New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

fixed income analysis

Fixed Income Analysis 5th Edition Barbara S. Petitt - Solutions

The holding period for a bond at which the coupon reinvestment risk offsets the market price risk is best approximated by:A. Duration gap.B. Modified duration.C. Macaulay duration.

When the investor’s investment horizon is less than the Macaulay duration of the bond she owns:A. The investor is hedged against interest rate risk.B. Reinvestment risk dominates, and the investor is at risk of lower rates.C. Market price risk dominates, and the investor is at risk of higher

An investor purchases an annual coupon bond with a 6% coupon rate and exactly 20 years remaining until maturity at a price equal to par value. The investor’s investment horizon is eight years. The approximate modified duration of the bond is 11.470 years. The duration gap at the time of purchase

A manufacturing company receives a ratings upgrade and the price increases on its fixedrate bond. The price increase was most likely caused by a(n):A. Decrease in the bond’s credit spread.B. Increase in the bond’s liquidity spread.C. Increase of the bond’s underlying benchmark rate.

Empirical duration is likely the best measure of the impact of yield changes on portfolio value, especially under stressed market conditions, for a portfolio consisting of:A. 100% sovereign bonds of several AAA rated euro area issuers.B. 100% covered bonds of several AAA rated euro area corporate

Which of the following best defines credit risk?A. The probability of default times the severity of loss given defaultB. The loss of principal and interest payments in the event of bankruptcyC. The risk of not receiving full interest and principal payments on a timely basis

The Acme Company has senior unsecured bonds as well as both first and second lien debt in its capital structure. Which ranks higher with respect to priority of claims: senior unsecured bonds or second lien debt?

Under which circumstance is a subordinated bondholder most likely to recover some value in a bankruptcy without a senior creditor getting paid in full? When:A. Absolute priority rules are enforced.B. The various classes of claimants agree to it.C. The company is liquidated rather than reorganized.

Using the S&P rating scale, investment-grade bonds carry which of the following ratings?A. AAA to EEEB. BBB− to CCCC. AAA to BBB−

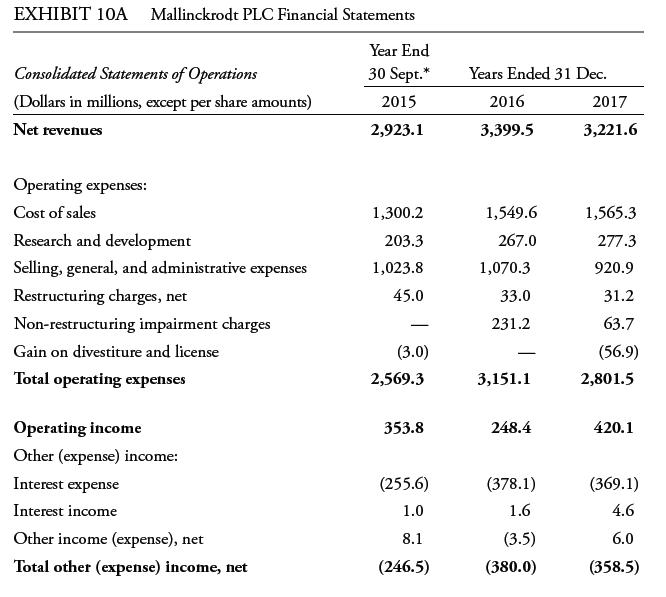

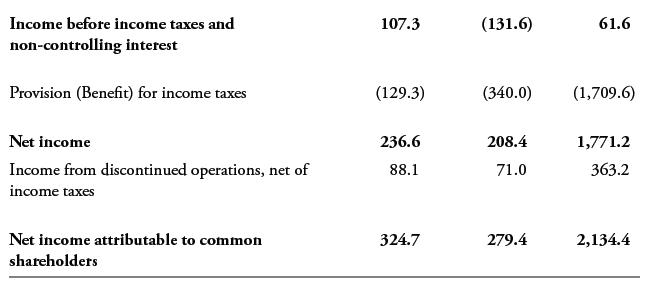

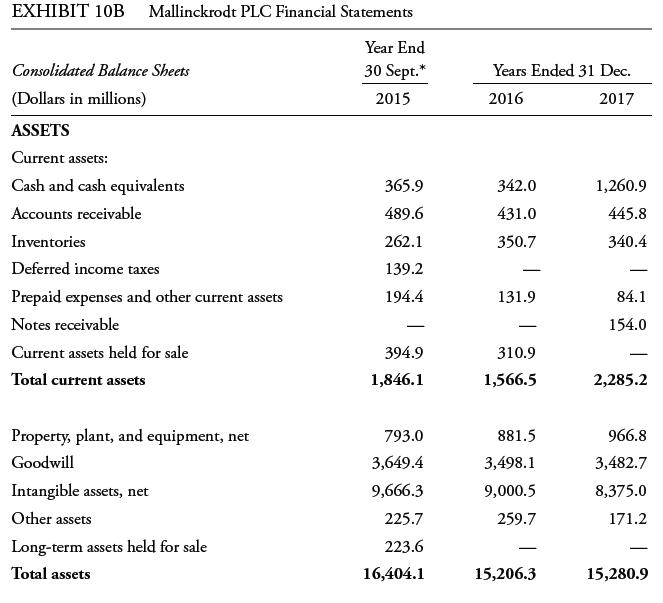

Mallinckrodt PLC (Mallinckrodt) is an Ireland-incorporated specialty pharmaceutical company. As a credit analyst, you have been asked to assess its creditworthiness—on its own, compared to a competitor in its overall industry, and compared with a similarly rated company in a different industry.

Given a hotel company, a chemical company, and a food retail company, which is most likely to be able to support a high debt load over an economic cycle?A. The hotel company, because people need a place to stay when they travel.B. The chemical company, because chemicals are a key input to many

Which of the following would not be a bond covenant?A. The issuer must file financial statements with the bond trustee on a timely basis.B. The company can buy back as much stock as it likes.C. If the company offers security to any creditors, it must offer security to this bond issue.

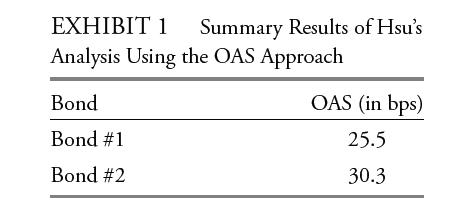

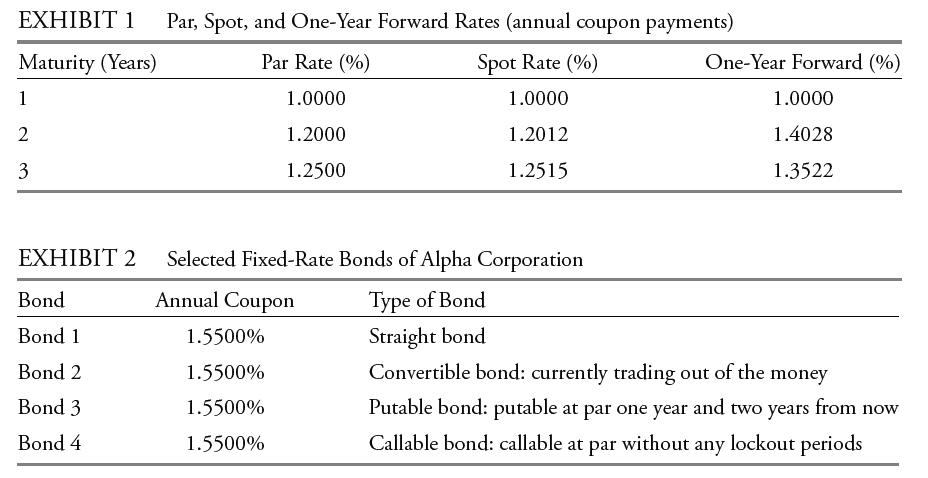

Based on Exhibit 1, Rayes would most likely conclude that relative to Bond #1, Bond #2 is:A. Overpriced.B. Fairly priced.C. Underpriced.Rayes Investment Advisers specializes in fixed-income portfolio management. Meg Rayes, the owner of the firm, would like to add bonds with embedded options to the

