New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

fixed income analysis

Fixed Income Analysis 5th Edition Barbara S. Petitt - Solutions

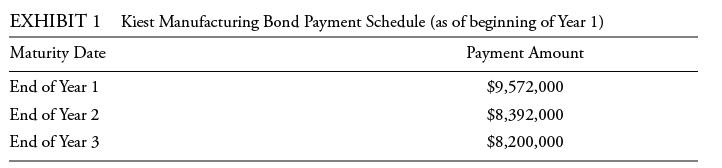

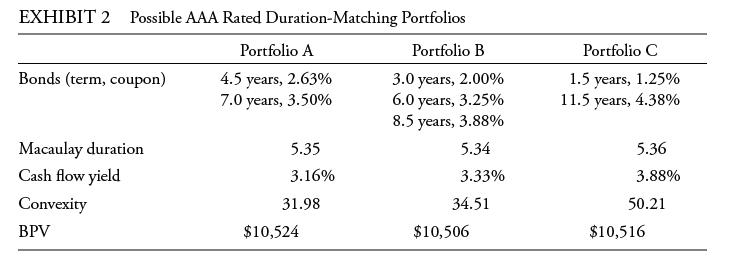

Which of Trey’s reasons for choosing bond mutual funds as an investment vehicle is correct?A. Reason 1B. Reason 2C. Reason 3Serena is a risk management specialist with Liability Protection Advisors. Trey, CFO of Kiest Manufacturing, enlists Serena’s help with three projects. The first project

The effects of a non-parallel shift in the yield curve on Strategy 2 can be reduced by:A. Minimizing the convexity of the bond portfolio.B. Maximizing the cash flow yield of the bond portfolio.C. Minimizing the difference between liability duration and bond-portfolio duration.Doug, the newly hired

Hui’s response to Doug’s question about the most efficient portfolio management strategy should be:A. Full replication.B. Active management.C. An enhanced indexing strategy.Doug, the newly hired chief financial officer for the City of Radford, asks the deputy financial manager, Hui, to prepare

Which portfolio structure should Hui recommend that would satisfy the school board member’s preference?A. Bullet portfolioB. Barbell portfolioC. Laddered portfolioDoug, the newly hired chief financial officer for the City of Radford, asks the deputy financial manager, Hui, to prepare an analysis

Chaopraya is an investment advisor for high-net-worth individuals. One of her clients, Schuylkill, plans to fund her grandson’s college education and considers two options:• Option 1: Contribute a lump sum of $300,000 in 10 years.• Option 2: Contribute four level annual payments of $76,500

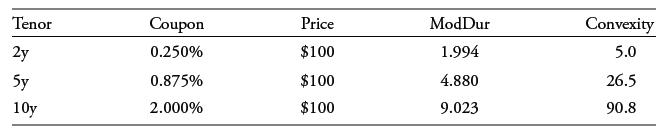

Consider two $50 million portfolios: Portfolio A is fully invested in the 5-year Treasury bond, and Portfolio B is an investment split between the 2-year (58.94%) and the 10-year (41.06%) bonds. The Portfolio B weights were chosen to (approximately) match the 5-year bond duration of 4.88. How will

Say a UK-based manager seeks to extend duration beyond an index by adding 10-year exposure. The manager considers either buying and holding a 10-year, 2.25% semi-annual coupon UK government bond priced at ₤93.947, with a corresponding yield-to-maturity of 2.9535%, or entering a new 10-year, GBP

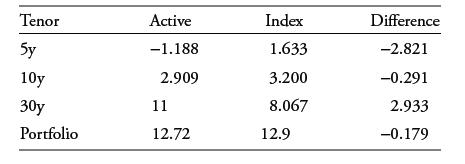

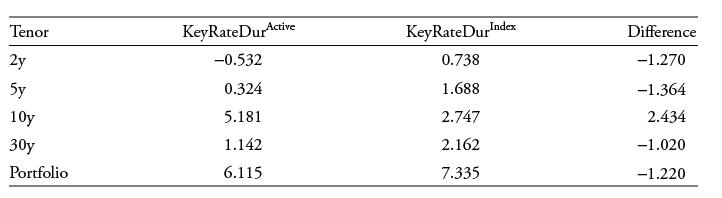

A fixed-income manager is presented with the following key rate duration summary of his actively managed bond portfolio versus an equally weighted index portfolio across 5-, 10-, and 30-year maturities:Assume the active manager has invested in the index bond portfolio and used only derivatives to

