New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

modern advanced accounting

Modern Advanced Accounting in Canada 8th edition Hilton Murray, Herauf Darrell - Solutions

What should happen if a foreign subsidiary's financial statements have been prepared using accounting principles different from those used in Canada?

Define a foreign operation as per lAS 21.

How are gains and losses on financial instruments used to hedge the net investment in a foreign operation reported in the consolidated financial statements when the PCT method is used to translate the foreign operation?

The FCT and PCT methods each produce different amounts for translation gains and losses due to the items at risk. Explain.

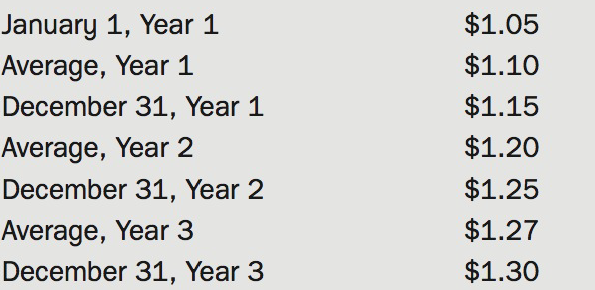

On January 1, Year 4, a Canadian firm, Canuck Enterprises Ltd., borrowed US$208,000 from a bank in Seattle, Washington. Interest of 7.5% per annum is to be paid on December 31 of each year during the four-year term of the loan. Principal is to be repaid on the maturity date of December 31, Year 7.

As a result of its export sales to customers in Switzerland, the Lenox Company has had Swiss-franc-denominated revenues over the past number of years. In order to gain protection from future exchange rate fluctuations, the company decides to borrow its current financing requirements in Swiss

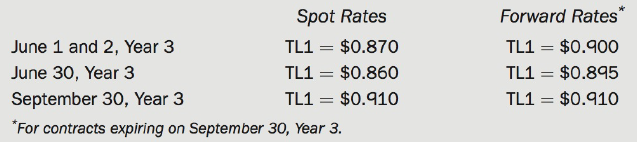

On June 1, Year 3, Forever Young Corp. (FYC) ordered merchandise from a supplier in Turkey for Turkish lira (TL) 217,000. The goods were delivered on September 30, with terms requiring cash on delivery. On June 2, Year 3, FYC entered a forward contract as a cash flow hedge to purchase TL217,000 on

On May 1, Year 1, JDH orders equipment from a supplier in Germany for €100,000 with delivery scheduled for October 1, Year 1. Payment is due on December 31, Year 1. On May 2, Year 1 JDH enters into an 8-month forward contract with its bank at a rate of €1 = $1.38 to purchase €100,000 on

Gemella Ltd. manufactures construction equipment for sale throughout eastern Canada and northeastern United States. Its year-end is June 30. The following foreign currency transactions occurred during the Year 11 calendar year:1. On January 10, Gemella agreed to sell equipment to an American

On January 1, Year 5, Ornate Company Ltd. purchased US$2,200,000 of the bonds of the Gem Corporation. The bonds were trading at par on this date, pay interest at 12% each December 31, and mature on December 31, Year 7. The following Canadian exchange rates were quoted during Year 5:January 1, Year

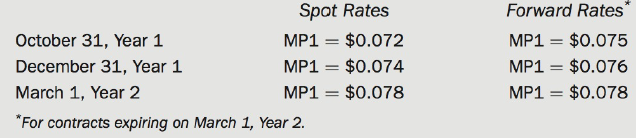

Lamont Company is a Canadian company that produces electronic switches for the telecommunicationsindustry. Lamont regularly imports component parts from Sousa Ltd., a supplierlocated in Mexico, and makes payments in Mexican pesos (MP). Based on past experience, Lamont Company expects to purchase

Assume that all of the facts in Problem 1 remain unchanged except that MEl uses hedge accounting. Also, assume that the forward element and spot elements on the forward contract are accounted for separately.Required(a) Prepare the journal entries for the same items as in part (a) of Problem 1

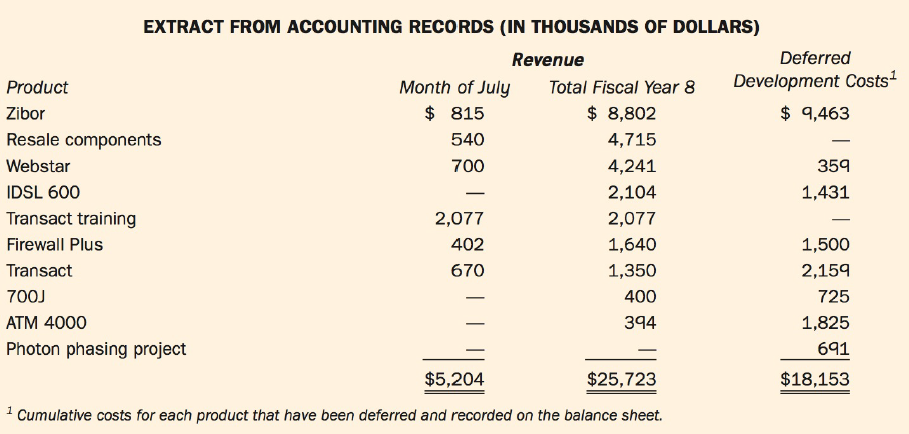

ZIM Inc. (ZIM) is a high-technology company that develops, designs, and manufactures telecommunications equipment. ZIM was founded in Year 5 by Dr. Alex Zimmer, the former assistant head of research and development at a major telephone company. He and the director of marketing left the company to

If a foreign-currency-denominated payable has been hedged, why is it necessary to adjust the liability for balance sheet purposes?

What are some typical reasons for acquiring a forward exchange contract?

Differentiate between a spot rate and a closing rate.

Differentiate between a spot rate and a forward rate.

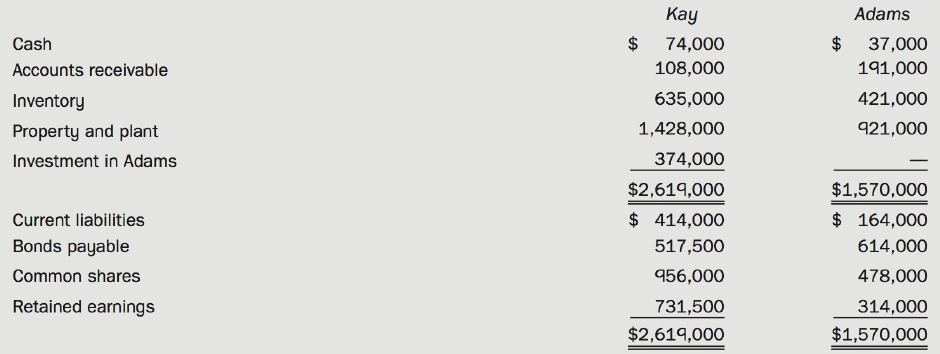

The following balance sheets have been prepared as at December 31, Year 6, for Kay Corp. and Adams Ventures:Additional Information:• Kay acquired its 40% interest in Adams for $374,000 in Year 2, when Adams's retained earnings amounted to $184,000. The acquisition differential on that date was

On January 1, Year 1, Amco Ltd. and Newstar Inc. formed Bearcat Resources, a joint venture. Newstar contributed miscellaneous assets with a fair value of $844,000 for a 65% interest in the venture. Amco contributed plant and equipment with a carrying amount of $319,000 and a fair value of

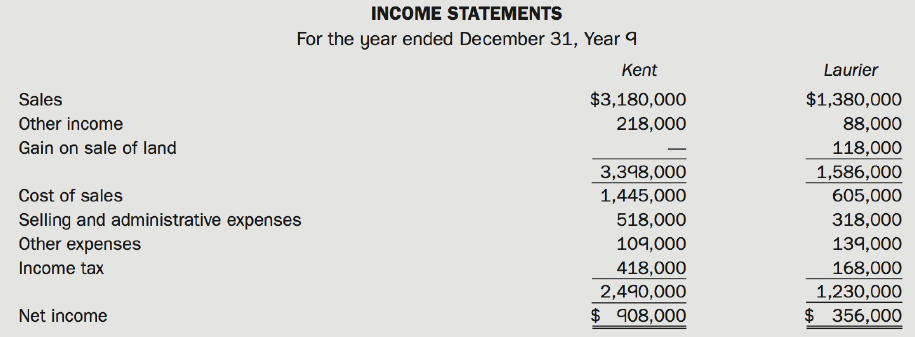

The following are the Year 9 income statements of Kent Corp. and Laurier Enterprises.Additional Information:• Kent acquired its 40% interest in the common shares of Laurier in Year 3 at a cost of $843,000 and uses the cost method to account for its investment for internal record keeping.• The

Access the 2014 consolidated financial statements for Rogers Communications Inc. by going to the investor relations section of the company's website. Answer the questions below. For each question, indicate where in the financial statements you found the answer, and/or provide a brief

