New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

fixed income analysis

Fixed Income Analysis 5th Edition Barbara S. Petitt - Solutions

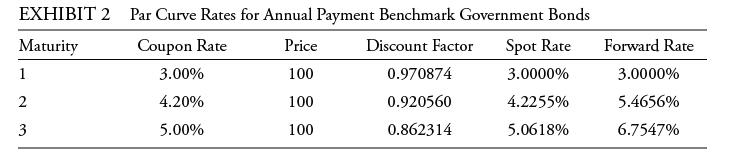

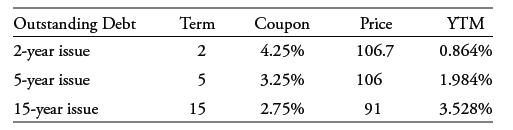

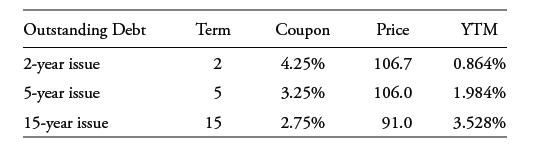

According to Watt’s statement, the shape of UNAB’s credit curve is most likely: A. Flat.B. Upward-sloping.C. Downward-sloping.On 1 January 20X2, Deem Advisors purchased a $10 million six-year senior unsecured bond issued by UNAB Corporation. Six months later (1 July 20X2), concerned about the

Should Watt conclude that UNAB experienced a credit event?A. YesB. No, because UNAB did not file for bankruptcyC. No, because the failure to pay occurred on a subordinated unsecured bondOn 1 January 20X2, Deem Advisors purchased a $10 million six-year senior unsecured bond issued by UNAB

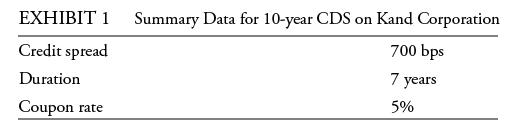

Based on Exhibit 1, the upfront premium as a percent of the notional for the CDS protection on Kand Corporation would be closest to:A. 2.0%.B. 9.8%.C. 14.0%.On 1 January 20X2, Deem Advisors purchased a $10 million six-year senior unsecured bond issued by UNAB Corporation. Six months later (1 July

On 1 January 20X2, Deem Advisors purchased a $10 million six-year senior unsecured bond issued by UNAB Corporation. Six months later (1 July 20X2), concerned about the portfolio’s credit exposure to UNAB, Doris Morrison, the chief investment officer at Deem Advisors, buys $10 million protection

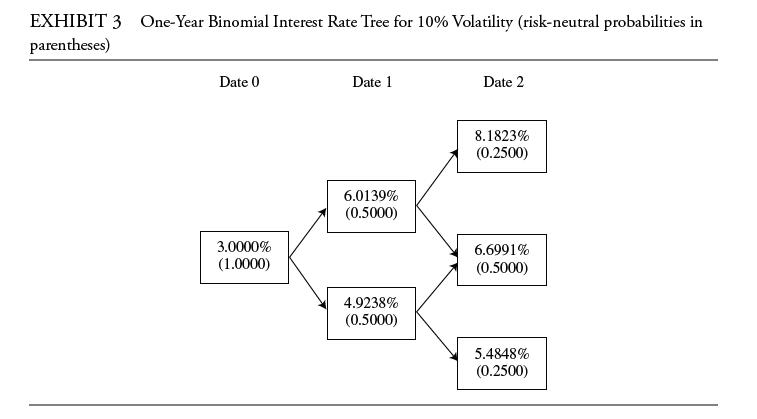

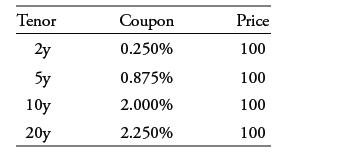

To satisfy the compliance requirements referenced by Chan, the Fund is most likely required to:A. Set a notional amount.B. Post an upfront payment.C. Sign an ISDA master agreement.John Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund (the Fund), meets with Sofia

Which type of CDS should Chan recommend to Smith?A. CDS indexB. Tranche CDSC. Single-name CDSJohn Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund (the Fund), meets with Sofia Chan, a derivatives strategist with Shire Gate Securities (SGS), to discuss investment