A fixed-income manager is considering a foreign currency fixed-income investment in a relatively high-yielding market, where she expects bear flattening to occur in the near future and her lower-yielding domestic yield curve to remain stable and upward-sloping. Under this scenario, which of the

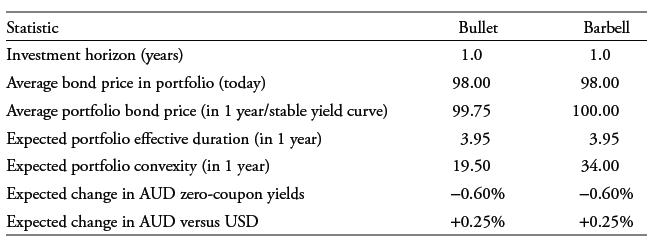

A US-based portfolio manager plans to invest in Australian zero-coupon bonds denominated in Australian dollars (AUD). He projects that over the next 12 months, the Australian zero-coupon yield curve will experience a downward parallel shift of 60 bps and that AUD will appreciate 0.25% against USD.

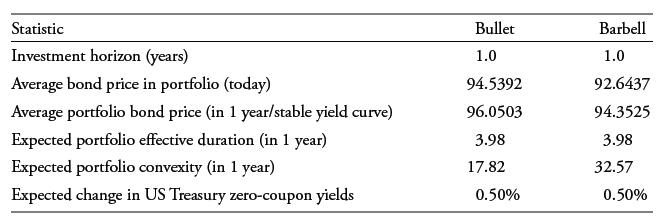

Assume a 1-year investment horizon for a portfolio manager considering US Treasury market strategies. The manager is considering two strategies to capitalize on an expected rise in US Treasury security zero-coupon yield levels of 50 bps in the next 12 months:1. A bullet portfolio fully invested in

The portfolio alternative with the highest modified duration is the:A. Bullet portfolio.B. Barbell portfolio.C. Equally weighted portfolio.A Sydney-based fixed-income portfolio manager is considering the following Commonwealth of Australia government bonds traded on the ASX (Australian Stock

The manager estimates that accelerated economic growth in Australia will increase the level of government yields-to-maturity by 50 bps. Under this scenario, which of the three portfolios experiences the smallest decline in market value?A. Bullet portfolioB. Barbell portfolioC. Equally weighted

In her market research, the manager learns that ASX 3-year and 10-year Treasury bond futures are the most liquid products for investors trading and hedging medium- to long-term Australian dollar (AUD) interest rates. Although neither contract matches the exact characteristics of the cash bonds of

An economic slowdown is expected to result in a 25 bp decline in Australian yield levels. Which portfolio alternative will experience the largest gain under this scenario?A. Bullet portfolioB. Barbell portfolioC. Equally weighted portfolioA Sydney-based fixed-income portfolio manager is considering

The portfolio alternative with the least exposure to convexity is the:A. bullet portfolio.B. barbell portfolio.C. equally weighted portfolio.A Sydney-based fixed-income portfolio manager is considering the following Commonwealth of Australia government bonds traded on the ASX (Australian Stock

The current butterfly spread for the Australian government yield curve based upon the manager’s portfolio choices is:A. 83 bps.B. 28 bps.C. −28 bps.A Sydney-based fixed-income portfolio manager is considering the following Commonwealth of Australia government bonds traded on the ASX (Australian

Which of the following statements best describes the forward rate bias?A. Investors tend to favor fixed-income investments in currencies that trade at a premium on a forward basis.B. Investors tend to hedge fixed-income investments in higher-yielding currencies given the potential for lower returns

Which of the following derivatives strategies would best offset the yield curve exposure difference between the active and index portfolios?A. Add a pay-fixed 10-year swap and long 2-year, 5-year, and 30-year bond futures positions to the active portfolio.B. Add a receive-fixed 30-year swap, a

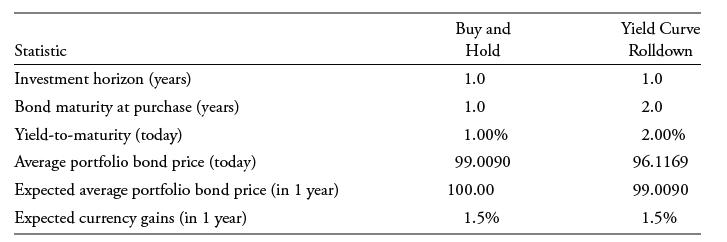

The rolldown returns over the 1-year investment horizon for the Buy-and-Hold and Yield Curve Rolldown portfolios are closest to:A. 1.00% for the Buy-and-Hold portfolio and 3.01% for the Yield Curve Rolldown portfolio, respectively.B. 0.991% for the Buy-and-Hold portfolio and 3.01% for the Yield

