New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

marketing strategy planning

A First Course in Quantitative Finance 1st edition Thomas Mazzoni - Solutions

What is the difference between a line graph and a time plot?

What does it mean for two variables to be linearly related?

What does an individual dot on a scatterplot represent?

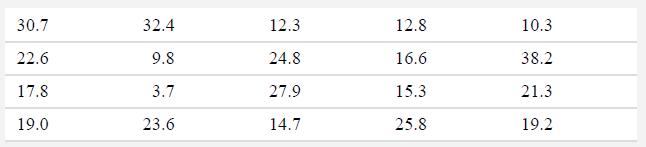

The World Happiness Report publishes a number of indicators related to physical and psychological well-being (Helliwell, Layard, & Sachs, 2018). For example, it publishes adult obesity rates for more than 30 countries, with those percentages ranging from 3.7% in Japan to 38.2% in the United

Use the data from Exercise 2.34 on the average number of years it takes students to complete a doctorate at 41 different universities. a. Construct a dot plot for these data.b. What can you learn about the shape of this distribution from this dot plot?Exercise 2.34The Survey of Earned

The following data are Consideration of Future Consequences (CFC) scores for 20 students, already arranged in order from lowest to highest:a. Construct a dot plot for these data.b. What can you learn about the shape of this distribution from this plot? 2.0, 2.0. 2.5, 2.5, 3.0. 3.0. 3.0, 3.0, 3.5,

The Canadian Radio-Television and Communications Commission (crtc.gc.ca/eng/publications) gathered data on the numbers of television sets in Canadian homes. Two percent of homes had no television; 28% had one television; 32% had two televisions; 20% had three televisions; and 18% had four or more

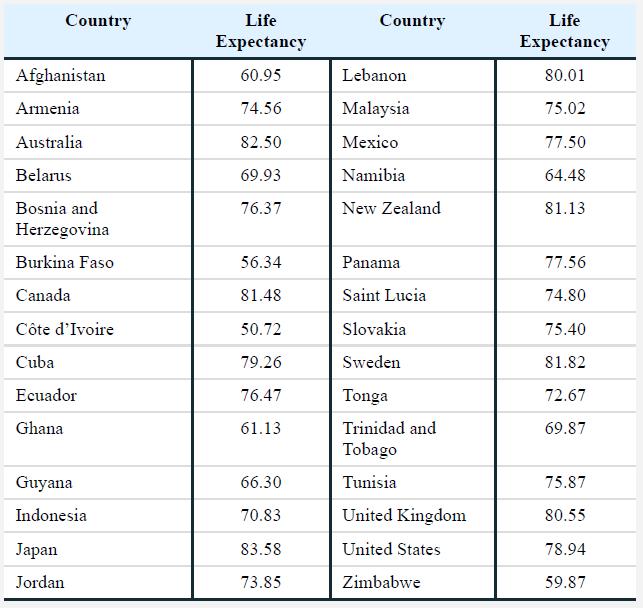

The United Nations Development Programme (2015b) published life expectancy rates—the number of years an adult can expect to live—for 195 countries around the world. Below is a randomly selected sample of 30 of them.a. Create a grouped frequency table for these data.b. The data have quite a

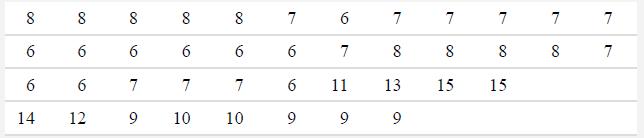

The Survey of Earned Doctorates provides data on the length of time in years that it takes to complete a doctorate. Each data point is the mean time for one university. Below is a modified list of this completion-time data, truncated to whole numbers and shortened to make your analysis easier.

Students in a statistics course reported the number of hours of sleep they get on a typical weeknight. These data appear below.a. Create a dot plot of these data.b. Use the dot plot to describe the distribution of the set of scores. 5 6.5 6. 8 6. 6 7 7 6 6.5 7 7 8 4.

a. Using the following set of data, construct a dot plot. Follow the steps in the Data Ethics box of the chapter to set up the dot plot.b. Refer to the dot plot created for part (a). Does it depict a symmetric or a skewed distribution? 3.5 2.0 4.0 3.5 2.0 2.5 4.5 4.0 3.0 3.5 3.0 3.0 4.0 4.5 2.5 3.5

A grouped frequency table has the following intervals: 30–44, 45–59, and 60–74. If converted into a histogram, what would the midpoints be?

In what way are dot plots similar to histograms?

What are potential benefits of using a dot plot instead of a histogram?

In your own words, define the word distribution, first as you would use it in everyday conversation and then as a statistician would use it.

Describe what a histogram looks like, including what goes on the xaxis and the y-axis.

What are raw scores?