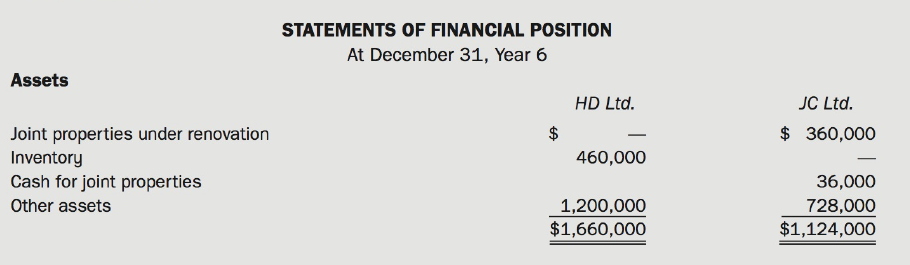

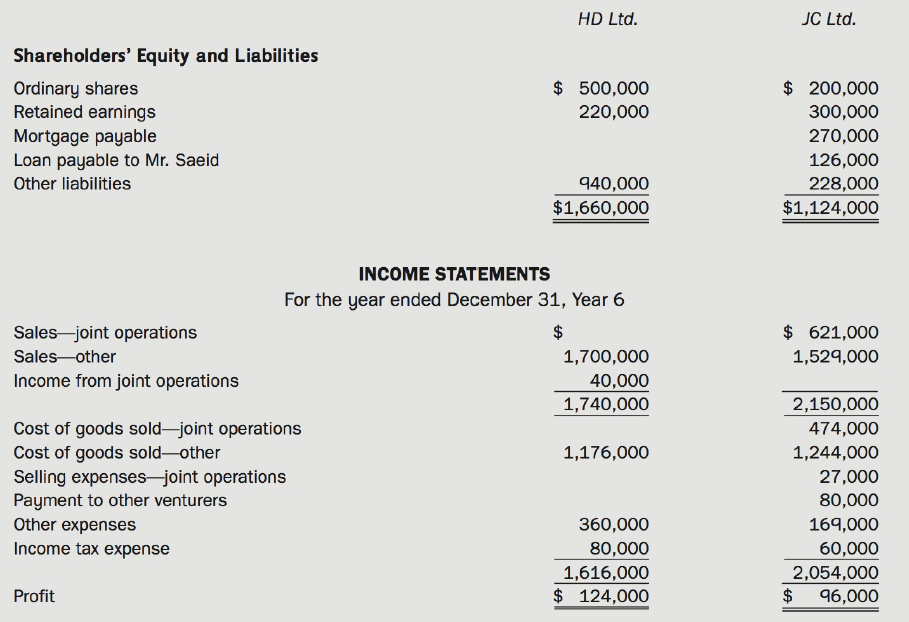

On January 1, Year 6, HD Ltd., a building supply company, JC Ltd., a construction company, and Mr. Saeid, a private investor, signed an agreement to carry out a joint operation under the following terms and conditions:• JC would buy and renovate homes on behalf of the three parties to the joint

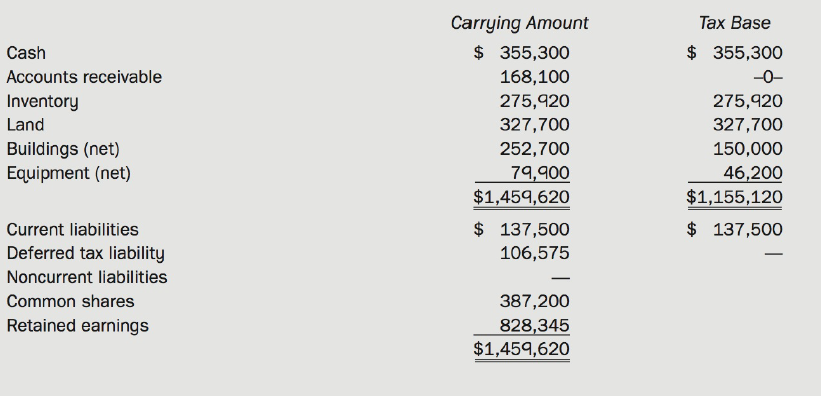

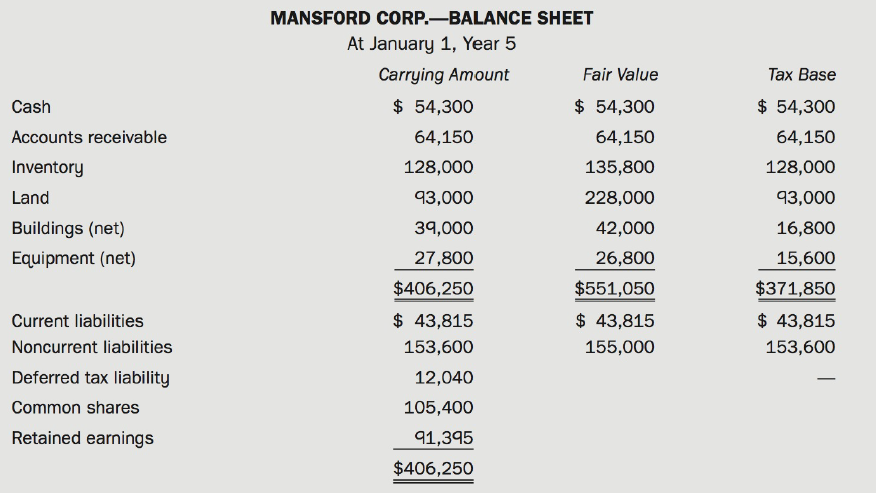

On January 1, Year 5, Green Inc. purchased 100% of the common shares of Mansford Corp. for $353,000. Green's balance sheet data on this date just prior to this acquisition were as follows:The balance sheet and other related data for Mansford are as follows:Additional Information:• As at January

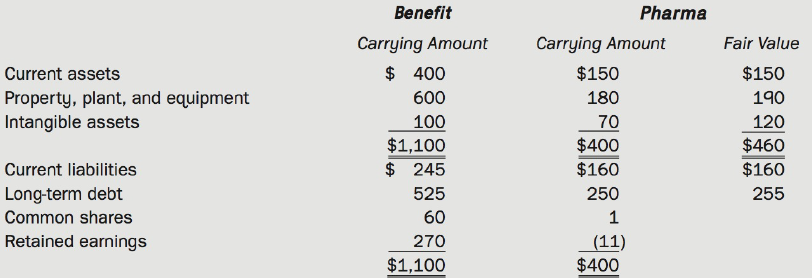

Pharma Company (Pharma) is a pharmaceutical company operating in Winnipeg. It is developing a new drug for treating multiple sclerosis (MS). On January 1, Year 3, Benefit Ltd. (Benefit) signed an agreement to guarantee the debt of Pharma and guarantee a specified rate of return to the common

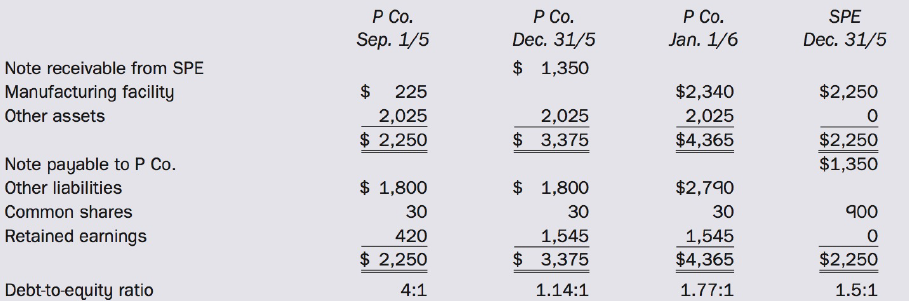

Prepare the memo requested by the CFO. Ignore income taxes.P Co. is looking for some additional financing in order to renovate one of the company's manufacturing plants. It is having difficulty getting new debt financing because its debt-to-equity ratio is higher than the 3:1 limit stated in its

(a) How should these two investments be reported on the financial statements of Holdco? Provide arguments to support your recommendations. (b) What impact will the adoption of the reporting methods suggested in part (a) have on Holdco's debt-to-equity ratio? Briefly explain.Mr. Landman has

Explain how the definitions of assets and liabilities can be used to support the consolidation of special-purpose entities.

Explain the similarities and differences between a subsidiary and a controlled special purpose entity and between a majority shareholder for a subsidiary and a sponsor for a controlled special-purpose entity.

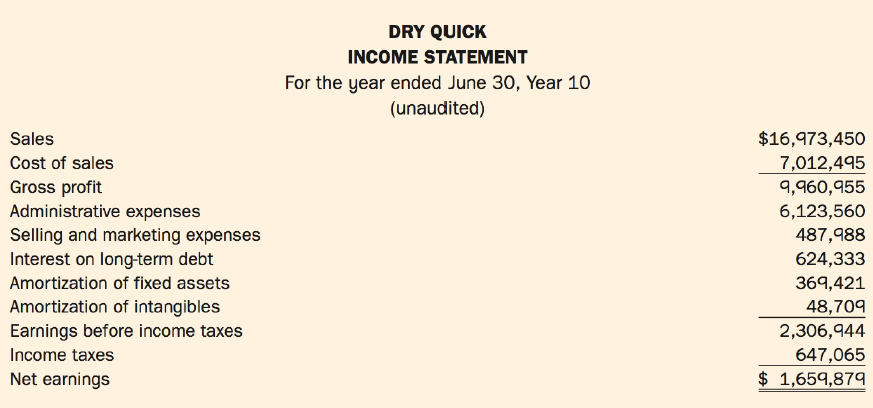

Dry Quick (DQ) is a medium-sized, private manufacturing company located near Timmins, Ontario. DQ has a June 30 year-end. Your firm, Poivre & Sel (P&S), has recently been appointed as auditors forDQ. It is now August 2, Year 10. You, CPA, have been asked to take on the senior role on

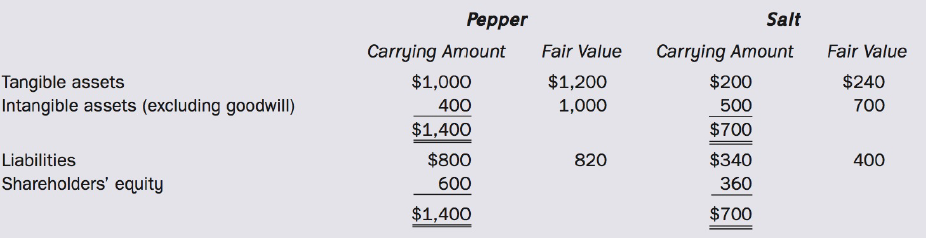

Prepare this presentation, answering the following questions:(a) How would Pepper's consolidated balance sheet differ at the date of acquisition under the two different valuation alternatives? Which method best reflects economic reality? Which method is required by GAAP?(b) How would Pepper's

Explain how the non-controlling interest in the net assets and net income of a subsidiary is calculated and reported when the parent owns 90% of the subsidiary's common shares and 30% of the subsidiary's cumulative preferred shares.