The total expected return over the 1-year investment horizon for the Buy-and-Hold and Yield Curve Rolldown portfolios are closest to:A. 2.515% for the Buy-and-Hold portfolio and 4.555% for the Yield Curve rolldown portfolio, respectively.B. 2.42% for the Buy-and-Hold portfolio and 4.51% for the

Which of the following statements best describes how the expected total return results would change if THB yields were to rise significantly over the investment horizon?A. Both the Buy-and-Hold and Yield Curve Rolldown expected portfolio returns would increase due to higher THB yields.B. Both the

Which of the following statements is true if yield levels increase by 50 bps?A. The active portfolio will outperform the index portfolio by approximately 61 bps.B. The index portfolio will outperform the active portfolio by approximately 61 bps.C. The index portfolio will outperform the active

Which of the following statements best characterizes how the active portfolio is positioned for yield curve changes relative to the index portfolio?A. The active portfolio is positioned to benefit from a bear steepening of the yield curve versus the benchmark portfolio.B. The active portfolio is

Which of the following would be expected to provide the most accurate modeling with respect to the observed term structure?A. CIR modelB. Ho–Lee modelC. Vasicek model

Which of the following investment alternatives includes an arbitrage opportunity?Bond A: The yield for a 3% annual coupon 10-year bond is 2.5% in New York City. The same bond sells for $104.376 per $100 face value in Chicago.Bond B: The yield for a 3% annual coupon 10-year bond is 3.2% in Hong Kong

The yield-to-maturity (“par rate”) for a benchmark one-year annual coupon bond is 2%, for a benchmark two-year annual coupon bond is 3%, and for a benchmark three-year annual coupon bond is 4%. A three-year, 5% annual coupon bond with the same risk and liquidity as the benchmarks is selling for

Which of the following statements about the Vasicek model is most accurate? It has:A. A single factor, the long rate.B. A single factor, the short rate.C. Two factors, the short rate and the long rate.

The CIR model:A. Assumes interest rates are not mean reverting.B. Has a drift term that differs from that of the Vasicek model.C. Assumes interest rate volatility increases with increases in the level of interest rates.

Which term structure model can be calibrated to closely fit an observed yield curve?A. The Ho–Lee modelB. The Vasicek modelC. The Cox–Ingersoll–Ross model

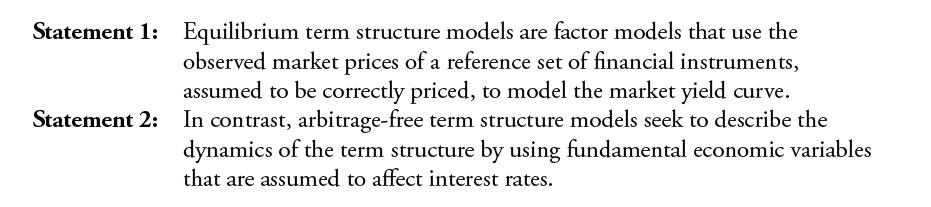

Keisha Jones is a junior analyst at Sparling Capital. Julie Anderson, a senior partner and Jones’s manager, meets with Jones to discuss interest rate models used for the firm’s fixed-income portfolio.Anderson begins the meeting by asking Jones to describe features of equilibrium and arbitrage-

Which of the following statements comparing the Ho–Lee and Kalotay–Williams– Fabozzi (KWF) equilibrium term structure models is correct?A. The Ho–Lee model assumes constant volatility, while the KWF model does not.B. The KWF model incorporates the possibility of negative rates, while the