Australian psychologist Mark Rubin (2017) likened the unethical practice of HARKing to the tale of the Texas sharpshooter. Rubin explains that the sharpshooter “aims and fires his gun at [a] target on a barn wall but misses. He then walks up to the wall, rubs out the initial target, and draws a

New York Times reporter Anahad O’Connor (2018) reported on a scandal in the field of psychology. A well-known researcher of food-related behaviors, Brian Wansink, resigned from his position at Cornell University after university investigators discovered “academic misconduct in his research and

As the use of e-cigarettes, or vaping, becomes more popular, researchers are exploring the potential negative effects from this behavior. According to Scientific American (2018), researchers have investigated the harmful effects of nicotine, including its links to heart disease, as well as the

a. As racing fans, we would be very interested in the variable finishing position. One year, a horse called Orb won, followed by Golden Soul in second and Revolutionary in third.b. We also might be interested in the variable finishing time. Orb won in 2 minutes, 2.89 seconds.c. Derby attendance was

According to the World Health Organization (2018), more than 300 million people suffer from depression globally.a. Do you think the research behind this statistic is based on a sample or a population? Explain.b. Is 300 million a descriptive statistic or an inferential statistic? Explain.

Suppose a researcher is interested in evaluating how pet ownership and social activity affect loneliness.a. Identify the independent variables and the dependent variable.b. Imagine that pet ownership is assessed as either owning no pets or owning at least one pet, and that social activity is

A researcher studies the average distance that 130 people living in urban areas in India walk each week.a. What is the size of the sample?b. Identify the population.c. Is this “average” a descriptive statistic or an inferential statistic if it is used to describe the 130 people studied?d. How

What is HARKing and how can preregistration help to eliminate this practice?

What is preregistration and why is it important?

Describe the kinds of unethical practices that researchers might be concerned with.

What do researchers mean by data ethics?

What is the difference between a between-groups research design and a within-groups research design?

What is the difference between a sample and a population?

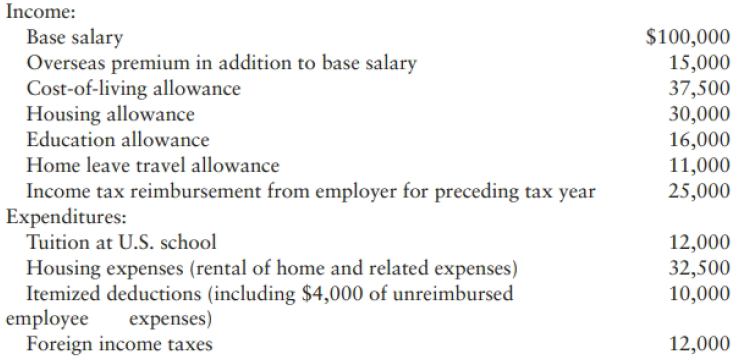

John Lawrence Bailey is employed in Country T by American Conglomerate Corporation. Bailey has resided with his wife and three children in Country T for seven years. He made one five-day business trip back to the United States in the current year, and $2,000 of his salary (but none of the

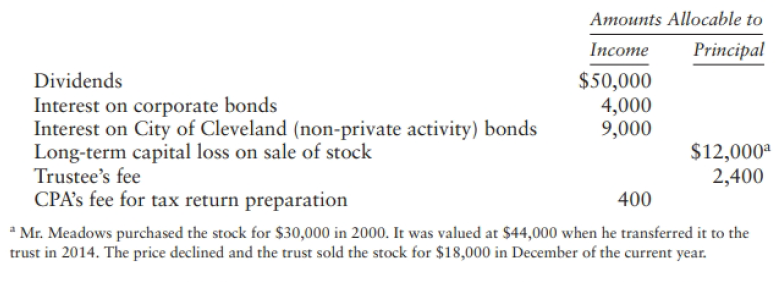

Mark Meadows funded a trust in 2014 with Merchants Bank named as trustee. He paid no gift tax on the transfer. The trustee in its discretion is to pay out income, but not principal, to Mark's children, Angela and Barry, for 15 years. Then the trust will terminate, and its assets, including

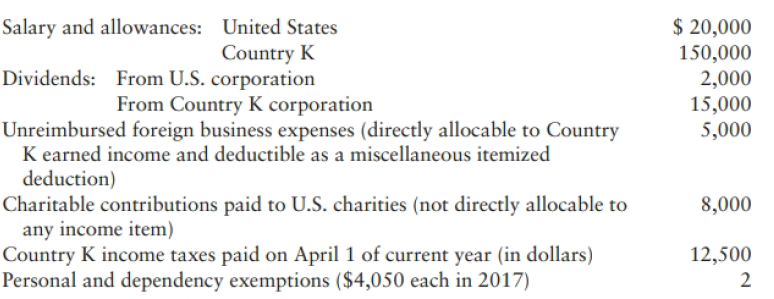

Stephen R. and Rachel K. Bates, both U.S . citizens, resided in Country K for the entire current year except when Stephen was temporarily assigned to his employer's home office in the United States. They file a joint return and use the calendar year as their tax year. The Bateses report the

