New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

financial reporting and analysis

Financial Reporting And Analysis 8th Edition Lawrence Revsine, Daniel Collins, Bruce Johnson, Fred Mittelstaedt, Leonard Soffer - Solutions

The stockholders’ equity section of Peter Corporation’s balance sheet at December 31, 20X1, follows:Common stock ($10 par value); authorized .......................... 1,000,000shares, issued and outstanding 900,000 shares ............... $ 9,000,000Additional paid-in capital

Cephalon Inc. issued $750 million of zero-coupon convertible notes. Because the notes were issued at par, meaning that Cephalon received $750 million cash for the notes, they have a zero yield-to-maturity. Settlement in cash upon conversion is not permitted. Here is what Cephalon said about the

Massey Coal (a fictional company) just issued $50 million of convertible notes. Each note has a $1,000 face value, has a stated interest rate of 2%, and matures in five years from the issue date. Investors have the option of holding each note to maturity or converting the note into 100 shares of

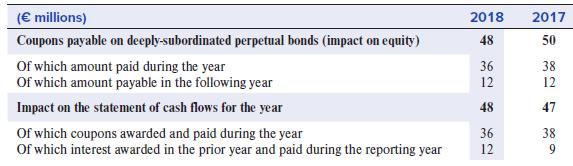

Groupe Casino is a French multinational company that operates more than 9,000 multiformat retail stores—hypermarkets, supermarkets, discount stores, convenience stores, and restaurants— throughout the world. It has two series of perpetual bonds described below in excerpts from its 2018

Keystone Enterprises (a fictional company) just announced record 20X1 EPS of $5.00, up $0.25 from last year. This is the 10th consecutive year that the company has increased its EPS, an enviable record. Unfortunately, management fears that this string of EPS increases is about to be broken.

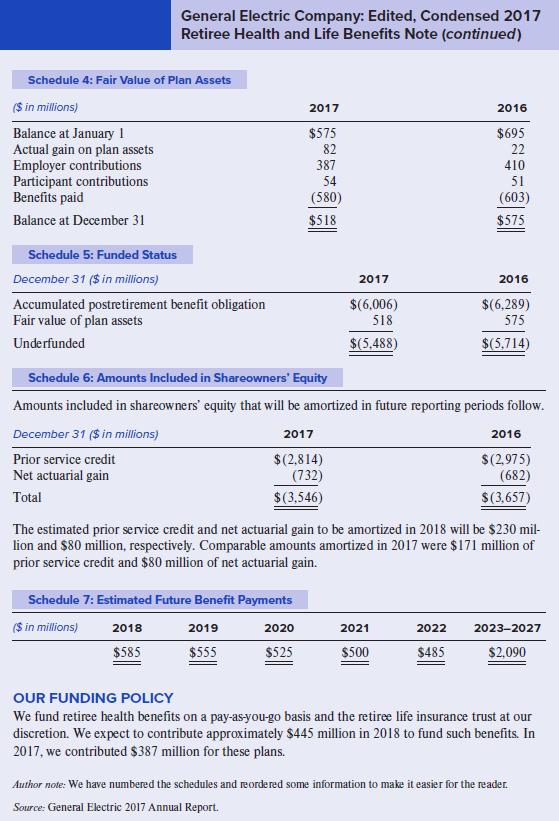

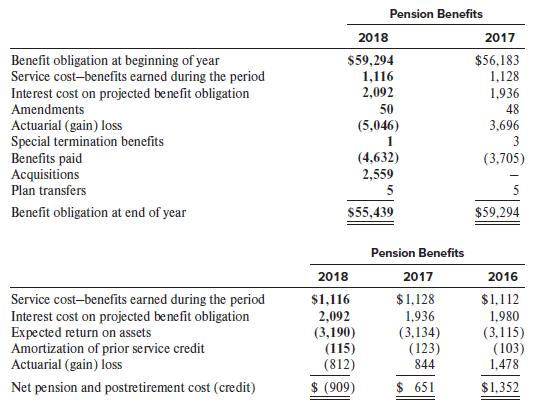

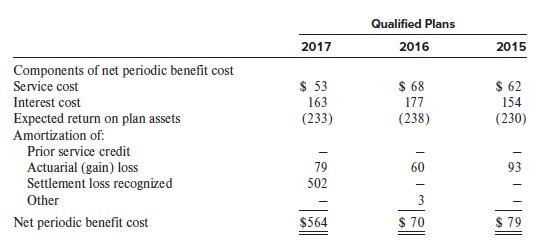

Refer to the 2017 General Electric Retiree Health and Life Benefits disclosure appearing in Exhibit 15.9.Required:1. Reconstruct the journal entries that GE would have made in 2017 to record the effects of its retiree health and life benefits plans. The curtailment loss of $4 should be treated as a

