New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

fixed income analysis

Fixed Income Analysis 5th Edition Barbara S. Petitt - Solutions

Which of the following statements best describes empirical duration?A. A common way to calculate a bond’s empirical duration is to run a regression of its price returns on changes in a benchmark interest rate.B. A bond’s empirical duration tends to be larger than its effective duration.C. The

An active manager is weighing an investment in the bonds of two issuers in the same industry with identical PODs using a structural credit model. Which of the following changes to the model inputs for one of the issuers would lead the analyst to expect an increase in the POD for that issuer?A. An

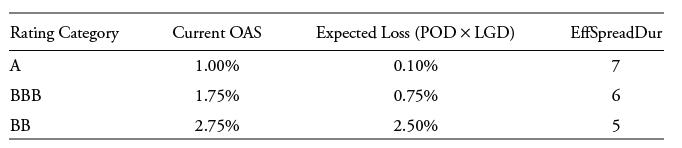

An investor has formed expectations across four bond rating categories and intends to overweight the category with the highest expected excess return over the next 12 months. Evaluate which rating group is the most attractive based on the information in the following table and assuming no change in

Consider the earlier case of an investor holding $50 million face value of a 15-year bond with a coupon of 2.75%, a current YTM of 3.528%, and a price of 91 per 100 of face value. What is the VaR for the full bond price at a 99% confidence interval for one month (assuming 21 trading days in the

An active fixed-income manager is considering increasing an overweight portfolio allocation to BBB rated health care issuers versus a targeted index. Which of the following VaR measures is the most appropriate to evaluate the impact of this decision on overall portfolio VaR?A. Incremental VaRB.

An investor seeks to purchase credit protection under a five-year CDS contract at a CDS market spread of 0.50% p.a. for an investment-grade issuer with an estimated effective spread duration (EffSpreadDurCDS) of 4.75.Determine whether the investor must pay or receive an upfront amount upon CDS

A European-based fixed-income manager intends to underweight exposure to a BBB rated French media and telecommunications issuer. She observes that the issuer’s current on-the-run five-year CDS contract is trading at a spread of 110 bps p.a. with an EffSpreadDurCDS of 4.595. Which position should

Consider the investor from the prior example who sought to underweight a French media and telecommunications issuer. Assume instead that the investor seeks to maintain a constant media and telecommunications credit allocation by overweighting a BBB rated German media and telecommunications

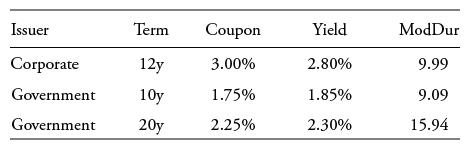

A portfolio manager considers the following annual coupon bonds:An increase in expected inflation causes the government yield curve to steepen, with a 20-point rise in the 10-year government bond YTM and no change in the 7-year government YTM. If the respective bank bond yield spread measures

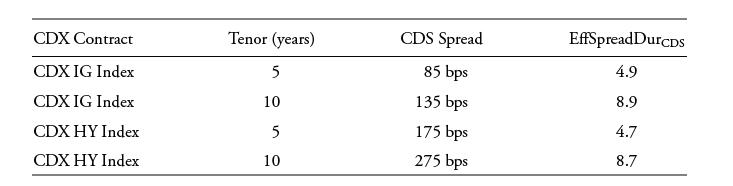

As in the prior example, an active fixed-income manager anticipates an economic slowdown in the next year with a greater adverse impact on lower-rated issuers. The manager chooses a tactical CDX (credit default swap index) strategy combining positions in investment-grade and high-yield CDX

An active manager is weighing the purchase of two callable bonds with similar credit risks and the same final maturity. Which of the two bonds is more likely to be called on the next call date?A. The bond with the lower ASWB. The bond with the lower Z-spreadC. The bond with the lower OAS

A London-based investor wants to estimate roll-down return attributable to a fixed-rate, option-free corporate bond versus UK gilts over the next six months assuming a static, upward-sloping government yield curve and a constant credit spread. The corporate bond has exactly 10 years remaining to

A corporate bond has an effective spread duration of five years and a credit spread of 2.75% (275 bps).What is the instantaneous (holding period of zero) excess return if the spread rises to 3.25%?

