New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

fixed income analysis

Fixed Income Analysis 5th Edition Barbara S. Petitt - Solutions

The yield spread of a specific bond over the standard swap rate in that currency of the same tenor is best described as the:A. I-spread.B. Z-spread.C. G-spread.

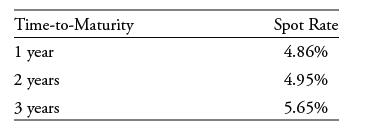

A corporate bond offers a 5% coupon rate and has exactly three years remaining to maturity. Interest is paid annually. The following rates are from the benchmark spot curve: Time-to-Maturity 1 year 2 years 3 years Spot Rate 4.86% 4.95% 5.65%

Agnelli Industries (Agnelli), a manufacturer of industrial machine tools based in Bergamo, Italy, has €500 million of corporate bonds outstanding. These bonds have a credit rating below investment grade. Agnelli has €400 million of receivables on its balance sheet that it would like to

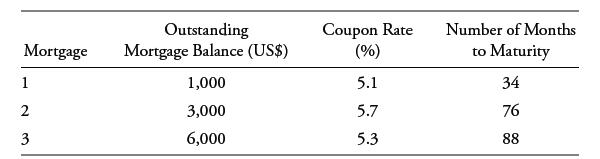

Assume that a pool includes three mortgages with the following characteristics: Outstanding Mortgage Mortgage Balance (US$) 1 2 3 1,000 3,000 6,000 Coupon Rate (%) 5.1 5.7 5.3 Number of Months to Maturity 34 76 88

Used Luxury Auto (ULA) is a hypothetical company that has established a nationwide business in buying used luxury autos and then refurbishing them with the latest in electronic equipment (for instance, UBS ports and rear-view cameras). ULA Corp then sells these autos in the retail market, often

Return to the ULA securitization described in Example 1. Based on the information provided, the form of credit enhancement that the transaction most likely includes is:A. Time tranching.B. Credit tranching.C. A financial guarantee.

In an interest-only mortgage, the borrower:A. Does not have to repay the principal as long as she pays the interest.B. Does not have to make principal repayments for a certain number of years, after which she starts paying down the original loan amount.C. Does not have to make principal repayments

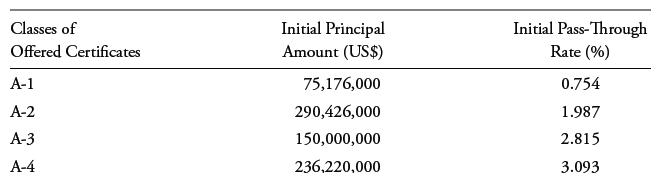

The following information is taken from a filing with the US Securities and Exchange Commission about a CMBS issued by a special purpose entity established by a major US commercial bank. The collateral for this CMBS was a pool of 72 fixed-rate mortgages secured by first liens (first claims) on

A non-conforming mortgage:A. Cannot be used as collateral in a mortgage-backed security.B. Does not satisfy the underwriting standards for inclusion as collateral for an agency residential mortgage-backed security.C. Does not give the lender a claim against the borrower for the shortfall between

A collateralized mortgage obligation:A. Eliminates prepayment risk.B. Is created from a pool of conforming loans.C. Redistributes various forms of prepayment risk among different bond classes.

Credit card receivable asset-backed securities differ from auto loan ABS in the following way:A. Credit card loans are recourse loans, whereas auto loans are non-recourse loans.B. The collateral for credit card receivable-backed securities is a pool of non-amortizing loans, whereas the collateral

An additional risk of an investment in an arbitrage collateralized debt obligation relative to an investment in an asset-backed security is:A. The default risk on the collateral assets.B. The risk that the CDO manager will fail to earn a return sufficient to pay off the investors in the senior and

Which of the following statements about covered bonds and asset-backed securities is most accurate?A. Both covered bonds and ABS pass prepayment and extension risk of the underlying asset pool through to investors.B. Both covered bonds and ABS offer investors recourse to both the bond’s issuer

Securitization is beneficial for banks because it:A. Repackages bank loans into simpler structures.B. Increases the funds available for banks to lend.C. Allows banks to maintain ownership of their securitized assets.

