New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

probability and stochastic modeling

Probability And Stochastic Modeling 1st Edition Vladimir I. Rotar - Solutions

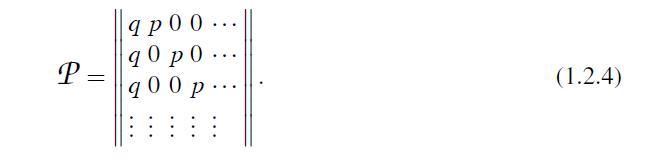

Consider the transition matrix(a) Argue why in this case we should not hope for ergodicity. How does the chain evolve in this case? Show that Doeblin’s condition of Theorem 4 does not hold for this matrix.(b) Let (π0, π1) and (˜ π0,˜ π1) be the stationary distributions for the two-state

Consider the situation of the example on weather-condition in Section 2.3 in the stationary regime. Given that the today weather conditions are either rainy or icy-road ones, find the mean waiting time for the normal conditions.

Assume that in the situation of Example 4.2-5, in the stationary regime, a daily number of accidents occurred to be greater than six. Find the probability that the weather on this day corresponds to the icy road condition. Comment on that it is greater then π2.Example 4.2-5We include in Example 2

A stochastic matrix is said to be doubly stochastic if for all columns, the sum of the probabilities is also equal to one. Show that if a chain with such a matrix is finite and ergodic, in the long run, all states are equally likely.

Peter runs a small business classifying each day as good, moderate, or bad. The transition process is Markov with transition matrix (1.2.2). A daily income is a r.v. assuming values 1 or 2 on a bad day; 2 or 3 on a moderate day; and 3 or 4 on a good day; in all these three cases, with equal

Argue that the Markov chain from Exercise 6b is not ergodic. Certainly, if this is true, Doeblin’s condition must not hold. Show directly that this is indeed the case. (Advice: Try to avoid long calculations.)Exercise 6bShow that the random walk process in Section 2.2.4 is a Markov chain. Find

In the problem of Example 4.3-1, assume that from state i the process moves to state i + 1 with probability pi = λ/1+i, and to state 0 with probability qi = 1− pi, where a number λ ≤ 1, and i = 0,1,2, ... .(a) Proceeding from (4.3.3), find the limiting distribution π.(b) Let T0 be the

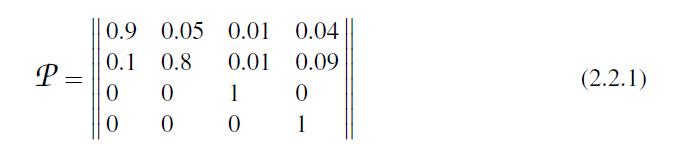

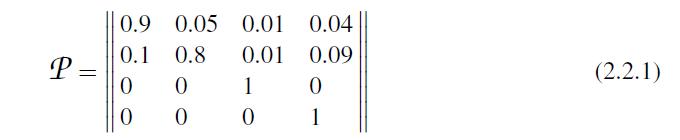

Classify the states and classes of the chain in Example 2.2-1.Example 2.2-1 Consider a medical insurance model with four states for an insured: healthy, sick, ceased paying, deceased. Suppose that for a particular group of customers, the matrixgives transition probabilities corresponding to annual

(a) Show that, if there are more than one state, and pii = 1 for some i, then the chain is reducible.(b) Give an example of a reducible chain for which all transition probabilities are less than one.(c) Show that in order to specify the classes of a chain, we do not need to know particular

Prove that if the number of states is a finite k and state i is accessible from state j, then it is accessible in k−1 or a less number of steps.

Classify the states of

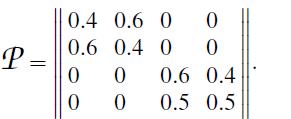

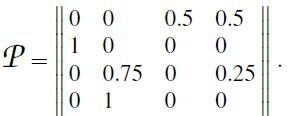

Figure out whether the matricescorrespond to periodic chains. Find periods.

LetXt =Σt i=1 ξi, where independent d-dimensional r.vec.’s ξi take on 2d vector values (±1, ...,±1) with equal probabilities 1/2d. Another way to state the problem is to write ξi = (ξi1, ..., ξid), where ξik’s are independent r.v.’s assuming values ±1 with equal probabilities 1/2.