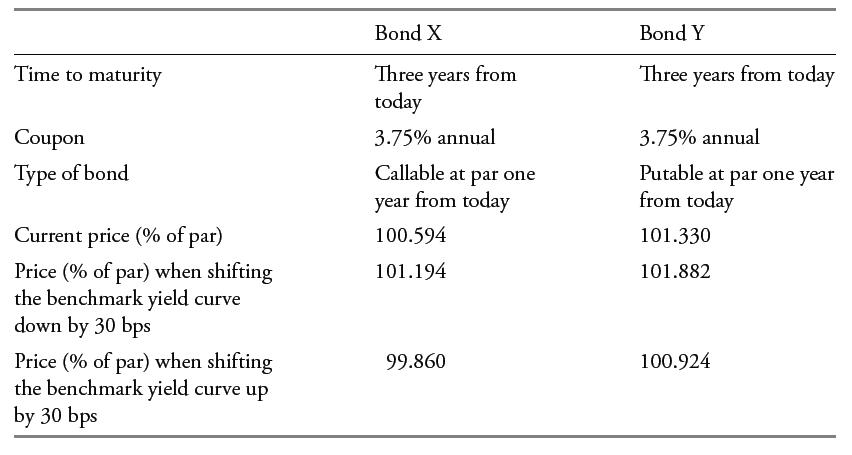

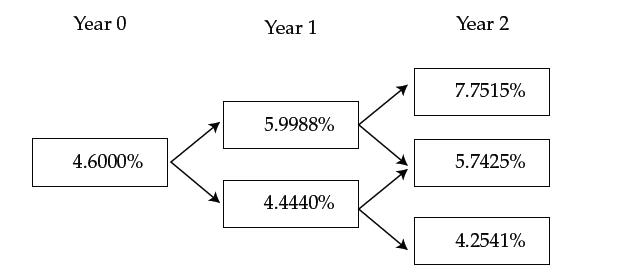

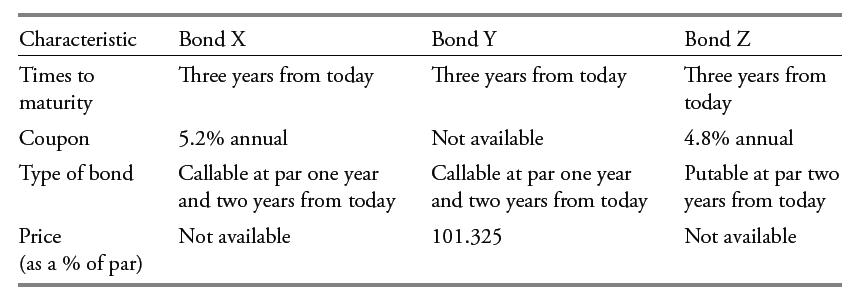

Erna Smith, a portfolio manager, has two fixed-rate bonds in her portfolio: a callable bond (Bond X) and a putable bond (Bond Y). She wants to examine the interest rate sensitivity of these two bonds to a parallel shift in the benchmark yield curve. Assuming an interest rate volatility of 10%, her

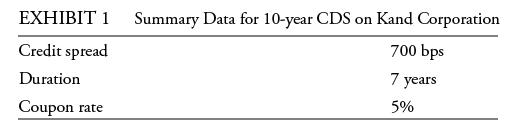

A three-year floating rate bond pays annual coupons of one-year reference rate (set in arrears) and is capped at 5.600%. The reference rate swap curve is as given in Exhibit 1 (i.e., the one-year, two-year, and three-year par yields are 2.500%, 3.000%, and 3.500%, respectively), and interest rate

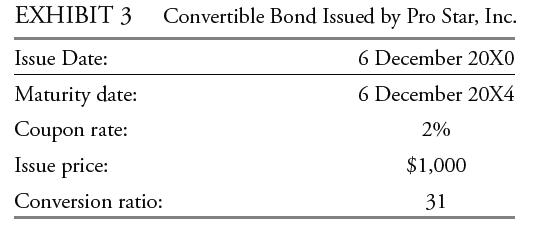

Nick Andrews, a fixed-income investment analyst, has been asked by his supervisor to prepare an analysis of the convertible bond issued by Heavy Element Inc., a chemical industry company, for presentation to the investment committee. Andrews has gathered the following data from the convertible

Investors in putable bonds most likely seek to take advantage of:A. Higher interest rates.B. Improvements in the issuer’s credit rating.C. Movements in the price of the issuer’s common stock.

George Cahill, a portfolio manager, has identified three five-year annual coupon bonds issued by a sovereign government. The three bonds have identical characteristics. The exceptions are that Bond A is an option-free bond; Bond B is callable at par two years and three years from today; and Bond C

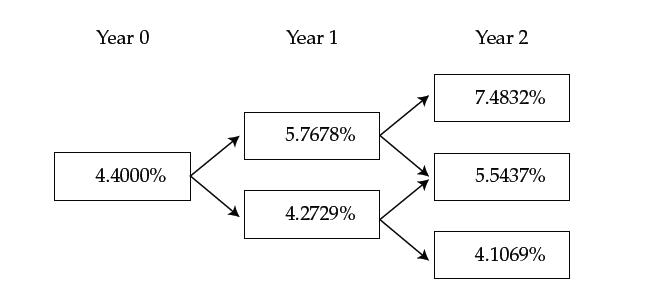

Return to the valuation of the Bermudan-style three-year 4.25% annual coupon bond putable at par one year and two years from now, as depicted in Exhibit 13. The one-year, two-year, and three-year par yields are 2.500%, 3.000%, and 3.500%, respectively, and the interest rate volatility is 10%.Assume