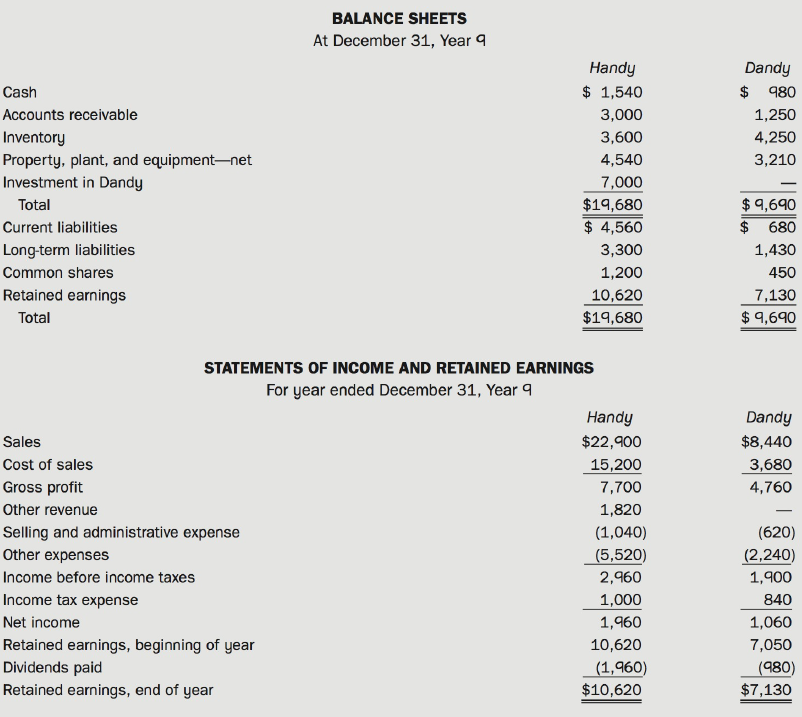

On January 1, Year 4, Handy Company (Handy) purchased 70% of the outstanding common shares of Dandy Limited (Dandy) for $13,300. On that date, Dandy's shareholders' equity consisted of common shares of $1,250 and retained earnings of $6,500.The financial statements for Handy and Dandy for Year 9

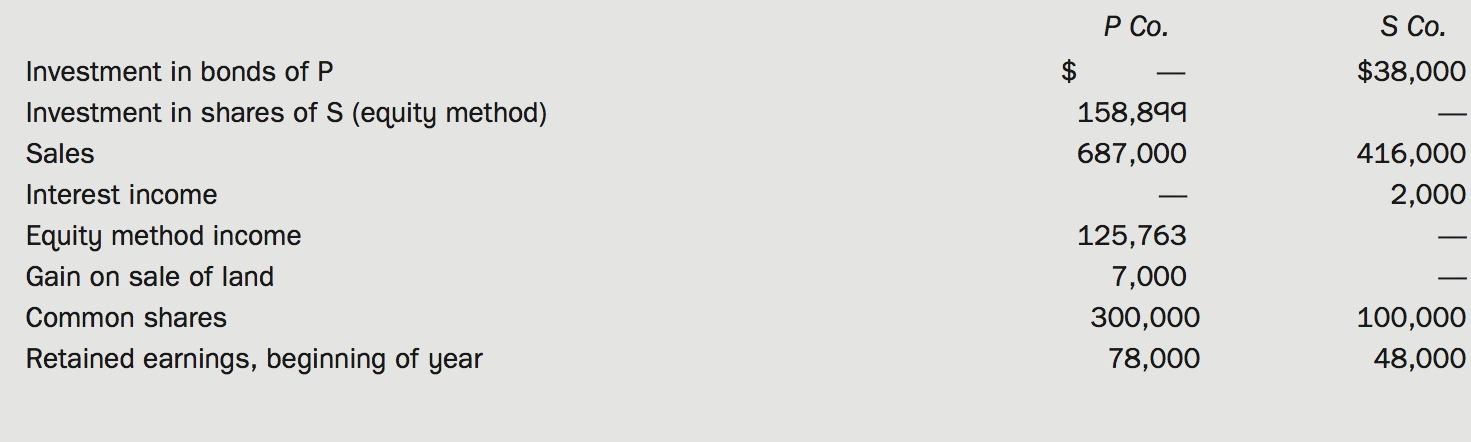

Shown below are selected ledger accounts from the trial balance of a parent and its subsidiary as of December 31, Year 10.Additional Information:• P Company purchased its 90% interest in S Company in Year 2, on the date that S Company was incorporated, and has followed the eq_uity method to

On December 31, Year 4, RAV Company purchased 60% of the outstanding common shares of ENS Company for $1,260,000. On that date, ENS had common shares of $500,000 and retained earnings of $130,000. In negotiating the purchase price, it was agreed that recorded assets and liabilities were fairly

Parent Co. owns 75% of Sub Co. and uses the cost method to account for its investment. The following are summarized income statements for the year ended December 31, Year 7.Additional Information:• On July 1, Year 7, Parent purchased all of the outstanding bonds of Sub for $381,250. On that date,

On January 1, Year 4, Goodkey Co. acquired all of the common shares of Jingya. The condensed income statements for the two companies for January Year 5, were as follows:The following transactions occurred in January, Year 5, and are properly reflected in the income statements above:• On January

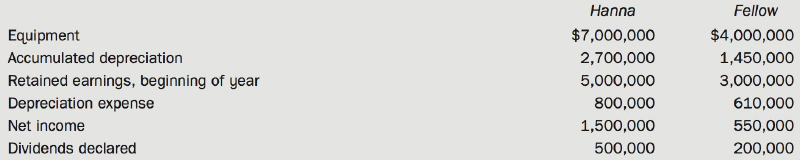

Hanna Corporation owns 80% of the outstanding voting stock of Fellow Inc. At the date of acquisition, Fellow's retained earnings were $2,100,000. On December 31, Year 2, Hanna Inc. sold equipment to Fellow at its fair value of $2,000,000 and recorded a gain of $500,000. The equipment had a

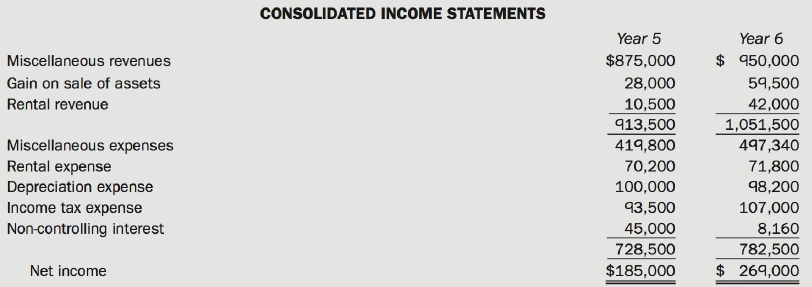

The comparative consolidated income statements of a parent and its 75%-owned subsidiary were prepared incorrectly as at December 31 and are shown in the following table. The following items were overlooked when the statements were prepared:• The Year 5 gain on sale of assets resulted from the

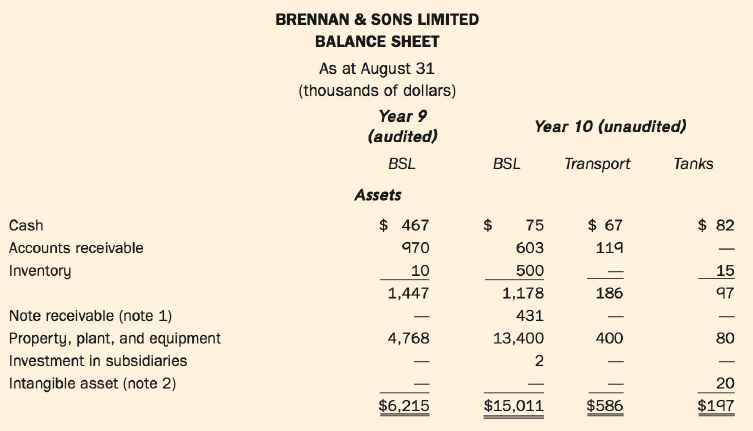

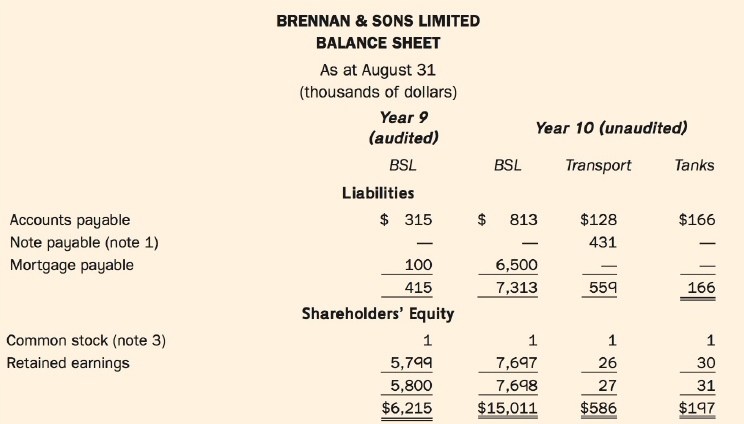

It is Monday, September 13, Year 10. You, CPA, work at Fife & Richardson LLP, a CPA firm. Ken Simpson, one of the partners, approaches you mid-morning regarding Brennan & Sons Limited (BSL), a private company client for which you performed the August 31, Year 9, year-end audit. "It

Stephanie Baker is an audit senior with the public accounting firm of Wilson & Lang. It is February Year 9, and the audit of Canadian Development Limited (CDL) for the year ended December 31, Year 8, is proceeding. Stephanie has identified several transactions that occurred in the Year 8 fiscal

Why does an intercompany sale of a depreciable asset (such as equipment or a building) require subsequent adjustments to depreciation expense within the consolidation process?