Based on Exhibits 1 and 2, the exchange that reflects the arbitrage-free price of the bond is:A. Eurex.B. Frankfurt.C. NYSE Euronext.Katrina Black, a portfolio manager at Coral Bond Management, Ltd., is conducting a training session with Alex Sun, a junior analyst in the fixed-income department.

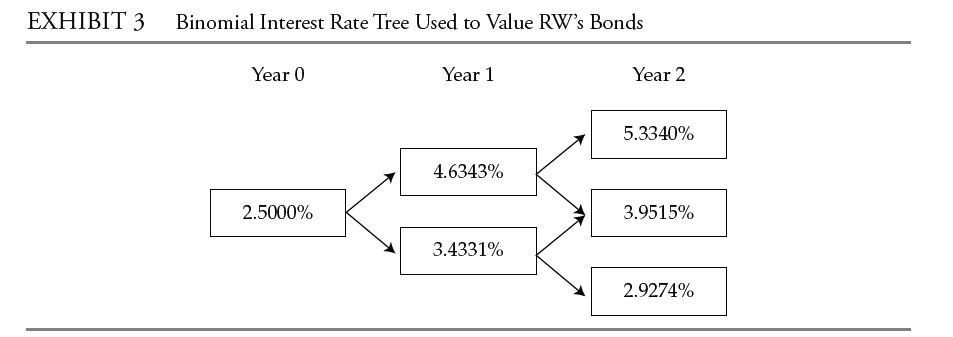

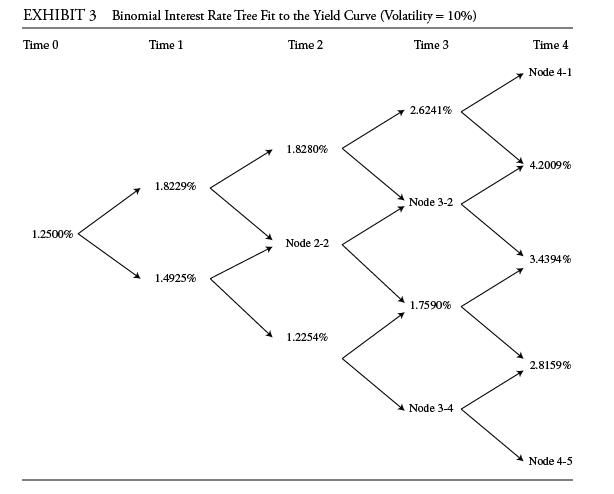

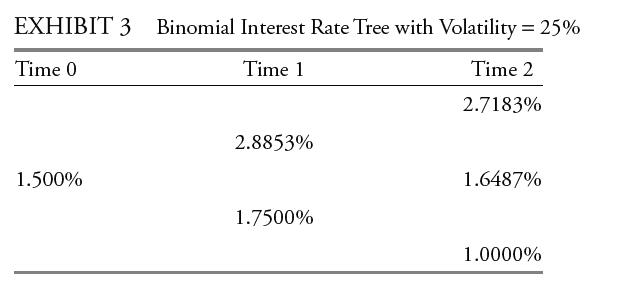

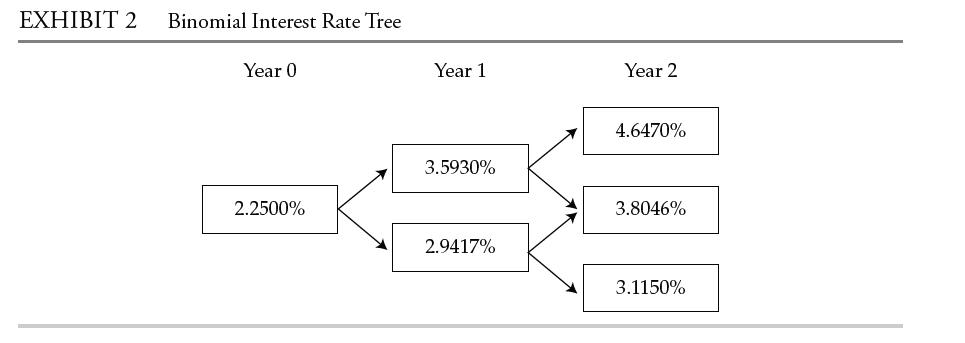

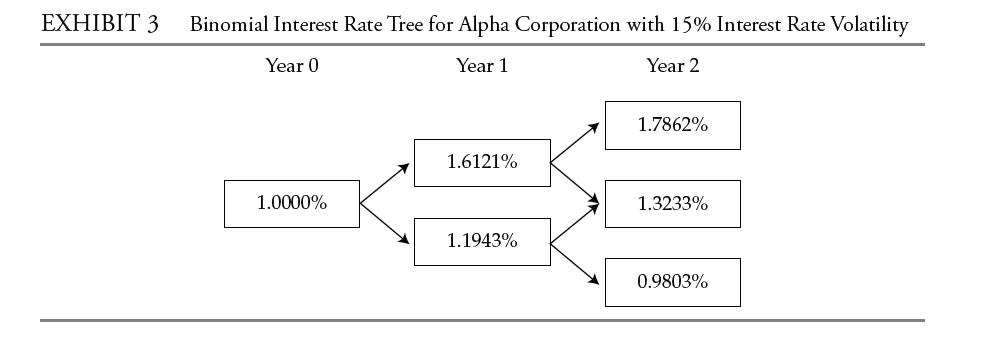

Recall from the chapter that each node is represented by both a time element and a rate change component. Which of the following statements about the missing data in Exhibit 3 is correct?A. Node 3–2 can be derived from Node 2–2.B. Node 4–1 should be equal to Node 4–5 multiplied by e0.4.C.