A junior analyst considers a 10-year high-yield bond issued by EKN Corporation (EKN) position in a high-yield portfolio. The bond has a price of 91.82, a modified duration of 8.47, and a spread duration of 8.47. The analyst speculates on the effects of an interest rate increase of 20 bps and,

A United Kingdom–based financial analyst considers a Z-score model in evaluating two publicly traded non-manufacturing companies as follows: Z-Score Model = 1.2 × A + 1.4 × B + 3.3 × C + 0.6 × D + 0.999 × E, whereA is Working Capital/Total AssetsB is Retained Earnings/Total AssetsC is

A portfolio manager considers two industrial bonds for a one-year investment:The manager observes a historical annual default probability of 0.27% for A2 rated issuers and 3.19% for B2 rated issuers and assumes a 40% recovery rate for both bonds.Which bond is more attractive if spreads are expected

An investor seeks to purchase credit protection under a five-year CDS contract at a CDS market spread of 0.50% p.a. for an investment-grade issuer with an estimated effective spread duration (EffSpreadDurCDS) of 4.75.Calculate the change in contract price if the CDS spread rises to 0.60% p.a. and

A corporate bond has an effective spread duration of five years and a credit spread of 2.75% (275 bps).Assume the bond has a 1% annualized expected POD and expected loss severity of 60% in the event of default. What is the expected excess return if the bond is held for six months and the credit

Which of the following outcomes is most likely if the junior analyst revises the bond’s original recovery rate higher?A. An increase in the bond’s PODB. A decrease in the bond’s PODC. A decrease in the bond’s credit spread

Which of the following observations on the risks of spread-based fixed-income portfolios is the most accurate?A. Because credit spreads equal the product of the LGD and the POD, distinguishing between the credit risk and liquidity risk components of yield spread across all market scenarios is

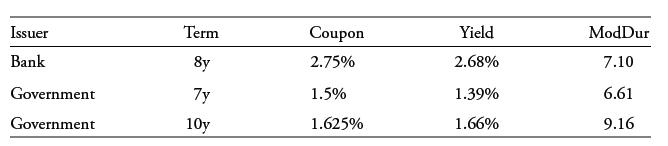

An active portfolio manager observes the following market information related to an outstanding corporate bond and two on-the-run government bonds that pay annual coupons:The portfolio manager also observes 10-year and 20-year swap spreads of 0.20% and 0.25%, respectively.Calculate the G-spread of

An active portfolio manager observes the following market information related to an outstanding corporate bond and two on-the-run government bonds that pay annual coupons:The portfolio manager also observes 10-year and 20-year swap spreads of 0.20% and 0.25%, respectively.Calculate the I-spread of

An active portfolio manager observes the following market information related to an outstanding corporate bond and two on-the-run government bonds that pay annual coupons:The portfolio manager also observes 10-year and 20-year swap spreads of 0.20% and 0.25%, respectively.Calculate the ASW of the

An active portfolio manager observes the following market information related to an outstanding corporate bond and two on-the-run government bonds that pay annual coupons:The portfolio manager also observes 10-year and 20-year swap spreads of 0.20% and 0.25%, respectively.Estimate the corporate

Which of the following statements about credit spread measures is most accurate?A. The DM is the yield spread over the MRR established upon issuance to compensate investors for assuming an issuer’s credit risk.B. The Z-DM will be above the DM if the MRR is expected to remain constant over time.C.

An active fixed-income manager is considering two corporate bond positions for an active portfolio. The first bond has a BBB rating with a credit spread of 2.75% and an effective spread duration of 6, and the second bond has a BB rating with a credit spread of 3.50% and an effective spread duration

An active fixed-income manager is considering two corporate bond positions for an active portfolio. The first bond has a BBB rating with a credit spread of 2.75% and an effective spread duration of 6, and the second bond has a BB rating with a credit spread of 3.50% and an effective spread duration

An active fixed-income manager is considering two corporate bond positions for an active portfolio. The first bond has a BBB rating with a credit spread of 2.75% and an effective spread duration of 6, and the second bond has a BB rating with a credit spread of 3.50% and an effective spread duration

An active manager is considering the senior bonds of one of several corporate issuers. Holding other factors constant, which of the following key financial ratio changes would lead the manager to expect a decrease in the POD for that issuer?A. An increase in the issuer’s coverage ratioB. An

Which of the following statements about statistical credit analysis models is most accurate?A. Structural credit models solve for the POD using observable company-specific variables such as financial ratios and macroeconomic variables.B. Reduced-form credit models use market-based variables to

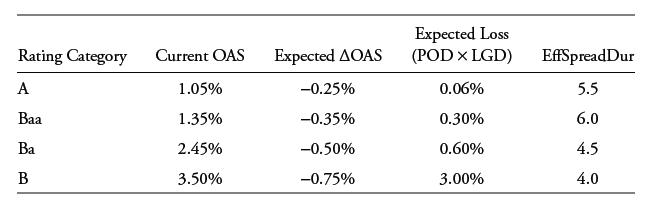

An investor is faced with an active portfolio decision across three bond rating categories based on the following current market information:Which bond rating category offers the highest expected excess return if credit spreads remain stable under current market conditions?A. A rated bond

An investor is faced with an active portfolio decision across three bond rating categories based on the following current market information:Which active bond portfolio maximizes expected excess return under a stable credit market assumption versus an equally weighted benchmark portfolio across the