Agnelli Industries (Agnelli), a manufacturer of industrial machine tools based in Bergamo, Italy, has €500 million of corporate bonds outstanding. These bonds have a credit rating below investment grade. Agnelli has €400 million of receivables on its balance sheet that it would like to

Used Luxury Auto (ULA) is a hypothetical company that has established a nationwide business in buying used luxury autos and then refurbishing them with the latest in electronic equipment (for instance, UBS ports and rear-view cameras). ULA Corp then sells these autos in the retail market, often

A bank advertises a mortgage with the following interest rate: 2.99% (12-month Euribor + 2.50%), resetting once a year. The mortgage is most likely:A. A hybrid mortgage.B. An adjustable-rate mortgage.C. An initial period fixed-rate mortgage.

The following information is taken from a filing with the US Securities and Exchange Commission about a CMBS issued by a special purpose entity established by a major US commercial bank. The collateral for this CMBS was a pool of 72 fixed-rate mortgages secured by first liens (first claims) on

The monthly cash flows of a mortgage pass-through security most likely:A. Are constant.B. Change when interest rates decline.C. Are equal to the cash flows of the underlying pool of mortgages.

The variability in the average life of the PAC tranche of a CMO relative to the average life of the mortgage pass-through securities from which the CMO is created is:A. Lower.B. The same.C. Higher.

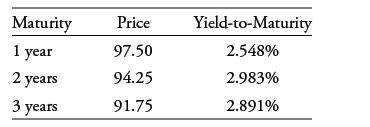

Suppose that an investor observes the following prices and yields-to-maturity on zerocoupon government bonds:The prices are per 100 of par value. The yields-to-maturity are stated on a semiannual bond basis.Compute the “1y1y” and “2y1y” implied forward rates, stated on a semiannual bond

A 6% annual coupon corporate bond with two years remaining to maturity is trading at a price of 100.125. The two-year, 4% annual payment government benchmark bond is trading at a price of 100.750. The one-year and two-year government spot rates are 2.10% and 3.635%, respectively, stated as

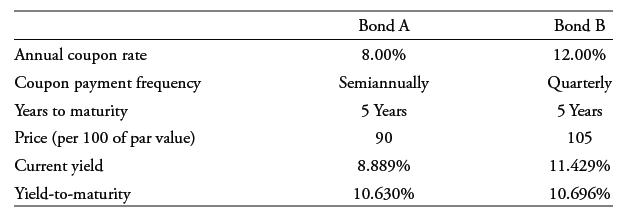

An analyst observes these reported statistics for two bonds.The analyst believes that Bond B has a little more risk than Bond A. How much additional compensation, in terms of a higher yield-to-maturity, does a buyer of Bond B receive for bearing this risk compared with Bond A? Annual coupon

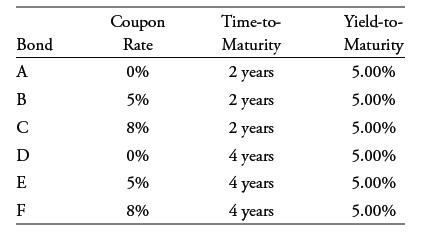

An investor is considering the following six annual coupon payment government bonds:Based on the relationships between the bond prices and bond characteristics, which bond will go down in price the least on a percentage basis if all yields go up from 5.00% to 5.10%?

Suppose that an investor observes the following prices and yields-to-maturity on zerocoupon government bonds:The prices are per 100 of par value. The yields-to-maturity are stated on a semiannual bond basis.The investor has a three-year investment horizon and is choosing between (1) buying the

A portfolio manager is considering the purchase of a bond with a 5.5% coupon rate that pays interest annually and matures in three years. If the required rate of return on the bond is 5%, the price of the bond per 100 of par value is closest to:A. 98.65.B. 101.36.C. 106.43.

Securitization benefits financial markets by:A. Increasing the role of intermediaries.B. Establishing a barrier between investors and originating borrowers.C. Allowing investors to tailor credit risk and interest rate risk exposures to meet their individual needs.