Based on the information in Exhibits 3 and 4, the bond price in euros at Node 1–2 in Exhibit 4 is closest to:A. 102.7917.B. 104.8640.C. 105.2917.Katrina Black, a portfolio manager at Coral Bond Management, Ltd., is conducting a training session with Alex Sun, a junior analyst in the fixed-income

A benefit of performing Task 1 is that it:A. Enables the model to price bonds with embedded options.B. Identifies benchmark bonds that have been mispriced by the market.C. Allows investors to realize arbitrage profits through stripping and reconstitution.Katrina Black, a portfolio manager at Coral

If the assumed volatility is changed as Black requested in Task 4, the forward rates shown in Exhibit 3 will most likely:A. Spread out.B. Remain unchanged.C. Converge to the spot rates.Katrina Black, a portfolio manager at Coral Bond Management, Ltd., is conducting a training session with Alex Sun,

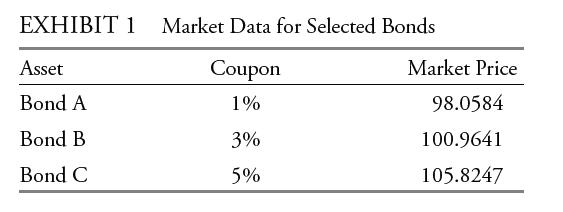

Based on Exhibit 1, which of the following bonds most likely includes an arbitrage opportunity?A. Bond AB. Bond BC. Bond CBetty Tatton is a fixed-income analyst with the hedge fund Sailboat Asset Management (SAM). SAM invests in a variety of global fixed-income strategies, including fixed-income

Based on Exhibits 2 and 3 and using Method 1, the amount (in absolute terms) by which the Hutto-Barkley Inc. corporate bond is mispriced is closest to:A. 0.3368 per 100 of par value.B. 0.4682 per 100 of par value.C. 0.5156 per 100 of par value.Betty Tatton is a fixed-income analyst with the hedge

Method 1 would most likely not be an appropriate valuation technique for the bond issued by:A. Hutto-Barkley Inc.B. Luna y Estrellas Intl.C. Peaton Scorpio Motors.Betty Tatton is a fixed-income analyst with the hedge fund Sailboat Asset Management (SAM). SAM invests in a variety of global

Based on Exhibit 4 and using Method 2, the correct price for Bond X is closest to:A. 97.2998.B. 109.0085.C. 115.0085.Betty Tatton is a fixed-income analyst with the hedge fund Sailboat Asset Management (SAM). SAM invests in a variety of global fixed-income strategies, including fixed-income

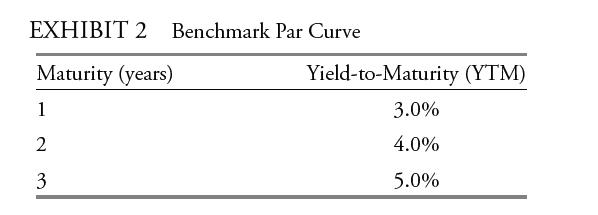

Based on Exhibit 1, Alvarez finds that an arbitrage opportunity is:A. Not available.B. Available based on the dominance principle.C. Available based on the value additivity principle.Meredith Alvarez is a junior fixed-income analyst with Canzim Asset Management. Her supervisor, Stephanie Hartson,

Based on the data in Exhibit 2, the most profitable arbitrage opportunity would be to buy the bond in:A. Mumbai and sell it in Hong Kong.B. Hong Kong and sell it in New York.C. New York and sell it in Hong Kong.Meredith Alvarez is a junior fixed-income analyst with Canzim Asset Management. Her

Based on Exhibits 3 and 4, the value of Bond C at the upper node at Time 1 is closest to:A. 97.1957.B. 99.6255.C. 102.1255.Meredith Alvarez is a junior fixed-income analyst with Canzim Asset Management. Her supervisor, Stephanie Hartson, asks AlvarezA to review the asset price and payoff data shown

Based on Exhibits 3 and 4, the price for Bond D is closest to:A. 97.4785.B. 103.3230.C. 106.3230.Meredith Alvarez is a junior fixed-income analyst with Canzim Asset Management. Her supervisor, Stephanie Hartson, asks AlvarezA to review the asset price and payoff data shown in Exhibit 1 to determine

Which of the various statements regarding binomial interest rate trees is correct?A. Statement 1B. Statement 2C. Statement 3Meredith Alvarez is a junior fixed-income analyst with Canzim Asset Management. Her supervisor, Stephanie Hartson, asks AlvarezA to review the asset price and payoff data

Based on Exhibits 5 and 6, the value of the lower one-period forward rate is closest to:A. 3.5122%.B. 3.5400%.C. 4.8037%.Meredith Alvarez is a junior fixed-income analyst with Canzim Asset Management. Her supervisor, Stephanie Hartson, asks AlvarezA to review the asset price and payoff data shown

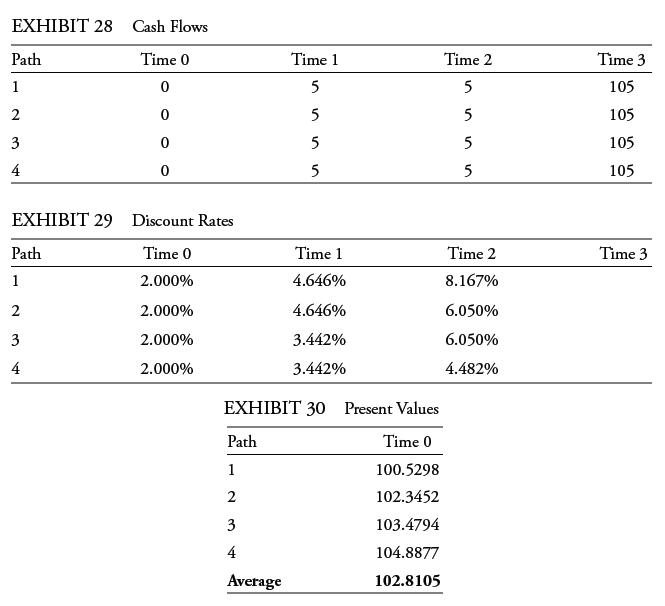

Based on Exhibits 4 and 7, the present value of Bond D’s cash flows following Path 2 i closest to:A. 97.0322.B. 102.8607.C. 105.8607.Meredith Alvarez is a junior fixed-income analyst with Canzim Asset Management. Her supervisor, Stephanie Hartson, asks AlvarezA to review the asset price and

Which of the statements regarding Monte Carlo simulation is correct?A. Only Statement 4 is correct.B. Only Statement 5 is correct.C. Both Statement 4 and Statement 5 are correct.Meredith Alvarez is a junior fixed-income analyst with Canzim Asset Management. Her supervisor, Stephanie Hartson, asks

