New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

fixed income analysis

Introduction To Fixed Income Analytics 2nd Edition Steven V. Mann, Frank J. Fabozzi - Solutions

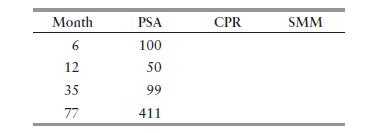

Using the PSA benchmark, complete the following table: Month PSA CPR SMM 6 100 12 50 35 99 77 411

What is the Prospectus Prepayment Curve?

a. Build an Excel spreadsheet that calculates the fraction of a 360-month pool that prepays each month of the pool’s life for any PSA speed. Make sure that you are getting good calculations by checking several months for PSAs of 0, 100, and 400.b. Calculate the scheduled amortization for the pool

Explain why you agree or disagree with the following statement: “By creating a CMO, an issuer eliminates the prepayment risk associated with the underlying mortgages.”

How does a collateralized mortgage obligation alter the cash flow from mortgages so as to shift prepayment risk across various classes of bondholders?

Explain how an accrual or Z bond works.

Describe how floating rate tranches can be created from fixed rate collateral.

In a CMO structure with PAC bonds, explain the role of the support bonds.

Explain why a senior-subordinated structure is a form of internal credit enhancement.

What is meant by a subprime mortgage-backed security?

What is meant by a shifting interest mechanism?

Describe the process of interest-only and principal-only strips are created?

Explain why individual loans that are of a nonamortizing type are not subject to prepayment risk?

What does it mean that the collateral for an asset-backed security consists of amortizing assets?

What is meant by an absolute prepayment speed?

a. What is static cash flow yield analysis?b. What are its shortcomings?

Why are prepayments path dependent?

What are the steps necessary in generating the scenario interest rate paths?

What is the relationship between the simulated one-month future interest rates and the simulated mortgage refinancing rates?

How is the present value of the cash flow for month T on interest rate path n determined?

In a Monte Carlo analysis, how is the theoretical or model price of a mortgage-backed security determined?

What is the relationship between the value of an MBS and the assumed volatility?

Does the valuation of an asset-backed security require the use of Monte Carlo simulation?

When is it appropriate to use the zero-volatility spread approach rather than the OAS approach when valuing an asset-backed security?

Explain why the minimum price of a convertible bond is greater of the conversion value and the straight value?

Consider the following convertible bond:Maturity = 10 years Coupon rate = 7%Conversion ratio = 50 Maturity value = 1,000 Moreover, the following information has been gathered about the bond and the common stock: Bond price = 950 Stock price = 17 Annual dividend per share = 1 Compute the

The valuation of convertible bonds is driven by what four fundamental factors?

Suppose that a bond issued by XXX Corporation is convertible into 30 shares of common stock. The delta of this bond is 0.77. Explain how to create a long position in the XXX convertible bond that is delta neutral.

What is the difference between a hard and soft call in a convertible bond issue?

What three elements do mandatory convertible bonds have in common?

Describe how a reverse convertible bond works.

What information can an analyst glean from breakeven yield advantage?

In March 2010, Bakrieland Development, an Indonesian property developer, issued $150 million in convertible bonds. The bonds had a 5-year maturity that granted the bondholder to put the bond back to the issuer on the third anniversary at par. The bonds were also callable by the issuer after three

Suppose an investor can purchase a 5-year, 9% coupon bond that pays interest semiannually and the price of this bond is $108.32. The yield to maturity for this bond is 7% on a bond equivalent basis. Assume the investor can reinvest the coupon payments at 5% compounded semiannually.What is the total

Define horizon yield. Why is it unnecessary to make an assumption about horizon yield if the bond is held to maturity?

Why is the yield to maturity a special case of total return analysis?

Explain how scenario analysis works?

An investor is considering the purchase of an option-free corporate bond with a coupon rate of 6.625% and 20 years remaining to maturity.The bond’s price is 102.833 and the yield to maturity is 6.372%.Assume that the Treasury yield curve is flat at 4% and the credit spread for this issuer is 237

a. What do portfolio total return measures tell us that portfolio yield measures do not?b. Why is it important to conduct scenario analysis when assessing a portfolio’s potential performance?

Suppose that a portfolio manager is considering investing in a passthrough with 6.5% coupon rate, 290 months remaining to maturity, and an original mortgage balance of $1,000,000. The cash flow yield is 4.413%. The portfolio manager has a 6-month investment horizon and has the following beliefs:a.

