New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

marketing strategy planning

Global Taxation How Modern Taxes Conquered The World 1st Edition Philipp Genschel, Laura Seelkopf - Solutions

Gaylord Gunnison (GG) died January 13, 2018, and his gross estate consisted of three properties-cash, land, and stock in a public company. The amount of cash on the date of his death was $10.9 mill ion, which went into the estate. On January 13, 2018, the land had a fair market value of $1 million,

Bonnie died on June 1, 2018, survived by her husband, Abner, and two sons, Carl and Doug. Bonnie's only lifetime taxable gift was made in October 2015 in the taxable amount of $6.25 million. She did not elect gift splitting. By the time of her death, the value of the gifted property (stock) had

Giovanni died in 2018 with a gross estate of $13.9 million and debts of $30,000. He made post-1976 taxable gifts of $100,000, valued at $80,000 when Giovanni died. His estate paid state death taxes of $110,200. Calculate his estate tax base.

Elaine died on May 1, 2018. Her gross estate consisted of the fol lowing items: Cash ..................................................................$ 40,000

Joseph Jernigan died in 2018 with a taxable estate of $4.1 million. He was survived by his spouse Josephine and several children. He made taxable gifts of $100,000 in 1974 and $650,000 in 2000. The property given in 1974 was valued at $425,000 when he died, and the property given in 2000 was valued

Maria Martinez died in 2018, survived by her spouse, Sergio, and two adult children. Her gross estate, all of which passed under her will, was valued at $17.2 million. She had Sec. 2053 deductions of $100,000. Her will left $200,000 to her church, 20% of her gross estate to her spouse, and the rest

Bess, a widow, died in October 2018. Her gross estate, which totaled $12.5 million, included a $100,000 life insurance policy on her life that she gave away in 2016. The taxable gift that arose from giving away the policy was $15,000. In December 2014, Bess made a $740,000 taxable gift of stock

Will, a bachelor, died in 2018. At that time, his sole asset was cash of $15 million. Assume no debts or funeral and administration expenses and no charitable bequests. His gift history was as follows:a. What was Will's estate tax base? b. How would your answer to Part a change if Will made

Sam Snider died February 14, 2017, survived by his spouse Janet and several children. Sam had not made any taxable gifts. Sam's gross estate was $7 million. In each of the following independent situations, indicate the amount of Sam's basic exclusion amount that is portable to Janet and that can be

Assume the same facts as in Problem C:13-48 and that before Yuji's death in 2018 his wife already owned property valued at $300,000. Assume that each asset owned by each spouse increased 8% in value by the surviving spouse's date of death later in 2018 and that Yuji's executor elected to claim the

When Yuji died in March 2018, his gross estate was valued at $15 million. He owed debts tota ling $300,000. Funeral and administration expenses were $12,000 and $120,000, respectively. The marginal estate tax rate exceeded his estate's marginal income tax rate. Yuji willed his church $300,000 and

Ten years ago, Art purchased land for $60,000 and immediately titled it in the names of Art and Bart, joint tenants with right of survivorship. Bart paid no consideration. In 2018, Art died and was survived by Bart, his brother. The land's value had appreciated to $300,000.a. What was the amount of

Twelve years ago, Latoya transferred property to an irrevocable trust with a bank trustee. Latoya named AI to receive the trust income annually for life and Pat or Pat's estate to receive the remainder upon Al's death. Latoya reserved the power to designate Mike or Mike's estate (instead of Pat or

John died in 2018. What amount, if any, was included in his gross estate in each of the following situations:a. In 1997, John created a revocable trust, funded it with $400,000 of assets, and named a bank as trustee. The trust instrument provided that the income is payable to John annually for

In December 2015, Curt and Kate elected gift splitting to report $16,228,000 of gifts of stocks Curt made to Curt, Jr. Each paid gift taxes of $1,068,000 by spending his or her own funds. Kate died in January 2018 and was survived by Curt. Her only taxable gift was the one reported for 2015. When

Val died on May 13, 2018. On July 3, 2015, she gave a $400,000 life insurance policy on her own life to son Ray. Because the value of the policy was relatively low, the transfer did not cause any gift tax to be payable.a. What amount was included in Val's gross estate as a result of the 2015

