruptcy 2. Benford's law 3. Sentiment analysis 4. Fuzzy matching 5. Summary statistics 6.

(LO 6-2) One type of descriptive analytics is simply sorting data. Why is seeing extreme values helpful (minimums, maximums, counts, etc.) in evaluating accuracy and completeness and in potentially finding errors and fraud and the like?

(LO 6-3) Using Table 6-2 as a guide, compare and contrast predictive and prescriptive analytics. How might these be used in an audit? Or a continuous audit?

(LO 6-1) When do you believe Data Analytics will add value to the audit process?How can it most help?

(LO 6-1) How do nature, extent, and timing of audit procedures help us identify when to apply Data Analytics to the audit process?

(LO 6-3) What type of analysis would help auditors find missing checks?a. Sequence checkb. Benford’s law analysisc. Fuzzy matchingd. Decision support systems

(LO 6-4) Which testing approach would be useful in assessing the value of inventory shrinkage given multiple environmental factors?a. Probabilityb. Sentiment analysisc. Regressiond. Applied statistics

(LO 6-4) Which testing approach would be used to predict whether certain cases should be evaluated as having fraud or no fraud?a. Classificationb. Probabilityc. Sentiment analysisd. Artificial intelligence

(LO 6-3) What describes finding correspondences between at least two types of text or entries that may not match perfectly?a. Incomplete linkagesb. Algorithmic matchingc. Fuzzy matchingd. Incomplete matching

(LO 6-2, 6-3, 6-4) Which type of audit analytics might be used to find hidden patterns or variables linked to abnormal behavior?a. Prescriptive analyticsb. Predictive analyticsc. Diagnostic analyticsd. Descriptive analytics

(LO 6-1) The determinants for sample size include all of the following except:a. confidence level.b. tolerable misstatement.c. potential risk of account.d. estimated misstatement.

(LO 6-2) Which audit technique is used to test completeness?a. Benford’s lawb. Sequence checkc. Summary statisticsd. Drill-down

(LO 6-1) Which items would be currently out of the scope of Data Analytics?a. Direct observation of processesb. Evaluation of time stamps to evaluate workflowc. Evaluation of phantom vendorsd. Duplicate payment of invoices

If sentiment analysis is used on a product advertisement, would you guess the overall sentiment would be positive or negative?

Why would a bankruptcy prediction be considered classification? And why would it be useful to auditors?

Let’s say a company has nine divisions, and each division has a different check number based on its division—so one starts with “1,” another with “2,” and so on. Would Benford’s law work in this situation?

A sequence check will help us to see if there is a duplicate payment to vendors.Why is that important for the auditor to find?

How does the computation of summary statistics (mean, mode, median, max, min, etc.) meet the definition of descriptive analytics?

What type of descriptive analytics would you use to find negative numbers that were entered in error?

In a continuous audit, how would a dashboard help to communicate audit findings and spur a response?

Using Exhibit 6-2 as a guide, compare and contrast descriptive and diagnostic analytics. How might these be used in an audit?page 289

Characterize the predictive and prescriptive analytics used in auditing.

Define and describe diagnostic analytics that are used in auditing.

Explain basic descriptive analytic techniques used in auditing.

Understand different types of analysis for auditing and when to use them.

What other filters might you include to satisfy the requirements of the auditor, financial accountant, or tax preparer from Part 1?

How does limiting the range of values improve the performance of your model?

Why would you want to set filters before you begin creating your analyses?

As a tax preparer, what additional data would you need to calculate your tax liability?

As a financial accountant, what data quality issues might you consider when calculating net sales?

As a manager, which measures would you most likely be interested in when evaluating store performance?

As an auditor, why might you be interested in expanding the date range when evaluating sales data?

As a tax preparer, which attribute would you most likely filter?

As a financial accountant, which attribute would you most likely filter?

As a manager, which attribute would you most likely filter?

As an auditor, which attribute would you most likely filter?

How does this evaluation help you identify opportunities for automation in the analytics process?

What is the most common frequency identified for the audit procedures?

Do you find that most of your identified procedures are manual or automatic?

What analyses could you do to evaluate these rules?

Which attributes were difficult to locate or in unexpected places in the dataset?

Read the first audit action sheet. What other data elements that are not listed in the procedures do you think would be useful in analyzing this account?

Where are most of these attributes located?

What is the most common attribute that you identified to evaluate?

How many attributes/fields are available in the dataset?

Looking at the files in your shared folder, what other files would you expect to be updated frequently?

How does version history act as a control for data files?

How many new employees were added to the Employee_Listing file?

What has changed between the two versions of the Audit Plan file?

How do you think these files can be used for data analysis?

Explore the two folders you just uploaded. What kinds of documents and files do you see?

What advantage is there to sharing files in one location rather than emailing copies back and forth?

What is the link to your shared folder?

Who is the most likely user of these shared working papers?

How many files are in the Current File?

How many files are in the Master File?

How else would you analyze purchase transactions?

What would happen if you change the data source to another file that is formatted following the audit data standard for purchase orders?

What do you think the ePay Cardholder account is used for?

Which user, represented by an actual name, spent the most?

How much was spent by the biggest business unit?

Which business unit spent the most?

How much was spent on the highest spending day?

Which date of this dataset had the highest total purchase amount?

Which three categories received the most purchases?