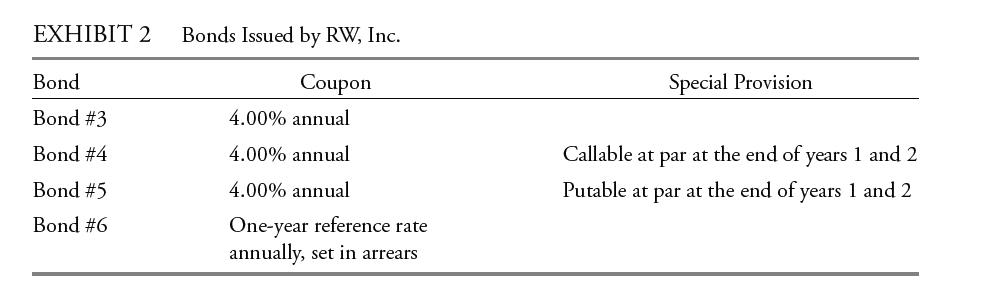

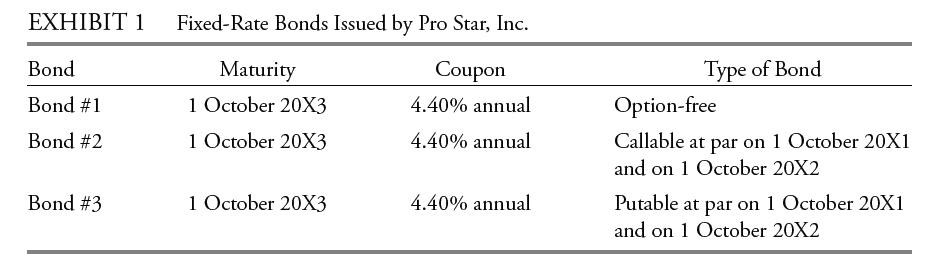

A fall in interest rates would most likely result in:A. A decrease in the effective duration of Bond #3.B. Bond #3 having more upside potential than Bond #2.C. A change in the effective convexity of Bond #3 from positive to negative.Samuel & Sons is a fixed-income specialty firm that offers

The value of Bond #3 is closest to:A. 102.103% of par.B. 103.688% of par.C. 103.744% of par.Samuel & Sons is a fixed-income specialty firm that offers advisory services to investment management companies. On 1 October 20X0, Steele Ferguson, a senior analyst at Samuel, is reviewing three fixed-rate

All else being equal, if Ferguson assumes an interest rate volatility of 15% instead of 10%, the bond that would most likely increase in value is:A. Bond #1.B. Bond #2.C. Bond #3.Samuel & Sons is a fixed-income specialty firm that offers advisory services to investment management companies. On 1

All else being equal, if the shape of the yield curve changes from upward sloping to flattening, the value of the option embedded in Bond #2 will most likely:A. Decrease.B. Remain unchanged.C. Increase.Samuel & Sons is a fixed-income specialty firm that offers advisory services to investment

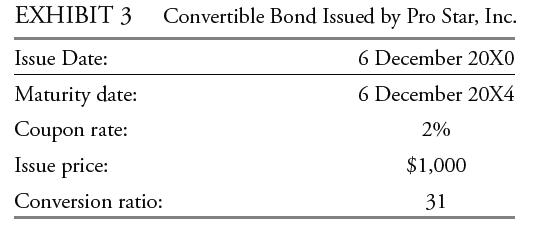

If the market price of Pro Star’s common stock falls from its level on 19 October 20X0, the price of the convertible bond will most likely:A. Fall at the same rate as Pro Star’s stock price.B. Fall but at a slightly lower rate than Pro Star’s stock price.C. Be unaffected until Pro Star’s

The effective duration of Bond #6 is:A. Close to 1.B. Higher than 1 but lower than 3.C. Higher than 3.Rayes Investment Advisers specializes in fixed-income portfolio management. Meg Rayes, the owner of the firm, would like to add bonds with embedded options to the firm’s bond portfolio. Rayes has

In Exhibit 2, the bond whose effective duration might lengthen if interest rates rise is:A. Bond #3.B. Bond #4.C. Bond #5.Rayes Investment Advisers specializes in fixed-income portfolio management. Meg Rayes, the owner of the firm, would like to add bonds with embedded options to the firm’s bond

The effective duration of Bond #4 is closest to:A. 0.76.B. 1.88.C. 3.77.Rayes Investment Advisers specializes in fixed-income portfolio management. Meg Rayes, the owner of the firm, would like to add bonds with embedded options to the firm’s bond portfolio. Rayes has asked Mingfang Hsu, one of

The value of Bond #7 is closest to:A. 99.697% of par.B. 99.936% of par.C. 101.153% of par.Rayes Investment Advisers specializes in fixed-income portfolio management. Meg Rayes, the owner of the firm, would like to add bonds with embedded options to the firm’s bond portfolio. Rayes has asked

The value of Bond #8 is closest to:A. 98.116% of par.B. 100.000% of par.C. 100.485% of par.Rayes Investment Advisers specializes in fixed-income portfolio management. Meg Rayes, the owner of the firm, would like to add bonds with embedded options to the firm’s bond portfolio. Rayes has asked

The value of Bond #9 is equal to the value of Bond #10:A. Plus the value of a put option on Whorton’s common stock.B. Plus the value of a call option on Whorton’s common stock.C. Minus the value of a call option on Whorton’s common stock.Rayes Investment Advisers specializes in fixed-income

The minimum value of Bond #9 is equal to the greater of:A. The conversion value of Bond #9 and the current value of Bond #10.B. The current value of Bond #10 and a call option on Whorton’s common stock.C. The conversion value of Bond #9 and a call option on Whorton’s common stock.Rayes

The factor that is currently least likely to affect the risk–return characteristics of Bond #9 is:A. Interest rate movements.B. Whorton’s credit spreads.C. Whorton’s common stock price movements.Rayes Investment Advisers specializes in fixed-income portfolio management. Meg Rayes, the owner

Based on Exhibit 1, the best action that an investor should take to profit from the arbitrage opportunity is to:A. Buy on Frankfurt, sell on Eurex.B. Buy on NYSE Euronext, sell on Eurex.C. buy on Frankfurt, sell on NYSE Euronext.Katrina Black, a portfolio manager at Coral Bond Management, Ltd., is

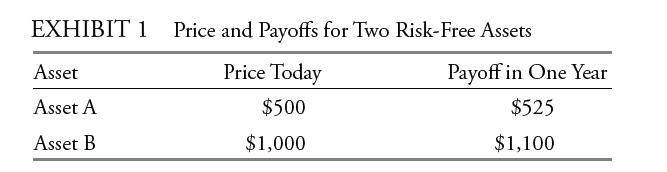

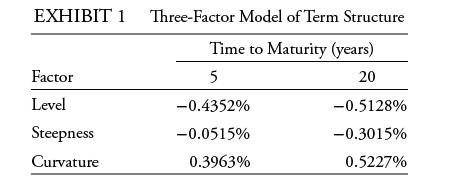

Based on Exhibit 1, the results of Analysis 1 should show the yield on the 20-year bond decreasing by:A. 0.3015%.B. 0.6030%.C. 0.8946%.Rowan Madison is a junior analyst at Cardinal Capital. Sage Winter, a senior portfolio manager and Madison’s supervisor, meets with Madison to discuss interest

The risk that a bond’s creditworthiness declines is best described by:A. Credit migration risk.B. Market liquidity risk.C. Spread widening risk.