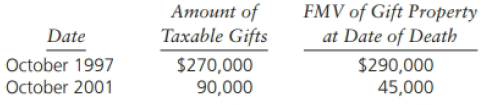

Sue died on May 3, 2018. On October 1, 2015, Sue gave her son Tom land valued at $7,014,000. Sue applied a unified credit of $2,117,800 against the gift tax due on this transfer. On Sue's date of death the land was valued at $9.4 mill ion.a. With respect to this transaction, what amount was

Mary died on April 3, 2018. As of this date, Mary's gross estate was valued at $16.5 million. On October 3, Mary's gross estate was valued at $15.8 million. The estate neither distributed nor sold any assets before October 3, 2018. Mary's estate had no deductions or adjusted taxable gifts. What was

Beth died on May 3, 2018. Her executor elected date-of-death valuation. Beth's gross estate included, among other properties, the items listed below. What is the estate tax value of each item?a. 4,000 shares of Highline Corporation stock, traded on a stock exchange on May 3, 2018 at a high of 30, a

Jeung Hong, a widower, died in March 2018. His gross estate was $14.5 million and, at the time of his death, he owed debts of $60,000. His will made a bequest of $200,000 to his undergraduate alma mater and left the rest of his properry to his children. His administrative expenses were $75,000.

Your firm has prepared the estate tax return (Form 706) for the Estate of Belinda Baker, a widow who died January 13, 2018. Besides substantial amounts of cash, mostly in certificates of deposit, she owned ABC stocks valued at $3.2 million, TUV stocks valued at $4.5 million, and 200 acres of

George Tanner died October 2, 2017, survived by his son Thomas and his daughter Gigi Tanner Stewart and her children, Sam and Cindy. George was the sole stockholder of Tanner, Inc., a C corporation. Gigi served as president of Tanner from its inception until early January 2018. However, she never

Sam and Taylor, residents of New Jersey, entered in to a domestic partnership in New Jersey in October 2004. However, they never obtained a marriage license. Sam died in March 2018, survived by Taylor. Sam's gross estate totals $13.2 million, he owed debts of $ 100,000, and funeral and

In May 2008, Jasper Mason died, survived by his spouse Amber Mason and four adult children. His gross estate was valued at $3 million, and he had Sec. 2053 deductions of $120,000. His will left the personal residence on which the mortgage had been paid off to Amber. Its value was $450,000. The will

Arthur Zolnick died at age 84 on June 7, 2017. In March 2008, he transferred $4 million of stock to a charitable remainder annuity trust (CRAT) from which he named himself to receive $200,000 per year for life. He designated a charitable organization to receive the remainder interest after his

Your client is Jon Jake, the executor of the Estate of Beth Adams, a widow. Mrs. Adams died 11 years after the death of her husband, Sam. Mr. Jake seeks assistance in the preparation of the estate tax return for Mrs. Adams, whose estate consists primarily of real estate. Mrs. Adams's estate will be

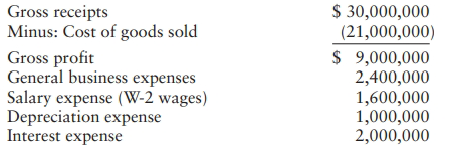

Epsilon Corporation, which does not qualify as a small business corporation, incurred a $10 mill ion NOL in the current year. It expects to earn relatively low amounts of net income for the next several years and also to incur substantial interest costs on amounts borrowed to finance operations and

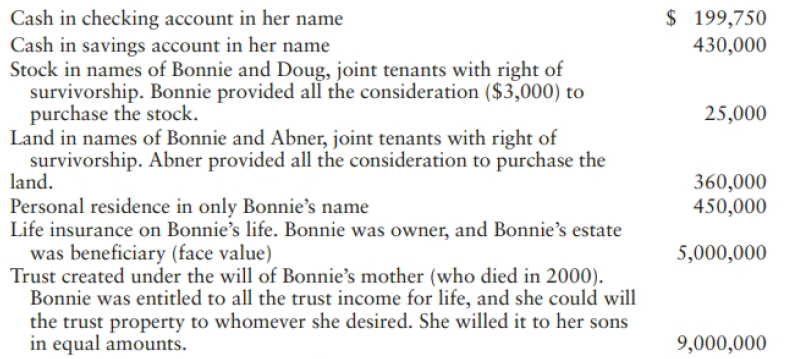

Annie James died early in 2018. All her property passed subject to her will, which provides that her surviving husband, Dave James, is to receive all the property outright. Her will further states that any property Dave disclaims will pass instead to their children in equal shares. Annie's gross

What was the Sec. 7520 rate for May, June, and July 2017?