What the advantages and disadvantages of the full valuation approach to assessing the interest rate risk exposure of a bond or a portfolio of bonds?

Which set of conditions will result in a bond whose price has greatest sensitivity to changes in interest rates? Explain your choice.a. A low coupon and a short maturity.b. A high coupon and a long maturity.c. A low coupon and a long maturity.d. A high coupon and a short maturity.

a. What does the duration of a bond measure?b. What does a bond’s convexity measure?c. Is convexity a superior measure to duration?

Consider an option-free Bond A with the following information (assume the bond’s coupon interest is paid semiannually):Coupon rate = 8%Yield to maturity on a bond equivalent basis = 8%Maturity in years = 2 Par value = $1,000 Market price = $1,000a. What is the price value of a basis point for

Suppose a bond has a modified duration of 4. By approximately how much will the bond’s value change if interest ratesa. increase by 50 basis pointsb. decrease by 150 basis pointsc. increase by 10 basis points

“Duration is only an accurate measure for very small changes in yield and assumes the yield shifts in parallel.” Critically evaluate this statement.

Consider a 6% coupon 20-year option-free bond selling at 89.32. If the yield is decreased by 20 basis points from 7.0% to 6.8%, the price would increase to 91.32. If the yield increases by 20 basis points, the price would decrease to 87.38. Given this information, answer the following questions.a.

Dean Corso, a portfolio manager at Ninth Gate Investments, is making a presentation to a group of investors. He states ”If two portfolios have the same modified duration, they have the same interest rate risk. Specifically, for a given change in yields, these two portfolios will respond in the

Consider a callable corporate bond with an 8% coupon currently trading at 102. You are asked by management to measure the interest rate risk exposure. How would you proceed?

What does it mean when a bond exhibits negative convexity?

On a graph, draw the price/yield relationship of a callable bond and an option-free bond. Explain why they differ. Now draw the price-yield relationship of a putable bond. Explain how it differs.

a. How is contribution to portfolio duration computed?b. How is the result interpreted?

Consider the following three bond portfolio:a. Compute the portfolio duration.b. Compute the contribution to portfolio duration of each bond.c. Suppose interest rates change by 50 basis points, what is the approximate percentage change in the portfolio’s value?d. What assumption does one making

What dimension of a floater’s price sensitivity do index duration and spread duration measure?

You are working as an analyst for a major dealer firm. You are having dinner with a fixed income portfolio manager. She remarks “The differences between the key rate durations of our portfolio and the benchmark tend to be positive on the short-end and negative in the long-end.” She asks you to

Consider a 4% coupon, 10-year Treasury note whose full price 103.3521 and is yielding 3.62%. The dollar value of a 1 basis point change in yield is 0.08421. What is the dollar duration for a 100 basis point change in yield?

What role does expected yield volatility play in making an assessment of interest rate risk?

What does VaR measure?

Suppose on February 14, 2008, we want to calculate the daily VaR for $1,000,000 face value position in U.S. Treasury principal strip that matures on February 15, 2036. The market value of the position is $274,715.27. The daily standard deviation of these daily returns over this period is estimated

Explain the difference between diversified and undiversified VaR.

What feature of the time series of returns is captured by using the exponential moving average?

What role does stress testing play in VaR analysis?

What is the purpose of mapping?

What are the advantages and disadvantages of the historical method of computing VaR?

The time horizon employed in a portfolio’s VaR is primarily by what portfolio objective?

What are the drawbacks of using VaR?

What is meant by the tails of a distribution?

What is the relationship between nominal interest rates, real interest rates, and expected inflation?

What is the breakeven inflation rate and what information does it convey?

Explain how TIPS are valued?

Explain why the coupon payment almost always accrues at a different rate every month?

a. What is meant by the nominal yield duration?b. What is meant by the real yield duration?

Why is the nominal yield duration generally not comparable to the real yield duration?

Suppose one estimates a linear regression with changes in the 5-year TIPS price as the dependent variable and changes in the 5-year nominal Treasury yield as the independent variable. The estimated slope is –4.What does this number tell us?

What are the five basic strategies that active portfolio managers utilize to add value relative to their benchmark?

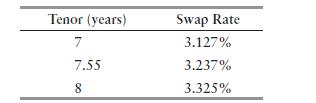

Consider a 5.25% coupon bond issued by General Electric that matures on December 6, 2017. The bond’s yield to maturity is 4.386%. Given the information below, compute the I-spread. The information is from May 14, 2010. Tenor (years) Swap Rate 7 3.127% 7.55 3.237% 8 3.325%

Describe the mechanics of an asset swap.