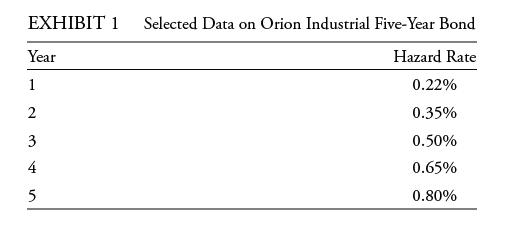

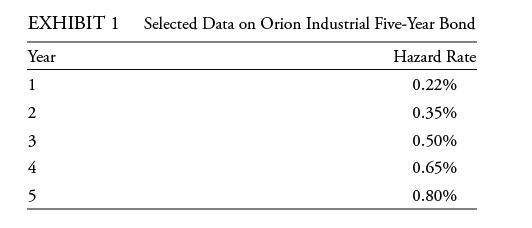

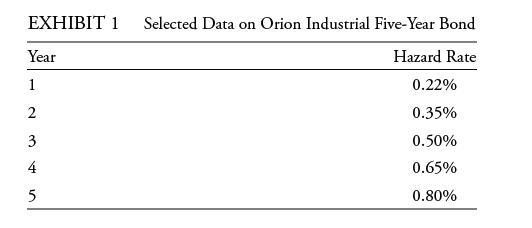

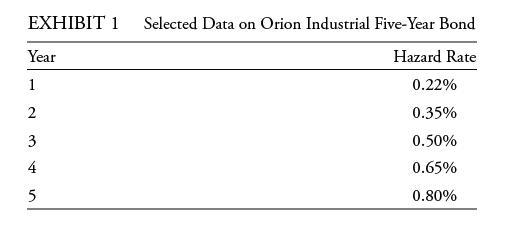

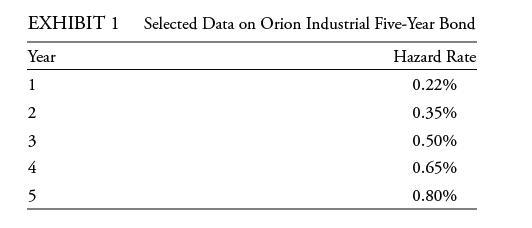

Based on Exhibit 1, the probability of Orion defaulting on the bond during the first three years is closest to:A. 1.07%.B. 2.50%.C. 3.85%.John Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund (the Fund), meets with Sofia Chan, a derivatives strategist with Shire Gate

To close the position on the hypothetical Orion trade, the Fund:A. Sells protection at a higher premium than it paid at the start of the trade.B. Buys protection at a lower premium than it received at the start of the trade.C. Buys protection at a higher premium than it received at the start of the

The hypothetical Orion trade generated an approximate:A. Loss of £117,000.B. Gain of £117,000.C. Gain of £234,000.John Smith, a fixed-income portfolio manager at a €10 billion sovereign wealth fund (the Fund), meets with Sofia Chan, a derivatives strategist with Shire Gate Securities (SGS), to

Based on the three economic outlook statements, a profitable long/short trade would be to:A. sell protection using a Canadian CDX IG and buy protection using a US CDX IG.B. buy protection using an iTraxx Crossover and sell protection using an iTraxx Main.C. buy protection using an electric car CDS

Given the description of the asset pool of the ABS, Kowalski should recommend a:A. Loan-by-loan approach.B. Portfolio-based approach.C. Statistics-based approach.Anna Lebedeva is a fixed-income portfolio manager. Paulina Kowalski, a junior analyst, and Lebedeva meet to review several positions in

The curve trade that would best capitalize on Chan’s view of the US credit curve is to:A. Buy protection using a 20-year CDX and buy protection using a 2-year CDX.B. Buy protection using a 20-year CDX and sell protection using a 2-year CDX.C. Sell protection using a 20-year CDX and buy protection

A profitable equity-versus-credit trade involving Delta and Zega is to:A. Short Zega shares and buy protection on Delta using the 10-year CDS.B. Go long Zega shares and buy protection on Delta using 5-year CDS.C. Go long Delta shares and buy protection on Delta using 5-year CDS.John Smith, a

Mary is anxious about the level of risk in her portfolio because of a recent period of increased equity market volatility. Most of her wealth is invested in a diversified global equity portfolio.She contacts two wealth management firms (Firm A and Firm B) for advice. In her conversations with each

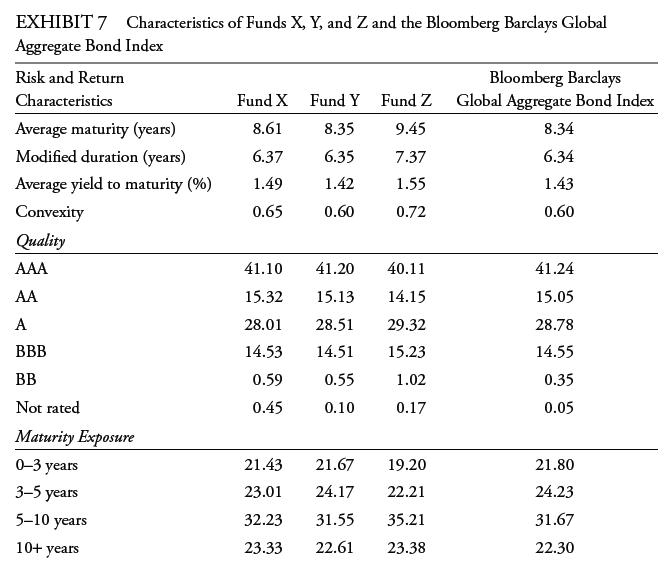

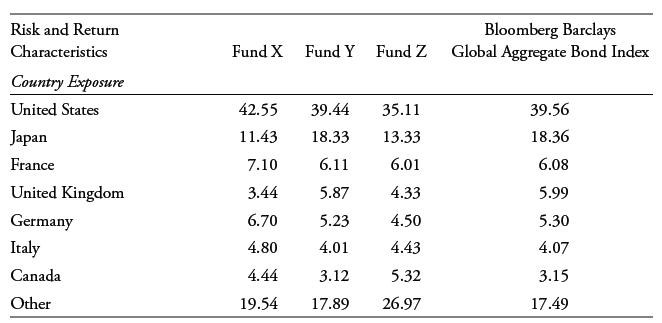

A consultant for a large corporate pension plan is looking at three funds (Funds X, Y, and Z) as part of the pension plan’s global fixed-income allocation. All three funds use the Bloomberg Barclays Global Aggregate Bond Index as a benchmark. Exhibit 7 provides characteristics of each fund and

Which of the following best describes a measure of sensitivity to changes in yields to maturity for a portfolio of bonds with cash flows contingent on interest rate changes?A. Portfolio dispersionB. Modified durationC. Effective duration