On August 3, 2015 Ginger Grayson, a widow, transferred $55,000 to each of two Sec. 529 plans (qualified tuition programs), one for grandson Greg Grayson and one for granddaughter Gayle Grayson. Her tax preparer, not a CPA, prepared a Form 1040 (individual income tax return) for Ginger for 2015 and

Janet Mason timely filed a 2016 gift tax return to report the gift on June 3, 2016, of closely held stock in Mason Meat Co., Inc. The tax return, which your firm prepared, reflected a value of $1,500 per share (determined by an appraiser) and a taxable gift of $6.3 million. This was Janet's first

Your manager advises you that clients Mike and Winona Marsh, residents of Bath, Maine, acquired beachfront property in Maine in 2002 and titled the property in their names as joint tenants with right of survivorship. Under Maine law, either joint tenant can sever the joint tenancy unilaterally.

Morris Jory, a long-time tax client of the firm that employs you, has made substantial gifts during his lifetime. Mr. Jory transferred Jory Corporation stock to 14 donees in December 2017. Each donee received shares valued at $14,000. Two of the donees were Mr. Jory's adult children, Amanda and

George and Martha, spouses, made a number of gifts during 2018. Their accountant is trying to help them decide whether to elect gift splitting. If they elect gift splitting, each spouse will have $8 million of taxable gifts. If they do not elect gift splitting, George's taxable gifts will be $2

In 2018, Ginger Graham, age 46 and wife of Greg Graham, engaged in the transactions described below. Determine Ginger's gift tax liability for 2018 if she and Greg elect gift splitting and Greg gave their son Stevie stock valued at $80,000 during 2018. Ginger's grandmother Mamie died November 12,

In June 2017, Karen transferred property with a $75,000 FMV and a $20,000 adjusted basis to Hal, her husband. Hal dies in March 2018; the property has appreciated to $85,000 in value by then. His gross estate is $1 million.a. What is the amount of Karen's taxable gift for 2017?b. What gain would

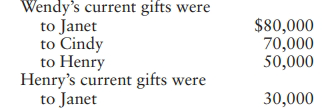

In 2018, Henry and his wife, Wendy, made the gifts shown below. All gifts are of present interests. What is Wendy's gift tax payable for 2018 if the couple elects gift splitting and Wendy's previous taxable gifts (made in 1995) total $1 million? Wendy's current gifts were to Janet to Cindy to Henry

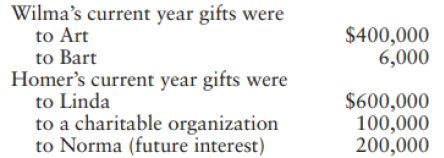

In 2018, Homer and his wife, Wilma (residents of a noncommunity property state) make the gifts listed below. Homer's previous taxable gifts consist of $100,000 made in 1975 and $1.4 million made in 1996. Wilma has made no previous taxable gifts. a. What are the gift tax liabilities of Homer

In earlier years, neither Hugo nor Wanda, his wife, made any taxable gifts. In 2017, Hugo gave $14,000 cash to each of his nieces, nephews, and grandchildren, 30 persons in total. In 2018, Wanda gives $34,000 of stock to each of the same people. What is the minimum legal gift tax liability before

During 2018, Will gives $40,000 cash to Will, Jr. and a remainder interest in a few acres of land to his friend Suzy. The remainder interest is valued at $32,000. Will and his wife, Helen, elect gift splitting, and during the current year Helen gives Joyce $8,000 of stock. What is the total amount

In March 1976, Sue made a taxable gift of $200,000. In arriving at the amount of her taxable gift, Sue elected to deduct the $30,000 specific exemption then available. In 2018, Sue makes her next gift; the taxable amount is $13 mill ion. a. What unified credit can Sue claim on her 2018