Explain the important differences between the par structure versus market structure using a diagram.

Explain how the asset swap spread is determined.

Explain how asset swap spreads are used as measures of relative value.

Describe in some detail how a credit default swap works. A diagram may prove useful.

Give some examples of a “credit event.”

If physical delivery of a credit default swap is required, what is meant by the “cheapest to deliver obligation.”

a. What is the linkage among asset swap spreads, CDS spreads, and credit spreads?b. What is the credit default swap basis and how is it used as a measure of relative value?

Explain why an “at market” interest rate swap can be described as buying and selling LIBOR.

What is meant by notional principal?

Why is the price quote of an interest rate swap in the form of a swap spread?

Give two interpretations of an interest rate swap and explain why an interest rate swap can be interpreted in each way.

Suppose that interest rates increase subsequent to the inception of an interest rate swap.a. What is the effect on the value of the swap from the perspective of the fixed rate payer?b. What is the effect on the value of the swap from the perspective of the floating rate payer?

Explain why both sides of a swap contract are exposed to counterparty risk?

“The swap rate is the fixed rate that will make the present value of the fixed rate payments equal the present value of the floating rate payments.”Do you agree or disagree with this statement.

What are the primary drivers of the level of swap spreads?

What role do Eurodollar futures play in the valuation of a swap contract?

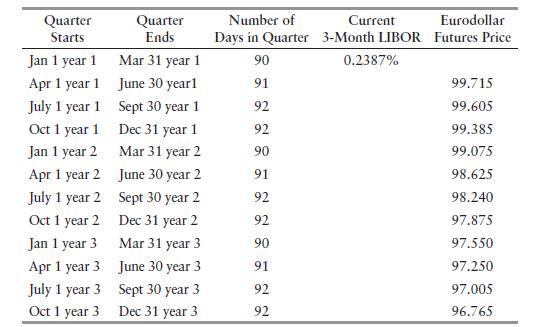

Using the information in the following table, construct an Excel spreadsheet to answer questions (a)–(d).Assume the frequency of both sides of the swap is quarterly and both use an actual/360 day count convention.a. What are projected future floating payments implied by the Eurodollar futures

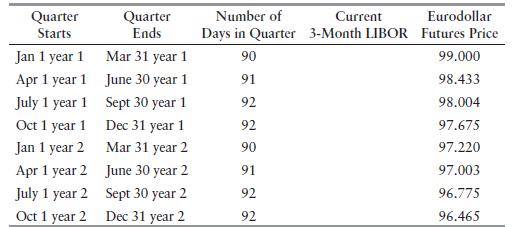

Using the information in the following table, construct an Excel spreadsheet to answer questions (a) and (b).Assume the frequency of both sides of the swap is quarterly and both use an actual/360 day count convention.a. What are the projected floating rate payments?b. What is the value of the swap?

a. What is implied volatility?b. What are the problems associated with using implied volatility as a measure of yield volatility?

Explain why you agree or disagree with the following statement: Two portfolio managers with the same set of daily yields will compute the same historical annual yield volatility.

In forecasting yield volatility, why would an analyst not want to weight each daily yield change equally?

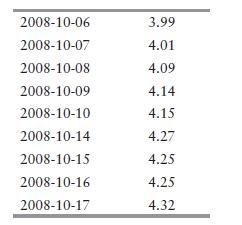

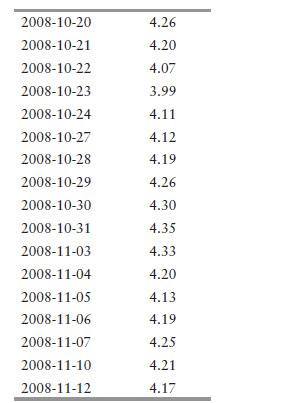

Using the data below, compute the daily standard deviation of the percentage change in yield using the daily yields for the 30-year Treasury CMT. 2008-10-06 3.99 2008-10-07 4.01 2008-10-08 4.09 2008-10-09 4.14 2008-10-10 4.15 2008-10-14 4.27 2008-10-15 4.25 2008-10-16 4.25 2008-10-17 4.32

For the daily yield volatility computed in Question 5, what is the annual yield volatility assuming the following number of trading days in the year: 250, 260 and 365.

Showing 1100 - 1200

of 2084

First

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

Last

Step by Step Answers