Proceeding from Theorem 9, justify rigorously the ergodicity property for chains in Examples 1.2-1,2,3.Examples 1.2A police department provides daily reports on traffic accidents in a particular area. The intensity of daily accidents depends on weather conditions. The department distinguishes three

Show that the chain in Example 2.2-1 is not ergodic.Example 2.2-1Consider a medical insurance model with four states for an insured: healthy, sick, ceased paying, deceased. Suppose that for a particular group of customers, the matrix

In the model of Section 4.2.2, consider the probability that one of the players will be leading 9900 times out of 10,000. Do you expect this probability to be small? Estimate it and comment on the result.

Suppose we are tossing a regular coin 10,000 times. Guess how often, on the average, the number of heads will be equal to the number of tails. Check your guess.

We have proved in Section 4.1 that E{τ} = ∞ for p = 1/2. Show that the same follows from (4.1.9).

In the model of Section 4.1, set p = 3/4 and find the probability that the random walk will revisit zero at most 3 times.

Find the extinction probability for the case where ξ’s are distributed as in Exercise 7 and X0 is Poisson with parameter λ.Exercise 7Show that for the case fk = 0, k > 2, the extinction probability is the same as in Example 1-1. Connect the condition f2 > f0 with the condition μ > 1. (Advice:

(a) Explain that if X0 is not random and greater than 1, then E{Xt} and Var{Xt} are given by the expressions (3.2) and (3.3), respectively, multiplied by X0.(b) Consider the case of a random X0. Write general formulas and consider the case where X0 is(i) Poisson with parameter λ and (ii)

Find E{Xt} and Var{Xt} in the case where ξ’s are Poisson with parameter λ. Do the same for the case where X0 is a Poisson r.v. with the same parameter.

Let X0 = 1, and S = Σ∞t=0 Xt , the total number of all “particles” in all generations. Show that E{S} = ∞, if μ ≥ 1; and E{S} = 1/(1−μ), if μ< 1. If f0 = 3/4, and f2 = 1/4, what is the total mean number of the particles?

In a country, practically all men are married, 10% of married couples do not have children, and 90% have three children. Each child is equally likely to be a girl or boy. Using software, estimate the probability that a married man’s male line of descent will ever cease to exist.

Show that, if f5 > 1/5, the extinction probability is less than one.

Find the extinction probability for f0 = 0.8, f1 = 0.1, f2 = 0.1.

Show that for the case fk = 0, k > 2, the extinction probability is the same as in Example 1-1. Connect the condition f2 > f0 with the condition μ > 1. (Advice: When solving (1.3), use the fact that f1 = 1−( f0+ f2).)

Find the extinction probability in the case where ξ, the number of offsprings of a particle, has the second version of the geometric distribution as in Example 2-2.

For the case f0 + f2 = 1, graph the extinction probability as a function of f0.

Show that the sum of Poisson independent r.v.’s is a Poisson r.v. using Theorem 1 and (2.7).

Find the mean and variance of the binomial distributions using g.f.’s.

Show that, if G(z) is the g.f. of a r.v. X, then G″(1) = E{X(X −1)}. How to find Var{X} using the g.f. G(z)? Do that for the second version of the geometric distribution.

Find the g.f. of the first version of the negative binomial distribution using (3.2.1.11).

In an area, the number of days during a season when you can watch shooting (falling) stars is a Poisson r.v. with a parameter λ. The number of falling stars on each of such days is also a Poison r.v. with a parameter μ. The numbers of stars on different days are independent, and do not depend on

Write a formula for P(N = k) in the case where X’s have a geometric distribution. Demonstrate directly, using the formula for total expectation, that E{N} = ∞. (Advice: In both cases, condition on X0.)