An intercompany gain on a depreciable asset resulting from a sale by the parent company is subsequently realized by an adjustment to the subsidiary's depreciation expense in the preparation of consolidated income statements. Should this adjustment be taken into account in the calculation of net

(a) Show the allocation of the acquisition cost at acquisition and the related amortization schedule. Show and label all calculations.(b) Prepare a consolidated income statement with expenses classified by function. (c) Calculate consolidated retained earnings at December 31, Year 11.(d)

(a) Prepare the following consolidated financial statements for Year 6:(i) Income statement(ii) Statement of financial position(b) Calculate goodwill impairment loss and profit attributable to non-controlling interest for the year ended December 31, Year 6, under parent company extension

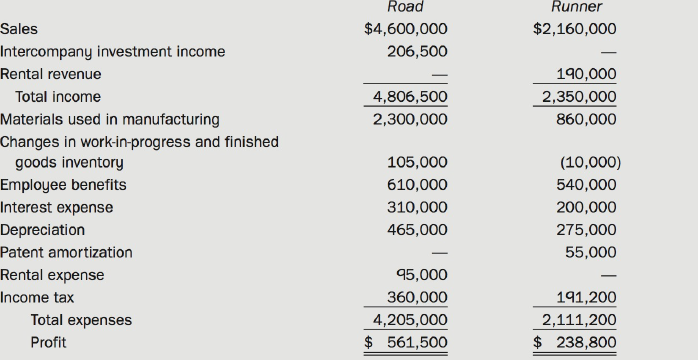

(a) Prepare a consolidated income statement for Year 9 with expenses classified by nature.(b) Calculate consolidated retained earnings at December 31, Year 9.(c) If Road had used parent company extension theory rather than entity theory, how would this affect the return on equity attributable to

(a) Assume that all intercompany sales were upstream. Calculate the amount to be reported on the Year 7 consolidated financial statements for the following accounts/items:(i) Consolidated net income(ii) Consolidated net income attributable to the controlling and non-controlling interest (iii)

(a) Prepare income statements for January and February for Fazli, Gervais, and Consolidation. Break down cost of sales into its three components.(b) Now assume that Fazli uses the equity method to account for its investment in Gervais. What accounts would change on the three statements in January

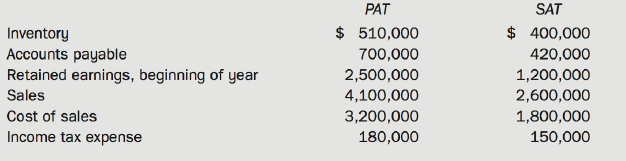

On January 1, Year 2, PAT Ltd. acquired 90% of SAT Inc. when SAT's retained earnings were $1,000,000. There was no acquisition differential. PAT accounts for its investment under the cost method. SAT sells inventory to PAT on a regular basis at a markup of 30% of selling price. The intercompany

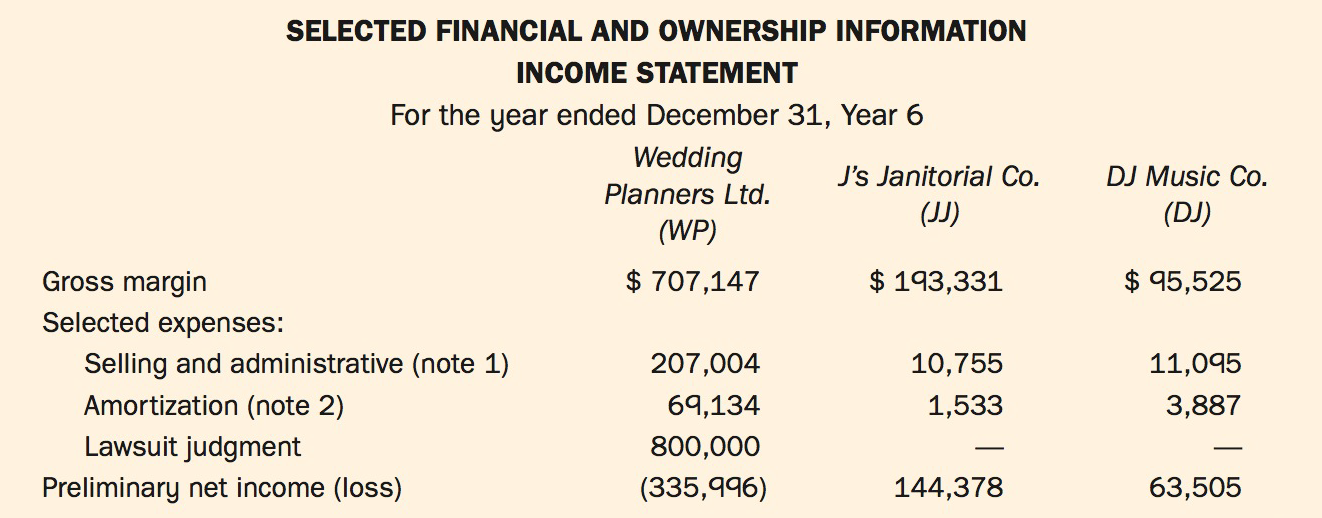

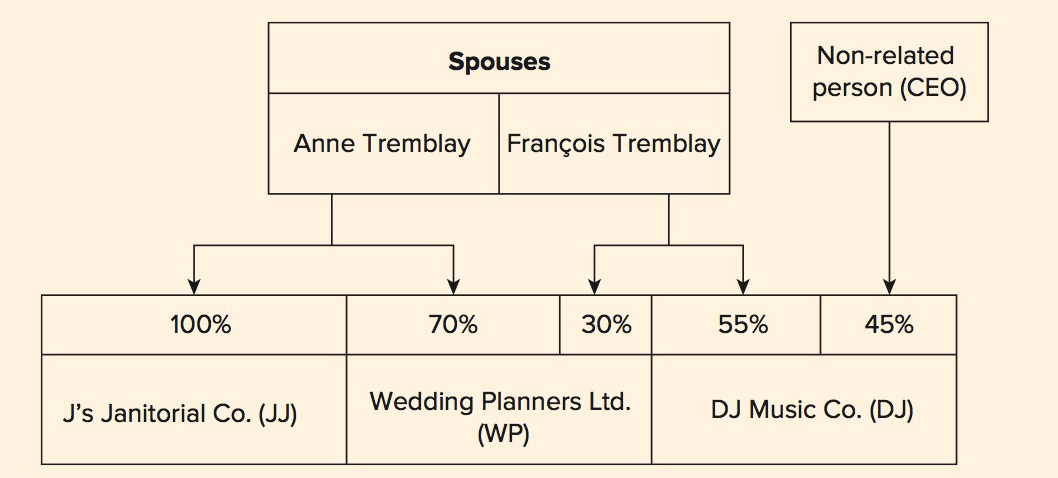

Wedding Planners Limited (WP), owned by Anne and Francois Tremblay, provides wedding planning and related services. WP owns a building (the Pavilion) that has been custom-made for hosting weddings. Usually, WP plans a wedding from start to finish and hosts the wedding day events photos, ceremony,

You, the CPA, an audit senior at Grey & Co., Chartered Professional Accountants, are in charge of this year's audit of Plex-Fame Corporation (PFC). PFC is a rapidly expanding, diversified, and publicly owned entertainment company with operations throughout Canada and the United States. PFC's

Good Quality Auto Parts Limited (GQ) is a medium-sized, privately owned producer of auto parts, which are sold to car manufacturers, repair shops, and retail outlets. In March Year 10, the union negotiated a new three-year contract with the company for the 200 shop-floor employees. At the time, GQ

Describe the journal entry on the parent's books under the equity method to adjust for unrealized profits in ending inventory for upstream transactions.

If an intercompany profit is recorded on the sale of an asset to an affiliate within the consolidated entity in Period 1, when should this profit be considered realized? Explain.