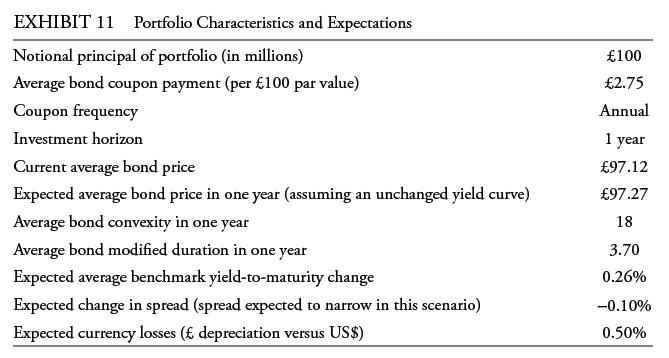

Ann Smith works for a US investment firm in its London office. She manages the firm’s British pound–denominated corporate bond portfolio. Her department head in New York City has asked Smith to make a presentation on next year’s total expected return of her portfolio in US dollars and the

Kevin Tucker manages a global bond portfolio. At a recent investment committee meeting, Tucker discussed his portfolio’s domestic (very high-credit-quality) government bond allocation with another committee member. The other committee member argued that if the yield curve is expected to remain

Arturo manages a mutual fund that is benchmarked to the Global Aggregate Bond Index. He currently has a bullish view of the global economy and believes corporate bond spreads are attractive. He is bearish on US Treasury interest rates given his economic growth forecast and expects rates to

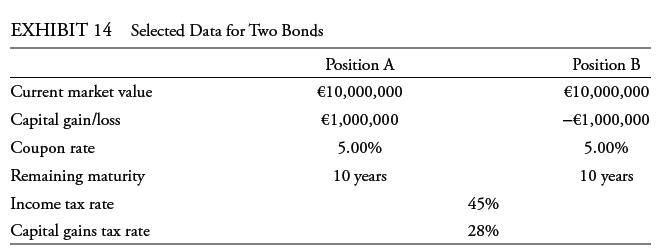

A bond portfolio manager needs to raise €10,000,000 in cash to cover outflows in the portfolio she manages. To satisfy her cash demands, she considers one of two corporate bond positions for potential liquidation: Position A and Position B. For tax purposes, capital gains receive pass-through

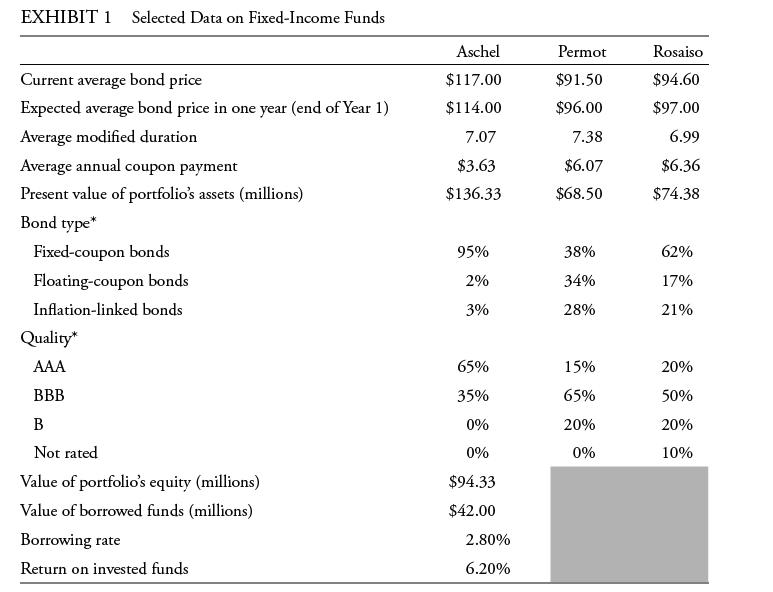

Based on Exhibit 1, which fund provides the highest level of protection against inflation for coupon payments?A. AschelB. PermotC. RosaisoCécile is a junior analyst for an international wealth management firm. Her supervisor, Margit, asks Cécile to evaluate three fixed-income funds as part of the

Based on Exhibit 1, the rolling yield of Aschel over a one-year investment horizon is closest to:A. −2.56%.B. 0.54%.C. 5.66%.Cécile is a junior analyst for an international wealth management firm. Her supervisor, Margit, asks Cécile to evaluate three fixed-income funds as part of the firm’s

Which of the following is a true statement about portfolio dispersion?A. It can be described as the variance of time to the receipt of cash flows.B. The higher the dispersion, the lower the convexity of the portfolio.C. It determines the portfolio’s sensitivity to changes in credit spreads.

The leveraged portfolio return for Aschel is closest to:A. 7.25%.B. 7.71%.C. 8.96%.Cécile is a junior analyst for an international wealth management firm. Her supervisor, Margit, asks Cécile to evaluate three fixed-income funds as part of the firm’s global fixed-income offerings. Selected

Based on Note 2, Rosaiso is the only fund for which the expected change in price based on the investor’s views of yields to maturity and yield spreads should be calculated using:A. convexity.B. modified duration.C. effective duration.Cécile is a junior analyst for an international wealth

Is Cécile correct with respect to key features of liability-based mandates?A. YesB. No, only Feature 1 is correct.C. No, only Feature 2 is correct.Cécile is a junior analyst for an international wealth management firm. Her supervisor, Margit, asks Cécile to evaluate three fixed-income funds as