A gambler is playing a slot machine. The results of plays are independent, the probability of winning in each play is p. Denote by Nk the number of the play when the kth win occurred, and by τk the number of plays between the (m−1)th and the mth including the latter. (a) Find the conditional

In Exercise 84, set n = ∞ and find the expected value of the number of the first success.Exercise 84Suppose that in a sequence of n independent trials, the common probability of success is a random variable; say, it depends on conditions under which the trials are being performed.(For example, in

Suppose that in a sequence of n independent trials, the common probability of success is a random variable; say, it depends on conditions under which the trials are being performed.(For example, in the quality control scheme, the share of defected items may depend on conditions under which the

In Lemma 19, which is larger:Does the convergence Yn(ω)−Y(ω)→0 imply

Let Sn be the number of successes in n independent trials with the probability of success in each trial equal to p. Let ξn = 1/n max{Sn,n−Sn}. Which is larger: E{ξn} or max{p,1− p}?Find limn→∞ ξn. In what sense does ξn converge to its limit?

Bob wishes to check whether the total sum in his credit card statement is plausible. He adds up all figures concerning the purchases made, rounding each number to the nearest integer.Let S be the cumulative error after summation. Suppose there were 100 purchases, and the fraction part of the cost

Each day, a manager of a store determines the daily number of customers. The numbers for different days are independent with the same Poisson distribution. Assume that the mean number of customers per day is 36. The manager does not know this, but she/he has data for the last n days, and can

The daily number of traffic accidents is a Poisson r.v. with λ = 30, and the probability that an accident causes a serious damage is p = 0.3. The outcomes of different accidents are independent. Find the probability that(a) The number of accidents with serious damages will exceed 8;(b) The number

(a) State generalizations of Propositions 13 and 14 for the case of k independent Poisson r.v.’s for the former proposition, and for the case of k types for the latter.(b) Prove the generalizations you stated.

Is it a linear combination of Poisson r.v.’s? Suppose E{N} = 4 (rather than 40) and find P(S = 100), P(S = 200), P(S = 350).

Suppose that in the scheme of Section 4.5.1, pn = λ/n (that is, we simplify the problem neglecting the remainder o(1/n) in (4.5.4)).(a) Is E{Xn} equal to the mean of the limiting Poisson distribution?(b) Is Var{Xn} equal to the variance of the limiting Poisson distribution? What happens when

Let Zn be a Poisson r.v. with parameter λ equal to an integer n. Show that Zn may be represented as Y1+...+Yn, where the Y’s are independent Poisson r.v.’s with parameter λ = 1.

Assume that N1,N2 are independent Poisson r.v.’s with the same λ. Find the distribution of the total number of the claims covered for the case of the two separate insurances and for the case of the joint insurance. Compare these distributions.

Suppose that, in a coastal area, during the hurricane season from August through November, hurricanes hit the coast with a monthly rate of 1.15, and outside the hurricane season the rate is 0.3 per month. The monthly number of hurricanes are independent Poisson r.v.’s. Find the probability that

Compute the coefficient of variation (see Exercise 53) for the geometric, binomial, and Poisson distribution. Describe the behavior of the ore the behavior of the coefficients of variation when in the second case n is increasing; and in the third case λ is increasing.Exercise 53For any

For an auto insurance portfolio, on the average, 10% of customers file claims for the coverage of their losses. Use the Poisson approximation to estimate the probability that at most 3 out of 25 customers will file claims.

Assume that a medicine has a side effect which happens on the average with one patient out of 750. Suppose that in a hospital during a certain period, 1500 patients took this medicine.Find the expected value and the variance of the number of the patients who had the side effect, and estimate, using

Let X be a Poisson r.v. with parameter λ, and p(λ) = P(X is even). Prove that p(λ) = 1/2 (1+ e−λ). Find the probability that X is odd.

Is (4.3.4) true for the r.v. K from Section 4.3? If not, write an appropriate counterpart.

For a sequence of independent trials with the probability of success equal to p, what is the probability that there will be exactly five failures before the eighth success? How is this question connected with the negative binomial distribution?

In some world chess championships, ties were not counted, and the competition lasted until a participant got six points. Assuming that the results of games are independent, and the participants are of equal strength, find the probability that at the end of the championship, a participant will have

Consider the r.v.’s N and K from Section 4.3. Show that the conditional distribution of K given K > 0 coincides with the distribution of N. Show that this is a special property of the geometric distribution.