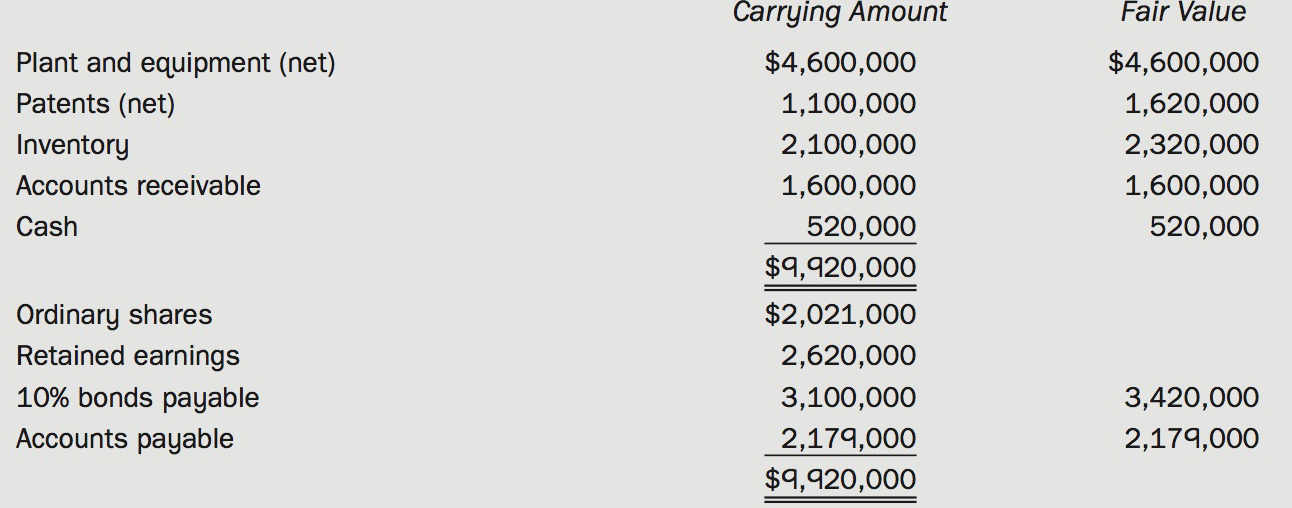

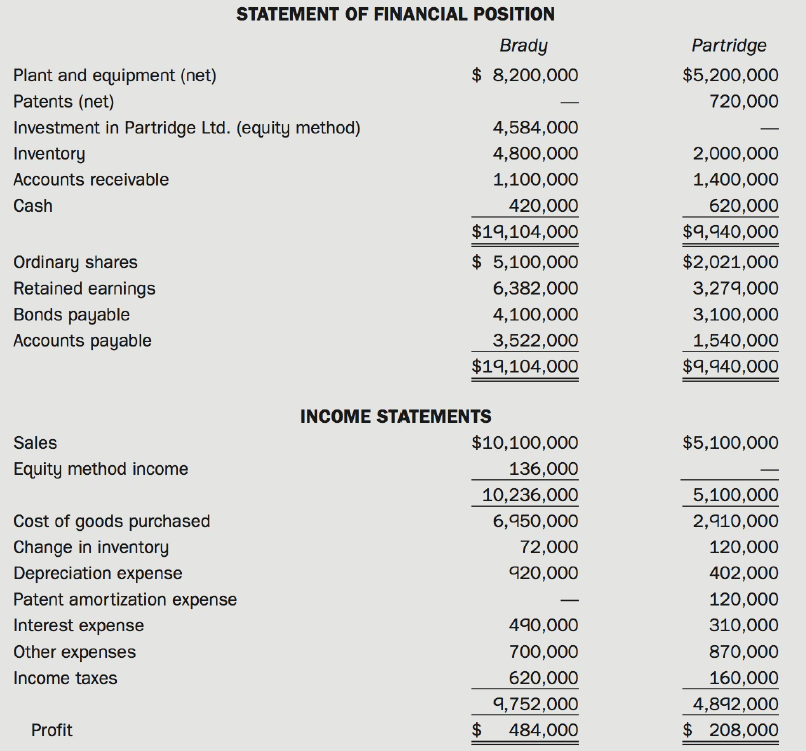

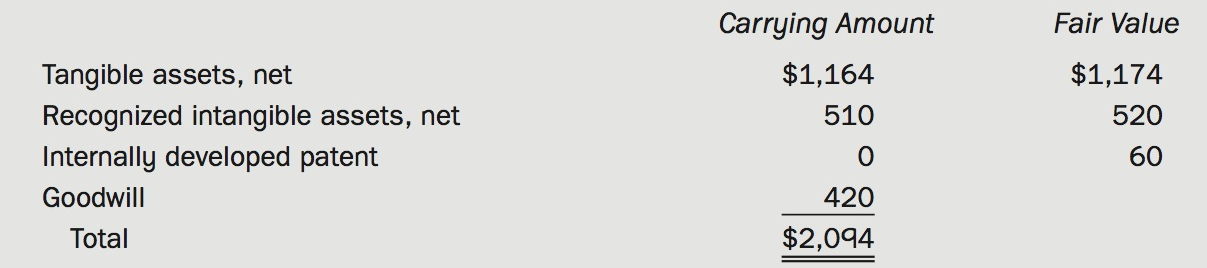

On January 2, Year 4, Brady Ltd. purchased 80% of the outstanding shares of Partridge Ltd. for $4,320,000. Partridge's statement of financial position and the fair values of its identifiable assets and liabilities for that date were as follows:The patents had a remaining useful life of ten years on

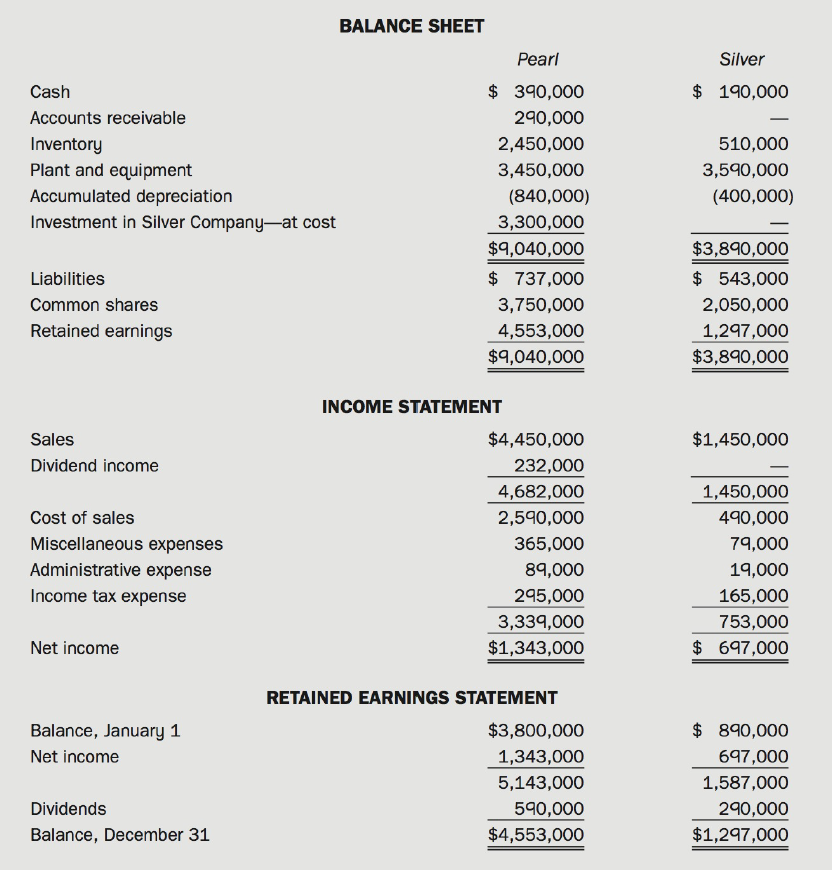

The following financial statements were prepared on December 31, Year 6.Additional Information:Pearl purchased 80% of the outstanding voting shares of Silver for $3,300,000 on July 1, Year 2, at which time Silver's retained earnings were $445,000, and accumulated depreciation was $69,000. The

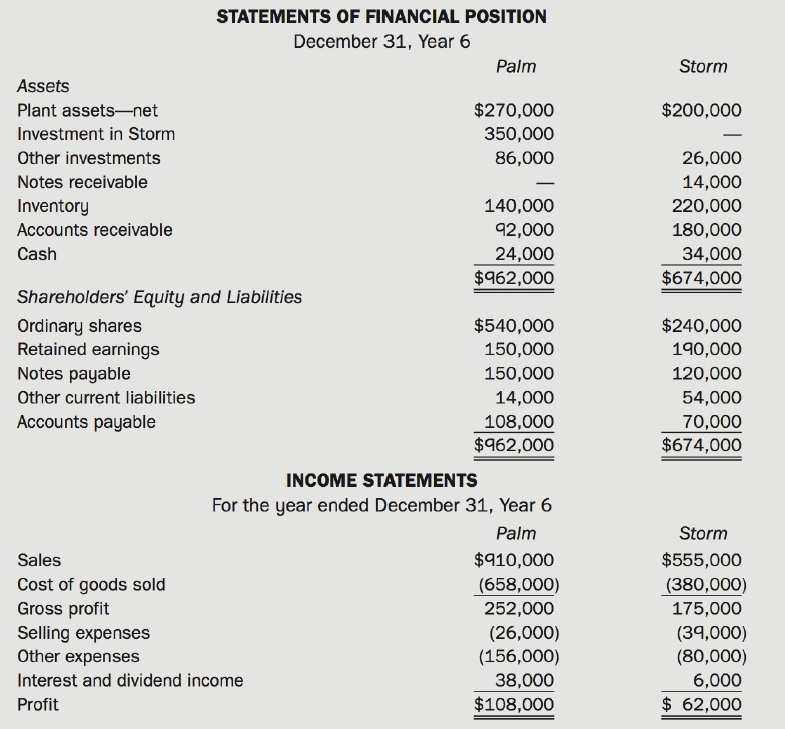

On December 31, Year 2, Palm Inc. purchased 80% of the outstanding ordinary shares of Storm Company for $350,000. At that date, Storm had ordinary shares of $240,000 and retained earnings of $64,000. In negotiating the purchase price, it was agreed that the assets on Storm's statement of financial

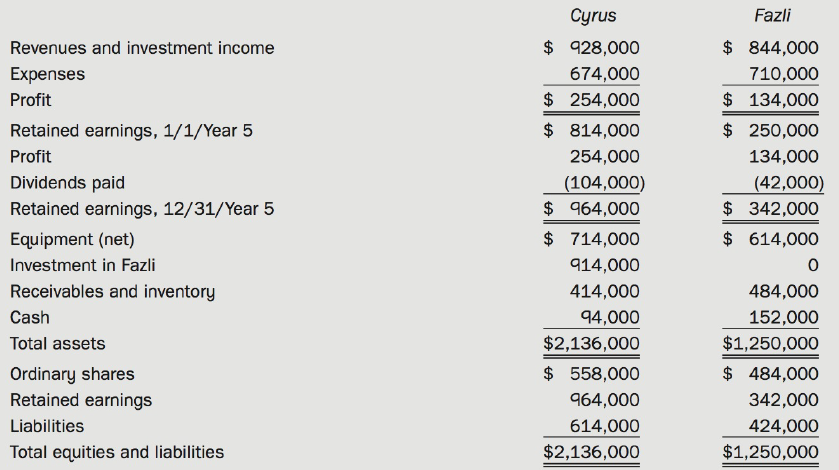

On January 1, Year 4, Cyrus Inc. paid $914,000 in cash to acquire all of the ordinary shares of Fazli Company. On that date, Fazli's retained earnings were $200,000. All of Fazli's assets and liabilities had fair values equal to carrying amounts except for equipment, which was worth $50,000 more