Bortles Corporation’s U.S. operations have been in “steady state” for several years, whereby its pre-tax income has been constant (at $400 million each year) and its originating temporary differences and reversing temporary differences exactly offset. At December 31, 2016, Bortles reported a

In Figland Company’s first year of operations (20X1), the company had pre-tax book income of $500,000 and taxable income of $800,000. Figland’s only temporary difference is for accrued product warranty costs, which are expected to be paid as follows:20X2 .................. $100,00020X3

On December 31, 20X1, Ball Company leased a machine from Cook for a 10 year period, expiring December 30, 20Y1. Annual payments of $100,000 are due on December 31. The first payment was made on December 31, 20X1, and the second payment was made on December 31, 20X2. The present value at the

On January 1, 20X1, Bare Trees Company signed a three-year noncancelable lease with Dreams Inc. The lease calls for three payments of $62,258.09 to be made at each year end. The lease payments include $3,000 of executory costs related to service. The lease is nonrenewable and has no bargain

On December 31, 20X1, Roe Company leased a machine from Colt for a five-year period. Equal annual payments under the lease are $105,000 (including $5,000 annual executory costs for servicing) and are due on December 31 of each year. The first payment was made on December 31, 20X1, and the second

Webb Company has outstanding a 7% annual, 10-year, $100,000 face value bond that it had issued several years ago. It originally sold the bond to yield 6% annual interest. Webb uses the effective interest rate method to amortize the bond premium. On June 30, 20X1, the outstanding bond’s carrying

On July 1, 20X1, McVay Corporation issued $15 million of 10-year bonds with an 8% stated interest rate. The bonds pay interest semiannually on June 30 and December 31 of each year. The market rate of interest on July 1, 20X1, for bonds of this type was 10%. McVay closes its books on December

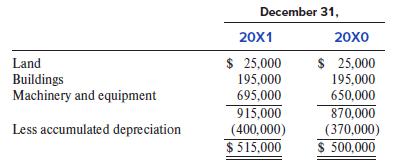

Weir Company (a fictional company) uses straight-line depreciation for its property, plant, and equipment, which, stated at cost, consisted of the following:Weir’s depreciation expenses for 20X1 and 20X0 were $55,000 and $50,000, respectively.Required:What amount was debited to accumulated

On January 2, 20X1, Criswell Acres purchased from Mifflinburg Farm Supply a new tractor that had a cash selling price of $109,837. As payment, Criswell gave Mifflinburg Farm Supply $25,000 in cash and a $100,000, five-year note that provided for annual interest payments at 6%. At the time of the

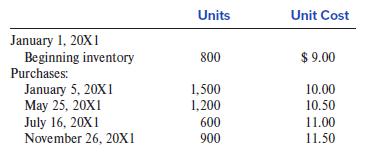

Frate Company was formed on January 1, 20X1. The following information is available from Frate’s inventory records for Product Ply:A physical inventory on December 31, 20X1, shows 1,600 units on hand.Required:Prepare schedules to compute the ending inventory at December 31, 20X1, and cost of

During your audit of Patti Company’s ending inventory at December 31, 20X1, you find the following inventory accounting errors:a. Goods in Patti’s warehouse on consignment from Valley, Inc., were included in Patti’s ending inventory.b. On December 31, 20X1, Patti received $4,700 worth of

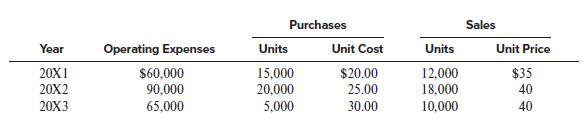

Sirotka Retail Company began doing business in 20X1. The following information pertains to its first three years of operation:Assume the following:• The income tax rate is 21%.• Purchase and sale prices change only at the beginning of the year.• Sirotka uses the LIFO cost flow assumption.•

On January 2, 20X0, Half, Inc., purchased a manufacturing machine for $864,000. The machine has an eight-year estimated life and a $144,000 estimated salvage value. Half expects to manufacture 1,800,000 units over the machine’s life. During 20X1, Half manufactured 300,000 units.Required:For each

On April 1, 20X1, Mills Company acquired equipment for $125,000. The estimated useful life is six years, and the estimated residual value is $5,000. Mills estimates that the equipment can produce 25,000 units of product. During 20X1 and 20X2, respectively, 3,000 and 4,200 units were produced. Mills

Four years ago Omega Technology, Inc., acquired a machine to use in its computer chip manufacturing operations at a cost of $35,000,000. The firm expected the machine to have a sevenyear useful life and a zero salvage value. The company has been using straight-line depreciation for the asset. Due

IceCap Hotels operates a series of northern European hotels and reports under IFRS. On June 30, 20X0, IceCap purchased a hotel for €2,100,000. IceCap reports hotel values on the balance sheet under Property, plant, and equipment. The estimated useful life of the hotel is 30 years from the date of

On January 1, 20X1, Fleetwood Inc. issued bonds with a face amount of $25 million and a stated interest rate of 8%. The bonds mature in 10 years and pay interest semiannually on June 30 and December 31 of each year. The market rate of interest on January 1, 20X1, for bonds of this type was 6%.