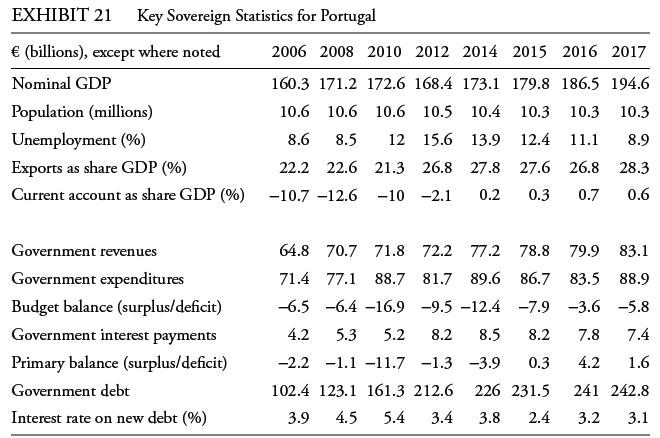

Exhibit 21 shows several key sovereign statistics for Portugal.1. Calculate the government debt/GDP ratio for Portugal for the years 2014−2017 as well as for the years 2006, 2008, 2010, and 2012.2. Calculate GDP/capita for the same periods. EXHIBIT 21 Key Sovereign Statistics for Portugal €

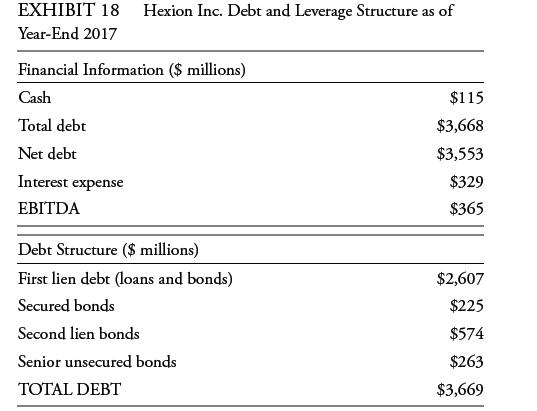

Hexion Inc. is a specialty chemical company. It has a complicated, high-yield debt structure, consisting of first lien debt (loans and bonds), secured bonds, second lien bonds, and senior unsecured debt, due to a series of mergers as well as a leveraged buyout in 2005. Exhibit 18 is a simplified

Calculate the price impact on a 10-year corporate bond with a 4.75% coupon priced at 100, with an instantaneous 50 bps widening in spread due to the issuer’s announcement that it was adding substantial debt to finance an acquisition (which resulted in a twonotch downgrade by the rating agencies).

Which bonds are likely to exhibit the greatest spread volatility?A. Bonds from issuers rated AAB. Bonds from issuers rated BBC. Bonds from issuers rated A

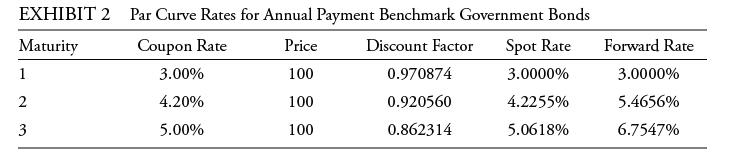

Using the par curve from Example 2, Example 4, and Example 5, the yield-to-maturity for a one-year annual coupon bond is 2%, for a two-year annual coupon bond is 3%, and for a three-year annual coupon bond is 4%. We know that if we generate the paths in the tree correctly and discount the cash

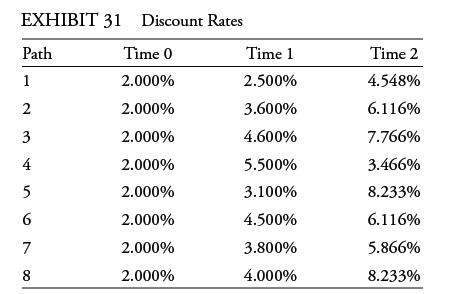

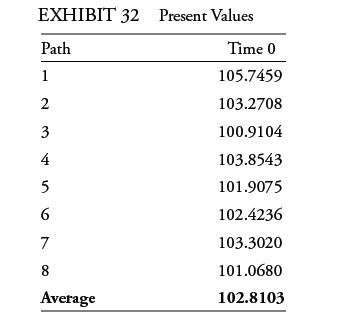

Replace the interest rate paths from Example 6 with randomly generated paths calibrated to the same initial par and spot curves, as shown in Exhibit 31. EXHIBIT 31 Discount Rates Time 0 2.000% 2.000% 2.000% 2.000% 2.000% 2.000% 2.000% 2.000% Path 1 2 3 4 5 6 7 8 Time

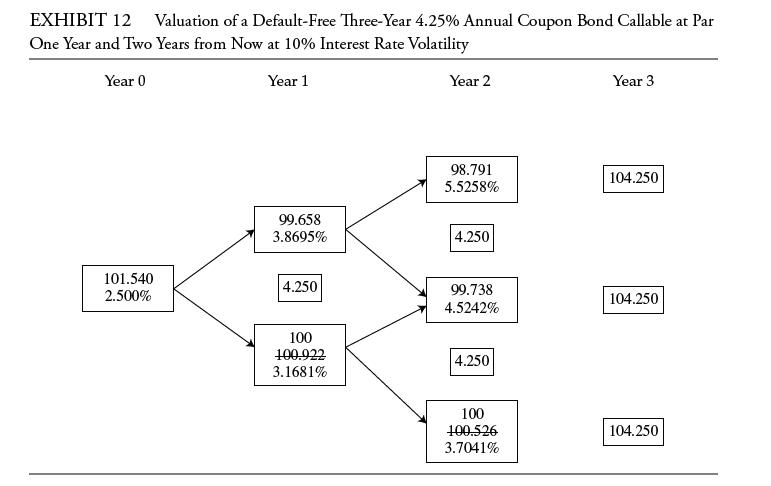

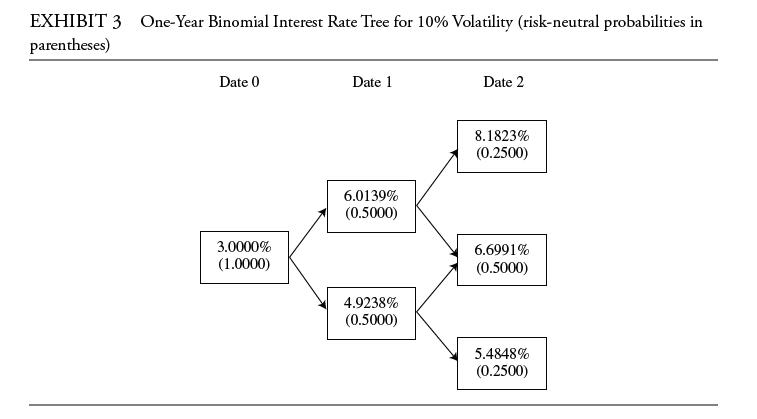

Return to the valuation of the Bermudan-style three-year 4.25% annual coupon bond callable at par one year and two years from now as depicted in Exhibit 12. The one-year, two-year, and three-year par yields are 2.500%, 3.000%, and 3.500%, respectively, and the interest rate volatility is 10%.Assume

Based on Exhibit 2, and assuming that the forecast for interest rates and Smith’s outlook for equity returns are validated, which bond’s option is most likely to be exercised?A. Bond 2B. Bond 3C. Bond 4John Smith, an investment adviser, meets with Lydia Carter to discuss her pending retirement

Based on Exhibit 2, the current price of Bond 1 is most likely greater than the current price of:A. Bond 2.B. Bond 3.C. Bond 4.John Smith, an investment adviser, meets with Lydia Carter to discuss her pending retirement and potential changes to her investment portfolio. Domestic economic activity