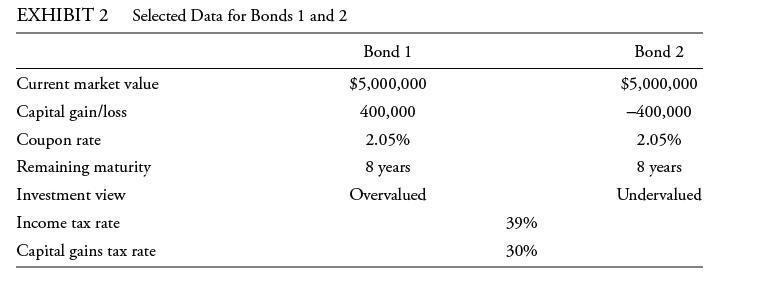

Based on Exhibit 2, the optimal strategy to meet Villash Foundation’s cash needs is the sale of:A. 100% of Bond 1.B. 100% of Bond 2.C. 50% of Bond 1 and 50% of Bond 2.Cécile is a junior analyst for an international wealth management firm. Her supervisor, Margit, asks Cécile to evaluate three

Which approach to its total return mandate is the fund’s domestic bond portfolio most likely to use?A. Pure indexingB. Enhanced indexingC. Active managementCelia is chief investment officer for the Topanga Investors Fund, which invests in equities and fixed income. The clients in the fund are all

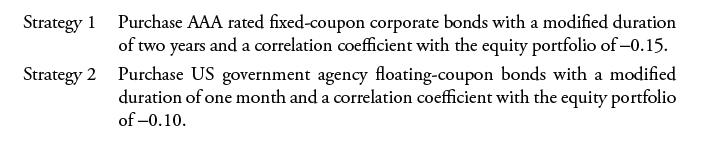

Strategy 2 is most likely preferred to Strategy 1 for meeting the objective of:A. Protecting against inflation.B. Funding future liabilities.C. Minimizing the correlation of the fund’s domestic bond portfolio and equity portfolio.Celia is chief investment officer for the Topanga Investors Fund,

Are Dan’s statements to Celia that support Dan’s choice of bonds to sell correct?A. Only Statement 1 is correct.B. Only Statement 2 is correct.C. Neither Statement 1 nor Statement 2 is correct.Celia is chief investment officer for the Topanga Investors Fund, which invests in equities and fixed

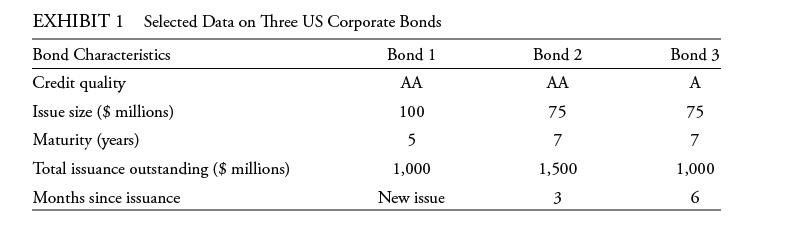

Based on Exhibit 1, which bond most likely has the highest liquidity premium?A. Bond 1B. Bond 2C. Bond 3Celia is chief investment officer for the Topanga Investors Fund, which invests in equities and fixed income. The clients in the fund are all taxable investors. The fixed-income allocation

Based on Exhibit 2, the total expected return of the fund’s global bond portfolio is closest to:A. 0.90%.B. 1.66%.C. 3.76%.Celia is chief investment officer for the Topanga Investors Fund, which invests in equities and fixed income. The clients in the fund are all taxable investors. The

Celia is chief investment officer for the Topanga Investors Fund, which invests in equities and fixed income. The clients in the fund are all taxable investors. The fixed-income allocation includes a domestic (US) bond portfolio and an externally managed global bond portfolio.The domestic bond

An institutional client asks a fixed-income investment adviser to recommend a portfolio to immunize a single 10-year liability. It is understood that the chosen portfolio will need to be rebalanced over time to maintain its target duration. The adviser proposes two portfolios of coupon-bearing

Modern Mortgage, a savings bank, decides to establish an ALCO (asset−liability committee) to improve risk management and coordination of its loan and deposit ratesetting processes. Modern’s primary assets are long-term, fixed-rate, monthly payment, fully amortizing residential mortgage loans.

Mr. Zheng is a Shanghai-based wealth adviser. A major client of his, the Wang family, holds most of its assets in residential property and equity investments and relies on regular cash flows from those holdings. Zheng recommends that the Wang family also have a laddered portfolio of Chinese

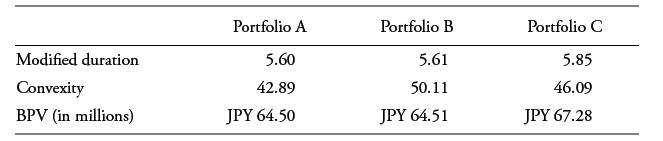

A Japanese corporation recently sold one of its lines of business and would like to use the cash to retire the debt liabilities that financed those assets. Summary statistics for the multiple debt liabilities, which range in maturity from three to seven years, are market value, JPY 110.4 billion;

A Frankfurt-based asset manager uses the Long Bund contract traded at the Intercontinental Exchange (ICE) futures exchange to manage the gaps that arise from “duration drift” in a portfolio of German government bonds that are used to immunize a portfolio of corporate debt liabilities. This

An asset manager is asked to build and manage a portfolio of fixed-income bonds to retire multiple corporate debt liabilities. The debt liabilities have a market value of GBP 50,652,108, a modified duration of 7.15, and a BPV of GBP 36,216.The asset manager buys a portfolio of British government

A corporation is concerned about the defined benefit pension plan that it sponsors for its unionized employees. Because of recent declines in corporate bond yields and weak performance in its equity investments, the plan finds itself to be only about 80% funded based on the PBO measure. That fact

A derivatives consultant, a former head of interest rate swaps trading at a major London bank, is asked by a Spanish corporation to devise an overlay strategy to “effectively defease” a large debt liability. That means that there are dedicated assets to retire the debt even if both assets and