An investor is faced with an active portfolio decision across three bond rating categories based on the following current market information:Which bond rating category offers the highest expected excess return if spreads instantaneously rise 10% across all ratings categories?A. A rated bond

Which of the following strategies best addresses the liquidity risk of a less frequently traded bond position in an active manager’s portfolio?A. Enter into a receive fixed, pay floating asset swap, unwinding the swap position once the illiquid bond position is sold.B. Sell single-name CDS

Which of the following statements best describes methods for assessing portfolio tail risk?A. Parametric methods use expected value and standard deviation of risk factors under a normal distribution and are well suited for option-based portfolios.B. Historical simulation methods use historical

Which of the following statements best describes how a single-name CDS contract is priced at inception?A. If the reference entity’s credit spread trades below the standard coupon rate, the CDS contract will be priced at a premium above par because the protection buyer pays a “below market”

Which of the following credit portfolio positioning strategies is the most appropriate to underweight the financial sector versus an index?A. Purchase protection on the CDX and sell protection on the CDX Financials subindex.B. Sell protection on the CDX and purchase protection on the CDX Financials

Which of the following phases of the credit cycle typically involves a decline in the number of issuer defaults?A. Late expansion phaseB. Early expansion phaseC. Peak phase

Which of the following regarding the shape of the credit spread curve for high yield issuers is most accurate?A. High-yield credit spread curves change shape more over the cycle than investment-grade ones do and usually invert during the peak phase.B. Investors should exercise caution in

Which of the following statements best describes a credit curve roll-down strategy?A. Returns from a credit curve roll-down strategy can be estimated by combining the incremental coupon from a longer maturity corporate bond with price appreciation due to the passage of time.B. A synthetic credit

An investor observes the following current CDS market information:Which of the following is the most appropriate credit portfolio positioning strategy to capitalize on an expected economic contraction?A. Buy protection on the 5-year CDX HY index and sell protection on the 5-year CDX IG index in

Which of the following is the most accurate statement related to international credit markets?A. Fixed exchange-rate regimes among emerging markets usually reduce the likelihood of financial distress because the domestic currency is tied to a major foreign currency.B. Although many emerging

Which of the following statements about the role of structured products in an active credit portfolio is most accurate?A. Covered bonds perform relatively well in a downturn versus other fixed-income bonds with real estate exposure because a covered bond investor also has recourse to the issuer.B.

An active fixed-income manager is evaluating the relative performance of an investment-grade corporate versus a high-yield corporate debt allocation in a fixed-income portfolio. Which of the following analytical model assumption changes is most likely to reduce the future value of the high-yield

The (flat) price on a fixed-rate corporate bond falls one day from 92.25 to 91.25 per 100 of par value because of poor earnings and an unexpected ratings downgrade of the issuer. The (annual) modified duration for the bond is 7.24. Which of the following is closest to the estimated change in the

AFC Investment Ltd. is a fixed-income investment firm that actively manages a government bond fund and a corporate bond fund. Holdings of the government bond fund are mainly medium-term US Treasury securities but also include debt of highly rated developed- market sovereign issuers. About half of

A “buy-and-hold” investor purchases a fixed-rate bond at a discount and holds the security until it matures. Which of the following sources of return is least likely to contribute to the investor’s total return over the investment horizon, assuming all payments are made as scheduled?A.

An investor plans to retire in 10 years. As part of the retirement portfolio, the investor buys a newly issued, 12-year, 8% annual coupon payment bond. The bond is purchased at par value, so its yield-to-maturity is 8.00% stated as an effective annual rate.Calculate the approximate Macaulay

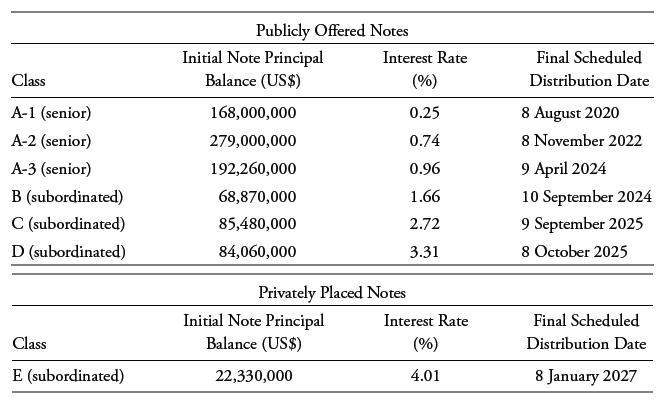

The following information is from the prospectus supplement for US$877,670,000 of auto loan ABS issued by XYZ Credit Automobile Receivables Trust 2019:The collateral for this securitization is a pool of subprime automobile loan contracts secured for new and used automobiles and light-duty trucks

Which statement about covered bonds is least accurate?A. Covered bonds provide investors with dual recourse, to the cover pool and also to the issuer.B. Covered bonds usually carry higher credit risks and offer higher yields than otherwise similar ABS.C. Covered bonds have a dynamic cover pool,