Assuming the forecast for interest rates is proven accurate, which bond in Exhibit 2 will likely experience the smallest price increase?A. Bond 1B. Bond 3C. Bond 4John Smith, an investment adviser, meets with Lydia Carter to discuss her pending retirement and potential changes to her investment

Based on the information in Exhibit 1 and Exhibit 2, the value of the embedded option in Bond 4 is closest to:A. Nil.B. 0.1906.C. 0.8789.John Smith, an investment adviser, meets with Lydia Carter to discuss her pending retirement and potential changes to her investment portfolio. Domestic economic

If Smith’s interest rate volatility forecast turns out to be true, which bond in Exhibit 2 is likely to experience the greatest price increase?A. Bond 2B. Bond 3C. Bond 4John Smith, an investment adviser, meets with Lydia Carter to discuss her pending retirement and potential changes to her

If the Brown and Company forecast comes true, which of the following is most likely to occur? The value of the embedded option in:A. Bond 3 decreases.B. Bond 4 decreases.C. both Bond 3 and Bond 4 increases.John Smith, an investment adviser, meets with Lydia Carter to discuss her pending retirement

Based on Exhibit 2 and Exhibit 3, the market price of Bond 4 is closest to:A. 100.0000.B. 100.5123.C. 100.8790.John Smith, an investment adviser, meets with Lydia Carter to discuss her pending retirement and potential changes to her investment portfolio. Domestic economic activity has been

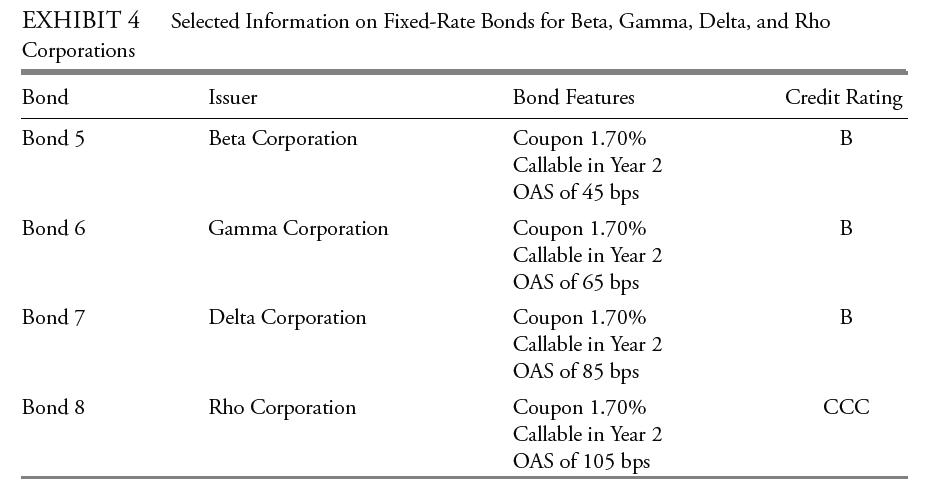

Which of the following conclusions regarding the bonds in Exhibit 4 is correct?A. Bond 5 is relatively cheaper than Bond 6.B. Bond 7 is relatively cheaper than Bond 6.C. Bond 8 is relatively cheaper than Bond 7.John Smith, an investment adviser, meets with Lydia Carter to discuss her pending

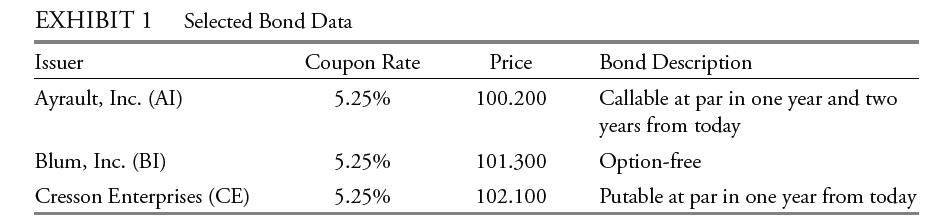

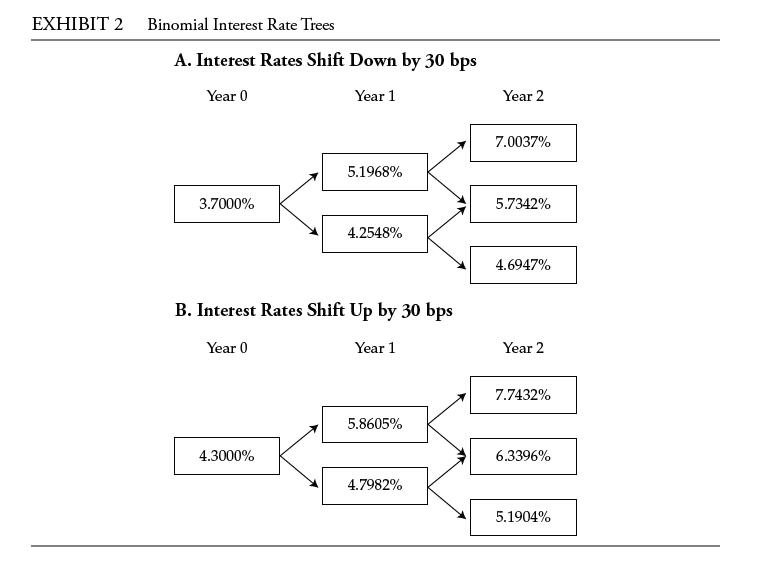

Based on Exhibits 1 and 2, the effective duration for the AI bond is closest to:A. 1.98.B. 2.15.C. 2.73.Jules Bianchi is a bond analyst for Maneval Investments, Inc. Bianchi gathers data on three corporate bonds, as shown in Exhibit 1.To assess the interest rate risk of the three bonds, Bianchi

If benchmark yields were to fall, which bond in Exhibit 1 would most likely experience a decline in effective duration?A. AI bondB. BI bondC. CE bondJules Bianchi is a bond analyst for Maneval Investments, Inc. Bianchi gathers data on three corporate bonds, as shown in Exhibit 1.To assess the

Based on Exhibit 1, for the BI bond, one-sided:A. Up-duration will be greater than one-sided down-duration.B. Down-duration will be greater than one-sided up-duration.C. Up-duration and one-sided down-duration will be about equal.Jules Bianchi is a bond analyst for Maneval Investments, Inc. Bianchi

Based on Exhibit 1, which key rate duration is the largest for the BI bond?A. One-year key rate durationB. Two-year key rate durationC. Three-year key rate durationJules Bianchi is a bond analyst for Maneval Investments, Inc. Bianchi gathers data on three corporate bonds, as shown in Exhibit 1.To

Which bond in Exhibit 1 most likely has the lowest effective convexity?A. AI bondB. BI bondC. CE bondJules Bianchi is a bond analyst for Maneval Investments, Inc. Bianchi gathers data on three corporate bonds, as shown in Exhibit 1.To assess the interest rate risk of the three bonds, Bianchi