Cindy Cheng, a Hong Kong-based portfolio manager, has established the All Asia Dragon Fund, a fixed-income fund designed to outperform the Markit iBoxx Asian Local Bond Index (ALBI). The ALBI tracks the total return performance of liquid bonds denominated in local currencies in the following

Adelaide Super, a superannuation fund, offers a range of fixed interest (or fixed-income) investment choices to its members. Superannuation funds are Australian government-supported arrangements for Australian workers to save for retirement, which combine a government-mandated minimum percentage of

Given the significant rise in regional bond issuance following the 2008 global financial crisis, Next Europe Asset Management Limited aims to grow its assets under management by attracting a variety of new local Eurozone investors to the broader set of alternatives available in the current

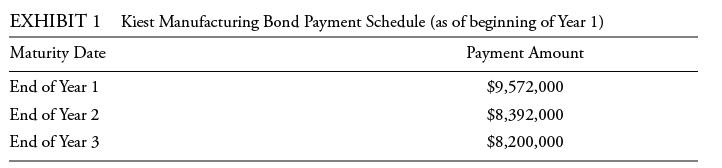

Based on Exhibit 1, Kiest’s liabilities would be classified as:A. Type I.B. Type II.C. Type III.Serena is a risk management specialist with Liability Protection Advisors. Trey, CFO of Kiest Manufacturing, enlists Serena’s help with three projects. The first project is to defease some of

A Japanese corporation recently sold one of its lines of business and would like to use the cash to retire the debt liabilities that financed those assets. Summary statistics for the multiple debt liabilities, which range in maturity from three to seven years, are market value, JPY 110.4 billion;

Modern Mortgage, a savings bank, decides to establish an ALCO (asset−liability committee) to improve risk management and coordination of its loan and deposit ratesetting processes. Modern’s primary assets are long-term, fixed-rate, monthly payment, fully amortizing residential mortgage loans.

A Frankfurt-based asset manager uses the Long Bund contract traded at the Intercontinental Exchange (ICE) futures exchange to manage the gaps that arise from “duration drift” in a portfolio of German government bonds that are used to immunize a portfolio of corporate debt liabilities. This

A corporation is concerned about the defined benefit pension plan that it sponsors for its unionized employees. Because of recent declines in corporate bond yields and weak performance in its equity investments, the plan finds itself to be only about 80% funded based on the PBO measure. That fact

A derivatives consultant, a former head of interest rate swaps trading at a major London bank, is asked by a Spanish corporation to devise an overlay strategy to “effectively defease” a large debt liability. That means that there are dedicated assets to retire the debt even if both assets and

Cindy Cheng, a Hong Kong-based portfolio manager, has established the All Asia Dragon Fund, a fixed-income fund designed to outperform the Markit iBoxx Asian Local Bond Index (ALBI). The ALBI tracks the total return performance of liquid bonds denominated in local currencies in the following

Given the significant rise in regional bond issuance following the 2008 global financial crisis, Next Europe Asset Management Limited aims to grow its assets under management by attracting a variety of new local Eurozone investors to the broader set of alternatives available in the current

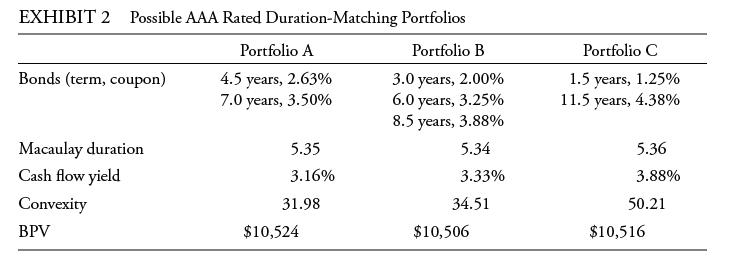

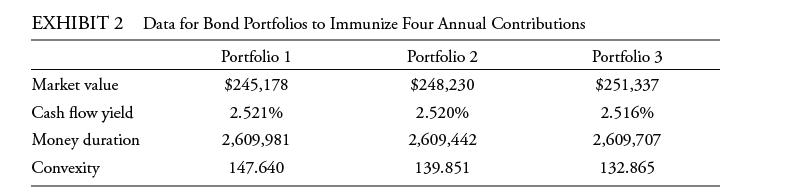

Based on Exhibit 2, the portfolio with the greatest structural risk is:A. Portfolio A.B. Portfolio B.C. Portfolio C.Serena is a risk management specialist with Liability Protection Advisors. Trey, CFO of Kiest Manufacturing, enlists Serena’s help with three projects. The first project is to

Modern Mortgage, a savings bank, decides to establish an ALCO (asset−liability committee) to improve risk management and coordination of its loan and deposit ratesetting processes. Modern’s primary assets are long-term, fixed-rate, monthly payment, fully amortizing residential mortgage loans.

Modern Mortgage, a savings bank, decides to establish an ALCO (asset−liability committee) to improve risk management and coordination of its loan and deposit ratesetting processes. Modern’s primary assets are long-term, fixed-rate, monthly payment, fully amortizing residential mortgage loans.