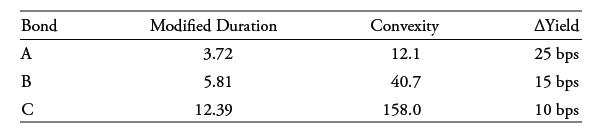

A fixed-income analyst is asked to rank three bonds in terms of interest rate risk. Interest rate risk here means the potential price decrease on a percentage basis given a sudden change in financial market conditions. The increases in the yields-to-maturity represent the “worst case” for the

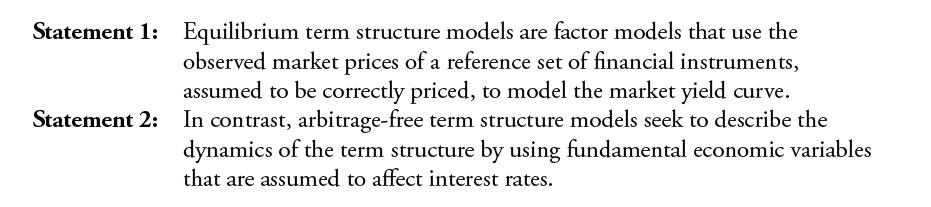

Keisha Jones is a junior analyst at Sparling Capital. Julie Anderson, a senior partner and Jones’s manager, meets with Jones to discuss interest rate models used for the firm’s fixed-income portfolio.Anderson begins the meeting by asking Jones to describe features of equilibrium and arbitrage-

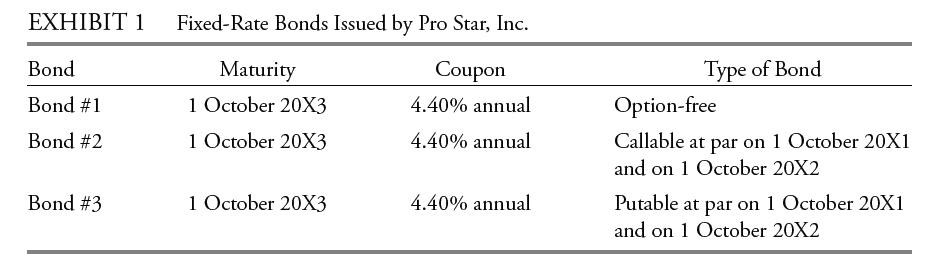

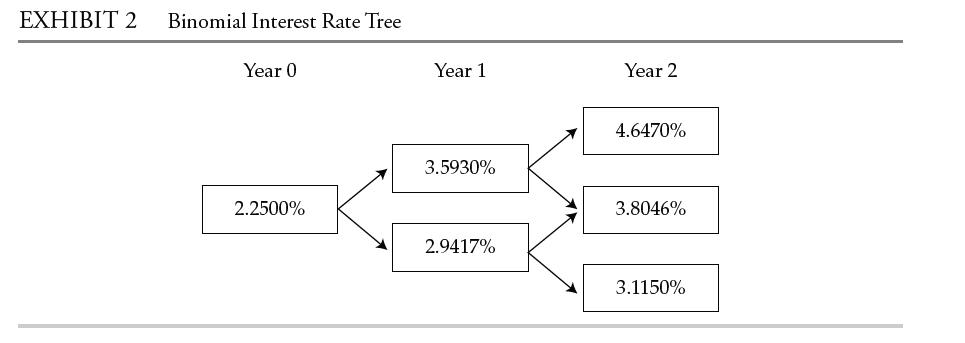

Samuel & Sons is a fixed-income specialty firm that offers advisory services to investment management companies. On 1 October 20X0, Steele Ferguson, a senior analyst at Samuel, is reviewing three fixed-rate bonds issued by a local firm, Pro Star, Inc. The three bonds, whose characteristics are