Agnelli Industries (Agnelli), a manufacturer of industrial machine tools based in Bergamo, Italy, has €500 million of corporate bonds outstanding. These bonds have a credit rating below investment grade. Agnelli has €400 million of receivables on its balance sheet that it would like to

Used Luxury Auto (ULA) is a hypothetical company that has established a nationwide business in buying used luxury autos and then refurbishing them with the latest in electronic equipment (for instance, UBS ports and rear-view cameras). ULA Corp then sells these autos in the retail market, often

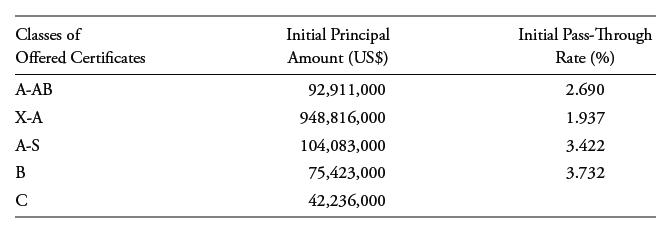

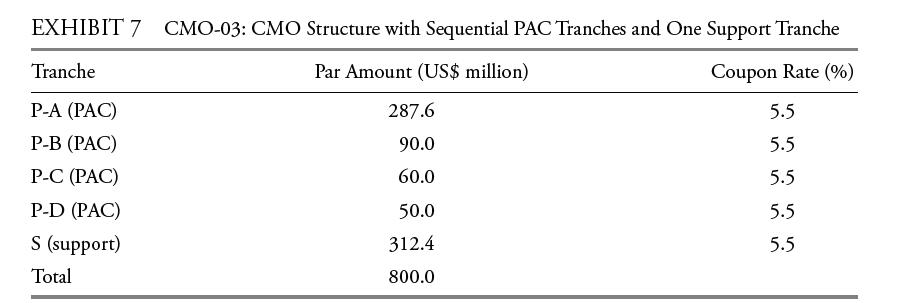

Referring to Exhibit 7, the tranche of CMO-03 that is most suitable for an investor concerned about contraction risk is:A. P-A (PAC).B. P-D (PAC).C. S (support). EXHIBIT 7 CMO-03: CMO Structure with Sequential PAC Tranches and One Support Tranche Tranche Par Amount (US$ million) Coupon Rate (%) P-A

If the borrower fails to make the contractual mortgage payments on a non-recourse mortgage, the lender:A. Cannot foreclose the property.B. Can recover the outstanding mortgage balance only through the sale of the property.C. Can recover the outstanding mortgage balance through the sale of the

A prepayment rate of 80 PSA means that investors can expect:A. 80% of the par value of the mortgage pass-through security to be repaid prior to the security’s maturity.B. 80% of the borrowers whose mortgages are included in the collateral backing the mortgage pass-through security to prepay their

The following information is taken from a filing with the US Securities and Exchange Commission about a CMBS issued by a special purpose entity established by a major US commercial bank. The collateral for this CMBS was a pool of 72 fixed-rate mortgages secured by first liens (first claims) on

The following information is from the prospectus supplement for US$877,670,000 of auto loan ABS issued by XYZ Credit Automobile Receivables Trust 2019:The collateral for this securitization is a pool of subprime automobile loan contracts secured for new and used automobiles and light-duty trucks

A benefit of securitization is the:A. Reduction in disintermediation.B. Simplification of debt obligations.C. Creation of tradable securities with greater liquidity than the original loans.

All else being equal, when interest rates decline:A. Investors in mortgage pass-through securities face extension risk.B. The weighted average maturity of a mortgage pass-through security lengthens.C. The increase in the price of a mortgage pass-through security is less than the increase in the

The tranche of a collateralized mortgage obligation that is most suitable for an investor who expects a fall in interest rates is:A. A fixed-rate tranche.B. An inverse floating-rate tranche.C. A PAC tranche.

The following information is taken from a filing with the US Securities and Exchange Commission about a CMBS issued by a special purpose entity established by a major US commercial bank. The collateral for this CMBS was a pool of 72 fixed-rate mortgages secured by first liens (first claims) on

Which of the following characteristics of a residential mortgage loan would best protect the lender from a strategic default by the borrower? A. RecourseB. A prepayment optionC. Interest-only payments

If a mortgage borrower makes prepayments without penalty to take advantage of falling interest rates, the lender will most likely experience:A. Extension risk.B. Contraction risk.C. Yield maintenance.

The last payment in a partially amortizing residential mortgage loan is best referred to as a:A. Waterfall.B. Principal repayment.C. Balloon payment.

A goal of securitization is to:A. Separate the seller’s collateral from its credit ratings.B. Uphold the absolute priority rule in bankruptcy reorganizations.C. Account for collateral’s primary influence on corporate bond credit spreads.