On January 1, 20X1, Newell Manufacturing purchased a new drill press that had a cash purchase price of $6,340. Newell decided instead to pay on an installment basis. The installment contract calls for four annual payments of $2,000 each beginning in one year. Newell was not required to make an

On February 1, 20X1, Davis Corporation issued 12%, $1,000,000 par, 10-year bonds for $1,117,000. Davis reacquired all of these bonds at 102% of par, plus accrued interest, on May 1, 20X3, and retired them. The unamortized bond premium on that date was $78,000. Required:Before income taxes,

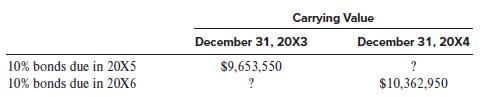

Rumours, Inc. issued $10 million, 10% coupon bonds on January 1, 20X1, due on December 31, 20X5. The prevailing market interest rate on January 1, 20X1, was 12%, and the bonds pay interest on June 30 and December 31 of each year.On January 1, 20X2, Rumours issued $10 million, 10% coupon bonds due

In its long-term liabilities section of its balance sheet at December 31, 20X1, Columbo Company reports a long-term operating lease liability of $82,004, net of the current portion of $13,327. Columbo makes $20,000 lease payments on December 31, 20X2, December 31, 20X3, and December 31, 20X4.

Mason Company has a machine with a cost and fair value of $100,000. On January 1, 20X1, it leases the machine for a 10-year period to Drake Company. The machine has a 12-year expected economic life. Payments are received at the beginning of each year. The machine is expected to have a $10,000

East Company leased a new machine from North Company on May 1, 20X1, under a lease with the following information:Lease term ............................................................................................. 10 yearsAnnual rental payable at beginning of each lease year

On January 1, 20X1, Seven Wonders Inc. signed a five-year noncancelable lease with Moss Company. The lease calls for five payments of $277,409.44 to be made at the end of each year. The leased asset has a fair value of $1,200,000 on January 1, 20X1. Seven Wonders cannot renew the lease, there is no

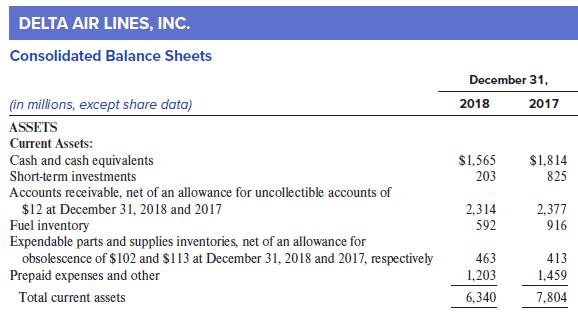

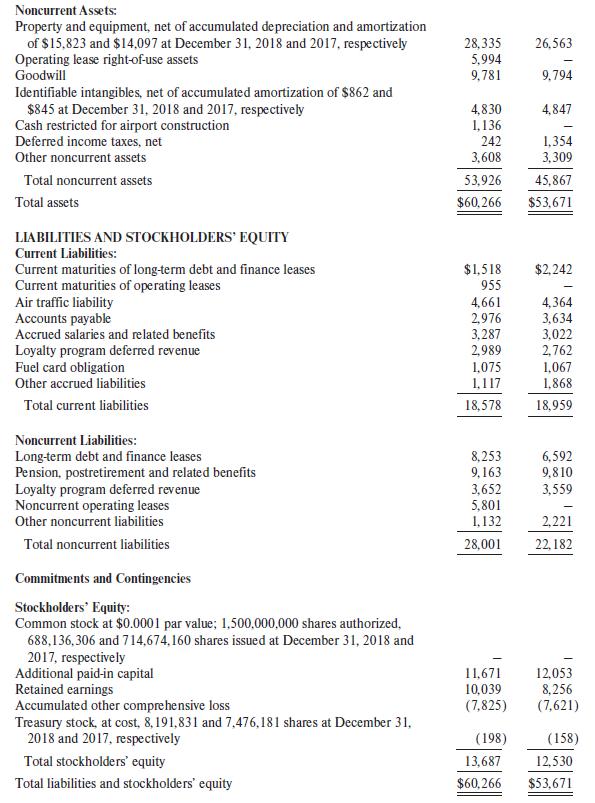

Delta Air Lines adopted the provisions of ASC Topic 842 using the optional alternative transition method in which a company makes a cumulative adjustment to the opening balance of retained earnings in the period of adoption instead of to the first comparative year reported. Presented below is