In 2014, Leon Lopez funded Lopez Trust #3, an irrevocable trust, at First Bank, 125 Seaview, Northwest City, WA 98112, for the benefit of his twin children, Loretta and Jorge. The trust's tax ID number is 74-1243565. The trustee, in its discretion, is to distribute income and/or principal to one or

Prepare an estate tax return (Form 706) for Adam Zugg of 45 Cornfield Place, Midwest City, IL 60000. Adam died October 31, 2017. He was survived by his wife, Callie, and their son, Zebulon. At the time of his death, Adam was employed by a farm equipment distributor as its office manager. T he

Prepare an estate tax return (Form 706) for Marcia Miller, who died July 23, 2017. Marcia (born April 2, 1930) resided at 117 Brandywine Way, Eastern City, PA 19000 and was a lifelong Pennsylvania resident. Her first husband, Arthur Adams, died in 1995. In June 1999, she married Matt Miller, a U.S.

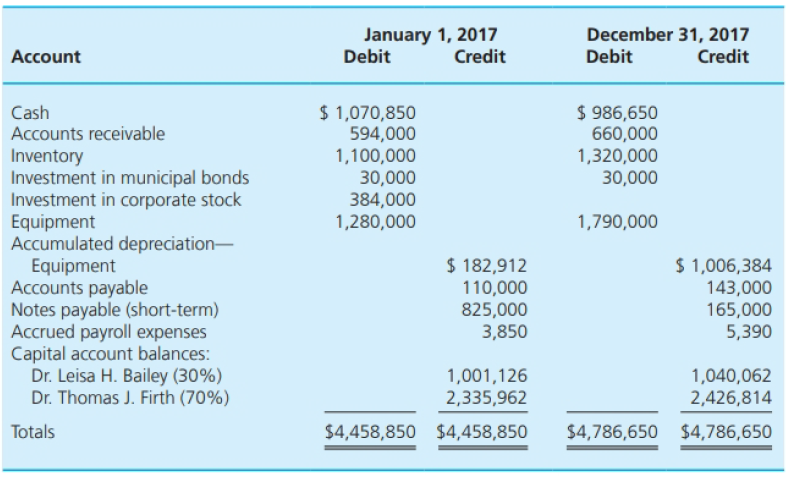

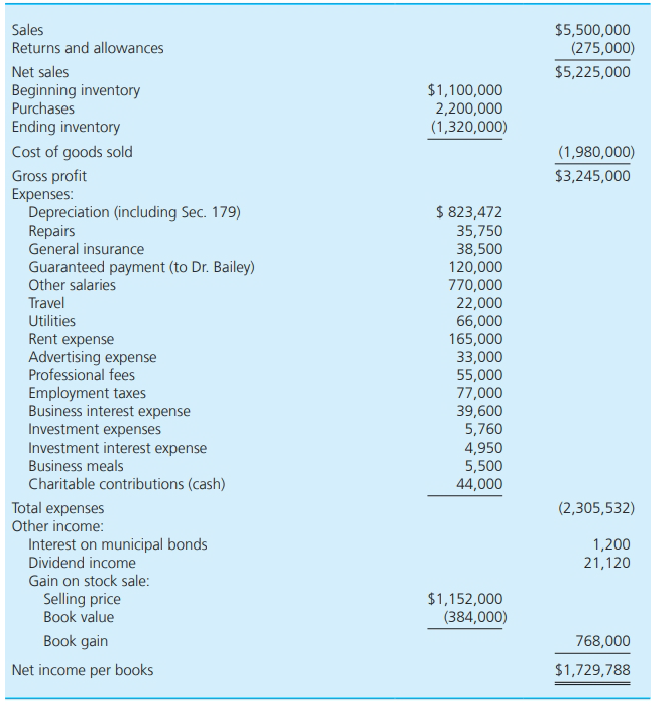

Healthwise Medical Supplies Company is located at 2400 Second Street, City, ST 12345. The company is a general partnership that uses the calendar year and accrual basis for both book and tax purposes. It engages in the development and sale of specialized surgical tools to hospitals. The employer