Mr. Smith bought a number of shares of a particular stock. Assume that each working day, the price per share drops with a probability of 0.4 and rises with a probability of 0.6. Mr. Smith has decided to sell all shares right away after the third drop. How many days on the average will Mr. Smith

Standard items produced in a factory go through quality control. The probability that an item taken at random does not meet certain requirements is 0.005. Suppose that the first 100 consecutive items have been found conforming. What is the probability that the total number of consecutive items

Let X be a Poisson r.v. with λ = 2, and Y be a geometric r.v. with the parameter p = 0.3. Assume X and Y to be independent.

Let X1, ...,Xn in Exercise 60 be independent, all expectations E{Xi} = m, but the variances be different, and Var{Xi} = σ2i . How would you distribute the money between the assets adopting the variance as a measure of riskiness? Would it influence the expected return of your investment? Find the

There are n assets with random returns X1, ...,Xn. The term “return” means that, if you invest $1 in, say, the first asset, you will get an income of X1 dollars. Note that a return may be less than one.Assume that X1, ...,Xn are i.i.d., E{Xi} = m, Var{Xi} = σ2. Consider two strategies of

Let E{X} = 0 and Var{X} = 1. Does it mean that X cannot assume “big” values? ConsiderCompute E{X} and Var{X}, and comment on the situation. Compute the third moment m3 and the third absolute moment m3. Consider their behavior for large n.

Compute the standard deviation of the r.v. from Exercise 41, compare it with the mean and comment on the situation with large n.Exercise 41Does the fact that E{X} has a “moderate” value, mean that X cannot assume “big” values?Let us consider a r.v.for large n. Such a r.v. may illustrate a

100 dice are rolled. What is the expected value and the variance of the sum of the faces shown?

8 cards are drawn from a 52-card deck. Find the expected number of spades. Does the answer depend on whether the cards were drawn with or without replacement? Can we reason in the same way when computing the variance?

Compare the problem in Exercise 54 with that in Exercise 45.Exercise 45It is known that for any positive r.v. X, the function n(s) = (E{Xs})1/s is non-decreasing in s. Prove it, using Jensen’s inequality.Exercise 54Which is larger: E{X2} or (E{|X|})2? (Unlike in (3.1.5), we consider |X|.)

Which is larger: E{X2} or (E{|X|})2? (Unlike in (3.1.5), we consider |X|.)

For any distribution with mean m ≠ 0 and standard deviation σ, the ratio σ/m is called a coefficient of variation (c.v.).(a) How would you interpret the situation when the c.v. of one r.v. is larger than that of another? (b) Will the c.v. change if we multiply the r.v. by a number?

Find the variance in the problem of Exercise 27 for independent trials.Exercise 27We run a sequence of trials for which the probabilities of success are different. Namely, for the first trial, it is 1/2, for the second, it is 1/4, and so on: for the kth trial, it is 1/2k. Find the expected number

We revisit Exercise 33. Suppose that the number of potential buyers is a Poisson r.v. with a mean of 60,000, and it does not depend on the price of the product. Find the standard deviation of the company’s income.Exercise 33A company is going to put a new computer in the market in one year. A

In which of two cases in Exercise 5d do you expect a larger variance? Check your guess computing the variances.Exercise 5d(d) Compare the two following distributions:What is the difference? Are both distributions symmetric? For which distribution does the “dispersion” or “variation” of

Find the mean and variance for the distribution in Exercise 6.Exercise 6There are six items in a row. You mark at random two of them. Find the distribution of the number of items between the marked items.

(a) Find the variance of the number on a die rolled.(b) Find the variance of the product of the numbers two dice rolled.

Let X = ±1 with equal probabilities. Do we need to calculate Var{X}, or is the result obvious?

Letbe the index of the first Xi whose value is greater than or equal to X0. Show that in the case of a finite number of the values of X’s, the meanFind it, if Xi = 0,1,2 with respective probabilities

It is known that for any positive r.v. X, the function n(s) = (E{Xs})1/s is non-decreasing in s. Prove it, using Jensen’s inequality.

The time X it takes for Michael to drive to school varies from day to day depending on weather and traffic conditions. Michael wishes to estimate the mean speed at which he drives.To this end, he estimates the mean time E{X} computing the average time for a significant number of trips, and divides

Consider the r.v. X from Exercise 41 replacing 0 by a “small” number ε. Compare 1/E{X}and E{1/X}. Which theorem does this example illustrate?Exercise 41Does the fact that E{X} has a “moderate” value, mean that X cannot assume “big” values?Let us consider a r.v.for large n. Such a r.v.