Robert Jourdan, a portfolio manager, has just valued a 7% annual coupon bond that was issued by a French company and has three years remaining until maturity. The bond is callable at par one year and two years from now. In his valuation, Jourdan used the yield curve based on the on-the-run French

Erna Smith, a portfolio manager, has two fixed-rate bonds in her portfolio: a callable bond (Bond X) and a putable bond (Bond Y). She wants to examine the interest rate sensitivity of these two bonds to a parallel shift in the benchmark yield curve. Assuming an interest rate volatility of 10%, her

A three-year floating-rate bond pays annual coupons of one-year reference rate (set in arrears) and is floored at 3.000%. The reference swap curve is as given in Exhibit 1 (i.e., the one-year, two-year, and three-year par yields are 2.500%, 3.000%, and 3.500%, respectively), and interest rate

Nick Andrews, a fixed-income investment analyst, has been asked by his supervisor to prepare an analysis of the convertible bond issued by Heavy Element Inc., a chemical industry company, for presentation to the investment committee. Andrews has gathered the following data from the convertible

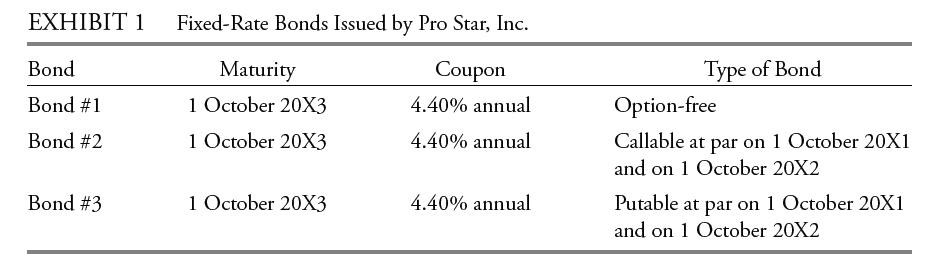

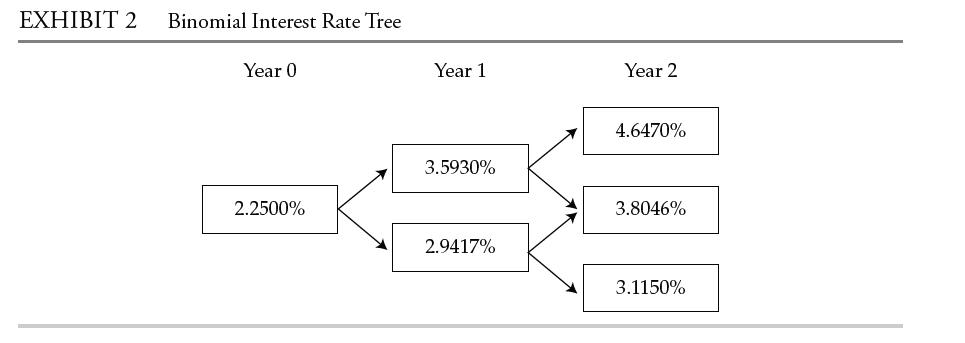

Samuel & Sons is a fixed-income specialty firm that offers advisory services to investment management companies. On 1 October 20X0, Steele Ferguson, a senior analyst at Samuel, is reviewing three fixed-rate bonds issued by a local firm, Pro Star, Inc. The three bonds, whose characteristics are

The conversion option in a convertible bond is a right held by:A. The issuer.B. The bondholders.C. The issuer and the bondholders jointly.