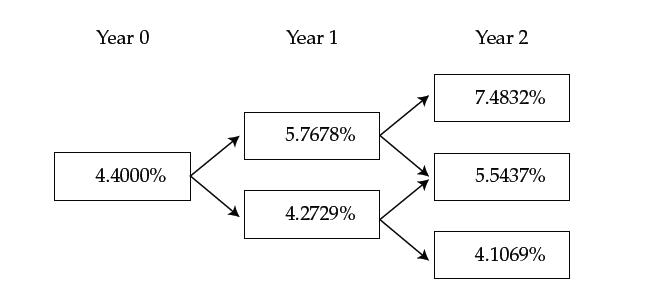

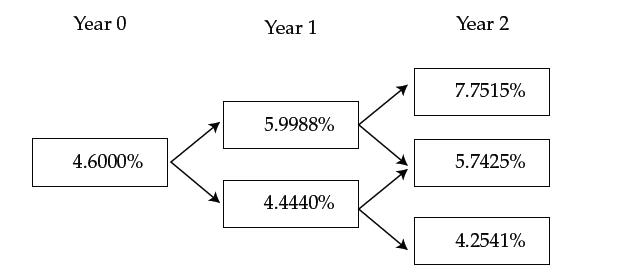

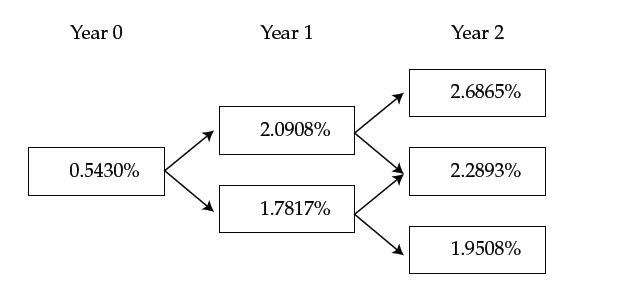

Sidley Brown, a fixed-income associate at KMR Capital, is analyzing the effect of interest rate volatility on the values of callable and putable bonds issued by Weather Analytics (WA). WA is owned by the sovereign government, so its bonds are considered default free. Brown is currently looking at

Robert Jourdan, a portfolio manager, has just valued a 7% annual coupon bond that was issued by a French company and has three years remaining until maturity. The bond is callable at par one year and two years from now. In his valuation, Jourdan used the yield curve based on the on-the-run French

Sidley Brown, a fixed-income associate at KMR Capital, is analyzing the effect of interest rate volatility on the values of callable and putable bonds issued by Weather Analytics (WA). WA is owned by the sovereign government, so its bonds are considered default free. Brown is currently looking at

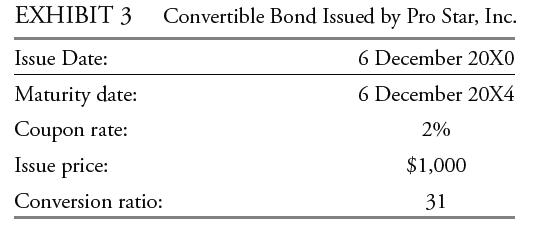

Nick Andrews, a fixed-income investment analyst, has been asked by his supervisor to prepare an analysis of the convertible bond issued by Heavy Element Inc., a chemical industry company, for presentation to the investment committee. Andrews has gathered the following data from the convertible

An issuer in the eurozone wants to sell a three-year floating-rate note at par \ with an annual coupon based on the 12-month Euribor + 300 bps. Because the 12 month Euribor is currently at a historic low and the issuer wants to protect itself against a sudden increase in interest cost, the

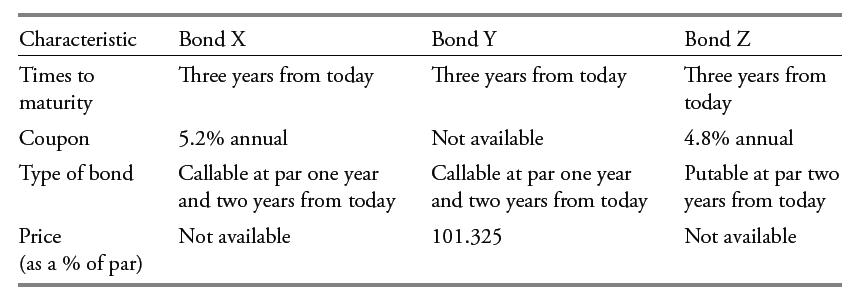

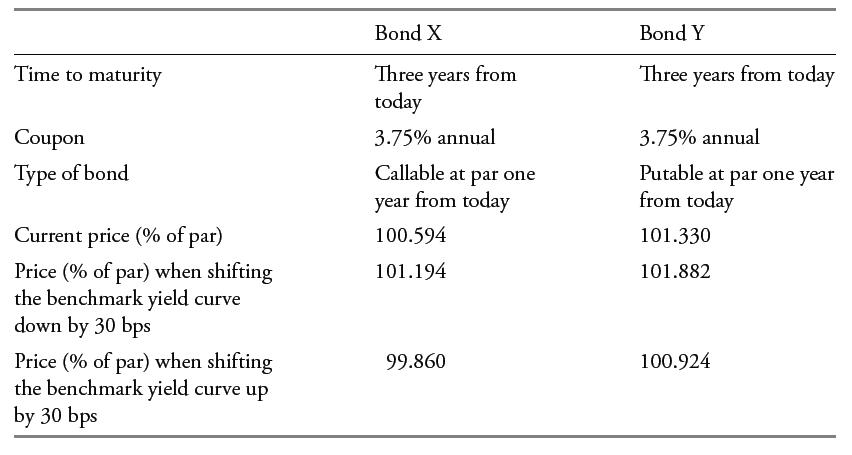

Erna Smith, a portfolio manager, has two fixed-rate bonds in her portfolio: a callable bond (Bond X) and a putable bond (Bond Y). She wants to examine the interest rate sensitivity of these two bonds to a parallel shift in the benchmark yield curve. Assuming an interest rate volatility of 10%, her