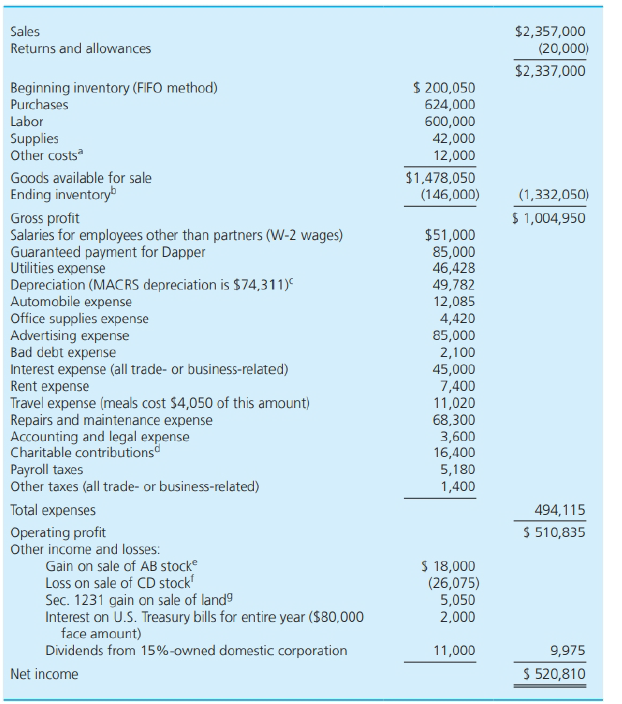

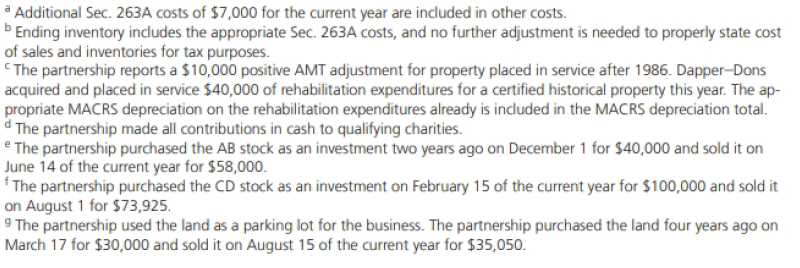

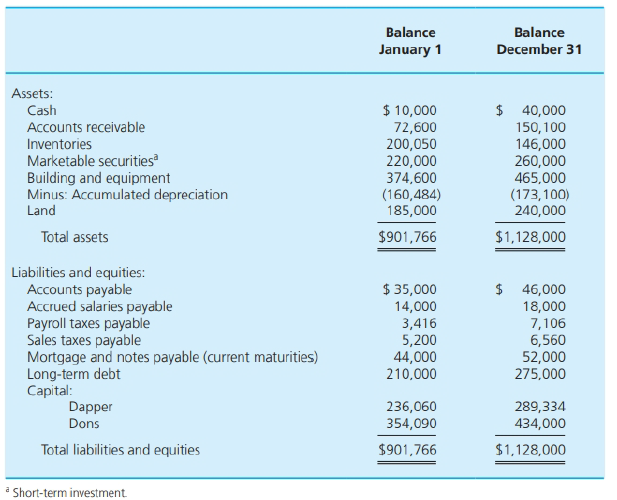

The Dapper-Dons Partnership was formed ten years ago as a general partnership to custom tailor men's clothing. Dapper-Dons is located at 123 Flamingo Drive in City, ST, 54321. Bob Dapper manages the business and has a 40% capital and profits interest. His address is 709 Brumby Way, City, ST, 54321.

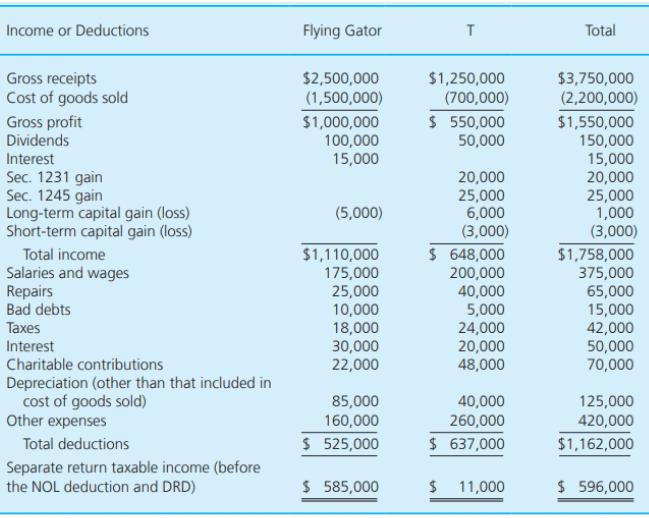

Flying Gator Corporation and its 100%-owned subsidiary, T Corporation, have filed consolidated tax returns for many years. Both corporations use the hybrid method of accounting and the calendar year as their tax year. During 2017 (which is the current year for this problem), they report the