Which of the following statements related to securitization is correct?A. Time tranching addresses the uncertainty of a decline in interest rates.B. Securitizations are rarely structured to include both credit tranching and time tranching.C. Junior and senior bond classes differ in that junior

The creation of bond classes with a waterfall structure for sharing losses is referred to as:A. Time tranching.B. Credit tranching.C. Overcollateralization.

In a securitization, time tranching provides investors with the ability to choose between:A. Extension and contraction risks.B. Senior and subordinated bond classes.C. Fully amortizing and partially amortizing loans.

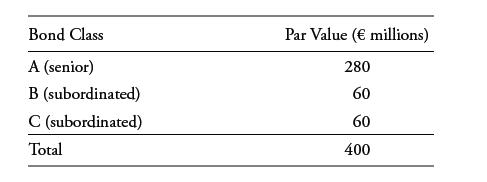

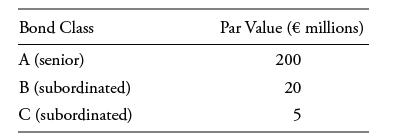

A special purpose entity issues asset-backed securities in the following structure.At which of the following amounts of default in par value would Bond Class A experience a loss?A. €20 millionB. €25 millionC. €26 million Bond Class A (senior) B (subordinated) C (subordinated) Par Value (€

In a securitization, the collateral is initially sold by the:A. Issuer.B. Depositor.C. Underwriter.

The following information is taken from a filing with the US Securities and Exchange Commission about a CMBS issued by a special purpose entity established by a major US commercial bank. The collateral for this CMBS was a pool of 72 fixed-rate mortgages secured by first liens (first claims) on

In a securitization, the special purpose entity (SPE) is responsible for the:A. Issuance of the asset-backed securities.B. Collection of payments from the borrowers.C. Recovery of underlying assets from delinquent borrowers.

The investment that is most suitable for an investor who is willing and able to accept significant prepayment risk is:A. A mortgage pass-through security.B. The support tranche of a collateralized mortgage obligation.C. The inverse floating-rate tranche of a collateralized mortgage obligation.

Securitization benefits investors by:A. Providing more direct access to a wider range of assets.B. Reducing the inherent credit risk of pools of loans and receivables.C. Eliminating cash flow timing risks of an ABS, such as contraction and extension risks.

William Marolf obtains a EUR5 million mortgage loan from Bank Nederlandse. A year later, the principal on the loan is EUR4 million and Marolf defaults on the loan. Bank Nederlandse forecloses, sells the property for EUR2.5 million, and is entitled to collect the EUR1.5 million shortfall from

Fran Martin obtains a non-recourse mortgage loan for $500,000. One year later, when the outstanding balance of the mortgage is $490,000, Martin cannot make his mortgage payments and defaults on the loan. The lender forecloses on the loan and sells the house for $315,000. What amount is the lender

A balloon payment equal to a mortgage’s original loan amount is a characteristic of a:A. Bullet mortgage.B. Fully amortizing mortgage.C. Partially amortizing mortgage.

Which of the following statements is correct concerning mortgage loan defaults?A. A non-recourse jurisdiction poses higher default risks for lenders.B. In a non-recourse jurisdiction, strategic default will not affect the defaulting borrower’s future access to credit.C. When a recourse loan

Which of the following describes a typical feature of a non-agency residential mortgagebacked security (RMBS)?A. Senior/subordinated structureB. A pool of conforming mortgages as collateralC. A guarantee by a government-sponsored enterprise

Which commercial mortgage-backed security characteristic causes a CMBS to trade more like a corporate bond than a residential mortgage-backed security?A. Call protectionB. Internal credit enhancementC. Debt-service-coverage ratio level

If interest rates increase, an investor who owns a mortgage pass-through security is most likely affected by:A. Credit risk.B. Extension risk.C. Contraction risk.

The longest-term tranche of a sequential-pay CMO is most likely to have the lowest:A. Average life.B. Extension risk.C. Contraction risk.

Which of the following is most likely an advantage of collateralized mortgage obligations (CMOs)? CMOs canA. Eliminate prepayment risk.B. Be created directly from a pool of mortgage loans.C. Meet the asset/liability requirements of institutional investors.