Samuel & Sons is a fixed-income specialty firm that offers advisory services to investment management companies. On 1 October 20X0, Steele Ferguson, a senior analyst at Samuel, is reviewing three fixed-rate bonds issued by a local firm, Pro Star, Inc. The three bonds, whose characteristics are

Nick Andrews, a fixed-income investment analyst, has been asked by his supervisor to prepare an analysis of the convertible bond issued by Heavy Element Inc., a chemical industry company, for presentation to the investment committee. Andrews has gathered the following data from the convertible

Brown is now analyzing the effect of interest rate volatility on the price of WA’s bonds.Relative to its price at 15% interest rate volatility, the price of Bond X at a lower interest rate volatility will be:A. Lower.B. The same.C. Higher.

Erna Smith, a portfolio manager, has two fixed-rate bonds in her portfolio: a callable bond (Bond X) and a putable bond (Bond Y). She wants to examine the interest rate sensitivity of these two bonds to a parallel shift in the benchmark yield curve. Assuming an interest rate volatility of 10%, her

Nick Andrews, a fixed-income investment analyst, has been asked by his supervisor to prepare an analysis of the convertible bond issued by Heavy Element Inc., a chemical industry company, for presentation to the investment committee. Andrews has gathered the following data from the convertible

Samuel & Sons is a fixed-income specialty firm that offers advisory services to investment management companies. On 1 October 20X0, Steele Ferguson, a senior analyst at Samuel, is reviewing three fixed-rate bonds issued by a local firm, Pro Star, Inc. The three bonds, whose characteristics are

Nick Andrews, a fixed-income investment analyst, has been asked by his supervisor to prepare an analysis of the convertible bond issued by Heavy Element Inc., a chemical industry company, for presentation to the investment committee. Andrews has gathered the following data from the convertible

Samuel & Sons is a fixed-income specialty firm that offers advisory services to investment management companies. On 1 October 20X0, Steele Ferguson, a senior analyst at Samuel, is reviewing three fixed-rate bonds issued by a local firm, Pro Star, Inc. The three bonds, whose characteristics are

Erna Smith, a portfolio manager, has two fixed-rate bonds in her portfolio: a callable bond (Bond X) and a putable bond (Bond Y). She wants to examine the interest rate sensitivity of these two bonds to a parallel shift in the benchmark yield curve. Assuming an interest rate volatility of 10%, her

Nick Andrews, a fixed-income investment analyst, has been asked by his supervisor to prepare an analysis of the convertible bond issued by Heavy Element Inc., a chemical industry company, for presentation to the investment committee. Andrews has gathered the following data from the convertible

Erna Smith, a portfolio manager, has two fixed-rate bonds in her portfolio: a callable bond (Bond X) and a putable bond (Bond Y). She wants to examine the interest rate sensitivity of these two bonds to a parallel shift in the benchmark yield curve. Assuming an interest rate volatility of 10%, her

Brown is now analyzing the effect of interest rate volatility on the price of WA’s bonds.Relative to its price at 15% interest rate volatility, the price of Bond Z at a higher interest rate volatility will be:A. Lower.B. The same.C. Higher.

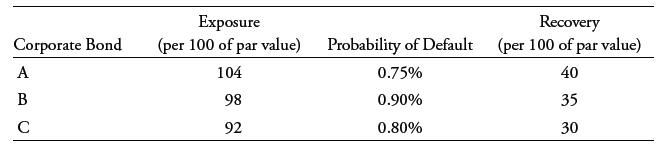

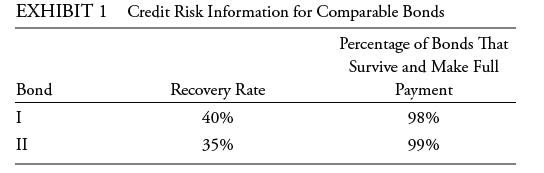

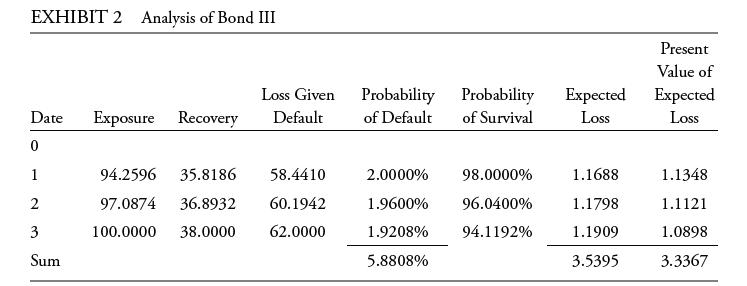

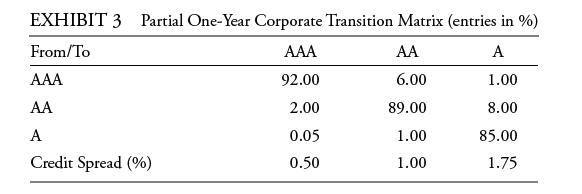

A fixed-income analyst is considering the credit risk over the next year for three corporate bonds currently held in her bond portfolio. Her assessment for the exposure, probability of default, and recovery is summarized in this table:Although all three bonds have very similar yields to maturity,