On January 1, 20X1, Bill Inc. leases manufacturing equipment from Beatrix Corporation. The lease covers seven years and requires annual lease payments of $51,000, beginning on January 1, 20X1. The unguaranteed residual value at the end of seven years is $150,000. On January 1, 20X1, the equipment

On January 1, 20X1, Beard Company purchased a machine for $620,000. The machine is expected to have a 10-year life, with no salvage value, and will be depreciated by the straightline method. On January 1, 20X1, it leased the machine to Child Company for a 3-year period at an annual rental of

Benedict Company leased equipment to Mark Inc. on January 1, 20X1. The lease is for an eight-year period, expiring December 31, 20X8. The first of eight equal annual payments of $600,000 was made on January 1, 20X1. Benedict had purchased the equipment on December 29, 20X0, for $3,200,000. The

On January 1, 20X1, Trask Co. signs an agreement to lease office equipment from Coleman Inc. for three years with payments of $193,357 beginning December 31, 20X1. The equipment’s fair value is $500,000 with an expected useful life of four years. At the end of three years, the equipment is

On December 31, 20X1, Thomas Henley, financial vice president of Kingston Corporation, signed a noncancelable three-year lease for an excavator. The lease calls for annual payments of $41,635 per year due at the end of each of the next three years. The leased equipment’s expected economic life is

On July 1, 20X1, Burgundy Studios leases camera equipment from Corningstone Corporation. Corningstone had to make significant changes to the equipment to meet Burgundy’s needs, and it would be significantly costly to modify the equipment for alternative lessees. The lease covers eight years and

On December 31, 20X1, Day Company leased a new machine from Parr with the following pertinent information:Lease term ................................................................................................................... 5 yearsAnnual rental payable on December 31 (beginning December

On January 1, 20X1, Railcar Leasing Inc. (the lessor) purchased 10 used boxcars from Railroad Equipment Consolidators at a price of $8,749,520. Railcar leased the boxcars to the Reading Railroad Company (the lessee) on the same date. The lease is for eight years and calls for eight annual payments

On October 1, 20X1, Vaughn, Inc., leased a machine from Fell Leasing Company for five years. The lease requires five annual payments of $10,000 beginning September 30, 20X2. Vaughn’s incremental borrowing rate is 11%, and it uses a calendar year for reporting purposes. The machine has a 12-year

Refer to the information in P13–10. Assume that at the commencement of the lease, collectibility of the payments is not probable and the lessor uses the straight-line depreciation method.Required:1. Prepare the necessary journal entries for Railcar for 20X1 and 20X2 under the lease. You do not

On January 1, 20X1, Babson, Inc., leased two automobiles for executive use. The lease requires Babson to make five annual payments of $13,000, beginning January 1, 20X1. At the end of the lease term on December 31, 20X5, Babson guarantees that the residual value of the automobiles will total

Moore Company sells and leases its computers. Moore’s cost and sales price per machine are $1,200 and $3,000, respectively. At the end of three years, the expected residual value is $400, which is guaranteed by the lessee. Moore leases 20 of these machines to Mitchum Co. on September 1, 20X1.

Assume that on January 1, 20X1, Trans Global Airlines leases two used Boeing 737s from Aircraft Lessors Inc. The eight-year lease calls for payments of $10,000,000 at each year end. On January 1, 20X1, the Boeing 737s have a total fair value of $60,000,000 and a remaining useful life of 11 years.

On December 31, 20X1, Lane, Inc., sold equipment to Nolte and simultaneously leased it back for 12 years. Pertinent information at this date is as follows:Sales price (received in cash) ................. $480,000Carrying amount ..................................... $360,000Estimated remaining

On January 1, 20X1, Overseas Leasing Inc. (the lessor) purchased five used oil tankers from Seven Seas Shipping Company at a price of $99,817,750. Overseas immediately leased the oil tankers to Pacific Ocean Oil Company (the lessee) on the same date. The lease calls for five annual payments of

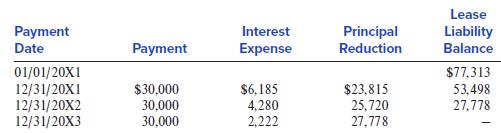

Mickelson reports on a calendar-year basis. On January 1, 20X1, Mickelson Corporation enters into a three-year lease with annual payments of $30,000. The first payment will be due on December 31, 20X1. The present value of the payments at 8% is $77,313. If the lease is classified as a finance