Given the significant rise in regional bond issuance following the 2008 global financial crisis, Next Europe Asset Management Limited aims to grow its assets under management by attracting a variety of new local Eurozone investors to the broader set of alternatives available in the current

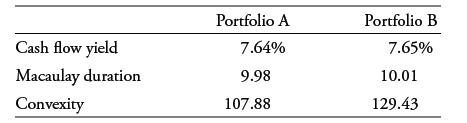

Which portfolio in Exhibit 2 fails to meet the requirements to achieve immunization for multiple liabilities?A. Portfolio AB. Portfolio BC. Portfolio CSerena is a risk management specialist with Liability Protection Advisors. Trey, CFO of Kiest Manufacturing, enlists Serena’s help with three

Based on Exhibit 2, relative to Portfolio C, Portfolio B:A. Has higher cash flow reinvestment risk.B. Is a more desirable portfolio for liquidity management.C. Provides less protection from yield curve shifts and twists. Serena is a risk management specialist with Liability Protection

Serena’s three assumptions regarding the duration-matching strategy indicate the presence of:A. Model risk.B. Spread risk.C. Counterparty credit risk.Serena is a risk management specialist with Liability Protection Advisors. Trey, CFO of Kiest Manufacturing, enlists Serena’s help with three

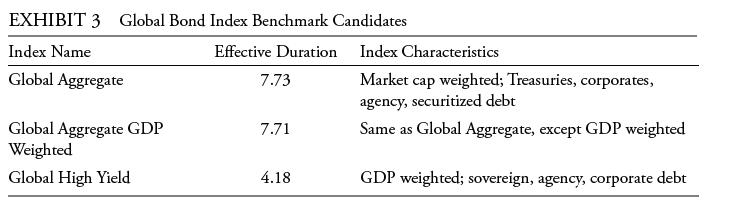

The global bond benchmark in Exhibit 3 that is least appropriate for Kiest to use is the:A. Global Aggregate Index.B. Global High Yield Index.C. Global Aggregate GDP Weighted Index.Serena is a risk management specialist with Liability Protection Advisors. Trey, CFO of Kiest Manufacturing, enlists

To meet both of Trey’s guidelines for the pension’s bond fund investment, Serena should recommend:A. Pure indexing.B. Enhanced indexing.C. Active management.Serena is a risk management specialist with Liability Protection Advisors. Trey, CFO of Kiest Manufacturing, enlists Serena’s help with

Chaopraya is an investment advisor for high-net-worth individuals. One of her clients, Schuylkill, plans to fund her grandson’s college education and considers two options:• Option 1: Contribute a lump sum of $300,000 in 10 years.• Option 2: Contribute four level annual payments of $76,500

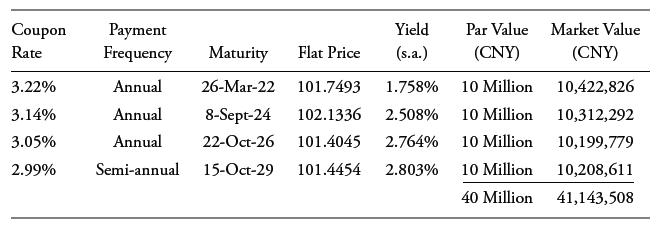

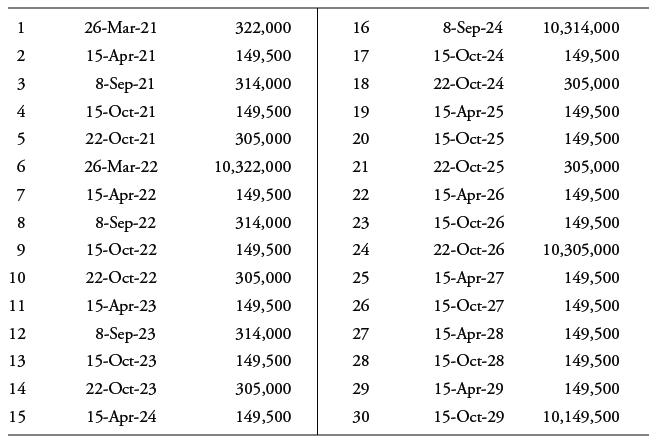

A Sydney-based fixed-income portfolio manager is considering the following Commonwealth of Australia government bonds traded on the ASX (Australian Stock Exchange):The manager is considering portfolio strategies based upon various interest rate scenarios over the next 12 months. She is considering

Returning to our earlier example of the German media and telecommunications issuer, the investor decides instead to position her portfolio for a steepening of the issuer’s credit curve using the CDS market. Details of on-the-run 5- and 10-year CDS contracts outstanding are as follows.Describe an

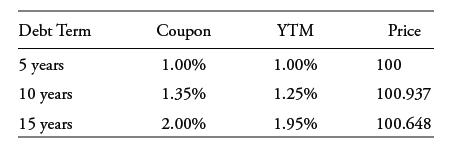

A Sydney-based investor notes the following available option-free bonds for an A rated Australian issuer:The 5-year, 10-year, and 15-year Australian government bonds have YTMs and coupons of 0.50%, 0.75%, and 1.10%, respectively, and both corporate and government bonds have a semiannual coupon. As

Returning to our earlier example of the investment-grade German media and telecommunications issuer, the investor decides instead to overweight exposure to this name by taking a long risk position in the single-name 10-year CDS market for one year. Details of today’s 5-year and 10-year CDS

A bank analyst observes a first lien bank loan maturing in two years with a spread of 100 bps from an issuer considering a new second lien bank loan. Using average historical volume weighted corporate debt recovery rates (RR) as a guide, what is the estimated credit spread for the new second lien

Which of the following best describes the expected shape of the credit spread curve in an economic downturn?A. Investment-grade and high-yield issuers usually experience similar credit spread curve steepening because of declining corporate profitability.B. High-yield issuers usually experience more