On 1 January 20X2, Deem Advisors purchased a $10 million six-year senior unsecured bond issued by UNAB Corporation. Six months later (1 July 20X2), concerned about the portfolio’s credit exposure to UNAB, Doris Morrison, the chief investment officer at Deem Advisors, buys $10 million protection

Alfred Simonsson is assistant treasurer at a Swedish lumber company. The company has sold a large tract of land and now has sufficient cash holdings to retire some of its debt liabilities. The company’s accounting department assures Alfred that its external auditors will approve of a defeasement

Jules Bianchi is a bond analyst for Maneval Investments, Inc. Bianchi gathers data on three corporate bonds, as shown in Exhibit 1.To assess the interest rate risk of the three bonds, Bianchi constructs two binomial interest rate trees based on a 10% interest rate volatility assumption and a

Jules Bianchi is a bond analyst for Maneval Investments, Inc. Bianchi gathers data on three corporate bonds, as shown in Exhibit 1.To assess the interest rate risk of the three bonds, Bianchi constructs two binomial interest rate trees based on a 10% interest rate volatility assumption and a

Jules Bianchi is a bond analyst for Maneval Investments, Inc. Bianchi gathers data on three corporate bonds, as shown in Exhibit 1.To assess the interest rate risk of the three bonds, Bianchi constructs two binomial interest rate trees based on a 10% interest rate volatility assumption and a

Jules Bianchi is a bond analyst for Maneval Investments, Inc. Bianchi gathers data on three corporate bonds, as shown in Exhibit 1.To assess the interest rate risk of the three bonds, Bianchi constructs two binomial interest rate trees based on a 10% interest rate volatility assumption and a

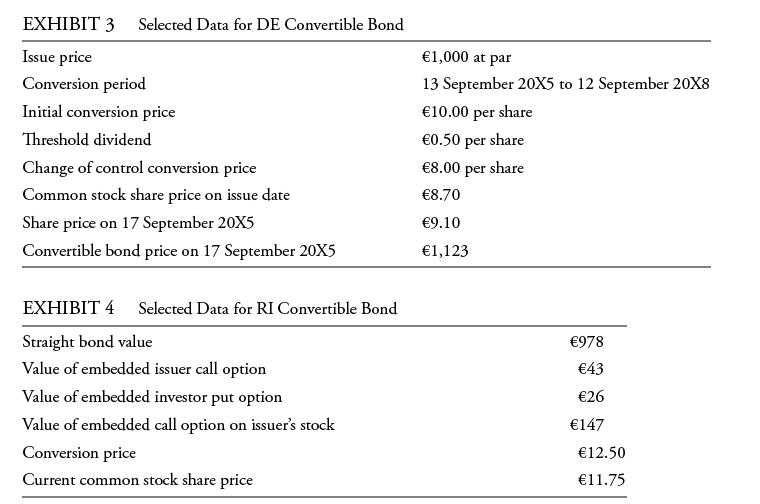

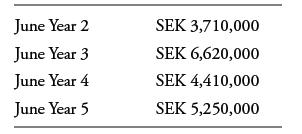

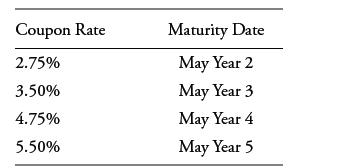

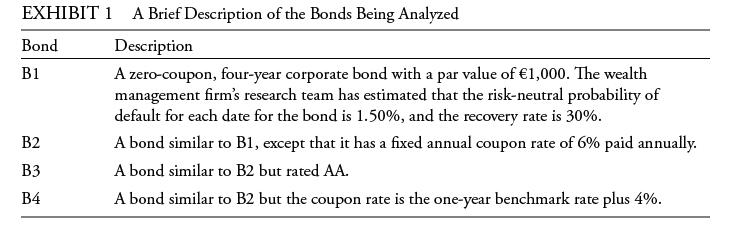

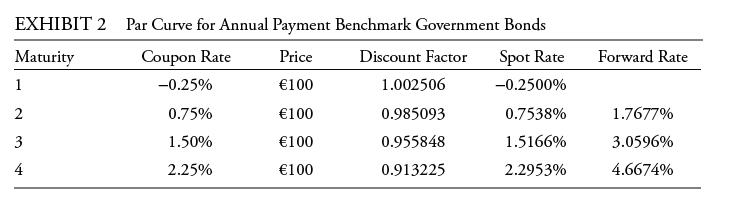

Daniela Ibarra is a senior analyst in the fixed-income department of a large wealth management firm. Marten Koning is a junior analyst in the same department, and David Lok is a member of the credit research team.The firm invests in a variety of bonds. Ibarra is presently analyzing a set of bonds

Daniela Ibarra is a senior analyst in the fixed-income department of a large wealth management firm. Marten Koning is a junior analyst in the same department, and David Lok is a member of the credit research team.The firm invests in a variety of bonds. Ibarra is presently analyzing a set of bonds

Daniela Ibarra is a senior analyst in the fixed-income department of a large wealth management firm. Marten Koning is a junior analyst in the same department, and David Lok is a member of the credit research team.The firm invests in a variety of bonds. Ibarra is presently analyzing a set of bonds

Daniela Ibarra is a senior analyst in the fixed-income department of a large wealth management firm. Marten Koning is a junior analyst in the same department, and David Lok is a member of the credit research team.The firm invests in a variety of bonds. Ibarra is presently analyzing a set of bonds

Daniela Ibarra is a senior analyst in the fixed-income department of a large wealth management firm. Marten Koning is a junior analyst in the same department, and David Lok is a member of the credit research team.The firm invests in a variety of bonds. Ibarra is presently analyzing a set of bonds

Daniela Ibarra is a senior analyst in the fixed-income department of a large wealth management firm. Marten Koning is a junior analyst in the same department, and David Lok is a member of the credit research team.The firm invests in a variety of bonds. Ibarra is presently analyzing a set of bonds

Daniela Ibarra is a senior analyst in the fixed-income department of a large wealth management firm. Marten Koning is a junior analyst in the same department, and David Lok is a member of the credit research team.The firm invests in a variety of bonds. Ibarra is presently analyzing a set of bonds

Daniela Ibarra is a senior analyst in the fixed-income department of a large wealth management firm. Marten Koning is a junior analyst in the same department, and David Lok is a member of the credit research team.The firm invests in a variety of bonds. Ibarra is presently analyzing a set of bonds

Daniela Ibarra is a senior analyst in the fixed-income department of a large wealth management firm. Marten Koning is a junior analyst in the same department, and David Lok is a member of the credit research team.The firm invests in a variety of bonds. Ibarra is presently analyzing a set of bonds

Daniela Ibarra is a senior analyst in the fixed-income department of a large wealth management firm. Marten Koning is a junior analyst in the same department, and David Lok is a member of the credit research team.The firm invests in a variety of bonds. Ibarra is presently analyzing a set of bonds

Daniela Ibarra is a senior analyst in the fixed-income department of a large wealth management firm. Marten Koning is a junior analyst in the same department, and David Lok is a member of the credit research team.The firm invests in a variety of bonds. Ibarra is presently analyzing a set of bonds