In a show, you are given two closed envelopes containing positive sums of money. It is known that one envelope contains twice as much as the other.You may choose one envelope and keep the money it contains. You pick one envelope at random, open it and see an amount of c. At this moment, the host

Does the fact that E{X} has a “moderate” value, mean that X cannot assume “big” values? Let us consider a r.v.for large n. Such a r.v. may illustrate a possible future loss connected with a possibility of a catastrophic event, say, an earthquake. The probability of the event is small, but

Compute the expected value for the geometric distribution using formula (2.2.1) and compare your calculation with those.

Let X be the number of successes in a sequence of n trials with the probability of success equal to p. Show that the relation E{X} = np is always true whether trials are independent or not.

Is the independence condition necessary for E{X1X2} = E{X1}E{X2}?

Find the expected value of the product of the numbers on two dice rolled.

A r.v. X has the Poisson distribution with parameter λ. Find E{1/(1+X)}.

A r.v. X assumes values 1, 2, 4, ... with respective probabilities

You roll a die until the first moment when “6” appears, but not more than ten times. Find the expected number of rolls. (Use of software is recommended.)

A company is going to put a new computer in the market in one year. A company’s analyst presupposes that the future market price for such a computer may assume three values: $900,$1000,$1100 with equal probabilities. The analyst also thinks that on the average, 60,000 people will buy the

There are two classes of 20 and 30 students. No student takes both classes. A student is randomly selected out of these 50 students. Let X be the number of students in the class this student is taking. Now, a class is randomly chosen (out of two). Denote by Y the number of students in this class.

Find the expected value of the number of customers at the first and second counter separately.

Let a r.v. X = 1,2,3,4, 5, and P(X = 3) = 0.2. Assign probabilities to the other values in a way that it would be clear without any calculations that E{X} = 3. Do not make all probabilities you assign the same.

Solve problem of Exercise 28 for 2n, n > 1, boxes. Does the above probability increase or decrease as n is increasing? Find the limit as n→∞.Exercise 28There are four closed boxes, one of which contains a prize and the others are empty. A player can consecutively check boxes until she/he finds

There are four closed boxes, one of which contains a prize and the others are empty. A player can consecutively check boxes until she/he finds the prize, and in this case, she/he pays $1 for each check (including the last box if the prize is there). The player may also divide the boxes into two

We run a sequence of trials for which the probabilities of success are different. Namely, for the first trial, it is 1/2, for the second, it is 1/4, and so on: for the kth trial, it is 1/2k. Find the expected number of successes in n trials. Consider the case n = ∞.

You play a game of chance with the probability of winning at each play equal to 1/3. You bet $1 and quit if you win. If you lose, you bet $2 and quit whatever happens. Find the expected value of your profit. Will this figure change, if you first bet $2, and then $1 (if you lose at the first time)?

(a) Explain without any calculations why the mean number on a die rolled should be equal to 3.5. Verify it proceeding from definition (2.1.1).(b) Let us revisit Exercise 5a. Say, without calculations, in which case the mean is larger.(c) Show that for any symmetric distribution (see a definition

Find the mean number of letters in the word taken at random from the rhyme in Exercise 1. Compare it with the number 5.1 that in some sources is referred to as the mean length of a word in an English text. Do you find the difference from what you got significant?Note that in our example, as well as

In Exercise 20b, for r = 3, find the distribution of X1 given X1 +X2 = 4 in two ways: using formulas for conditional probabilities, and considering different outcomes given X1 + X2 =4.Exercise 20b(b) Do the same for X1 and X2 taking on equiprobable values 1, ..., r for a natural r.

(a) Just looking at the table of joint probabilities and providing all calculations in mind, find P(X1 = 3|X2 = 0).(b) Just looking at the table of joint probabilities and providing all calculations in mind, write the conditional distribution of X2 given X1 = 0; the conditional distribution of X1

Showing 6700 - 6800

of 6914

First

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

Step by Step Answers