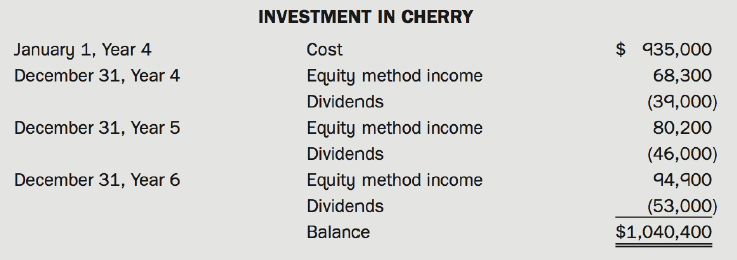

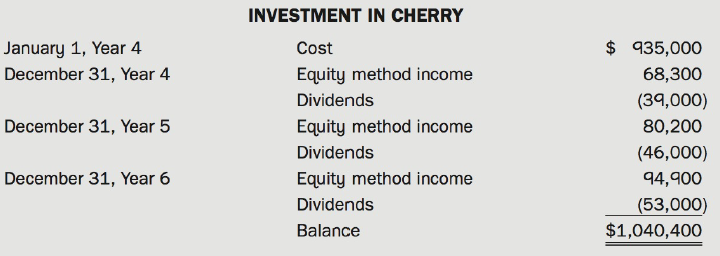

Peach Ltd. acquired 80% of the common shares of Cherry Company on January 1, Year 4. On that date, Cherry had common shares of $710,000 and retained earnings of $410,000.The following is a summary of the changes in Peach's investment account from January 1, Year 4, to December 31, Year 6:Additional

Large Ltd. purchased 70% of Small Company on January 1, Year 6, for $770,000, when the statement of financial position for Small showed common shares of $560,000 and retained earnings of $260,000. On that date, the inventory of Small was undervalued by $71,000, and a patent with an estimated

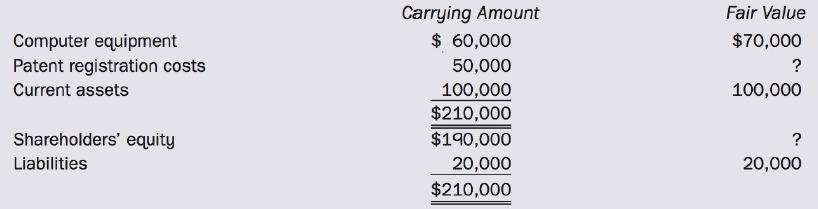

The following information is available for the assets of Saman Ltd. at December 31, Year 5:(The following 3 parts are independent situations.)Part A. Assume that the total fair value for all of Saman's assets as a group is $1,860.(a) Calculate the total impairment loss for Year 5.(b) After

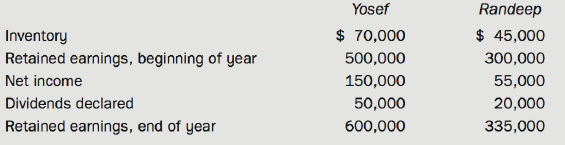

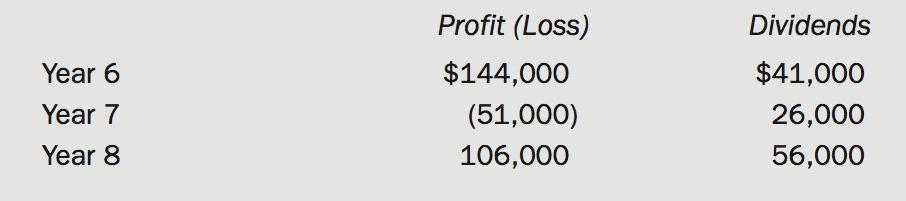

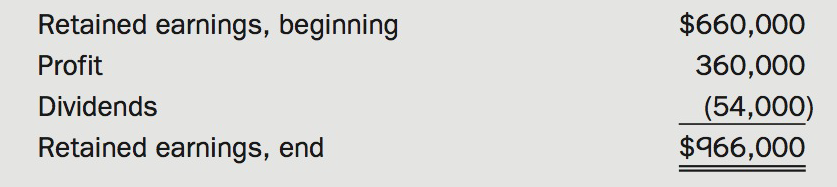

Calculate the following:(a) The amount of dividends declared by Cherry in Year 4(b) The reported profit of Cherry for Year 5(c) The amount for non-controlling interest that would appear in the Year 6 consolidated income statement and statement of financial position(d) The amount of goodwill that

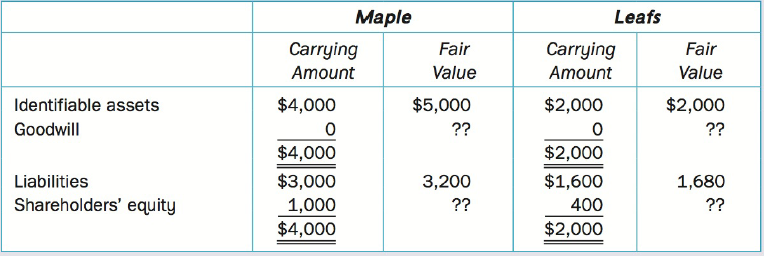

Prepare a consolidated balance sheet at the date of acquisition under the three theories, and respond to the questions asked by management.On December 31, Year 7, Maple Company issued preferred shares with a fair value of $1,200,000 to acq_uire 24,000 (60%) of the common shares of Leafs Limited.

How would the consolidation of a parent-founded subsidiary differ from the consolidation of a purchased subsidiary?

What is negative goodwill, and how is it accounted for?

Explain how changes in the fair value of contingent consideration should be reported, assuming that the contingent consideration will be paid in the form of cash.

What is non-controlling interest, and where is it reported in the consolidated balance sheet under the parent company extension and entity theories?

With respect to the valuation of non-controlling interest, what are the major differences among proprietary, parent company extension, and entity theories?

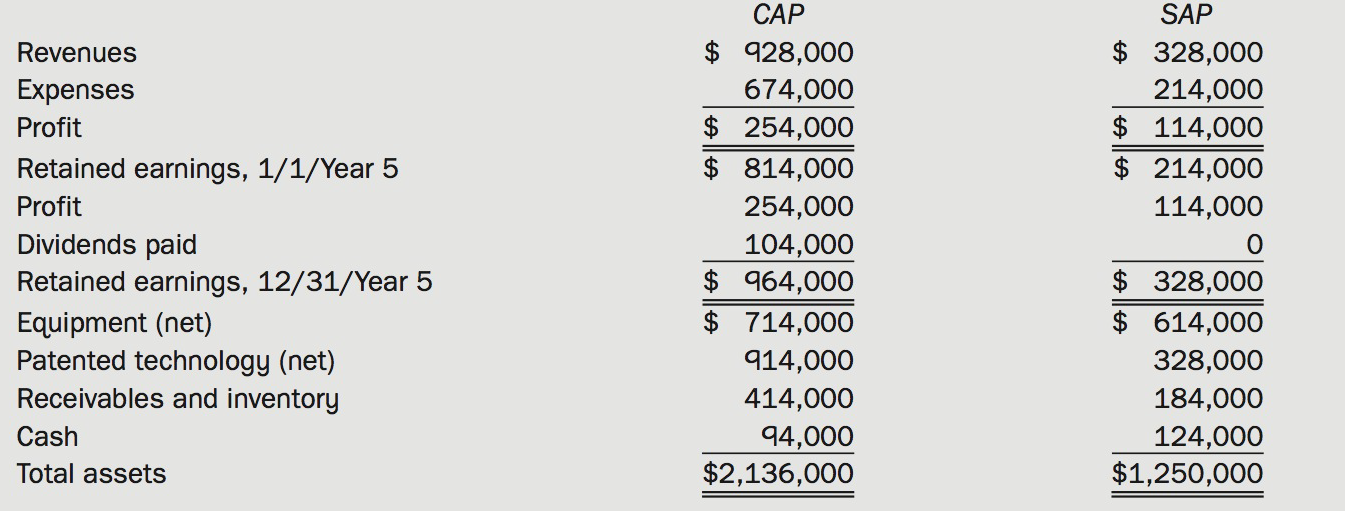

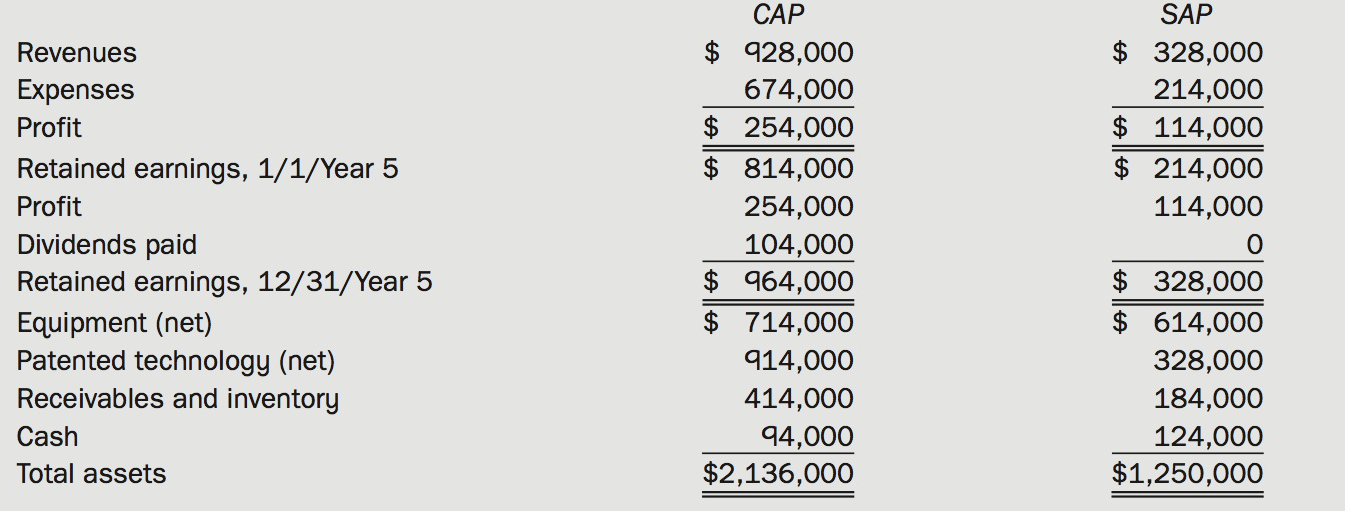

The financial statements for CAP Inc. and SAP Company for the year ended December 31, Year 5, follow:On December 31, Year 5, after the above figures were prepared, CAP issued $314,000 in debt and 12,400 new shares to the owners of SAP to purchase all of the outstanding shares of that company. CAP