On January 1, 20X1, Draper Inc. signed a five-year noncancelable lease with Thornhill Company for custom-made equipment. The lease calls for five payments of $161,364.70 to be made at the beginning of each year. The leased asset has a fair value of $900,000 on January 1, 20X1. There is no bargain

On January 1, 20X1, Merchant Co. sold a tractor to Swanson Inc. and simultaneously leased it back for five years. The tractor’s fair value is $300,000, but its carrying value on Merchant’s books prior to the transaction was $200,000. The tractor has a seven-year remaining estimated useful life,

On January 1, 20X1, Walker, Inc., signs a 5-year lease for two floors of a 20-floor building. The building has an expected remaining life of 20 years. The space is available immediately, and Walker agrees to make annual payments of $325,000 on December 31 of each year. The lease contains no renewal

On October 1, 20X1, Brady Consulting leases unmodified equipment from Damon Corporation. The lease covers four years and requires lease payments of $73,046, beginning on September 30, 20X2. The unguaranteed residual value is $200,000. On October 1, 20X1, the equipment has an approximate fair value

On January 1, 20X1, Dwyer Company leases space for a donut shop. The lease is for five years with payments to be made at the beginning of each year. The lease calls for Dwyer to pay $10,000 on January 1, 20X1; $11,000 on January 1, 20X2; $12,500 on January 1, 20X3; $14,000 on January 1, 20X4; and

On January 1, 20X1, Bonduris Company leases warehouse space in Oakland, CA. The lease is for six years with payments to be made at the beginning of each year. The lease calls for Bonduris to pay $15,000 on January 1, 20X1. The lease calls for subsequent lease payments to increase 10% per year. For

On January 2, 20X1, Allen Company purchased a machine for $70,000. This machine has a five-year useful life, has a residual value of $10,000, and is depreciated using the straight-line method for financial statement purposes. For tax purposes, depreciation expense was $25,000 in 20X1 and $20,000 in

Moss Inc. follows GAAP for financial reporting purposes and appropriately uses the installment method of accounting for income tax purposes. It reported $250,000 of pre-tax income under GAAP, but it will report the corresponding taxable income in the following years. The enacted tax rate is

In its 20X1 income statement, Tow Inc. reported proceeds from an officer’s life insurance policy of $90,000 and depreciation of $250,000. Tow was the owner and beneficiary of the life insurance on its officer. Tow deducted depreciation of $370,000 in its 20X1 income tax return. The tax rate is

The following information pertains to Ramesh Company for 20X1:Book income before income taxes .................... $106,000Income tax expense ................................................. 27,300Income taxes due for this year ............................... 16,800Statutory income tax rate

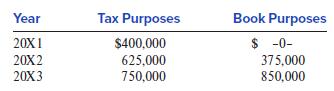

Mill Company began operations on January 1, 20X1, and recognized income from construction- type contracts under different methods for tax purposes and financial reporting purposes. Information concerning income recognition under each method is as follows:Required:Assume the income tax rate is 21%

For financial statement reporting, Lexington Corporation recognizes royalty income according to GAAP. However, royalties are taxed when collected. At December 31, 20X0, deferred royalty income of $400,000 was included in Lexington’s balance sheet. All of these royalties had been collected in

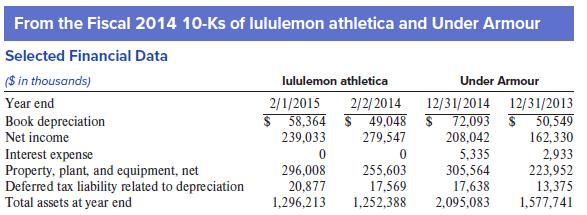

lululemon athletica and Under Armour are both in the athletic apparel business. But the two companies’ depreciation methods differ. The following explanations were excerpted from the two companies’ fiscal 2014 financial statements:lululemon athleticaProperty and Equipment Property and equipment

For the year ended December 31, 20X1, Tyre Company reported pre-tax financial statement income of $750,000. Its taxable income was $650,000. The difference was due to the use of accelerated depreciation for income tax purposes and straight-line for financial reporting. Tyre’s income tax rate is

Nelson Inc. purchased machinery at the beginning of 20X1 for $90,000. Management used the straight-line method to depreciate the cost for financial reporting purposes and the sum-of-theyears’ digits method to depreciate the cost for tax purposes. The life of the machinery was estimated to be

Dunn Company’s 20X1 income statement reported $90,000 income before provision for income taxes. To aid in the computation of the provision for federal income taxes, the following 20X1 data are provided:Rent received in advance .....................................................................