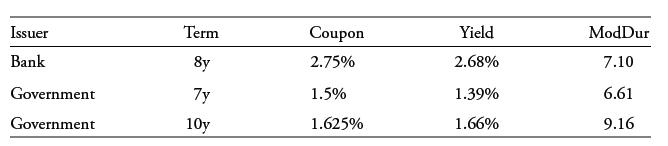

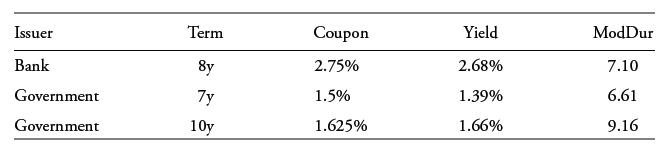

A portfolio manager considers the following annual coupon bonds:Calculate the yield spread and G-spread for the bank bond. Issuer Bank Government Government Term 8y 7y 10y Coupon 2.75% 1.5% 1.625% Yield 2.68% 1.39% 1.66% ModDur 7.10 6.61 9.16

A high-yield bond fund manager is considering adding a US$50 million face value, fiveyear, 6.75% semiannual coupon bond with a YTM of 5.40% to an active portfolio. The manager uses regression analysis to estimate the bond’s empirical duration to be 2.95. Calculate the bond’s analytical

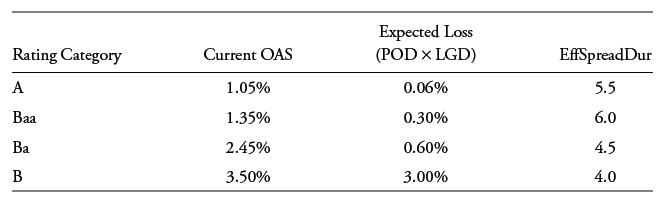

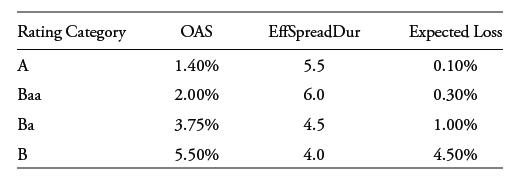

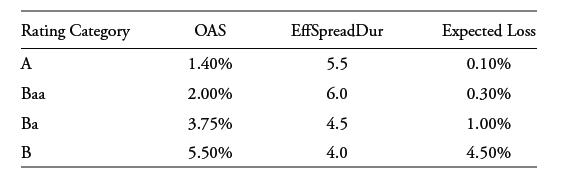

An active credit portfolio manager considers the following corporate bond portfolio choices familiar from an earlier example:The investor anticipates an economic slowdown in the next year that will have a greater adverse impact on lower-rated issuers. Assume that an index portfolio is equally

Consider the information from the bank and government annual coupon bonds from the prior example:Assuming that 7- and 10-year swap spreads over the respective government benchmark yields to maturity are 15 bps and 20 bps, calculate the ASW and the I-spread for the bank bond, and interpret the

An active United States–based credit manager is offered similar US corporate bond portfolio choices to those in an earlier example:As in the earlier case, the manager expects an economic rebound but now believes that European economies will experience a stronger recovery than the United States.In

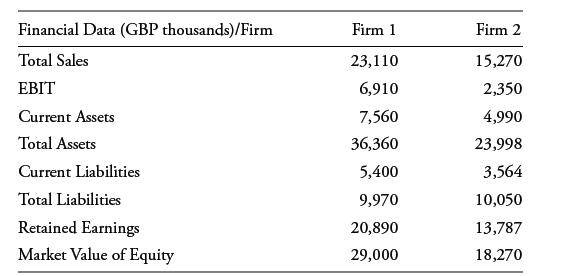

A United Kingdom–based financial analyst considers a Z-score model in evaluating two publicly traded non-manufacturing companies as follows: Z-Score Model = 1.2 × A + 1.4 × B + 3.3 × C + 0.6 × D + 0.999 × E, whereA is Working Capital/Total AssetsB is Retained Earnings/Total AssetsC is

An investor is conducting a relative value analysis on global bond issuers in the health care sector. He is trying to decide whether the global health care sector is a sufficiently narrow sector for his analysis. Through his research, he has determined the following:• Biotech and pharmaceutical

A portfolio manager considers two industrial bonds for a one-year investment:The manager observes a historical annual default probability of 0.27% for A2 rated issuers and 3.19% for B2 rated issuers and assumes a 40% recovery rate for both bonds.Compute the estimated excess return for each bond

A United States–based issuer has the following option-free bonds outstanding:Current on-the-run US Treasury YTMs are as follows:An investor considers the purchase of a new 10-year issue from the company and expects the new bond to include a 10 bp new issue premium. What is the fair value spread

Recall the earlier example of a United States–based issuer with the following option-free bonds outstanding:Assume the investor instead holds a US$50 million face value position in the outstanding 15-year bond. Historical TRACE data suggest an average $5 million daily trading volume in the

An active credit portfolio manager considers the following corporate bond portfolio choices familiar from an earlier example:The investor anticipates an economic slowdown in the next year that will have a greater adverse impact on lower-rated issuers. Assume that an index portfolio is equally

An investor is considering the portfolio impact of a new 12-year corporate bond position with a $75 million face value, a 3.25% coupon, current YTM of 2.85%, modified duration of 9.887, and a price of 104.0175 per 100 of face value.Which of the following VaR measures is most appropriate for the

An investor is considering the portfolio impact of a new 12-year corporate bond position with a $75 million face value, a 3.25% coupon, current YTM of 2.85%, modified duration of 9.887, and a price of 104.0175 per 100 of face value.What is the approximate VaR for the bond position at a 99%

An active portfolio manager seeking to purchase single-name CDS protection observes a 1.75% 10-year market credit spread for a private investment-grade issuer. The effective spread duration is 8.75 and CDS basis is close to zero.What should the protection buyer expect to pay or receive to enter a