The tranches in a collateralized mortgage obligation that are most likely to provide protection for investors against both extension and contraction risk are:A. Planned amortization class (PAC) tranches.B. Support tranches.C. Sequential-pay tranches.

Support tranches are most appropriate for investors who are:A. Concerned about their exposure to extension risk.B. Concerned about their exposure to concentration risk.C. Willing to accept prepayment risk in exchange for higher returns.

In the context of mortgage-backed securities, a conditional prepayment rate (CPR) of 8% means that approximately 8% of the outstanding mortgage pool balance at the beginning of the year is expected to be prepaid:A. In the current month.B. By the end of the year.C. Over the life of the mortgages.

For a mortgage pass-through security, which of the following risks most likely increases as interest rates decline?A. BalloonB. ExtensionC. Contraction

Compared with the weighted average coupon rate of its underlying pool of mortgages, the pass-through rate on a mortgage pass-through security is:A. Lower.B. The same.C. Higher.

The single monthly mortality rate (SMM) most likely:A. Increases as extension risk rises.B. Decreases as contraction risk falls.C. Stays fixed over time when the standard prepayment model remains at 100 PSA.

Credit risk is an important consideration for commercial mortgage-backed securities (CMBS) if the CMBS are backed by mortgage loans that:A. Are non-recourse.B. Have call protection.C. Have prepayment penalty points.

A commercial mortgage-backed security does not meet the debt-to-service coverage at the loan level necessary to achieve a desired credit rating. Which of the following features would most likely improve the credit rating of the CMBS?A. SubordinationB. Call protectionC. Balloon payments

If a default occurs in a non-recourse commercial mortgage-backed security, the lender will most likely:A. Recover prepayment penalty points paid by the borrower to offset losses.B. Use only the proceeds received from the sale of the property to recover losses.C. Initiate a claim against the

Which of the following investments is least subject to prepayment risk?A. Auto loan receivable–backed securitiesB. Commercial mortgage-backed securitiesC. Non-agency residential mortgage-backed securities

An excess spread account incorporated into a securitization is designed to limit:A. Credit risk.B. Extension risk.C. Contraction risk.

Which of the following best describes the cash flow that owners of credit card receivable asset-backed securities receive during the lockout period?A. No cash flowB. Only principal payments collectedC. Only finance charges collected and fees

Which type of asset-backed security is not affected by prepayment risk?A. Auto loan ABSB. Residential MBSC. Credit card receivable ABS

In auto loan ABS, the form of credit enhancement that most likely serves as the first line of loss protection is the:A. Excess spread account.B. Sequential-pay structure.C. Proceeds from repossession sales

In credit card receivable ABS, principal cash flows can be altered only when the:A. Lockout period expires.B. Excess spread account is depleted.C. Early amortization provision is triggered.

The CDO tranche with a credit-rating status between senior and subordinated bond classes is called the:A. Equity tranche.B. Residual tranche.C. Mezzanine tranche.

The key to a CDO’s viability is the creation of a structure with a competitive return for the:A. Senior tranche.B. Mezzanine tranche.C. Subordinated tranche.

When the collateral manager fails pre-specified risk tests, a CDO is:A. Deleveraged by reducing the senior bond class.B. Restructured to reduce its most expensive funding source.C. Liquidated by paying off the bond classes in order of seniority.

Collateralized mortgage obligations are designed to:A. Eliminate contraction risk in support tranches.B. Distribute prepayment risk to various tranches.C. Eliminate extension risk in planned amortization tranches.

An example of a sovereign bond is a bond issued by:A. The World Bank.B. The city of New York.C. The federal German government.

The term most likely used to refer to the legal contract under which a bond is issued is:A. Indenture.B. Debenture.C. Letter of credit.

An example of a domestic bond is a bond issued by:A. LG Group from South Korea, denominated in British pounds, and sold in the United Kingdom.B. The UK Debt Management Office, denominated in British pounds, and sold in the United Kingdom.C. Wal-Mart from the United States, denominated in US

The coupon payment is most likely to be taxed as:A. Ordinary income.B. Short-term capital gain.C. Long-term capital gain.

The structure that requires the largest repayment of principal at maturity is that of a:A. Bullet bond.B. Fully amortized bond.C. Partially amortized bond.

Showing 2000 - 2100

of 2084

First

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

Step by Step Answers