Metge Corporation’s worksheet for calculating taxable income for 20X1 follows:($ in thousands)20X1Pre-tax income$1,000Permanent differences:Goodwill impairment400Interest on municipal bonds(200)Temporary differences:Depreciation(800)Warranty costs400Rent received in advance600Taxable

Kent Inc.’s reconciliation between financial statement and taxable income for 20X1 follows:Pre-tax financial income ........................................ $150,000Permanent difference ............................................... (12,000)

On January 1, 20X1, the Dolan Company purchased a new office building in Las Vegas for $6,100,000, which it holds for rentals and capital appreciation. Dolan estimated the building would have a useful life of 25 years and a residual value of $1,100,000. Dolan uses straight-line depreciation for

West Corporation leased a building and received the $36,000 annual rental payment on July 15, 20X1. The beginning of the lease period was August 1, 20X1. Rental income is taxable when received. West had no other permanent or temporary differences. West’s tax rate is 21%. It determined that no

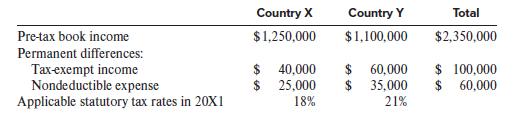

Bryan Trucking Corporation began business on January 1, 20X1, and consists of the parent entity, domiciled and operating in Country X, and a subsidiary operating in Country Y. Bryan is required, as a listed company in Country X, to prepare financial statements using IFRS. Bryan is also listed on

Black Company, organized on January 2, 20X1, had pre-tax accounting income of $500,000 and taxable income of $800,000 for the year ended December 31, 20X1. The only temporary difference is accrued product warranty costs, which are expected to be paid as follows:20X2 ..........................

Mozart Inc.’s $98,000 taxable income for 20X1 will be taxed at the 21% corporate tax rate. For tax purposes, its depreciation expense exceeded the depreciation used for financial reporting purposes by $27,000. Mozart has $45,000 of purchased goodwill on its books; during 20X1, the company

Quinn Company reported a net deferred tax asset of $6,300 in its December 31, 20X0, balance sheet. For 20X1, Quinn reported pre-tax financial statement income of $300,000. Temporary differences of $100,000 resulted in taxable income of $200,000 for 20X1. At December 31, 20X1, Quinn had net

In 20X1, Phillips Company reported $10,000,000 of pre-tax book income and also had $10,000,000 of taxable income. It incurred a $1,000,000 book expense that it deducted on its tax return. Assuming a 21% tax rate, this deduction results in a $210,000 tax benefit. The tax law was unclear at that time

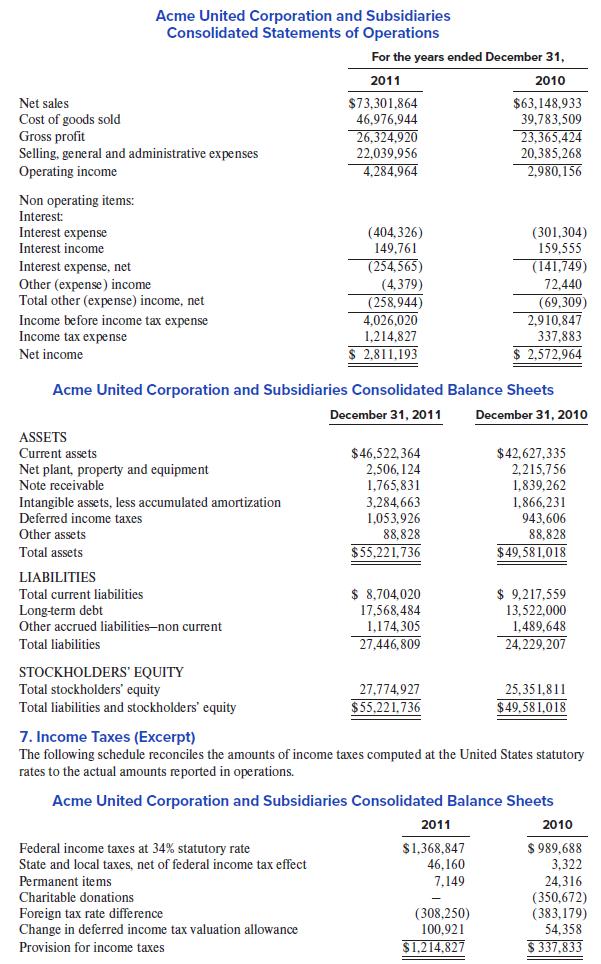

Following are the consolidated statement of operations, balance sheet, and portions of the income tax note from Acme United Corporation’s December 31, 2011, Form 10-K. (For the sake of brevity, the statements have been condensed in ways that are unrelated to the case.)Required:Suppose that during