Daniela Ibarra is a senior analyst in the fixed-income department of a large wealth management firm. Marten Koning is a junior analyst in the same department, and David Lok is a member of the credit research team.The firm invests in a variety of bonds. Ibarra is presently analyzing a set of bonds

Daniela Ibarra is a senior analyst in the fixed-income department of a large wealth management firm. Marten Koning is a junior analyst in the same department, and David Lok is a member of the credit research team.The firm invests in a variety of bonds. Ibarra is presently analyzing a set of bonds

Daniela Ibarra is a senior analyst in the fixed-income department of a large wealth management firm. Marten Koning is a junior analyst in the same department, and David Lok is a member of the credit research team.The firm invests in a variety of bonds. Ibarra is presently analyzing a set of bonds

Daniela Ibarra is a senior analyst in the fixed-income department of a large wealth management firm. Marten Koning is a junior analyst in the same department, and David Lok is a member of the credit research team.The firm invests in a variety of bonds. Ibarra is presently analyzing a set of bonds

Anna Lebedeva is a fixed-income portfolio manager. Paulina Kowalski, a junior analyst, and Lebedeva meet to review several positions in Lebedeva’s portfolio.Lebedeva begins the meeting by discussing credit rating migration. Kowalski asks Lebedeva about the typical impact of credit rating

Anna Lebedeva is a fixed-income portfolio manager. Paulina Kowalski, a junior analyst, and Lebedeva meet to review several positions in Lebedeva’s portfolio.Lebedeva begins the meeting by discussing credit rating migration. Kowalski asks Lebedeva about the typical impact of credit rating

Anna Lebedeva is a fixed-income portfolio manager. Paulina Kowalski, a junior analyst, and Lebedeva meet to review several positions in Lebedeva’s portfolio.Lebedeva begins the meeting by discussing credit rating migration. Kowalski asks Lebedeva about the typical impact of credit rating

Anna Lebedeva is a fixed-income portfolio manager. Paulina Kowalski, a junior analyst, and Lebedeva meet to review several positions in Lebedeva’s portfolio.Lebedeva begins the meeting by discussing credit rating migration. Kowalski asks Lebedeva about the typical impact of credit rating

Anna Lebedeva is a fixed-income portfolio manager. Paulina Kowalski, a junior analyst, and Lebedeva meet to review several positions in Lebedeva’s portfolio.Lebedeva begins the meeting by discussing credit rating migration. Kowalski asks Lebedeva about the typical impact of credit rating

Anna Lebedeva is a fixed-income portfolio manager. Paulina Kowalski, a junior analyst, and Lebedeva meet to review several positions in Lebedeva’s portfolio.Lebedeva begins the meeting by discussing credit rating migration. Kowalski asks Lebedeva about the typical impact of credit rating

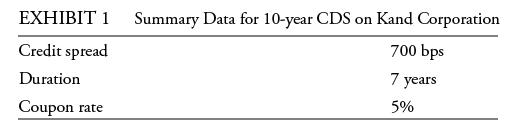

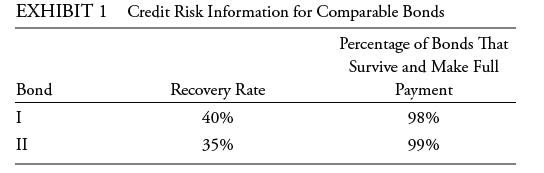

The expected exposure to default loss for Bond I is:A. Less than the expected exposure for Bond II.B. The same as the expected exposure for Bond II.C. Greater than the expected exposure for Bond II.Lena Liecken is a senior bond analyst at Taurus Investment Management. Kristel Kreming, a junior

Based on Exhibit 1, the loss given default for Bond II is:A. Less than that for Bond I.B. The same as that for Bond I.C. Greater than that for Bond I.Lena Liecken is a senior bond analyst at Taurus Investment Management. Kristel Kreming, a junior analyst, works for Liecken in helping conduct

Based on Exhibit 1, the expected future value of Bond I at maturity is closest to:A. 98.80.B. 103.74.C. 105.00.Lena Liecken is a senior bond analyst at Taurus Investment Management. Kristel Kreming, a junior analyst, works for Liecken in helping conduct fixed-income research for the firm’s

Based on Exhibit 1, the risk-neutral default probability for Bond I is closest to:A. 2.000%.B. 3.175%.C. 4.762%.Lena Liecken is a senior bond analyst at Taurus Investment Management. Kristel Kreming, a junior analyst, works for Liecken in helping conduct fixed-income research for the firm’s

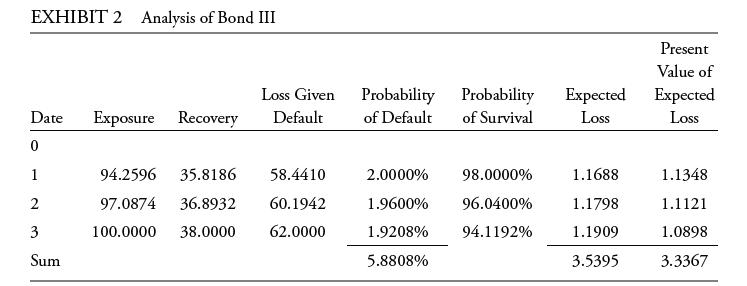

Based on Exhibit 2, the credit valuation adjustment for Bond III is closest to:A. 3.3367.B. 3.5395.C. 5.8808.Lena Liecken is a senior bond analyst at Taurus Investment Management. Kristel Kreming, a junior analyst, works for Liecken in helping conduct fixed-income research for the firm’s

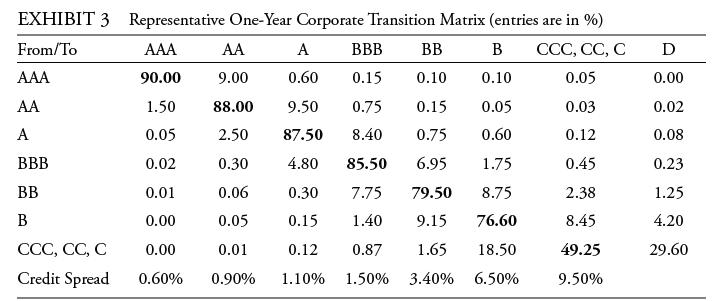

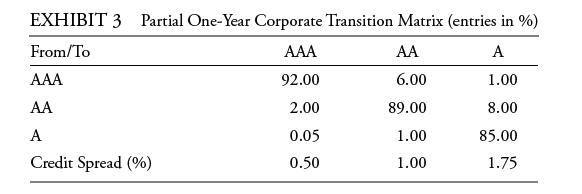

Based on Exhibit 3, if Bond IV’s credit rating changes during the next year to an A rating, its expected price change would be closest to:A. −8.00%.B. −7.35%.C. −3.15%.Lena Liecken is a senior bond analyst at Taurus Investment Management. Kristel Kreming, a junior analyst, works for Liecken

Kreming’s suggested model for Bond IV is a:A. Structural model.B. Reduced-form model.C. Term structure model.Lena Liecken is a senior bond analyst at Taurus Investment Management. Kristel Kreming, a junior analyst, works for Liecken in helping conduct fixed-income research for the firm’s

Showing 1300 - 1400

of 2084

First

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

Step by Step Answers