George Cahill, a portfolio manager, has identified three five-year annual coupon bonds issued by a sovereign government. The three bonds have identical characteristics. The exceptions are that Bond A is an option-free bond; Bond B is callable at par two years and three years from today; and Bond C

George Cahill, a portfolio manager, has identified three five-year annual coupon bonds issued by a sovereign government. The three bonds have identical characteristics. The exceptions are that Bond A is an option-free bond; Bond B is callable at par two years and three years from today; and Bond C

Erna Smith, a portfolio manager, has two fixed-rate bonds in her portfolio: a callable bond (Bond X) and a putable bond (Bond Y). She wants to examine the interest rate sensitivity of these two bonds to a parallel shift in the benchmark yield curve. Assuming an interest rate volatility of 10%, her

Robert Jourdan, a portfolio manager, has just valued a 7% annual coupon bond that was issued by a French company and has three years remaining until maturity. The bond is callable at par one year and two years from now. In his valuation, Jourdan used the yield curve based on the on-the-run French

Sidley Brown, a fixed-income associate at KMR Capital, is analyzing the effect of interest rate volatility on the values of callable and putable bonds issued by Weather Analytics (WA). WA is owned by the sovereign government, so its bonds are considered default free. Brown is currently looking at

Return to the valuation of the Bermudan-style three-year 4.25% annual coupon bond putable at par one year and two years from now, as depicted in Exhibit 13. The one-year, two-year, and three-year par yields are 2.500%, 3.000%, and 3.500%, respectively, and the interest rate volatility is 10%.Assume

Return to the valuation of the Bermudan-style three-year 4.25% annual coupon bond callable at par one year and two years from now as depicted in Exhibit 12. The one-year, two-year, and three-year par yields are 2.500%, 3.000%, and 3.500%, respectively, and the interest rate volatility is 10%.Assume

An investor buys $10 million of five-year protection, and the CDS contract has a duration of four years. The company’s credit spread was originally 500 bps and widens to 800 bps.Does the investor (credit protection buyer) benefit or lose from the change in credit spread?

An analyst is evaluating two US apparel companies: Atelier and Trapp. Atelier is a large company that focuses on high-end apparel brands. It is profitable despite a high cost structure. Trapp is smaller and less profitable than Atelier. Trapp focuses on less expensive brands and strives to keep

An investor owns some intermediate-term bonds issued by a company and has become concerned about the risk of a near-term default, although he is not very concerned about a default in the long term. The company’s two-year CDS currently trades at 350 bps, and the four-year CDS is at 600

An investor wants to be long the credit risk of a given company. The company’s bond currently yields 6% and matures in five years. A comparable five-year CDS contract has a credit spread of 3.25%. The investor can borrow at Libor, which is currently 2.5%.Calculate the bond’s credit spread.

An investor believes that a company will undergo a leveraged buyout (LBO) transaction, whereby it will issue large amounts of debt and use the proceeds to repurchase all of the publicly traded equity, leaving the company owned by management and a few insiders.Why might the CDS spread change?

On 1 January 20X2, Deem Advisors purchased a $10 million six-year senior unsecured bond issued by UNAB Corporation. Six months later (1 July 20X2), concerned about the portfolio’s credit exposure to UNAB, Doris Morrison, the chief investment officer at Deem Advisors, buys $10 million protection

A French company files for bankruptcy, triggering various CDS contracts. It has two series of senior bonds outstanding: Bond A trades at 30% of par, and Bond B trades at 40% of par. Investor X owns €10 million of Bond A and owns €10 million of CDS protection. Investor Y owns €10 million of

Assume that an investor sells $500 million of protection using the CDX IG index, which has 125 reference entities. Concerned about the creditworthiness of a few of the components, the investor hedges a portion of the credit risk in each. For Company A, he purchases $3 million of single-name CDS

Assume that a company’s hazard rate is a constant 8% per year, or 2% per quarter. An investor sells five-year CDS protection on the company with the premiums paid quarterly over the next five years.What is the conditional probability of survival for the second quarter?

A company’s 5-year CDS trades at a credit spread of 300 bps, and its 10-year CDS trades at a credit spread of 500 bps.The company’s 10-year spread is unchanged, but the 5-year spread widens by 500 bps. Describe the implication of this change in the credit curve.

Imagine an investor sold five-year protection on an investment-grade company and had to pay a 2% upfront premium to the buyer of protection. Assume the duration of the CDS to be four years. What are the company’s credit spreads and the price of the CDS per 100 par?

An investor buys $10 million of five-year protection, and the CDS contract has a duration of four years. The company’s credit spread was originally 500 bps and widens to 800 bps.Estimate the CDS price change and estimated profit to the investor.