Dix Company reported operating income (loss) before income tax in its first three years of operations as follows:20X1 .................... $ 100,00020X2 ..................... (200,000)20X3 ...................... 240,000Dix had no permanent or temporary differences between book income and taxable

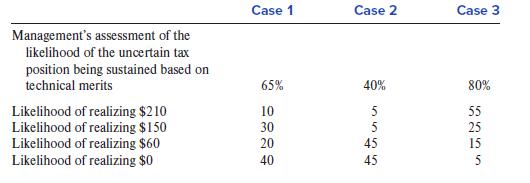

In 20X1, MB Inc. is subject to a 21% tax rate. For book purposes, it expenses $1,500,000 of expenditures. MB intends to deduct these expenditures on its 20X1 tax return despite tax law precedent that makes it less than 50% probable that the deduction will be sustained on its technical merits.

As of December 31, 20X1, Colt Corporation has a loss carryforward of $180,000 available to offset future taxable income. At December 31, 20X1, the company believes that realization of the tax benefit related to the loss carryforward is probable. The tax rate is 21%.Required:What amount of tax

Flower Company started doing business on January 1, 20X0. For the year ended December 31, 20X1, it reported $450,000 pre-tax book income on its income statement. Flower is subject to a 21% corporate tax rate for this year and the foreseeable future. Additionally, it has the following issues that

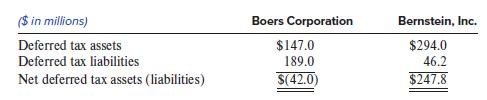

Boers Corporation and Bernstein, Inc. both project pre-tax income of $100 million in 20X1. Both also expect there to be no change in their cumulative temporary differences during the year. However, the two companies are in very different deferred tax positions, as the following information about

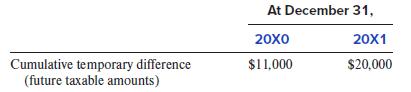

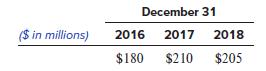

Goff Corporation has only one temporary difference, which is related to the use of accelerated depreciation for income tax purposes and straight-line depreciation for financial reporting. Goff had the following amounts of cumulative temporary difference at December 31, 2016, 2017, and 2018:($ in

On December 31, 20X0, Toms River Rafting, Inc. (TRR), has a deferred tax asset related to a $250,000 net operating loss carryforward. The enacted tax rate (and substantively enacted tax rate) at the time was 21%. When it recognized this deferred tax asset, TRR expected to have sufficient earnings

Cishek Corporation sold $100 million of gift cards in 20X1. The gift cards may be used to purchase goods from Cishek in the future. The gift cards never expire, and Cishek expects that none of the gift cards will go unused. Cishek projects the gift cards will be used to purchase goods according to

Millie Co. completed its first year of operations on December 31, 20X1, with pre-tax financial income of $400,000. Millie accrued a contingent liability of $900,000 for financial reporting purposes; however, no tax deduction is permitted until a payment is made. Millie also has gross profit of

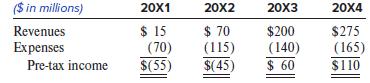

Devers Corporation began operations in 20X1 and had the following partial income statements, which are complete only down to pre-tax income. Devers had no book-tax differences except for the effects of its net operating loss carryforward. The corporate tax rate is 21%.As of December 31, 20X1, and

Collins Company incurs a $1,000 book expense that it deducts on its tax return. The tax law is unclear whether this expense is deductible, so the deduction leads to an uncertain tax position. Assuming a 21% tax rate, the deduction results in a $210 uncertain tax benefit.Required:For each of the

Trevathan Corporation has only one source of temporary differences warranties. At December 31, 2016, 2017, and 2018, the amounts of cumulative temporary differences were as follows:Temporary differences related to warranties arise because warranty costs are expensed under U.S. GAAP in the same

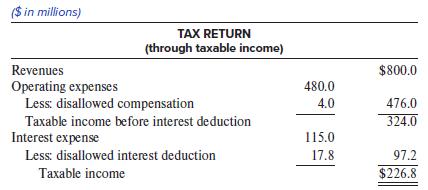

Current tax law limits the amount of interest expense that corporations may deduct to the sum of (a) taxable interest income and (b) 30% of taxable income (excluding taxable interest income) before any deductions for interest, depreciation, amortization, or depletion. However, the law permits any

In early 2017, Quintana Corporation prepared the following forecast of its earnings for 2017 and 2018:Quintana’s pre-tax income forecasts include $40 million of nontaxable income in 2017 and $30 million of nontaxable income in 2018. These were the only permanent differences in the