An active portfolio manager seeking to purchase single-name CDS protection observes a 1.75% 10-year market credit spread for a private investment-grade issuer. The effective spread duration is 8.75 and CDS basis is close to zero.Once the manager purchases CDS protection, the issuer’s CDS spread

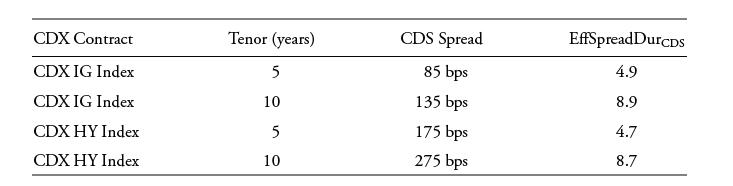

An investor observes the following current CDS market information:Select the most appropriate credit portfolio positioning strategy to capitalize on an expected steepening of the investment-grade credit spread curve.A. Sell protection on the 10-year CDX IG index and purchase protection on the

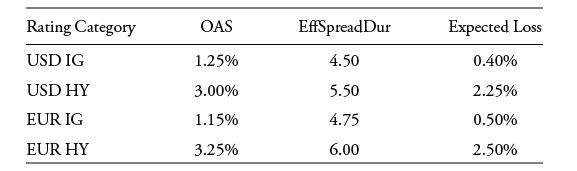

An active United States–based credit manager faces the following US and European investment-grade and high-yield corporate bond portfolio choices:The EUR IG and EUR HY allocations are denominated in euros, and the euro is expected to depreciate by 2% versus the US dollar over the next year.What

An active United States–based credit manager faces the following US and European investment-grade and high-yield corporate bond portfolio choices:The EUR IG and EUR HY allocations are denominated in euros, and the euro is expected to depreciate by 2% versus the US dollar over the next year.Which

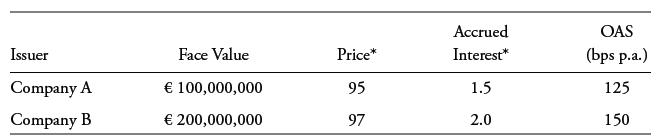

A European portfolio manager is presented with the following information on a portfolio of two bonds. Calculate the OAS of the portfolio. Issuer Company A Company B Face Value € 100,000,000 € 200,000,000 Price* 95 97 Accrued Interest* 1.5 2.0 OAS (bps p.a.) 125 150

As in the prior example, an active fixed-income manager anticipates an economic slowdown in the next year with a greater adverse impact on lower-rated issuers. The manager chooses a tactical CDX (credit default swap index) strategy combining positions in investment-grade and high-yield CDX

An active manager observes a yield spread for an outstanding corporate bond that is above the G-spread for that same bond. Which of the following is the most likely explanation for the difference?A. The government benchmark bond used to calculate the yield spread has a shorter maturity than the

A long-only active credit manager faces similar corporate bond portfolio choices to those in an earlier example:Given an expectation that an economic rebound will cause both credit spreads and expected loss rates to fall by one-third, an active manager decides to tilt her credit portfolio toward

A London-based investor owns a five-year ₤100 million FRN that pays three-month MRR + 1.75% on a quarterly basis. The current MRR of 0.50% is assumed to remain constant over time. If the issuer’s credit risk deteriorates and the DM rises to 2.25%, explain whether the FRN is trading at a

An Australian investor holds a three-year FRN with a coupon of three-month MRR + 1.25%. Given an expected strong economic recovery, she anticipates a rise in Australian MRR over the next three years and an improvement in the FRN issuer’s creditworthiness. Which of the following credit spread

As in the prior example, an active fixed-income manager anticipates an economic rebound that is expected to cause high-yield credit curve steepening. The manager chooses a tactical CDX strategy combining 5-year and 10-year credit positions to capitalize on this view. Current market information for

A London-based investor wants to estimate roll-down return attributable to a fixed-rate, option-free corporate bond versus UK gilts over the next six months assuming a static, upward-sloping government yield curve and a constant credit spread. The corporate bond has exactly 10 years remaining to

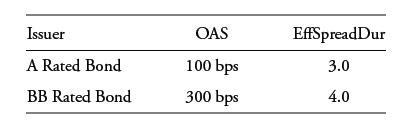

A financial analyst compares a portfolio evenly split between two technology company bonds trading at par to an index with an average OAS of 125 bps.Calculate the portfolio DTS, and estimate how the technology bond portfolio will perform if index OAS widens by 10 bps. Issuer A Rated Bond BB Rated

A financial analyst is considering the likelihood that an emerging market sovereign issuer of US dollar–denominated bonds is able to meet its interest payments over the next 12 months. Which of the following financial ratios is most appropriate to assess the sovereign borrower’s liquidity

A corporate bond has an effective spread duration of five years and a credit spread of 2.75% (275 bps).What is the approximate excess return if the bond is held for six months and the credit spread narrows 50 bps to 2.25%? Assume the spread duration remains at five years and that the bond does not

An active United States–based investor is considering a portfolio allocation to the bonds of a major commodities producer headquartered in an emerging market economy. The issuer is a major exporter, and commodity exports comprise a significant proportion of the country’s economic growth.

An active credit manager anticipates an economic slowdown led by a decline in residential housing prices. Which of the following portfolio positioning strategies involving structured products is the most appropriate to consider under this scenario?A. Shift exposure from an A rated tranche of a

An active fixed-income manager is conducting scenario analysis for the MBS component of a portfolio. Which of the following analytical model input changes is most likely to reduce the future value of the MBS subportfolio versus similar option-free bond holdings?A. An increase in benchmark yield

Showing 1400 - 1500

of 2084

First

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

Step by Step Answers