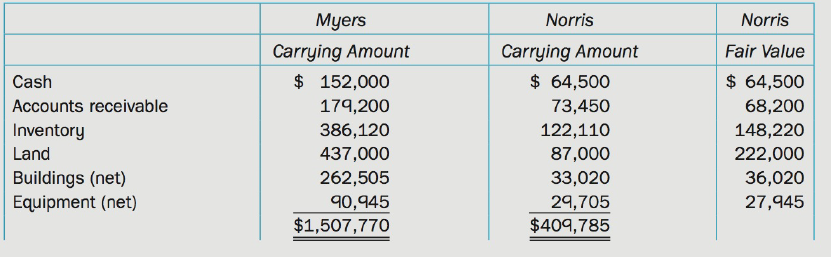

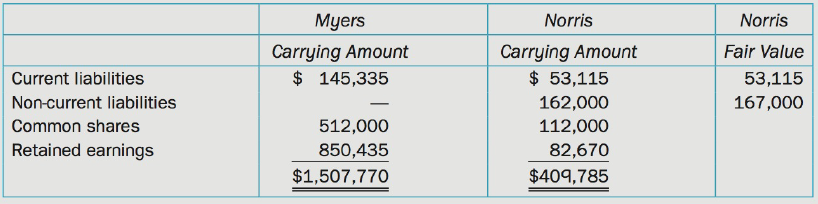

Refer to Problem 11. All of the facts and data are the same except that in the proposed takeover, Myers Company will purchase all of the outstanding common shares of Norris Inc.Data from problem 11:Myers Company Ltd. was formed 10 years ago by the issuance of 34,000 common shares to three

Myers Company Ltd. was formed 10 years ago by the issuance of 34,000 common shares to three shareholders. Four years later, the company went public and issued an additional 30,000 common shares.The management of Myers is considering a takeover in which Myers would purchase all of the assets and

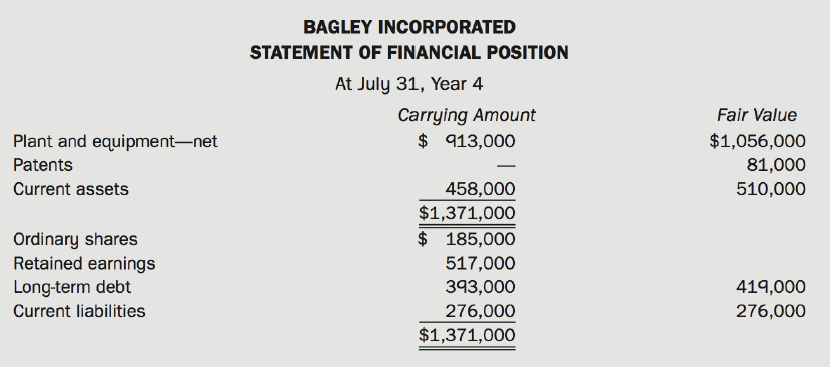

The statement of financial position of Bagley Incorporated as at July 31, Year 4, is as follows:On August 1, Year 4, the directors of Bagley considered a takeover offer from Davis Inc., whereby the corporation would sell all of its assets and liabilities. Davis's costs of investigation and drawing

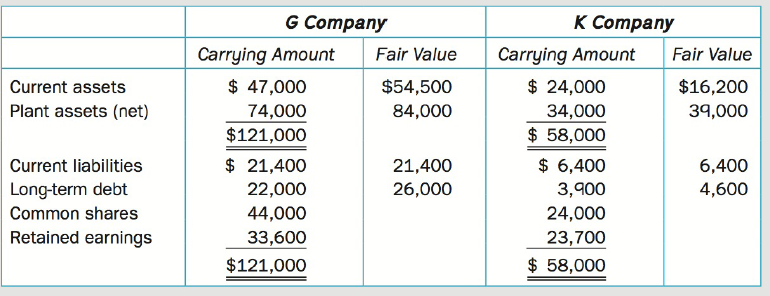

G Company is considering the takeover of K Company whereby it will issue 7,400 common shares for all of the outstanding shares of K Company. K Company will become a wholly owned subsidiary of G Company. Prior to the acquisition, G Company had 13,000 shares outstanding, which were trading at $8.00

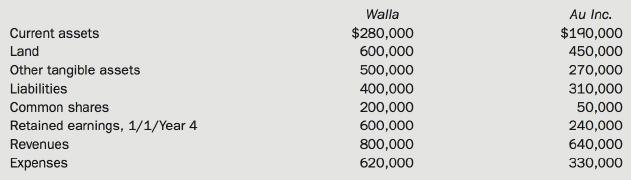

The trial balances for Walla Corporation and Au Inc. at December 31, Year 4, just before the transaction described below, were as follows:On December 31, Year 4, Walla purchased all of the outstanding shares of Au Inc. by issuing 20,000 common shares with a market value of $36 per share. The

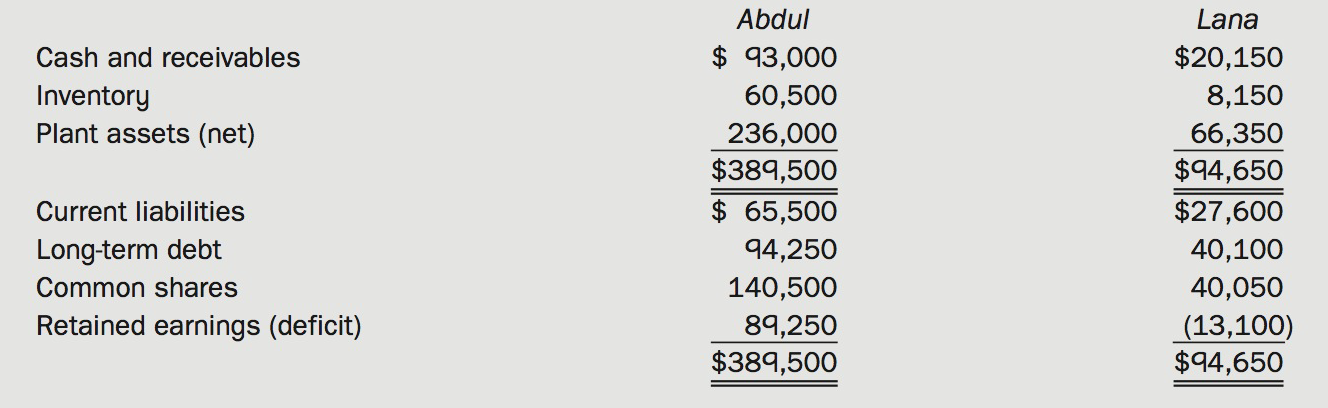

The balance sheets of Abdul Co. and Lana Co. on June 30, Year 2, just before the transaction described below, were as follows:On June 30, Year 2, Abdul Co. purchased all of Lana Co. assets and assumed all of Lana Co. liabilities for $58,000 in cash. The carrying amounts of Lana's net assets were

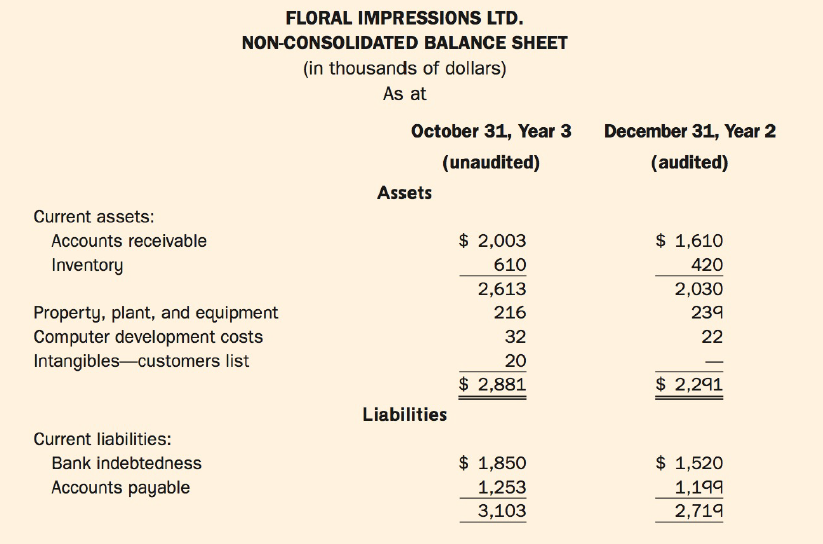

You, CPA, are employed at Beaulieu & Beauregard, Chartered Professional Accountants. On November 20, Year 3, Dominic Jones, a partner in your firm, sends you the following email:Our firm has been reappointed auditors of Floral Impressions Ltd. (FIL) for the year ending December 31, Year 3. I

Prepare the presentation slides and related speaker's notes for the presentation. Limit your presentation to five slides. Your presentation should provide recommendations related to the issues raised by Arthur. Use financial statement concepts to support your recommendations. Provide a detailed

Can a statutory amalgamation be considered a form of business combination? Explain.

What key element must be present in a business combination?