Early in 2017, Altuve Corporation forecasted that it would report a deferred tax liability of $70 million at December 31, 2017, representing the additional tax that would be due to U.S. authorities if its unrepatriated foreign earnings were to be repatriated. Altuve is now considering the financial

The following information pertains to Seda Company’s pension plan for 20X1:Actuarial estimate of projected benefit obligation at 1/1 ........... $ 72,000Service cost .......................................................................................... 18,000Pension benefits paid on 12/31

Turner Inc. provides a defined benefit pension plan to its employees. The company has 150 employees. The remaining amortization period at December 31, 20X0, for prior service cost is 5 years. The average remaining service life of employees is 11 years at January 1, 20X1, and 10 years at December

AT&T reported pre-tax income of $24,873 million, $15,139 million, and $12,976 million for the years ended December 31, 2018, 2017, and 2016, respectively. At December 31, 2018, it had 7,281.6 million common shares outstanding and a common share price of $28.54. AT&T Inc. reported the

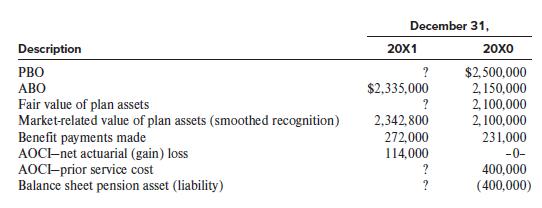

At December 31, 20X1, Kerr Corporation’s pension plan administrator provided the following information:Fair value of plan assets ..................... $ 3,450,000Accumulated benefit obligation ........... 4,300,000Projected benefit obligation ................. 5,700,000Required:What amount of the

Puhlman Inc. provides a defined benefit pension plan to its employees. It smooths recognition of its gains and losses when computing its market-related value to compute expected return. Additional information follows:During 20X1, the PBO increased by $33,000 due to a decrease in the discount rate

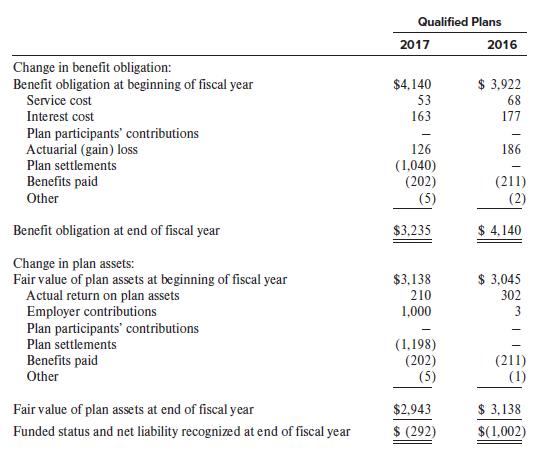

The Kroger Co. operates numerous grocery store chains. Excerpts from Kroger’s Note 15 are presented below. The 2017 amounts are for the fiscal year ended February 3, 2018. All amounts are in millions of U.S. dollars. At February 3, 2018, Kroger had 870 million outstanding shares of common stock.

On January 2, 20X1, Loch Company established a defined benefit plan covering all employees and contributed $1,000,000 to the plan. At December 31, 20X1, Loch determined that the 20X1 service and interest costs totaled $620,000. The expected and the actual rate of return on plan assets for 20X1 was

Refer to The Kroger Co. information in Case 15-3.Required:Explain how net benefit cost and OCI would change if The Kroger Co. were using IAS 19.Case 15-3.The Kroger Co. operates numerous grocery store chains. Excerpts from Kroger’s Note 15 are presented below. The 2017 amounts are for the fiscal

Mary Abbott is a long-time employee of Love Enterprises, a manufacturer and distributor of farm implements. Abbott plans to retire on her 65th birthday, five years from January 1, 20X1. Her salary at January 1, 20X1, is $48,000 per year, and her projected salary for her last year of employment is

On January 1, 20X1, Magee Corporation started doing business by hiring R. Walker as an employee at an annual salary of $50,000, with an annual salary increment of $10,000. Based on his current age and the company’s retirement program, Walker is required to retire at the end of the year in 20X4.

Use the facts given in E15-4. Repeat the requirements assuming that the discount and earnings rate is 11% instead of 8%.E15-4.Mary Abbott is a long-time employee of Love Enterprises, a manufacturer and distributor of farm implements. Abbott plans to retire on her 65th birthday, five years from

The following information pertains to Gali Company’s defined benefit pension plan for 20X1:Fair value of plan assets, beginning of year ............ $ 350,000Fair value of plan assets, end of year ......................... 525,000Employer contributions

Showing 2700 - 2800

of 3092

First

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

Step by Step Answers