A fixed-income trader at a hedge fund observes a three-year, 5% annual payment corporate bond trading at 104 per 100 of par value. The research team at the hedge fund determines that the risk-neutral annual probability of default used to calculate the conditional POD for each date for the bond,

Edward Kapili is a summer intern working on a fixed-income trading desk at a major money-center bank. His supervisor asks him to value a three-year, 3% annual payment corporate bond using a binomial interest rate tree model for 20% volatility and the current par curve for benchmark government

Manuel Perello is a wealth manager for several Latin American families who seek to keep a portion of their assets in very high-quality corporate bonds. Mr. Perello explains that the yields to maturity on the bonds should be adjusted for possible credit spread widening to measure the expected rate

Tess Waresmith is a young finance professional who plans to eventually buy a two-family house, live in one unit, and rent the other to help cover the mortgage payments. She is a careful money manager and every year checks her FICO credit score. She is pleased to see that it has improved from 760

Carol Feely is a junior credit analyst at one of the major international credit rating agencies. She understands that in the standard structural models, equity is interpreted as a call option on the asset value of the company. However, she is not comfortable with the assumption that it is the

Lori Boller is a fixed-income money manager specializing in taking long positions on high-yield corporate bonds that she deems to be undervalued. In particular, she looks for bonds for which the credit spread over government securities appears to indicate too high a probability of default or too

Omar Yassin is an experienced credit analyst at a fixed-income investment firm. His current assignment is to assess potential purchases of distressed high-yield corporate bonds. One intriguing prospect is a three-year, annual payment floating-rate note paying the one-year benchmark rate plus 2.50%.

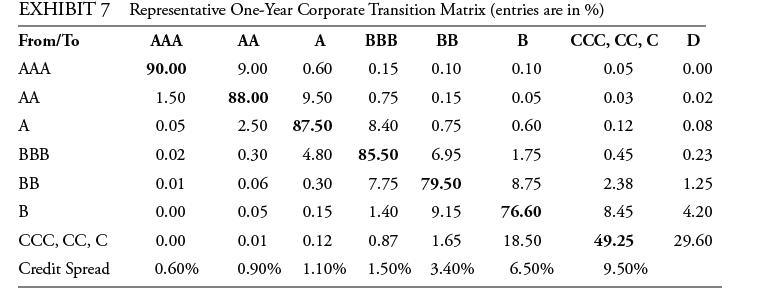

Which of Kreming’s observations regarding actual and risk-neutral default probabilities is correct?A. Only Observation 1B. Only Observation 2C. Both Observation 1 and Observation 2Lena Liecken is a senior bond analyst at Taurus Investment Management. Kristel Kreming, a junior analyst, works for

Assume that a company with several debt issues trading in the market files for bankruptcy (i.e., a credit event takes place). What is the cheapest-to-deliver obligation for a CDS contract where the reference bond is a five-year senior unsecured bond?A. A subordinated unsecured bond trading at 20%

A French company files for bankruptcy, triggering various CDS contracts. It has two series of senior bonds outstanding: Bond A trades at 30% of par, and Bond B trades at 40% of par. Investor X owns €10 million of Bond A and owns €10 million of CDS protection. Investor Y owns €10 million of

Assume that an investor sells $500 million of protection using the CDX IG index, which has 125 reference entities. Concerned about the creditworthiness of a few of the components, the investor hedges a portion of the credit risk in each. For Company A, he purchases $3 million of single-name CDS

Assume that a company’s hazard rate is a constant 8% per year, or 2% per quarter. An investor sells five-year CDS protection on the company with the premiums paid quarterly over the next five years.What is the probability of survival for the first quarter?

A company’s 5-year CDS trades at a credit spread of 300 bps, and its 10-year CDS trades at a credit spread of 500 bps.The company’s 5-year spread is unchanged, but the 10-year spread widens by 100 bps. Describe the implication of this change in the credit curve.

Assume a high-yield company’s 10-year credit spread is 600 bps and the duration of the CDS is 8 years. What is the approximate upfront premium required to buy 10-year CDS protection? Assume high-yield companies have 5% coupons on their CDS.

A French company files for bankruptcy, triggering various CDS contracts. It has two series of senior bonds outstanding: Bond A trades at 30% of par, and Bond B trades at 40% of par. Investor X owns €10 million of Bond A and owns €10 million of CDS protection. Investor Y owns €10 million of

Assume that an investor sells $500 million of protection using the CDX IG index, which has 125 reference entities. Concerned about the creditworthiness of a few of the components, the investor hedges a portion of the credit risk in each. For Company A, he purchases $3 million of single-name CDS

Assume that a company’s hazard rate is a constant 8% per year, or 2% per quarter. An investor sells five-year CDS protection on the company with the premiums paid quarterly over the next five years.What is the probability of survival through the second quarter?

The investment process followed by DFC’s previous fixed-income manager is best described as:A. Asset-driven liabilities.B. Liability-driven investing.C. Asset−liability management.SD&R Capital (SD&R), a global asset management company, specializes in fixed-income investments. Molly,

Relative to Approach 1 of gaining passive exposure, an advantage of Approach 2 is that it:A. Minimizes tracking error.B. Requires less risk analysis.C. Is more appropriate for socially responsible investors.SD&R Capital (SD&R), a global asset management company, specializes in fixed-income

The two-bond hypothetical portfolio’s immunization goal is to lock in a rate of return equal to:A. 9.55%.B. 9.85%.C. 10.25%.SD&R Capital (SD&R), a global asset management company, specializes in fixed-income investments. Molly, chief investment officer, is meeting with a prospective

Which of Molly’s statements about liability-driven investing is (are) correct?A. Statement 1 only.B. Statement 2 only.C. Both Statement 1 and Statement 2.SD&R Capital (SD&R), a global asset management company, specializes in fixed-income investments. Molly, chief investment officer, is

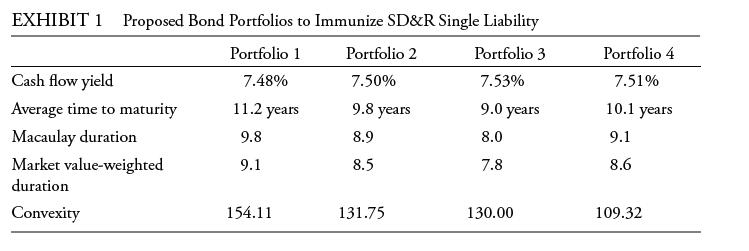

Based on Exhibit 1, which of the portfolios will best immunize SD&R’s single liability?A. Portfolio 1B. Portfolio 2C. Portfolio 3SD&R Capital (SD&R), a global asset management company, specializes in fixed-income investments. Molly, chief investment officer, is meeting with a

Which of the portfolios in Exhibit 1 best minimizes the structural risk to a single-liability immunization strategy?A. Portfolio 1B. Portfolio 3C. Portfolio 4SD&R Capital (SD&R), a global asset management company, specializes in fixed-income investments. Molly, chief investment officer, is

Which of the custom benchmark’s characteristics violates the requirements for an appropriate benchmark portfolio?A. Characteristic 1B. Characteristic 2C. Characteristic 3SD&R Capital (SD&R), a global asset management company, specializes in fixed-income investments. Molly, chief

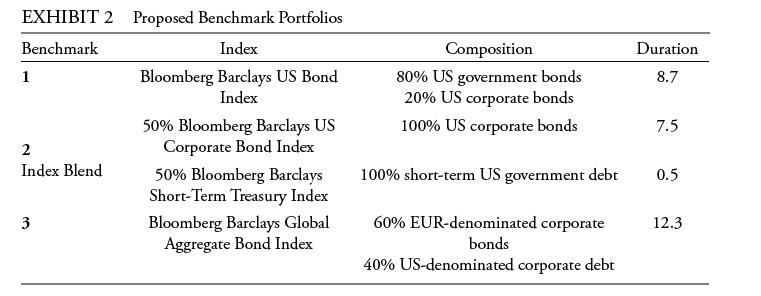

Based on DFC’s bond holdings and Exhibit 2, Molly should recommend:A. Benchmark 1.B. Benchmark 2.C. Benchmark 3.SD&R Capital (SD&R), a global asset management company, specializes in fixed-income investments. Molly, chief investment officer, is meeting with a prospective client, Leah of

A disadvantage of Strategy 1 is that:A. Price risk still exists.B. Interest rate volatility introduces risk to effective matching.C. There may not be enough bonds available to match all liabilities. Doug, the newly hired chief financial officer for the City of Radford, asks the deputy financial

A Radford School Board member has stated that she prefers a bond portfolio structure that provides diversification over time, as well as liquidity. In addressing the board member’s inquiry, Hui examines a bullet portfolio, a barbell portfolio, and a laddered portfolio.Which duration measure

A Radford School Board member has stated that she prefers a bond portfolio structure that provides diversification over time, as well as liquidity. In addressing the board member’s inquiry, Hui examines a bullet portfolio, a barbell portfolio, and a laddered portfolio.An upward shift in the yield

Showing 1500 - 1600

of 2084

First

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

Step by Step Answers