Refer to the facts of Problem C: 12-36 and assume the current year is 2018. Emily's prior gifts are as follows:Year . . . . . . . . . . . . . . . . . . . . Amount of Taxable Gifts1974 . . . . . . . . . . . . . . . . . . . .$ 500,0001998. . . . . . . . . . . . . . . . . . . . 1,000,000What is

In the current year, Emily, a widow, engages in the following transactions. Determine the amount of the completed gift, if any, arising from each of the following occurrences.a. Emily names Lauren the beneficiary of a $100,000 life insurance policy on Emily's life. The beneficiary designation is

Amir made taxable gifts as follows: $800,000 in 1975,$1.2 million in 1999, and $600,000 in 2018. What is Amir's gift tax liability for 2018?

In 2018, Sondra makes taxable gifts aggregating $300,000. Her only other taxable gifts amount to $200,000, all of which she made in 1997.a. What is Sondra's 2018 gift tax liability?b. What is her 2018 gift tax liability under the assumption that she made the $200,000 of taxable gifts in 1974

Kwambe is thinking of making a substantial gift of stock to his fiancee, Maya. The wedding is scheduled for October 1 of the current year. Assume Kwambe already has exhausted his unified credit. He also is considering giving $30,000 cash this year to each of his three children by a previous

In 2008, Frank made an installment sale of real property to Stu, his son, for $1 million with payments due over a 10-year period. Frank did not file a gift tax return. For 2016, Frank reported taxable gifts so large that he used all of his unified credit then available. In 2018, the IRS audits

Assume the same facts as in Problem C:12-21 and that Marcy has decided to give Phil property valued at $11 mill ion. Phil probably will leave the gifted property to their children under his will. a. What are the gift tax consequences to Marcy and the estate tax consequences to Phil of the

Phil and Marcy have been married for a number of years. Marcy is very wealthy, but Phil is not. In fact, Phil, who has only $200,000 of property, is very ill, and his doctor believes that he probably will die within the next few months. Make one (or more) tax planning suggestions for the couple.

Both Damien and Latoya make taxable gifts of $250,000 in the current year. Will their current year gift tax necessarily be identical? Explain.

What is the purpose of the gift tax annual exclusion?

Alice, a married taxpayer, will form Morning Corporation in the current year. Alice plans to acquire all of Morning's common stock for a $1 mill ion contribution to the corporation. Morning will obtain additional capital by borrowing $200,000 from a local bank. Morning will conduct a variety of

Cara, Bob, and Steve want to begin a business on January 1, 2019. The individuals are considering three business forms-C corporation, partnership, and S corporation.• Cara has investment land with a $36,000 adjusted basis and a $50,000 FMV that she is willing to contribute. The land has a rundown

Tina, a single taxpayer, owns 100% of Rocket Corporation, an S corporation. She has an $80,000 stock basis for her investment on January 1 of the current year (Year 1). During the first 11 months of Year 1, Rocket reports an ordinary loss of $100,000. The corporation expects an additional $20,000

Tango Corporation, a calendar year taxpayer, has been an S corporation for several years. Tango's business activities have become very profitable in recent years. On June 16, 2018, its sole shareholder desires to revoke the Selection. a. How does Tango revoke its Selection? When does the

Orlando Corporation, a calendar year taxpayer, has been an S corporation for several years. On July 9, 2018, Orlando authorizes a second class of nonvoting preferred stock that pays a 10% annual dividend. The corporation issues the stock to Sid on September 11, 2018, to raise additional equity

Voyles Corporation, a calendar year taxpayer formed five years ago, desires to make an Selection beginning in 2019. Sue and Andrea each own one-half of the Voyles stock.a. How does Voyles make the Selection?b. When can Voyles file its election form?c. If in Part b the corporation does not file the

Carl Carson, a single taxpayer, owns 100% of Delta Corporation. During 2018, Delta reports $150,000 of taxable income. Carl reports no income other than that earned from Delta, and Carl claims the standard deduction.a. What is Delta's income tax liability assuming Carl withdraws none of the

Julio, age 50, is a U.S. citizen who has a 22% marginal tax rate. He has operated the A&B Automotive Parts Company for a number of years as a C corporation. Last year, A&B reported $200,000 of pre-tax profits, from which it paid $50,000 in salary and $25,000 in dividends to Julio. The