Right Company purchased 25,000 common shares (25%) of ON Inc. on January 1, Year 11, for $250,000. Right uses the equity method to report its investment in ON because it has significant influence in the operating and investing decisions made by ON. Right has no legal obligation to pay any of ON's

On January 1, Year 2, Grow Corp. paid $200,000 to purchase 20,000 common shares of UP Inc., which represented an 8% interest in UP. On December 27, Year 2, UP declared and paid a dividend of $0.50 per common share. During Year 2, UP reported net income of $400,000. On December 31, Year 2, the

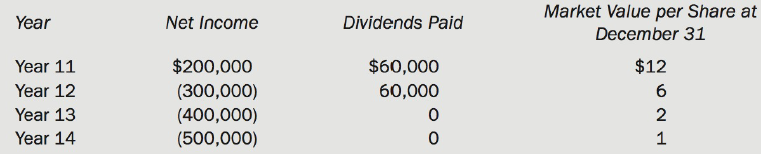

Her Company purchased 22,000 common shares (20%) of Him Inc. on January 1, Year 4, for $374,000. Additional information on Him for the three years ending December 31, Year 6, is as follows:On December 31, Year 6, Her sold its investment in Him for $506,000.(a) Compute the balance in the investment

Pender Corp. paid $285,000 for a 30% interest in Saltspring Limited on January 1, Year 6. During Year 6, Saltspring paid dividends of $110,000 and reported profit as follows: Profit before discontinued operations.....................................$339,000Discontinued operations loss (net of

(a) Assume that Blake is a public company and the number of shares held by Blake is enough to give it significant influence over Stergis. Prepare all the journal entries that Blake should make regarding this investment in Year 5 and Year 6. Also, state the disclosure requirements for Year 6

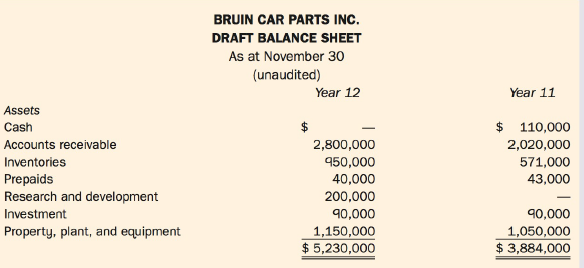

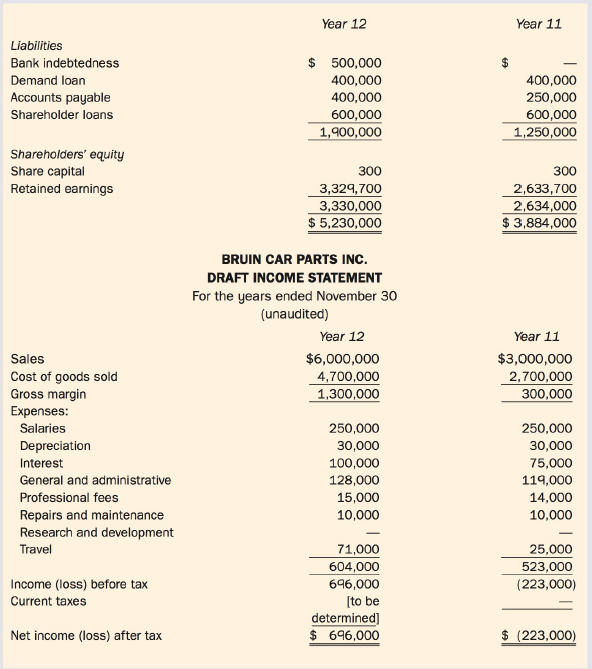

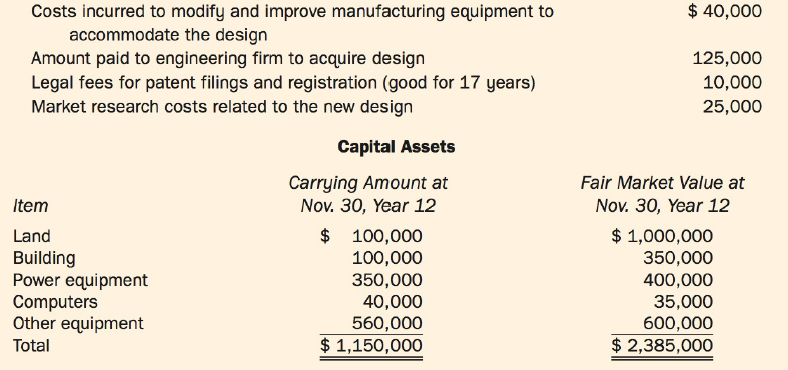

It is January 20, Year 13. Mr. Neely, a partner in your office, wants to see you, CPA, about Bruin Car Parts Inc. (BCP), a client req_uiring assistance. BCP prepares its financial statements in accordance with ASPE. Richard (Rick) Bergeron, Lyle Chara, and Jean Perron each own 100 common shares of

Ashton Inc. acquired a 40% interest in Villa Corp. for $200,000. In the first year after acquisition, Villa reported a loss of $700,000. Using the equity method, how should Ashton account for this loss assuming (a) Ashton has guaranteed the liabilities of Villa and (b) Ashton has not

Distinguish between the financial reporting for FVTPL investments and that for investments in associates.

Briefly describe the trend in reporting of investments in equity securities over the past 12 years.

When writing the final case report, how much attention, if any, should be given to discussing alternatives?

Identify the main factors to be used when ranking the importance of issues to be resolved.

Explain the difference between report recipient and primary users as they are described in the framework for analyzing a case and which users should be given priority in financial reporting.

List the six steps of the case framework.

In Year 1, XZY Co. expensed all development costs as incurred. How would the current ratio, debt-to-equity ratio and return on eq_uity change if XZY Co. had capitalized the development costs?

Identify the financial statement ratios typically used to assess profitability, liquidity and solvency, respectively.

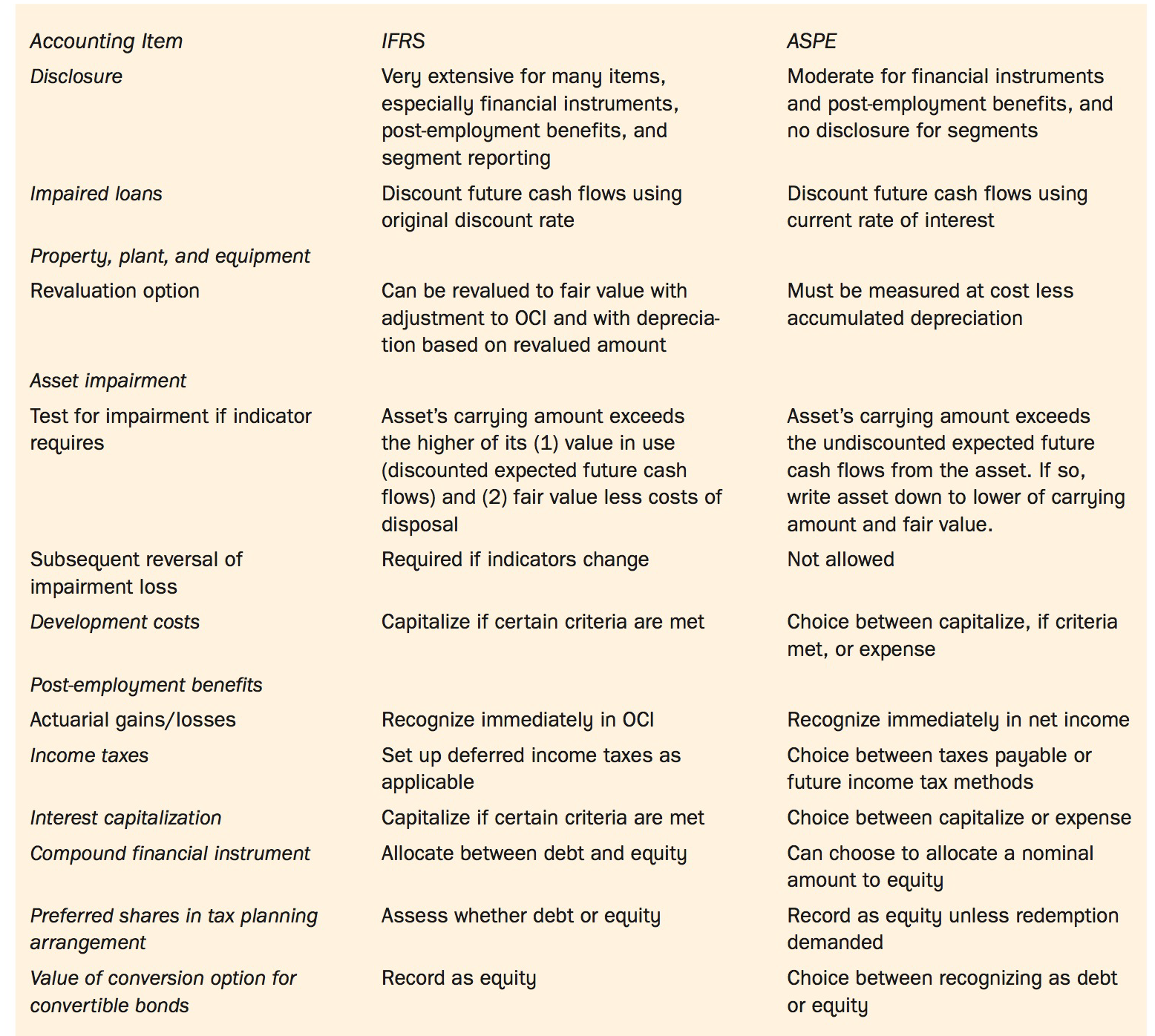

For the items listed in Exhibit 1.1, for which items would the debt-to-equity ratio not change when a company switched from ASPE to IFRS?Exhibit 1.1:Some key different between IFRS and ASPE Accounting Item IFRS ASPE Very extensive for many items, especially financial instruments, post-employment

Identify some of the financial statement items for which ASPE is different from IFRS.

Briefly explain why a Canadian private company may decide to follow IFRS even though it could follow ASPE.

Briefly explain why the Canadian AcSB decided to create a separate section of the CPA Canada Handbook for private enterprises.

Explain whether the needs of external users or management should take precedence in GAAP-based financial statements.

Identify three main areas where judgment needs to be applied when preparing financial statements.

Prepare a schedule to convert net income and total shareholders' equity from the preliminary financial statements amounts to amounts under ASPE and IFRS. Where accounting choices exist, choose policies that minimize return on total shareholders' equity under ASPE and maximize return on total

Showing 5000 - 5100

of 5104

First

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

Step by Step Answers