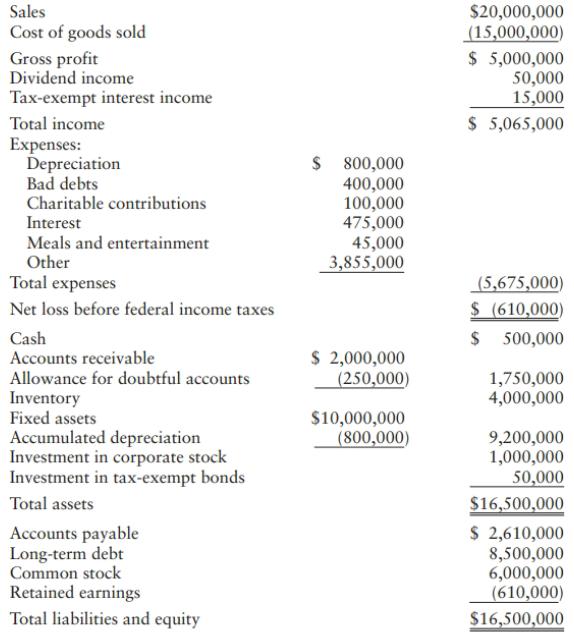

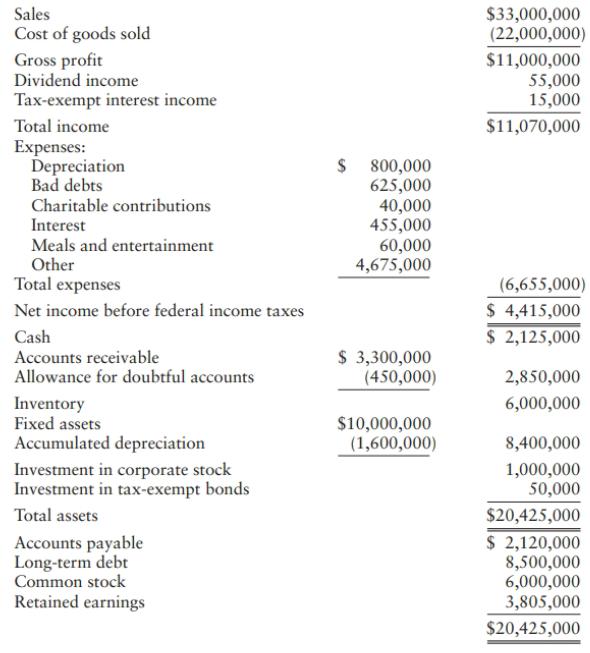

Permtemp Corporation formed in 2016 and, for that year, reported the following book income statement and balance sheet, excluding the federal income tax expense, deferred tax assets, and deferred tax liabilities:Additional information for 2016:• The investment in corporate stock is comprised of

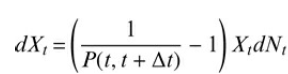

Use the change-of-num?raire toolkit and the DC-operator to derive the drift of the n-th forward LIBOR under the spot LIBOR measure QB, for an arbitrary time 0 ? t n?1. Keep in mind that the process Xt in the definition of Bd(t) in Problem 21.1 is almost surely constant. Problem 21.1 Suppose that

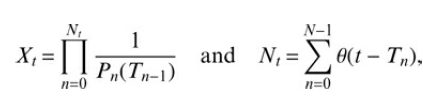

Show that Bd(t) as defined in Problem 21.1 is almost surely a continuous process.Problem 21.1Suppose that the tenor structure T−1, T0,..., TN is equispaced, withΔt = Tn − Tn−1 and T−1 = 0. For 0 ≤ t ≤ TN, the discretely rebalanced bank account Bd(t) has present value.withwhere θ(x) is

Suppose that the tenor structure T?1, T0, . . . , TN is equispaced, with ?t = Tn ? Tn?1 and T?1 = 0. For 0 ? t ? TN, the discretely rebalanced bank account Bd(t) has present value. with where ?(x) is again the Heaviside-?-function. Use Theorem 17.2 on page 390 to prove that Xt has the dynamics

Verify this statement by reviewing (20.107) on page 476. (20.107) т аr., D 3D Zoи, )| ,9dsd + Zo,0, Taw,0) q=1 q=1

In fitting the historical volatility structure of the HJM-factors, quadratic splines were used. Suppose there are N observations ?(t, ?n), for n = 1, . . . , N. Show that all spline coefficients can be computed, if the data points are matched exactly, the condition holds, and the first spline is

Check that A(T, T) = B(T, T) = 0 holds.

Compute the convexity adjustment in the Hull–White-extended Vasicek-model.

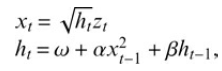

Show that the GARCH(1,1)-process xt, defined by? with independent and identically distributed innovations zt ? N(0, 1), is not a Markov-process. X, = Vh,z, h; = w + ax_, +Bh;-1, + Bh1-1

Consider the short rate model Show that this model is a member of the affine term structure class and derive the ATS-functions A(t, T) and B(t, T). dr(1) = e "dt + o,dW(t)

Suppose pricing is conducted with a one-factor short rate model. Use the Jamshidian-decomposition to compute the generic price of a receiver swaption, expiring at T0, with tenor structure t < T0, . . . , TN and Δt = Tn − Tn−1.

Derive the discount bond volatility σP(t, T) in the Vasicek-model and verify that σP(T, T) = 0 holds.

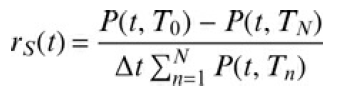

Prove that the forward swap rate can be understood as a weighted average of all forward LIBORs within the tenor of the swap. P(t, To) – P(t, TN) rs(t) = Δι ΣΚ Ρ(, Τ)

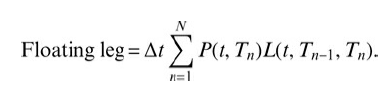

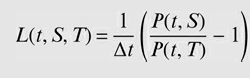

Use the definition of the forward LIBOR, (19.31) on page 447, to show that the present value of the floating leg of a plain vanilla interest rate swap is indeed (19.31) Floating leg = At> P(1, T„)L(t, Tn-1, Tn). n=1 1 ( P(t, S) At P(t, T) L(t, S, T) =

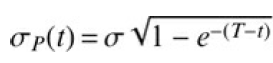

Let today be time t. Suppose you want to price a plain vanilla option with expiry date T on a discount bond, maturing at S, within the Black-76-model, with t Compute the quantity d+/?, required in Black?s formula. O p(t) = o V1 – e-(T-1)

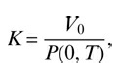

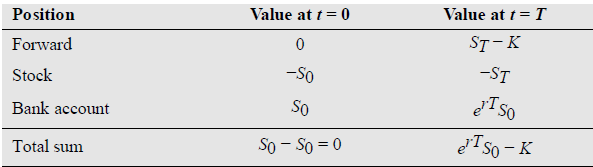

Use an arbitrage argument, analogous to the one in Table 11.1 on page 212, to prove that in a stochastic interest rate world, the strike price of a forward contract Ft(K, T) that can be entered costlessly at time t = 0 has to be which is the forward price of a non-dividend paying underlying V at

Suppose you have an expectation with respect to the T-forward measure, based on the information available at time t T, Derive the Radon?Nikodym-derivative dQT/dQS|Ft and write the solution for Vt d@т V, = P(t, T)E®r[Vr\Fi]= P(t, T)Eºs VrF. dQs

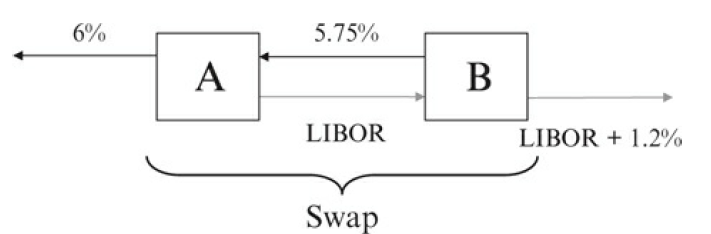

Consider the financing conditions in Table 18.2 on page 436 for companies A and B. Assume that a financial intermediary C offers both companies a payer and a receiver swap to realize comparative advantages. C takes 20 bps of the comparative difference to insure herself against default of one

Show that the bootstrap formula (18.49) on page 435 is equivalent to a finite difference approximation of (18.44), if the respective bonds are expressed in terms of their yield to maturity y(t, Tn) and y(t, Tn?1). (18.49) (18.44) log P(t, T,) – log P(t, Tn-1) T - Ty-1. F(t, Tµ-1, Tn) =- At,

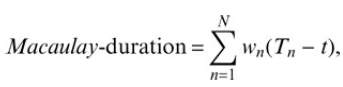

Show that Macaulay-duration is a weighted average of times to maturity where the weights wn are the fractions of the present value of the bond, represented by the n-th cashflow. Macaulay-duration= >, wn(Tn – t), Σν.Τ n=1

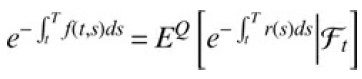

Use the banking account as a num?raire to show that has to hold. le-S" ro»d|/

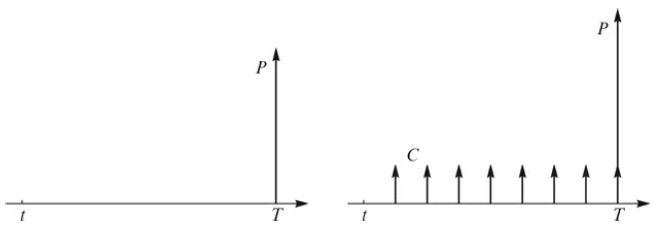

Relate this formula to Figure 18.1 right. Figure 18.1 т

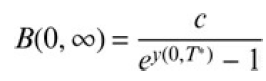

A consol is a perpetual bond that pays coupons forever, without repaying the principal. Consider a standardized consol, issued today at t = 0, with annual coupon payments c. Show that the relation between price and yield to (average) maturity holds. B(0, 0) = e0,T°) – 1

Show that in the Black–Scholes-framework, the Esscher-transform of the Wiener-process Wt is equivalent to the Girsanov-transformation.

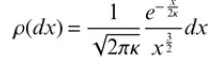

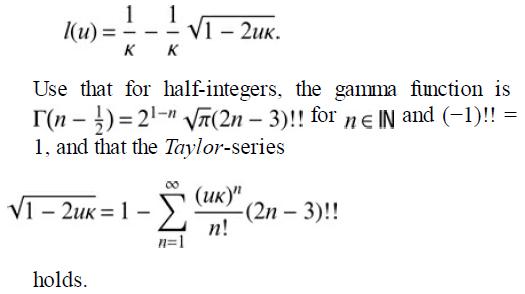

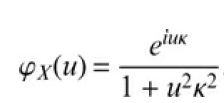

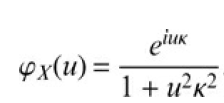

The normal inverse Gaussian process is a subordinated Brownian motion, where the subordinator is a process with drift η = 0, and Levy-measure Prove that the Laplace-exponent is e- -dx p(dx) = V2лк х2 I(и) — VI - 2ик к к

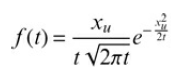

Suppose xu is an upper barrier. Use the reflection principle to prove that with t ? 0, is the probability density function of the stopping time ?, when the Wiener-process Wt hits the barrier xu for the first time. Хи f(t) = I V2лt

Analyze the characteristic exponent of the Kou-model of Problem 17.2. What is the proper drift adjustment to obtain the exponential Q-martingale Yt and is the necessary strip condition satisfied? Problem 17.2 The double exponential jump-diffusion of Kou (2002) replaces the log-normal distributed

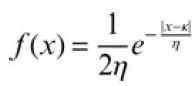

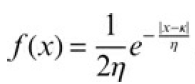

The double exponential jump-diffusion of Kou (2002) replaces the log-normal distributed jumps of the Merton-model, by Laplace-distributed ones, with probability density function and 0 f(x) = 27 eiux ex(u) = 1 + u?k?

Consider the random variable N ∼ Poi(λ), which has expectation value E[N] = λ. Show that the variance is also Var[N] = λ.

Consider the SABR-model with β = 1. Show that the at-the-money smile for F0 = K ± δ, with small δ, is symmetric. Use that δ is so small that O(δ2) terms can be neglected.

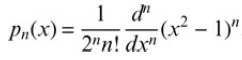

Polynomials, orthogonal with respect to the weighting function w(x) = 1 in the interval [?1, 1], are called the Legendre-polynomials. They are generated by? Compute the Legendre-polynomials up to N = 2, as well as the associated quadrature points and weights. 1 ф dxт (x — 1уч1 P, (х) %3D -

Prove that the payoff function of a protective put position W(x) = max (ex, K) has no transformed payoff function ŵ(z), regular in a connected strip Sw = {z = u + iv: v ∈(α, β)}.

Shifting the integration contours to v = 0 and v = 1, respectively, the complex line integrals in Problem 16.2 become principal value integrals and pick up one half of the associated residue. The result is where again k = log(S0/K) + bT. Show that the call price can be expressed in a completely

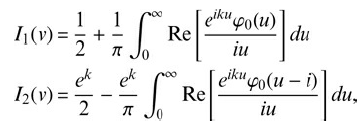

Show that the fair price of a European plain vanilla call option can be represented as where I1(v) and I2(v) are the complex line integrals evaluated along the contour v ? (0, 1). Co(K, T) = eb-1)T S, – e-rT K(I((v) + I½(v)), iv+0o niv+o 1(v) = 2л Фо(-2)-dz and h)- *go(-2)-dz, e-izk 2л

Derive the extended Black–Scholes-equation for the Heston-model.

The Heston?Nandi-model for option pricing (Heston and Nandi, 1997, 2000) is specified as where zt?is again independent and identically standard normally distributed. In going from probability measure P to Q, the model can be written in unchanged algebraic form but with the substitutions ? ? ?Q,

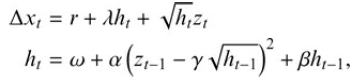

The Duan-model is a modified version of the GARCH-in-mean specification where again ?t = ?htzt, and zt ? N(0, 1). Show that under the asymmetric variance dynamics Ax, = µ + Ah, + E %3D

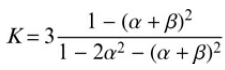

Show that the kurtosis in an ordinary GARCH(1,1)-model is K=3- 1- (a + B)? 1- 2a2 – (a + B)?

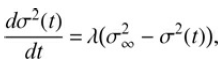

Assume that actual variance has the mean reverting term structure where ?2?is the stationary variance and ?2(0)?=??20. What is the implied volatility of an option at time t = 0? (t) do²(1) = 1(o - o²(1), dt

Consider a floating strike version of an exponential arithmetic Asian call (Problem 14.6) with European exercise right, contingent on a forward contract with TF > T. Assume that S0, T, r, σ, and λ are known. Additionally, the option is knocked out, if ST/2 ≤ S̅T/2 holds. Create a

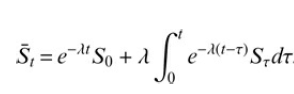

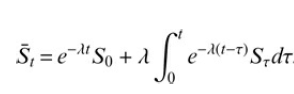

A continuously exponential averaged arithmetic Asian option is a contract, where the average price of the underlying is computed as The parameter ? ? 0 is an arbitrary weight factor. Rewrite the averaging condition in differential form and explain the effect of the parameter ?. Š, = e-" So + A

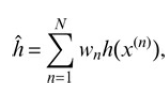

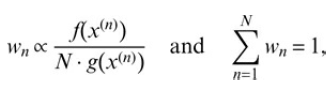

An important variance reduction technique in Monte Carlo simulation is importance sampling. The idea behind this concept is to approximate an expectation by a weighted average value where the normalized weights are proportional to the so-called likelihood ratio and the sampling is conducted

Monte Carlo simulation approximates an unknown expectation value by an arithmetic mean, computed from a random sample. This mean can be understood as the expectation value with respect to the estimated probability density Show that for an arbitrary function h(x), the arithmetic mean is the

Suppose the underlying S follows the standard geometric Brownian motion Use the associated Fokker?Planck-equation, together with the definition of the probability current to prove that the probability mass is conserved over time, Assume that the probability density function p(S, t) is a

A power option is a contract, whose value depends on the payoff V(S, T), with S = Sa. Show that the generalized Black–Scholes-equation can be expressed in terms of , with adjusted cost-of-carry rate badj. and volatility σadj..

Verify that the mixed boundary conditions x(0) = c1 and x?(?) = c2 require the solution x(t) = c1 cos t ? c2 sin t of (14.25). (14.25) dx(1) = -x(t) dt?

Derive an explicit formula for the value of the liabilities in the Merton-model of the firm value.

There is another Greek called vanna, defined by the mixed partial derivative Derive the vanna of a European plain vanilla contract and show that it is identical for both put and call options. vanna aSdo

Prove that the so-called European put-call symmetry holds in the generalized Black?Scholes-framework. ( e2b(T=1) S; K |C,(K, T) = eb(T-1) S, K

Consider the fair price of a European plain vanilla binary contract in the Black– Scholes-framework. What is the delta of a binary call and put option?

The evolution of the bank account is governed by which can be understood as geometric Brownian motion with ? = 0. Manipulate the resulting Black?Scholes-equation to show that it is equivalent to the so-called transport equation with the substitution V(B, t) = e?r(T?t)U(B, t) and x = log B. dB(t)

In demonstrating the transition from the binomial model to the Black?Scholesmodel, the parametrization u/d = e????t chosen in step 3, with ?t = ?/T.?Show that the martingale principle results in the same risk-neutral probability? if the u/d-parametrization is Taylor-expanded to second order. VAi,

Imagine the stopping time τ is a fixed deterministic time τ = s, with 0 < s < T. What are the stopping events?

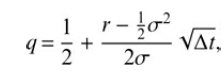

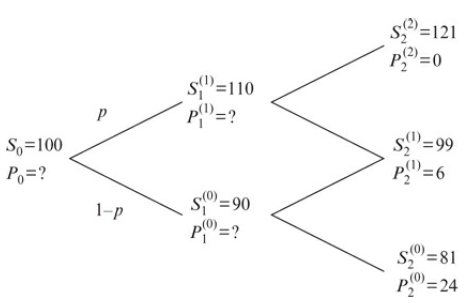

Look at the binomial tree in Figure 12.14. Assume that the risk-free interest rate vanishes, r = 0%, and price the European plain vanilla put option by computing the hedge-portfolios ?(1)1, ?(1)1 and ?0. Fig. 12.14?Binomial tree for European plain vanilla put option. s=121 S"=110 P"=? s"=99 P"=e

Assume an investor holds long positions in a covered call and a protective put. Both options have identical expiries and exercise prices. What is the payoff of this combined position at expiry?

Describe the position an investor holds, if she is long in a covered call and short in a protective put, with both options having the same exercise price and time to expiry.

It is possible to generalize the butterfly position even more to the form with K12 3, and a, b > 0 How are the coefficients a and b to be chosen, to generate a vanishing payoff for ST ? K1 and ST ? K3? IIButterfly = C(K1, T) – a · C(K2, T) +b. C(K3, T)

Consider a modified butterfly position with K12 3, and a > 0. How is a to be chosen to guarantee a vanishing payoff for ST = K1 and ST = K3? IlButterfly = C(K1, T) – a · C(K2, T) + C(K3, T) %3D

Establish a parity relation for binary calls and puts by adding their payoff functions and derive a formula for 0 ≤ t ≤ T.

Sketch the arbitrage portfolio for the contract initiated at t = τ.

An option that pays off one unit of currency at expiry, in case of ST ≥ K, and zero else, is called a binary or digital call option. Likewise a binary put option pays one unit of currency, if ST < K holds, and nothing otherwise. Sketch the payoff function of a binary call and put.

Showing 3400 - 3500

of 4319

First

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

Last

Step by Step Answers