Refer to the facts in Comprehensive Problem C:6-54. Now assume the entity is a partnership named Lifecycle Partnership. Additional facts are as follows:• Except for precontribution gains and losses, the partners agree to share profits and losses in a 60% (Able)-40% (Baker) ratio.• The partners

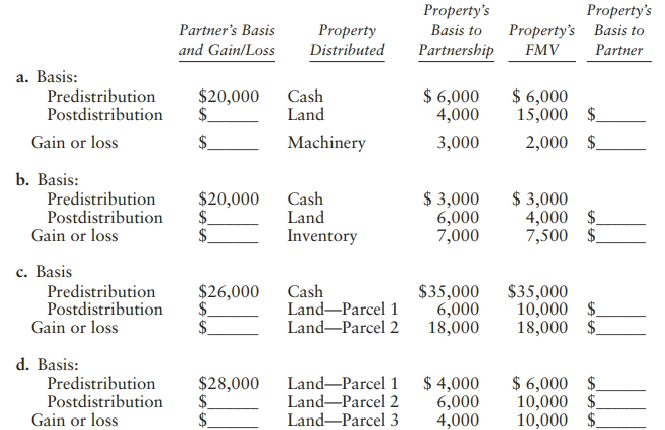

Assume the same four independent distributions as in Problem C:10-23. Fill in the blanks in that problem assuming the only change in the facts is that the distributions are now liquidating distributions instead of nonliquidating distributions.Data from C:10-23: Property's Property's Property's

The Net Partnership has four partners, with each having a 25% interest in the partnership. The partners share all losses equally, but in accordance with a special allocation, the partnership agreement allocates a ll gains and profits to Partners 1, 2, and 3, but none to Partner 4. The partnership

The JKL Partnership has three partners with the following interests: Jason 55%, Kathy 25%, and Louis 20%. Will the partnership terminate if jason sells his entire interest to Maurice?

Caitlin and Wally formed the C & W Partnership on September 20,2018. Caitlin contributed cash of $195,000, and Wally contributed office furniture with a FMV of $66,000. He bought the furniture for $60,000 on January 5, 2018, and placed it in service on that date. Wally did not elect Sec. 179

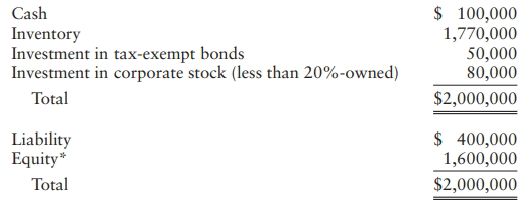

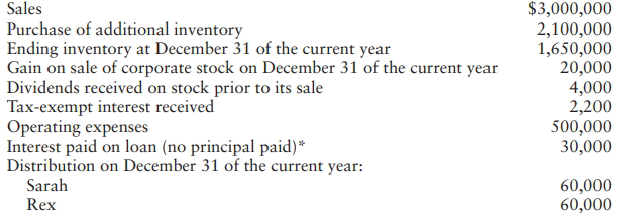

Sarah and Rex formed SR Entity on December 28 of last year. The entity operates on a calendar tax year. Each individual contributed $800,000 cash in exchange for a 50% ownership interest in the entity (common stock if a corporation; partnership interest if a partnership). In addition, the entity

Refer to Example C:9-27 in the text. Provide computations showing that the partners' total tax liability under the special allocation is less than their total liability under an equal allocation of the two types of interest income.

Charlene is an equal partner in the CD Partnership. The partnership does not qualify as a small business under the $25 million gross receipts text. The partnership incurred the following items for the current year.Charlene is single, has no other sources of income, and claims the standard

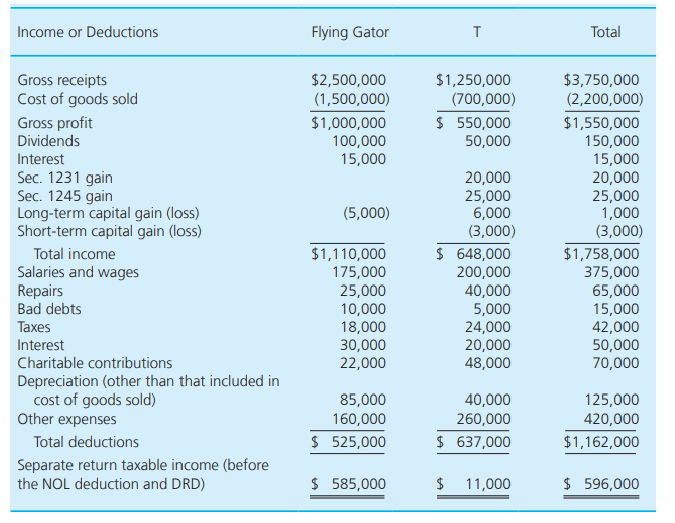

Using the facts from Problem C:8-67 below, calculate the tax liabilities of Flying Gator and T Corporations for 2017. How much larger (or smaller) would be the total of the two separate return tax liabilities if they were to file separate tax returns than the affiliated group's consolidated return

P Corporation acquires all of S Corporation's stock at the beginning of the current year in a transaction that qualifies as a Sec. 382 ownership change. P and S elect to file a consolidated tax return for the current yea r. At the time of the acquisition, S has $900,000 of pre-2018 NOLs it has not

P and S Corporations comprise an affiliated group that files separate tax returns. P and Shad no intercompany inventory sales before the current year (Year 1). P and S use the first-in, first-out (FIFO) inventory method. During Year 1, S sells 40,000 widgets to P, earning $7 per unit profit on the

P Corporation owns 100% of S Corporation's stock, and S owns 100% of T Corporation's stock. The three corporations have filed consolidated tax returns for several years. On January 1 of the current yea r, P's basis for its S stock is $5 million, and S's basis for its T stock is $3 million. The

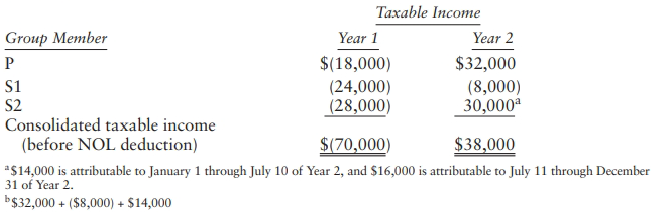

Corporation owns all the stock of S1 and S2 Corporations. The corporations have filed consolidated tax returns since their creation in Year 1. At the close of business on July 10 of Year 3, P sells all of its 52 stock. The group reports the following results:In what year(s) can the corporations

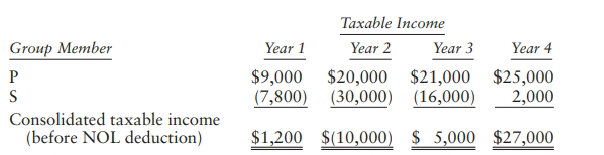

P and S Corporations form in Year 1, with S as P's wholly-owned subsidiary. The corporations immediately elect to file consolidated tax returns. The group reports the following results:In what year(s) can the group deduct the Year 2 consolidated NOL? Assume that Year 2 is 2018 or a later year.

Peoria and Salem Corporations have filed consolidated tax returns for several years. For the current year, consolidated taxable income is $300,000. The consolidated general business credit (computed without regard to the overall limitation) is $15,000.a. What is the group's federal tax liability?b.

P Corporation uses the calendar year as its tax year and the accrual method as its overall accounting method. S Corporation uses a fiscal year ending June 30 as its tax year and the cash method as its overall accounting method. On July 31, 2019, P acquires all of S's stock, and the P-S affiliated

Sid Kess, a long-time tax client of yours, has decided to acquire the snow blower manufacturing firm owned by Richard Smith, one of his closest friends. Richard has a $200,000 adjusted basis in his Richard Smith Snow Blowers (RSSB) stock. Sid Kess Enterprises (SKE), a C corporation 100%-owned by

At the beginning of the current year, Allegro Corporation acquires all of Tempo Corporation's stock in a Type B reorganization. At the time of the acquisition, Tempo's stock has a $900,000 FMV, and Tempo has a $115,000 net operating loss (NOL) carryover. Assuming a 3.25% long-term tax-exempt

Albert Corporation is a profitable publicly traded corporation. None of its shareholders owns more than 1% of its outstanding shares. On December 31, 2017, Albert exchanged $8 million of its stock for all the stock of Turner Corporation as part of a merger. Turner is owned by Tara, who receives 15%

Murray Corporation's stock is owned by about 1,000 shareholders, none of whom own more than 1% of the outstanding shares. Pursuant to a tender offer, Said purchased all the Murray stock for $7.5 million cash at the close of business on December 31, 2017. Before the acquisition, Said owned no Murray

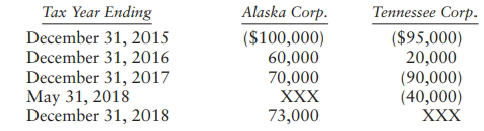

At the close of business on May 31, 2018, Alaska Corporation exchanges $2 million of its voting common stock for all the noncash assets of Tennessee Corporation. Tennessee uses its cash to pay off its liabilities and then liquidates. Tennessee and Alaska report the following taxable income

Parent Corporation has owned all 100 shares of Subsidiary Corporation common stock since 2011. Parent has been in the business of manufacturing and selling light fixtures, and Subsidiary has been in the business of manufacturing and selling light bulbs. Amy and Bill are the two equal shareholders

Silvia exchanges all her Theta Corporation stock (acquired August 1, 2014) for $300,000 of Alpha Corporation voting common stock pursuant to Theta's merger into Alpha. Immediately after the stock-for-stock exchange Silvia owns 25% of Alpha's 2,000 outstanding shares of stock. Silvia's adjusted

Alpha Corporation purchases 20% of Theta Corporation stock from Milt on August 10 of the current year. Alpha purchases an additional 30% of the stock from Nick on November 15 of the current year. Alpha purchases the remaining 50% of the Theta stock from Phil on April 10 of the following year. The

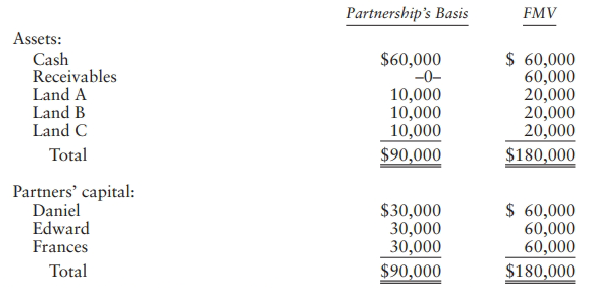

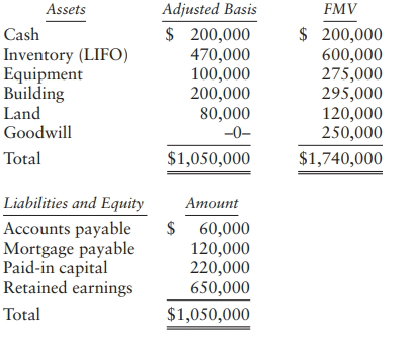

The following facts pertain to Lifecycle Corporation: • Able owns a parcel of land (Land A) having a $30,000 FMV and $16,000 adjusted basis. Baker owns an adjacent parcel of land (Land B) having a $20,000 FMV and $22,000 adjusted basis. On January 2, 2018, Able and Baker contribute their

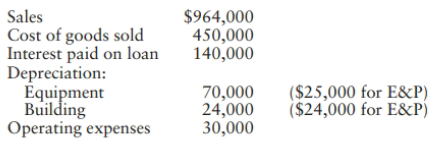

Howard Corporation conducts a manufacturing business and has a compelling need to accumulate earnings. Its January 1, E&P balance is $600,000. It reports the following operating results for the current year:Other information relating to Howard's current year operations is as follows:NOL

Century Cleaning, Inc. provides cleaning services in Atlanta, Georgia. It is not a member of a controlled or an affiliated group. Century reports the following results for the current year:Taxable income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $500,000Federal

In the current year, Kennedy Corporation is deemed to be a PHC and reports the following results: Taxable income . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $400,000Federal income taxes .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Rick owns investments that generate $20,000 of ordinary income per year (4% annual before-tax rate of return). In each part, determine how much higher or lower Rick's after-tax income would be if he transfers the investments to his wholly-owned corporation rather than owning them himself, assuming

Angela forms a corporation during the current year to conduct her new business. The corporation is a C corporation, and Angela is its only shareholder. Is the corporation potentially subject to the personal holding company tax or the accumulated earnings tax?

Your friend Carlos often asks you about tax avoidance strategies. He heard that he can reduce his taxes by putting his investments in a corporation and asks you whether this is true. Explain to Carlos the issues surrounding this strategy.

John died on March 3, 2018. His gross estate of $16.5 million includes First Corporation stock (400 of the 1,000 outstanding shares) worth $10 million or $25,000 per share ($10,000,000/400). This FMV amount also is the estate's basis in the stock (see Chapter C:13). John's wife, Myra, owns the

Forward Corporation is owned by a group of 15 shareholders. During the current year, Forward pays $550,000 in salary and bonuses to Alvin, its president and controlling shareholder. The corporation's tax rate is 21%, and Alvin's marginal tax rate is 37% for ordinary income and 23.8% (20% + 3.8% on

For many years preceding 2018, Minimis Corporation, a calendar year corporation, had incurred the alternative minimum tax (AMT) and as a result has a $2 million minimum tax carryover into 2018. However, the Tax Cuts and Jobs Act of 2017 repealed the corporate AMT for tax years beginning after 2017.

Mike Barton owns Barton Products, Inc. The corporation has 30 employees. Barton Corporation expects $800,000 of net income before taxes in 2018. Mike is married and files a joint return with his wife, Elaine, who has no earnings of her own. Mike and Elaine have no other income, file a joint tax

In the current year, Alpha Corporation generated $500,000 of ordinary operating income and incurred a $20,000 capital loss on the sale of marketable securities from its investment portfolio. Alpha expects to generate $500,000 of ordinary operating income in each of the next five years. Alpha

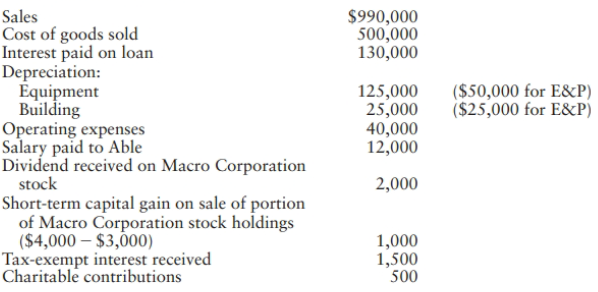

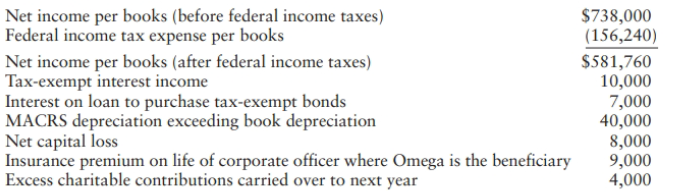

Omega Corporation reports the following results for the current year:a. Prepare a reconciliation of Omega's taxable income before special deductions with its book income.b. Prepare a tax provision reconciliation as in Step 9 of the Tax Provision Process. Assume a 21% tax rate. Net income per books

Wright Corporation's taxable income for calendar years 2015, 2016, and 2017 was $120,000, $150,000, and $100,000, respectively. Its total tax liability for 2017 was $22,250 (under the tax rates in effect that year). Wright estimates that its 2018 taxable income will be $600,000, on which it will

Zeta Corporation's taxable income for 2017 was $1.1 million, on which Zeta paid federal income taxes of $374,000 (at its then 34% tax rate). Zeta estimates calendar year 2018's taxable income to be $2 million, on which it will owe $420,000 in federal income taxes.a. What are Zeta's minimum

Refer to the facts in Problem C:3-53. Elizabeth has read an article explaining the advantages of paying nontaxable fringe benefits (premiums on group term life insurance, accident and health insurance, etc.) and having deferred compensation plans (e.g., qualified pension and profit-sharing plans).

Elizabeth owns 100% of Omega Corporation's stock and also runs the company as its CEO. Omega is a C corporation that expects to earn $400,000 before deducting any salary paid to Elizabeth. Elizabeth wants the corporation to pay her $250,000 for the current year in pre-tax dollars. She is

Showing 3600 - 3700

of 4319

First

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

Step by Step Answers