An investor owns some intermediate-term bonds issued by a company and has become concerned about the risk of a near-term default, although he is not very concerned about a default in the long term. The company’s two-year CDS currently trades at 350 bps, and the four-year CDS is at 600 bps.Explain

An investor believes that a company will undergo a leveraged buyout (LBO) transaction, whereby it will issue large amounts of debt and use the proceeds to repurchase all of the publicly traded equity, leaving the company owned by management and a few insiders.What equity-versus-credit trade might

An investor wants to be long the credit risk of a given company. The company’s bond currently yields 6% and matures in five years. A comparable five-year CDS contract has a credit spread of 3.25%. The investor can borrow at Libor, which is currently 2.5%.Identify a basis trade that would exploit

Chaopraya is an investment advisor for high-net-worth individuals. One of her clients, Schuylkill, plans to fund her grandson’s college education and considers two options:• Option 1: Contribute a lump sum of $300,000 in 10 years.• Option 2: Contribute four level annual payments of $76,500

Portfolio convexity is a second-order effect that causes the value of a portfolio to respond to a change in yields-to-maturity in a non-linear manner. Which of the following best describes the effect of positive portfolio convexity for a given change in yield-to-maturity?a. Convexity causes a

An investment manager who pursues the cash-based yield curve strategies described in Exhibit 5 faces an inverted yield curve (with a decline in long-term yields-to-maturity and a sharp increase in short-term yields-to-maturity) instead. Which of the following is the least likely portfolio outcome

Consider a $50 million Treasury portfolio equally weighted between 2-, 5-, and 10-year Treasuries using parameters from the prior example as the index, and an active portfolio with 20% each in 2- and 5-year Treasuries and the remaining 60% invested in 10-year Treasuries. Which of the following is

Consider a Treasury portfolio consisting of a $124.6 million long 2-year zero-coupon Treasury with an annualized 2% yield-to-maturity and a short $25.41 million 10-year zero-coupon bond with a 4% yield-to-maturity. Calculate the net portfolio duration and solve for the first-order change in

An investment manager is considering an incremental position in a callable, putable, or option-free bond with otherwise comparable characteristics. If she expects a downward parallel shift in the yield curve, it would be most profitable to be:a. Long a callable bond.b. Short a putable bond.c. Long

A parallel upward shift in the yield curve is expected. Which of the following would be the best option strategy?a. Long a receiver swaptionb. Short a payer swaptionc. Long a put option on a bond futures contract

Given a parallel shift upwards in the yield curve, what is the most likely ordering in terms of expected decline in value—from least to most—for otherwise comparable bonds? Assume that the embedded options are deep out-of-the-money.a. Callable bond, option-free bond, putable bondb. Putable

Consider the case of a portfolio manager examining a cross-currency carry trade between US dollar (USD) and Mexican peso (MXN) money market rates. The manager is contemplating borrowing in USD for one year and investing in 90-day Mexican treasury bills, rolling them over at maturity for the next 12

An analyst manages an active fixed-income fund that is benchmarked to the Bloomberg Barclays US Treasury Index. This index of US government bonds currently has a modified portfolio duration of 7.25 and an average maturity of 8.5 years. The yield curve is upward-sloping and expected to remain

A Dutch investor considering a 5-year EUR government bond purchase expects yields-to-maturity to decline by 25 bps in the next six months. Which of the following statements about the rolldown return is correct?A. The rolldown return equals the difference between the price of the 5-year bond and

An investment manager is considering decreasing portfolio duration versus a benchmark index given her expectations of an upward parallel shift in the yield curve. If she has a choice between a callable, putable, or option-free bond with otherwise comparable characteristics, the most profitable

An active fixed-income manager holds a portfolio of commercial and residential mortgage-backed securities that tracks the Bloomberg Barclays US Mortgage-Backed Securities Index. Which of the following choices is the most relevant portfolio statistic for evaluating the first-order change in his

An active fund trader seeks to capitalize on an expected steepening of the current upward- sloping yield curve using option-based fixed-income instruments. Which of the following portfolio positioning strategies best positions her to gain if her interest rate view is realized?A. Sell a 30-year

An active investor enters a duration-neutral yield curve flattening trade that combines 2-year and 10-year Treasury positions. Under which of the following yield curve scenarios would you expect the investor to realize the greatest portfolio gain?A. Bear flatteningB. Bull flatteningC. Yield curve

Which of the following is the best measure of credit risk?A. The expected lossB. The severity of lossC. The probability of default

In the event of bankruptcy, claims at the same level of the capital structure are:A. On an equal footing, regardless of size, maturity, or time outstanding.B. Paid in the order of maturity from shortest to longest, regardless of size or time outstanding.C. Paid on a first-in, first-out (FIFO) basis

Using both Moody’s and S&P ratings, which of the following pairs of ratings is considered high yield, also known as “below investment grade,” “speculative grade,” or “junk”?A. Baa1/BBB−B. B3/CCC+C. Baa3/BB+