Look at the fields that you removed in the data transformation. What types of analysis can you no longer perform with those missing data?

How does transforming the data to a common data model help make analysis easier in the future?

Why do you think it is important to combine cardholder names in your data before you conduct your analysis?

How many attributes or columns appear in your cleaned dataset?

How many records or rows appear in your cleaned dataset, excluding the header?

(LO 5-3) Analysis: Implementing continuous auditing procedures is similar to automating an audit plan with the additional step of scheduling the automated procedures to match the timing and frequency of the data being evaluated and the notification to the auditor when exceptions occur. In your

(LO 5-4) Multiple Choice: What actions should be taken by either internal auditors or management if a company’s continuous audit system has too many missed abnormal events (such as false negatives)?a. Ignore the alarms.b. Abandon the system.c. Change the parameters to focus on lower-risk items.d.

(LO 5-4) Multiple Choice: What actions should be taken by either internal auditors or management if a company’s continuous audit system has too many alarms that are false positive?a. Abandon the system.b. Change the parameters to focus on lower-risk items.c. Change the parameters to focus on

(LO 5-1) Multiple Choice: Auditors can apply simple to complex Data Analytics to a client’s data. At which stage would DA be applied to identify which areas the auditor should focus on?a. Continuousb. Planningc. Remoted. Reportinge. Performance

(LO 5-2) Analysis: Who developed the audit data standards? In your opinion, why is it the right group to develop and maintain them rather than, say, the Big Four firms or a small practitioner? What is purpose of the data standards and to whom are the standards applicable?

(LO 5-2) Multiple Choice: Consider Exhibit 5-3. Looking at the audit data standards order-to-cash process, which of the following describes the purpose of the AR Adjustments table?a. Shows the balance in accounts receivableb. Shows manual changes to accounts receivables, such as credit and debit

(LO 5-2) Analysis: What are the advantages of the use of homogeneous systems?Would a merger target be more attractive if it used a similar financial reporting system as the potential parent company?

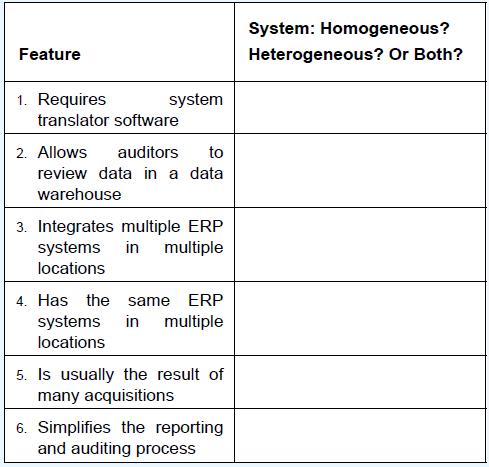

(LO 5-2) Companies have primarily homogeneous systems or heterogeneous systems. Identify the system that relates to each feature listed below. (Select “Both”from the feature column if more than one feature is applicable.) Feature 1. Requires system translator software 2. Allows auditors to

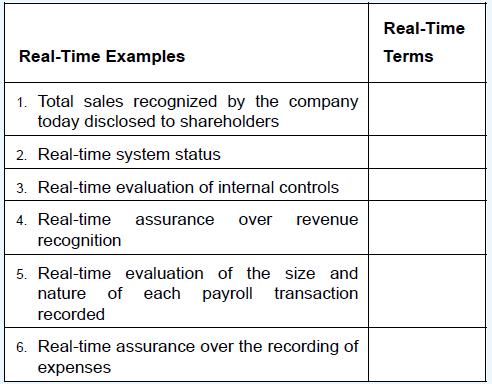

(LO 5-1, 5-2, 5-4, 5-5) Match the definitions to these real-time terms:Continuous reporting Continuous auditing Continuous monitoring Real-Time Examples 1. Total sales recognized by the company today disclosed to shareholders 2. Real-time system status 3. Real-time evaluation of internal controls

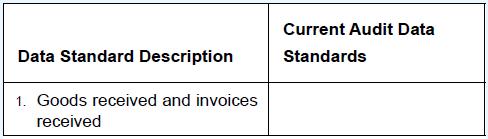

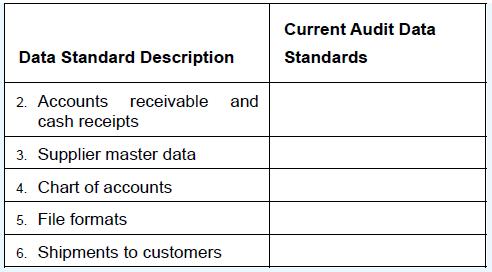

(LO 5-2) Match the description of the data standard to each of the current audit data standards:Base General Ledger Order-to-Cash Subledger Procure-to-Pay Subledger Data Standard Description 1. Goods received and invoices received Current Audit Data Standards

(LO 5-5) Why would audit firms prefer to use proprietary workpapers rather than just storing working papers on the cloud?

(LO 5-2) Would an auditor view heterogeneous systems as an audit risk? Why or why not?

(LO 5-2) Why is it better to extract data from a data warehouse than a production or live system directly?

(LO 5-2) How does the systems translator software work? How does it store the merged data into a data warehouse?

(LO 5-2) Is it possible for multinational firms to have many different financial reporting systems and enterprise systems packages all in use at the same time?

Showing 500 - 600

of 1576

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers