New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

fixed income analysis

Fixed Income Analysis 5th Edition Barbara S. Petitt - Solutions

If goodwill makes up a large percentage of a company’s total assets, this most likely indicates that:A. The company has low free cash flow before dividends.B. There is a low likelihood that the market price of the company’s common stock is below book value.C. A large percentage of the

In order to analyze the collateral of a company, a credit analyst should assess the:A. Cash flows of the company.B. Soundness of management’s strategy.C. Value of the company’s assets in relation to the level of debt.

In order to determine the capacity of a company, it would be most appropriate to analyze the:A. Company’s strategy.B. Growth prospects of the industry.C. Aggressiveness of the company’s accounting policies.

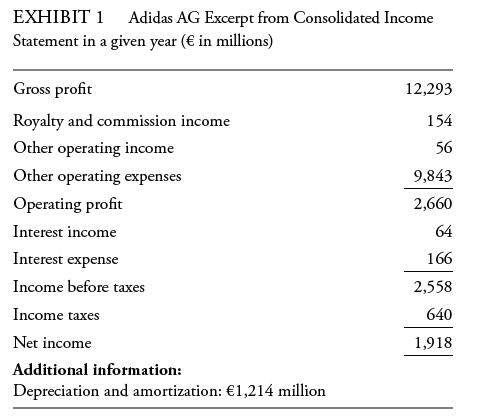

Based on the information provided in Exhibit 1, the EBITDA interest coverage ratio of Adidas AG is closest to:A. 16.02x.B. 23.34x.C. 37.98x. EXHIBIT 1 Adidas AG Excerpt from Consolidated Income Statement in a given year (€ in millions) Gross profit Royalty and commission income Other operating

A credit analyst is evaluating the credit worthiness of three companies: a construction company, a travel and tourism company, and a beverage company. Both the construction and travel and tourism companies are cyclical, whereas the beverage company is noncyclical. The construction company has the

The following information is from the annual report of Adidas AG for December 2019:• Depreciation and amortization: €1,214 million• Total assets: €20,640 million• Total debt: €4,364 million• Shareholders’ equity: €7,058 millionThe debt/capital of Adidas AG is closest to:A.

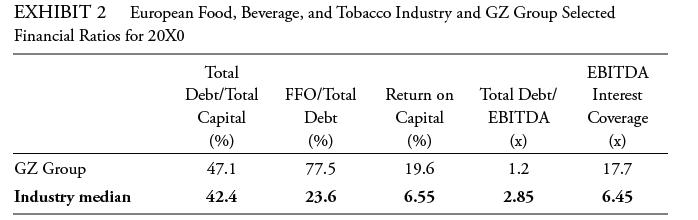

Based on the information in Exhibit 2, GZ Group’s (a hypothetical company) credit risk is most likely:A. Lower than the industry.B. Higher than the industry.C. The same as the industry. EXHIBIT 2 European Food, Beverage, and Tobacco Industry and GZ Group Selected Financial Ratios for 20X0 GZ

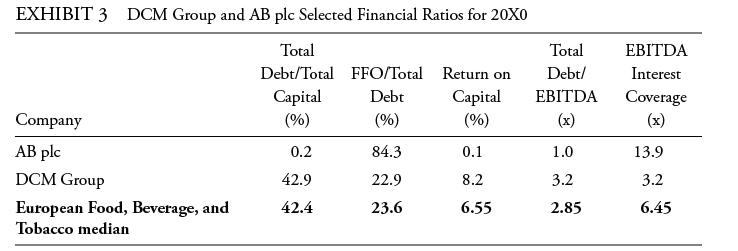

Based on the information in Exhibit 3, the credit rating of DCM Group (a hypothetical company in the European food & beverage sector) is most likely:A. Lower than AB plc.B. Higher than AB plc.C. The same as AB plc. EXHIBIT 3 DCM Group and AB plc Selected Financial Ratios for

Funds from operations (FFO) of Pay Handle Ltd (a fictitious company) increased in 20X1. In 20X1, the total debt of the company remained unchanged while additional common shares were issued. Pay Handle Ltd’s ability to service its debt in 20X1, as compared to 20X0, most likely:A. Improved.B.

Holding all other factors constant, the most likely effect of low demand and heavy new issue supply on bond yield spreads is that yield spreads will:A. Widen.B. Tighten.C. Not be affected.

Credit risk of a corporate bond is best described as the:A. Risk that an issuer’s creditworthiness deteriorates.B. Probability that the issuer fails to make full and timely payments.C. Risk of loss resulting from the issuer failing to make full and timely payments.

The risk that the price at which investors can actually transact differs from the quoted price in the market is called:A. Spread risk.B. Credit migration risk.C. Market liquidity risk.

Loss severity is best described as the:A. Default probability multiplied by the loss given default.B. Portion of a bond’s value recovered by bondholders in the event of default.C. Portion of a bond’s value, including unpaid interest, an investor loses in the event of default.

The two components of credit risk are default probability and:A. Spread risk.B. Loss severity.C. Market liquidity risk.

For a high-quality debt issuer with a large amount of publicly traded debt, bond investors tend to devote most effort to assessing the issuer’s:A. Default risk.B. Loss severity.C. Market liquidity risk.

The expected loss for a given debt instrument is estimated as the product of default probability and:A. (1 + Recovery rate).B. (1 − Recovery rate).C. 1/(1 + Recovery rate).

The priority of claims for senior subordinated debt is:A.Lower than for senior unsecured debt.B. The same as for senior unsecured debt.C. Higher than for senior unsecured debt.

A senior unsecured credit instrument holds a higher priority of claims than one ranked as:A. Mortgage debt.B. Second lien loan.C. Senior subordinated.

In a bankruptcy proceeding, when the absolute priority of claims is enforced:A. Senior subordinated creditors rank above second lien holders.B. Preferred equity shareholders rank above unsecured creditors.C. Creditors with a secured claim have the first right to the value of that specific property.

In the event of default, which of the following is most likely to have the highest recovery rate?A. Second lienB. Senior unsecuredC. Senior subordinated

The process of moving credit ratings of different issues up or down from the issuer rating in response to different payment priorities is best described as: A. Notching.B. Structural subordination.C. Cross-default provisions.

The factor considered by rating agencies when a corporation has debt at both its parent holding company and operating subsidiaries is best referred to as:A. Credit migration risk.B. Corporate family rating.C. Structural subordination.

Which type of security is most likely to have the same rating as the issuer?A. Preferred stockB. Senior secured bondC. Senior unsecured bond

Which of the following corporate debt instruments has the highest seniority ranking?A. Second lienB. Senior unsecuredC. Senior subordinated

An issuer credit rating usually applies to a company’s:A. Secured debt.B. Subordinated debt.C. Senior unsecured debt.

The rating agency process whereby the credit ratings on issues are moved up or down from the issuer rating best describes:A. Notching.B. Pari passu ranking.C. Cross-default provisions.

The notching adjustment for corporate bonds rated Aa2/AA is most likely:A. Larger than the notching adjustment for corporate bonds rated B2/B.B. The same as the notching adjustment for corporate bonds rated B2/B.C. Smaller than the notching adjustment for corporate bonds rated B2/B.

Which of the following statements about credit ratings is most accurate?A. Credit ratings can migrate over time.B. Changes in bond credit ratings precede changes in bond prices.C. Credit ratings are focused on expected loss rather than risk of default.

Which industry characteristic most likely has a positive effect on a company’s ability to service debt?A. Low barriers to entry in the industryB. High number of suppliers to the industryC. Broadly dispersed market share among large number of companies in the industry

When determining the capacity of a borrower to service debt, a credit analyst should begin with an examination of:A. Industry structure.B. Industry fundamentals.C. Company fundamentals.

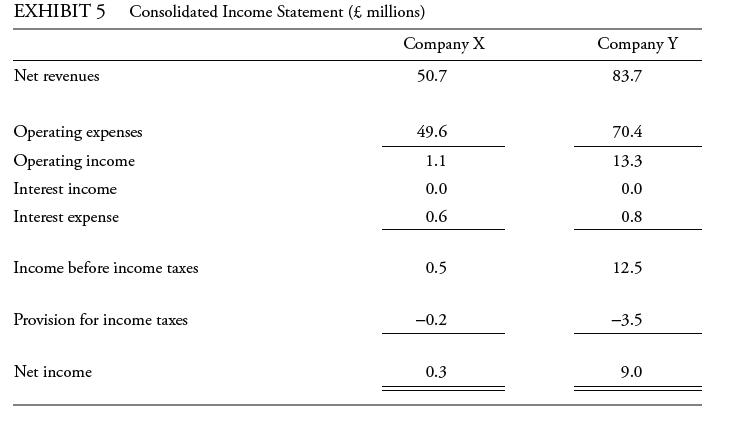

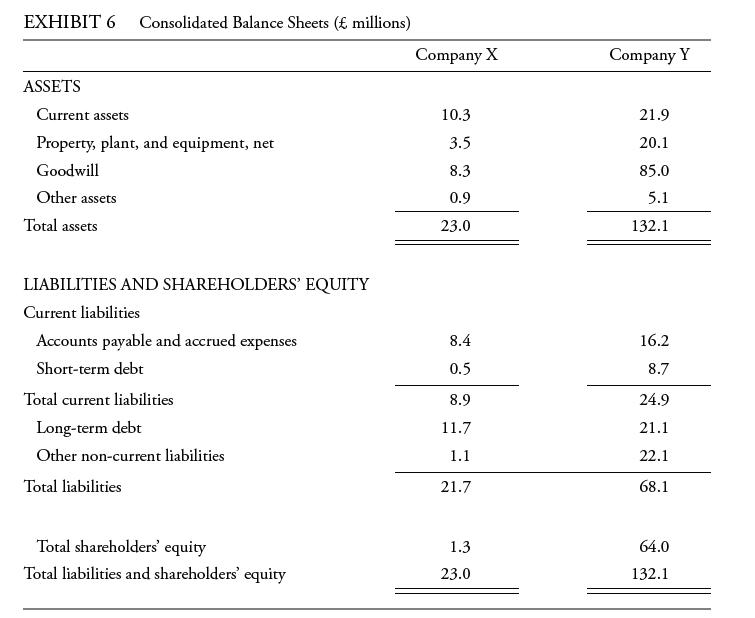

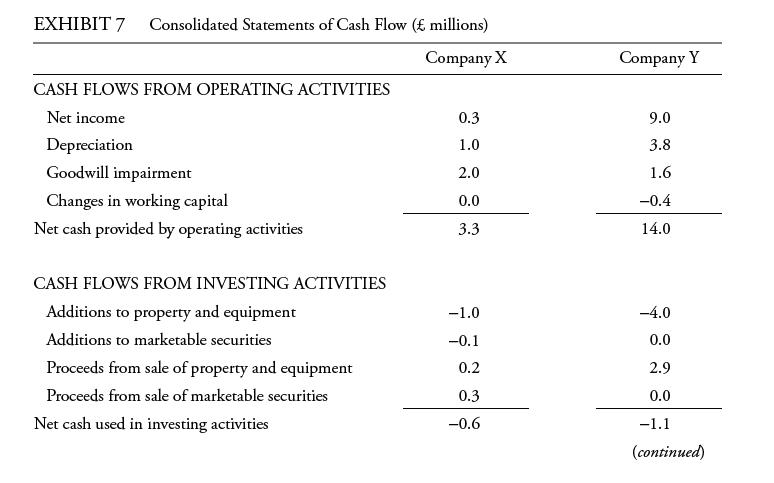

Based on Exhibits 5−7, in comparison to Company X, Company Y has a higher:A. Debt/capital.B. Debt/EBITDA.C. Free cash flow after dividends/debt.The following information relates EXHIBIT 5 Consolidated Income Statement (£ millions) Net revenues Operating expenses Operating income Interest

Which of the following accounting issues should mostly likely be considered a character warning flag in credit analysis?A. Expensing items immediatelyB. Changing auditors infrequentlyC. Significant off-balance-sheet financing

Based on Exhibits 5−7, in comparison to Company Y, Company X has greater:A. Leverage.B. Interest coverage.C. Operating profit margin.The following information relates EXHIBIT 5 Consolidated Income Statement (£ millions) Net revenues Operating expenses Operating income Interest income Interest

In credit analysis, capacity is best described as the:A. Quality of management.B. Ability of the borrower to make its debt payments on time.C. Quality and value of the assets supporting an issuer’s indebtedness.

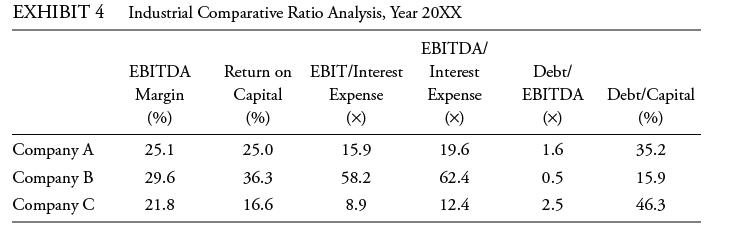

Based on only the leverage ratios in Exhibit 4, the company with the highest credit risk is:A. Company A.B. Company B.C. Company C.The following information relates EXHIBIT 4 Industrial Comparative Ratio Analysis, Year 20XX EBITDA/ Interest Expense Company A Company B Company

Among the four Cs of credit analysis, the recognition of revenue prematurely most likely reflects a company’s:A. Character.B. Covenants.C. Collateral.

Based on only the coverage ratios in Exhibit 4, the company with the highest credit quality is:A. Company A.B. Company B.C. Company C.The following information relates EXHIBIT 4 Industrial Comparative Ratio Analysis, Year 20XX EBITDA/ Interest Expense Company A Company B Company

Credit yield spreads most likely widen in response to:A. High demand for bonds.B. Weak performance of equities.C. Strengthening economic conditions.

The factor that most likely results in corporate credit spreads widening is:A. An improving credit cycle.B. Weakening economic conditions.C. A period of high demand for bonds.

Credit spreads are most likely to widen:A. In a strengthening economy.B. As the credit cycle improves.C. In periods of heavy new issue supply and low borrower demand.

Which of the following factors would best justify a decision to avoid investing in a country’s sovereign debt?A. Freely floating currencyB. A population that is not growingC. Suitable checks and balances in policymaking

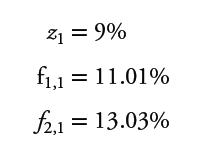

The spot rates for three hypothetical zero-coupon bonds (zeros) with maturities of one, two, and three years are given in the following table.Calculate the forward rate for a one-year zero issued one year from today, f1,1. Maturity (7) Spot rates 1 Z1 = 9% 2 Z₂ = 10% 3 23 = 11%

Consider a two-year loan beginning in one year (A = 1, B = 3). The one-year spot rate is z1 = zA = 7% = 0.07. The three-year spot rate is z3 = zB = 9% = 0.09.Calculate the one-year discount factor: DFA = DF1.

Given the data and conclusions for z1, f1,1, and f2,1 from Example 2:Show that the two-year spot rate of z2 = 10% and the three-year spot rate of z3 = 11% are geometric averages of the one-year spot rate and the forward rates. 21 = 9% f₁,1 f1,1 = 11.01% £2,1 = 13.03%

Given the spot rates z1 = 9%, z2 = 10%, and z3 = 11%:Determine whether the forward rate f1,2 is greater than or less than the long-term rate, z3.

Recall from earlier examples the spot rates z1= 9%, z2 = 10%, and z3 = 11%. Let yT be the YTM.Calculate the price of a two-year annual coupon bond using the spot rates. Assume the coupon rate is 6% and the face value is $1,000. Next, state the formula for determining the price of the bond in terms

When the spot curve is upward sloping, the forward curve:A. Lies above the spot curve.B. Lies below the spot curve.C. Is coincident with the spot curve.

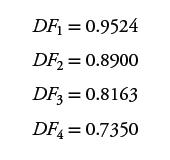

Suppose a government spot curve implies the following discount factors:Given this information, determine the swap rate curve. DF₁ = 0.9524 DF₂ = 0.8900 DF3 = 0.8163 DF4=0.7350

The “rolling down the yield curve” strategy is executed by buying bonds whose maturities are:A. Equal to the investor’s investment horizon.B. Longer than the investor’s investment horizon.C. Shorter than the investor’s investment horizon.

Many fixed-income portfolio managers are limited in or prohibited from high-yield bond investments. When a bond is downgraded from an investment-grade to a high-yield (junk) rating, it is referred to as a fallen angel. Because of restrictions, many pension funds sell fallen angels when they are

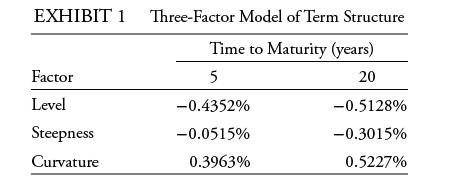

The most important factor in explaining changes in the yield curve has been found to be:A. Level.B. Curvature.C. Steepness.

Morgan Salaz is a fixed income analyst responsible for advising fixed income clients about bond trading opportunities. In the current recessionary environment, the level of government bond yields is low and the term structure is nearly flat. Salaz’s firm forecasts that after a brief recession,

Given spot rates for one-, two-, and three-year zero coupon bonds, how many forward rates can be calculated?

The spot rates for three hypothetical zero-coupon bonds (zeros) with maturities of one, two, and three years are given in the following table.Calculate the forward rate for a one-year zero issued two years from today, f2,1. Maturity (7) Spot rates 1 Z1 = 9% 2 2₂ = 10% 3 23 = 11%

Consider a two-year loan beginning in one year (A = 1, B = 3). The one-year spot rate is z1 = zA = 7% = 0.07. The three-year spot rate is z3 = zB = 9% = 0.09.Calculate the three-year discount factor: DFB = DF3.

Given the spot rates z1 = 9%, z2 = 10%, and z3 = 11%:Determine whether forward rates rise or fall as the initiation date, A, for the forward rate is later.

Recall from earlier examples the spot rates z1= 9%, z2 = 10%, and z3 = 11%. Let yT be the YTM.Calculate the price of a three-year annual coupon-paying bond using the spot rates. Assume the coupon rate is 5% and the face value is £100. Next, write a formula for determining the price of the bond

Which of the following statements concerning the YTM of a default-risk-free bond is most accurate? The YTM of such a bond:A. Equals the expected return on the bond if the bond is held to maturity.B. Can be viewed as a weighted average of the spot rates applying to its cash flows.C. Will be closer

A bond will be overvalued if the expected spot rate is:A. Equal to the current forward rate.B. Lower than the current forward rate.C. Higher than the current forward rate.

The term structure theory in which investors can be induced by relatively attractive yields to hold debt securities whose maturities do not match their investment horizon is best described as the:A. Preferred habitat theory.B. Segmented markets theory.C. Unbiased expectations theory.

A movement of the yield curve in which the short rate decreases by 150 bps and the long rate decreases by 50 bps would best be described as a:A. Flattening of the yield curve resulting from changes in level and steepness.B. Steepening of the yield curve resulting from changes in level and

Morgan Salaz is a fixed income analyst responsible for advising fixed income clients about bond trading opportunities. In the current recessionary environment, the level of government bond yields is low and the term structure is nearly flat. Salaz’s firm forecasts that after a brief recession,

Give two interpretations for the following forward rate: The two-year forward rate one year from now is 2%.

The spot rates for three hypothetical zero-coupon bonds (zeros) with maturities of one, two, and three years are given in the following table.Calculate the forward rate for a two-year zero issued one year from today, f1,2. Maturity (7) Spot rates 1 Z1 = 9% 2 2₂ = 10% 3 23 = 11%

Consider a two-year loan beginning in one year (A = 1, B = 3). The one-year spot rate is z1 = zA = 7% = 0.07. The three-year spot rate is z3 = zB = 9% = 0.09.Calculate the forward price of a two-year bond to be issued in one year: FA,B–A = F1,3.

When the spot curve is downward sloping, a later initiation date results in a forwardcurve that is:A. Closer to the spot curve.B. A greater distance above the spot curve.C. A greater distance below the spot curve.

Assume a flat yield curve of 6%. A three-year £100 bond is issued at par paying an annual coupon of 6%. What is the portfolio manager’s expected return if he predicts that the yield curve one year from today will be a flat 7%?A. 4.19%B. 6.00%C. 8.83%

The unbiased expectations theory assumes investors are:A. Risk averse.B. Risk neutral.C. Risk seeking.

The yield curve starts off flat, and then intermediate-maturity yields decrease by 10 bps while short- and long-maturity yields remain constant. This movement is best described as involving a change in:A. Level only.B. Curvature only.C. Level and curvature.

Describe the relationship between forward rates and spot rates if the yield curve is flat.

The spot rates for three hypothetical zero-coupon bonds (zeros) with maturities of one, two, and three years are given in the following table.Based on your answers to 1 and 2, describe the relationship between the spot rates and the implied one-year forward rates. Maturity (7) Spot rates 1 Z1 =

Consider a two-year loan beginning in one year (A = 1, B = 3). The one-year spot rate is z1 = zA = 7% = 0.07. The three-year spot rate is z3 = zB = 9% = 0.09.Interpret your answer to Problem 3.Problem 3Calculate the forward price of a two-year bond to be issued in one year: FA,B–A = F1,3.

A forward contract price will increase if:A. Future spot rates evolve as predicted by current forward rates.B. Future spot rates are lower than what is predicted by current forward rates.C. Future spot rates are higher than what is predicted by current forward rates.

Market evidence shows that forward rates are:A. Unbiased predictors of future spot rates.B. Upwardly biased predictors of future spot rates.C. Downwardly biased predictors of future spot rates.

Typically, short-term interest rates:A. Are less volatile than long-term interest rates.B. Are more volatile than long-term interest rates.C. Have about the same volatility as long-term interest rates.

A. Define the yield-to-maturity for a coupon bond.B. Is it possible for a coupon bond to earn less than the yield-to-maturity if held to maturity?

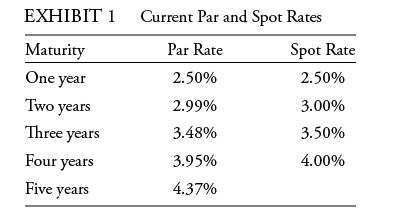

Based on Exhibit 1, the five-year spot rate is closest to:A. 4.40%.B. 4.45%.C. 4.50%.Jane Nguyen is a senior bond trader for an investment bank, and Chris Alexander is a junior bond trader at the bank. Nguyen is responsible for her own trading activities and also for providing assignments to

Based on Exhibit 1, the market is most likely expecting:A. Deflation.B. Inflation.C. No risk premiums.Jane Nguyen is a senior bond trader for an investment bank, and Chris Alexander is a junior bond trader at the bank. Nguyen is responsible for her own trading activities and also for providing

Based on Exhibit 1, the forward rate of a one-year loan beginning in three years is closest to:A. 4.17%.B. 4.50%.C. 5.51%.Jane Nguyen is a senior bond trader for an investment bank, and Chris Alexander is a junior bond trader at the bank. Nguyen is responsible for her own trading activities and

Based on Exhibit 1, which of the following forward rates can be computed?A. A one-year loan beginning in five yearsB. A three-year loan beginning in three yearsC. A four-year loan beginning in one yearJane Nguyen is a senior bond trader for an investment bank, and Chris Alexander is a junior bond

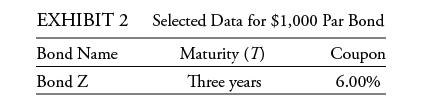

For Assignment 1, the yield-to-maturity for Bond Z is closest to the:A. One-year spot rate.B. Two-year spot rate.C. Three-year spot rate.Jane Nguyen is a senior bond trader for an investment bank, and Chris Alexander is a junior bond trader at the bank. Nguyen is responsible for her own trading

For Assignment 2, Alexander should conclude that Bond Z is currently:A. Undervalued.B. Fairly valued.C. Overvalued.Jane Nguyen is a senior bond trader for an investment bank, and Chris Alexander is a junior bond trader at the bank. Nguyen is responsible for her own trading activities and also for

By choosing to buy Bond Z, Nguyen is most likely making which of the following assumptions?A. Bond Z will be held to maturity.B. The three-year forward curve is above the spot curve.C. Future spot rates do not accurately reflect future inflation.Jane Nguyen is a senior bond trader for an investment

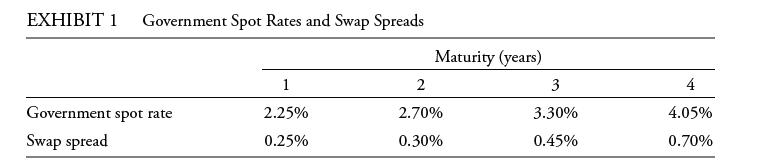

In his presentation of Investment 1, Smith could show that under the no-arbitrage principle, the forward price of a one-year government bond to be issued in one year is closest to:A. 0.9662.B. 0.9694.C. 0.9780.Laura Mathews recently hired Robert Smith, an investment adviser at Shire Gate Advisers,

In presenting Investment 1, using Shire Gate Advisers’ interest rate outlook, Smith could show that riding the yield curve provides a total return that is most likely:A. Lower than the return on a maturity-matching strategy.B. Equal to the return on a maturity-matching strategy.C. Higher than the

In presenting Investment 2, Smith should show an annual return closest to:A. 4.31%.B. 5.42%.C. 6.53%.Laura Mathews recently hired Robert Smith, an investment adviser at Shire Gate Advisers, to assist her in investing. Mathews states that her investment time horizon is short, approximately two years

The bond in Investment 3 is most likely trading at a price of:A. 100.97.B. 101.54.C. 104.09.Laura Mathews recently hired Robert Smith, an investment adviser at Shire Gate Advisers, to assist her in investing. Mathews states that her investment time horizon is short, approximately two years or less.

The most appropriate response to Mathews’ question regarding a spread measure is the:A. Z-spread.B. TED spread.C. Libor–OIS spread.Laura Mathews recently hired Robert Smith, an investment adviser at Shire Gate Advisers, to assist her in investing. Mathews states that her investment time horizon

Madison’s views on the term structure of interest rates are most consistent with the:A. Local expectations theory.B. Segmented markets theory.C. Liquidity preference theory.Rowan Madison is a junior analyst at Cardinal Capital. Sage Winter, a senior portfolio manager and Madison’s supervisor,

Is Madison’s response regarding the factors that affect short-term and long-term rate volatility correct?A. YesB. No, she is incorrect regarding factors linked to long-term rate volatilityC. No, she is incorrect regarding factors linked to short-term rate volatilityRowan Madison is a junior

In contrast to high-yield credit analysis, investment-grade analysis is more likely to rely on:A. Spread risk.B. An assessment of bank credit facilities.C. Matching of liquidity sources to upcoming debt maturities.

Which of the following factors in credit analysis is more important for general obligation non-sovereign government debt than for sovereign debt?A. Per capita incomeB. Power to levy and collect taxesC. Requirement to balance an operating budget

Market evidence shows that short holding-period returns on short-maturity bonds most often are:A. Less than those on long-maturity bonds.B. About equal to those on long-maturity bonds.C. Greater than those on long-maturity bonds.

Suppose for a given portfolio that key rate changes are considered to be changes in the yield on 1-year, 5-year, and 10-year securities. Estimated key rate durations are KeyDur1 = 0.50, KeyDur2 = 0.70, and KeyDur3 = 0.90. What is the percentage change in the value of the portfolio if a parallel

If a bond trader believes that current forward rates overstate future spot rates, how might she profit from that conclusion?

Explain the strategy of rolling down the yield curve.

What are the advantages of using the swap curve as a benchmark of interest rates relative to a government bond yield curve?

What is the TED spread, and what type of risk does it measure?

What is the SOFR rate, and which market conditions does it reflect?

According to the local expectations theory, what would be the difference in the onemonth total return if an investor purchased a five-year zero-coupon bond versus a twoyear zero-coupon bond?

Showing 1700 - 1800

of 2084

First

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

Step by Step Answers