Heavily regulated monopoly companies, such as utilities, often carry high debt loads. Which of the following statements about such companies is most accurate?A. Regulators require them to carry high debt loads.B. They generate strong and stable cash flows, enabling them to support high levels of

Why should credit analysts be concerned if a company’s stock trades below book value?A. It means the company is probably going bankrupt.B. It means the company will probably incur lots of debt to buy back its undervalued stock.C. It’s a signal that the company’s asset value on its balance

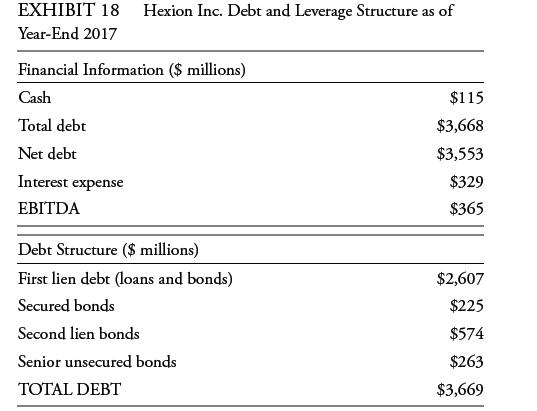

Hexion Inc. is a specialty chemical company. It has a complicated, high-yield debt structure, consisting of first lien debt (loans and bonds), secured bonds, second lien bonds, and senior unsecured debt, due to a series of mergers as well as a leveraged buyout in 2005. Exhibit 18 is a simplified

Exhibit 21 shows several key sovereign statistics for Portugal.Based on those calculations, as well as other data from Exhibit 21, what can you say about Portugal’s credit trend? EXHIBIT 21 Key Sovereign Statistics for Portugal € (billions), except where noted Nominal GDP Population

If investors become increasingly worried about the economy—say, as shown by declining stock prices—what is the most likely impact on credit spreads?A. There will be no change to credit spreads. They aren’t affected by equity markets.B. Narrower spreads will occur. Investors will move out of

Stedsmart Ltd and Fignermo Ltd are alike with respect to financial and operating characteristics, except that Stedsmart Ltd has less publicly traded debt outstanding than Fignermo Ltd. Stedsmart Ltd is most likely to have:A. No market liquidity risk.B. Lower market liquidity risk.C. Higher market

Which of the following is not credit or credit-related risk?A. Default riskB. Interest rate riskC. Downgrade or credit migration risk

What is the difference between an issuer rating and an issue rating?A. The issuer rating applies to all of an issuer’s bonds, whereas the issue rating considers a bond’s seniority ranking.B. The issuer rating is an assessment of an issuer’s overall creditworthiness, whereas the issue rating

XYZ Corp. manufactures a commodity product in a highly competitive industry in which no company has significant market share and where there are low barriers to entry. Which of the following best describes XYZ’s ability to take on substantial debt?A. Its ability is very limited because companies

If management is of questionable character, how can investors incorporate this assessment into their credit analysis and investment decisions?A. They can choose not to invest based on the increased credit risk.B. They can insist on getting collateral (security) and/or demand a higher return.C. They

In the event of default, the recovery rate of which of the following bonds would most likely be the highest?A. First mortgage debtB. Senior unsecured debtC. Junior subordinate debt

Based on the practice of notching by the rating agencies, a subordinated bond from a company with an issuer rating of BB would likely carry what rating?A. B+B. BBC. BBB−

During bankruptcy proceedings of a firm, the priority of claims was not strictly adhered to. Which of the following is the least likely explanation for this outcome?A. Senior creditors compromised.B. The value of secured assets was less than the amount of the claims.C. A judge’s order resulted in

The fixed-income portfolio manager you work with asked you why a bond from an issuer you cover didn’t rise in price when it was upgraded by Fitch from B+ to BB. Which of the following is the most likely explanation?A. Bond prices never react to rating changes.B. The bond doesn’t trade often, so

A fixed-income analyst is least likely to conduct an independent analysis of credit risk because credit rating agencies:A. May at times mis-rate issues.B. Often lag the market in pricing credit risk.C. Cannot foresee future debt-financed acquisitions.

Amalgamated Corp. and Widget Corp. each have bonds outstanding with similar coupons and maturity dates. Both bonds are rated B2, B−, and B by Moody’s, S&P, and Fitch, respectively. The bonds, however, trade at very different prices—the Amalgamated bond trades at €89, whereas the Widget bond

Showing 1600 - 1700

of 2084

First

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

Step by Step Answers